💸 A Family-Owned REIT Yielding 5%!

A Guest Post From Compounding Dividends

Today, I’m excited to share an excellent guest post from my friend TJ at Compounding Dividends.

You can learn plenty from his writings, and his thoughts and beliefs on dividend investing closely align with mine!

I enjoy following his work on Substack and X.

Enjoy the below writing from Compounding Dividends!

- Dividendology

Argan SA is a specialized French property company that develops and leases out Premium logistics warehouses.

The investment case comes down to three simple things:

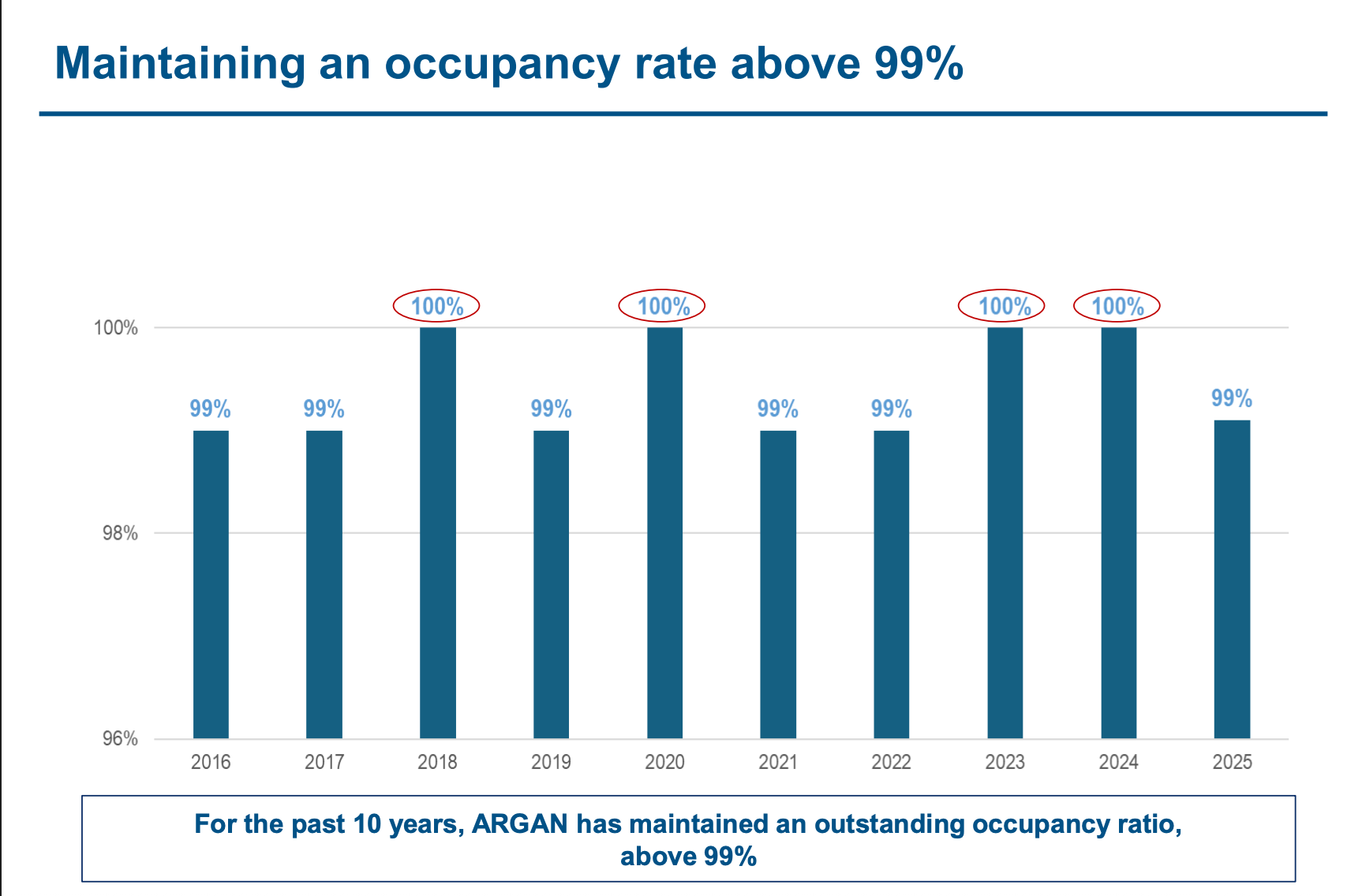

Necessary Assets: Companies like Amazon and Carrefour can’t easily move out of custom-built, robotic-heavy warehouses that produce their own renewable energy. That’s why Argan’s occupancy rate is above 99%.

Inflation Protection: Every lease is indexed to inflation, and their “AutOnom” warehouses protect tenants from rising energy costs.

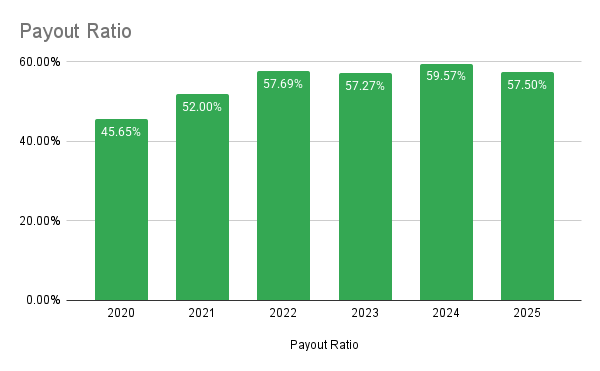

Safe Yield: You are getting a starting yield of 4.7%, which is well above the historical average, backed by a family management team that owns nearly 38% of the company. With a payout ratio of just 57.5%, the dividend looks safe now, with plenty of room to grow

Company name: Argan SA

✍️ ISIN: FR0010481960

🔎 Ticker: $ARG

📚 Type: High Yield Stock

📈 Stock Price: €69.80

💵 Market cap: €1.79 Billion

📊 Average daily volume: €1.5 million

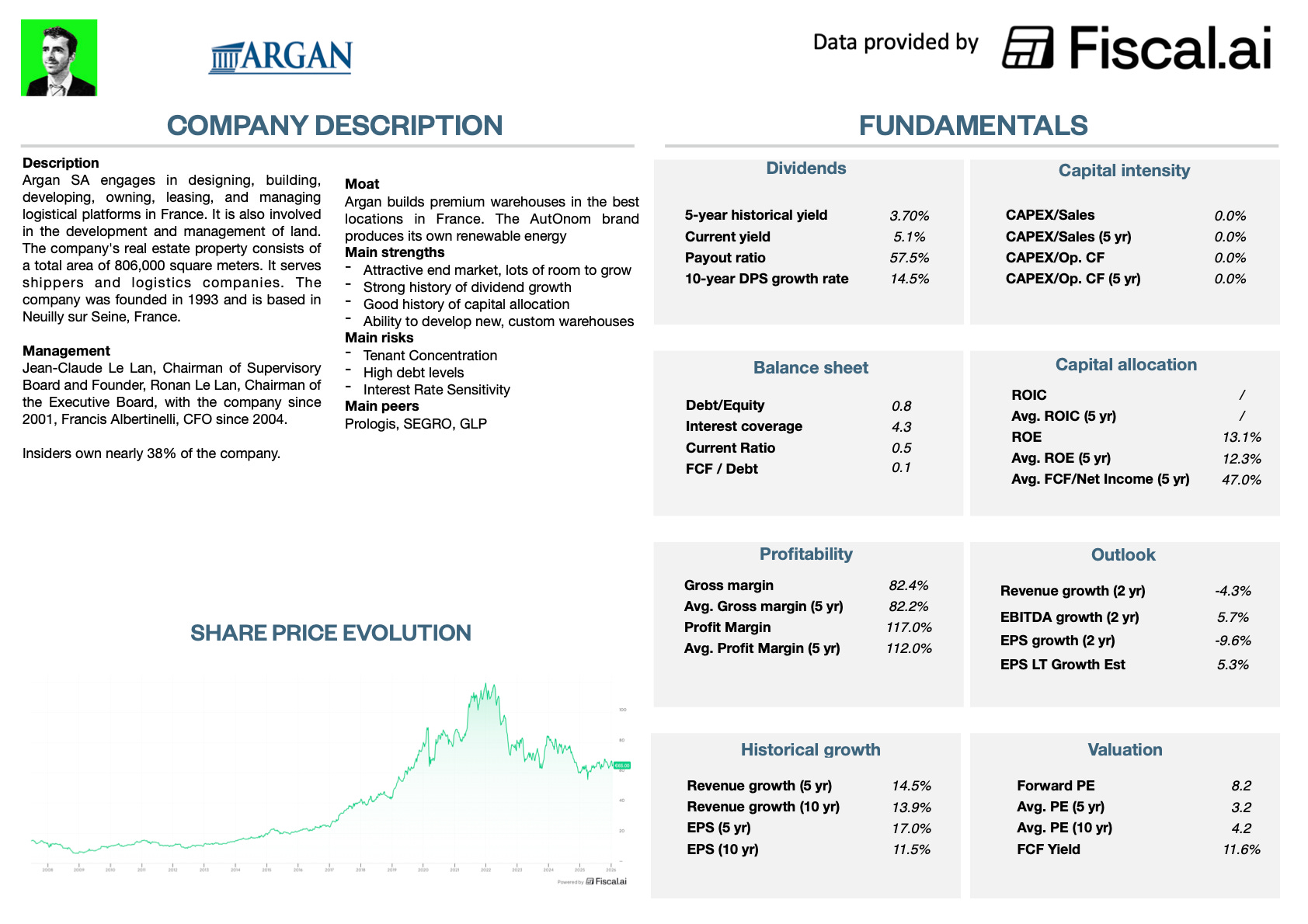

Onepager

Don’t know Argan SA?

Here are the basics (click on the picture to expand):

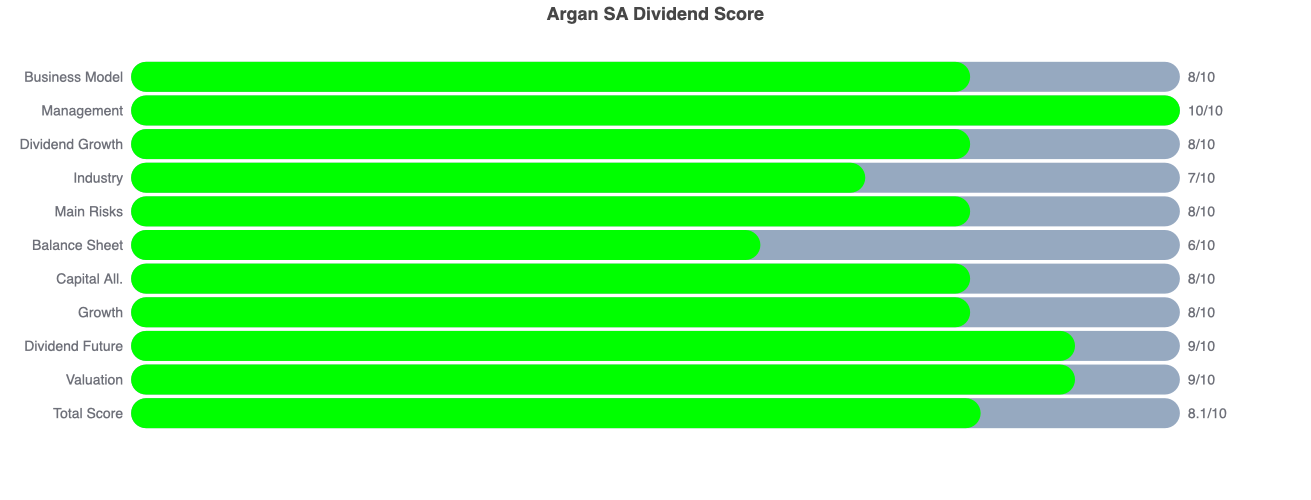

Dividend Score

Argan receives a Dividend Score of 8.1/10.

Now let’s dive into the full investment case!

1. Do I understand the business model?

Argan is a developer-landlord.

Unlike many REITs that just buy existing buildings, Argan identifies strategic land in France, builds a high-tech warehouse (often custom-designed for a specific client), and then keeps it in their portfolio forever.

They focus on the Premium segment - warehouses that are large, modern, and in the best locations.

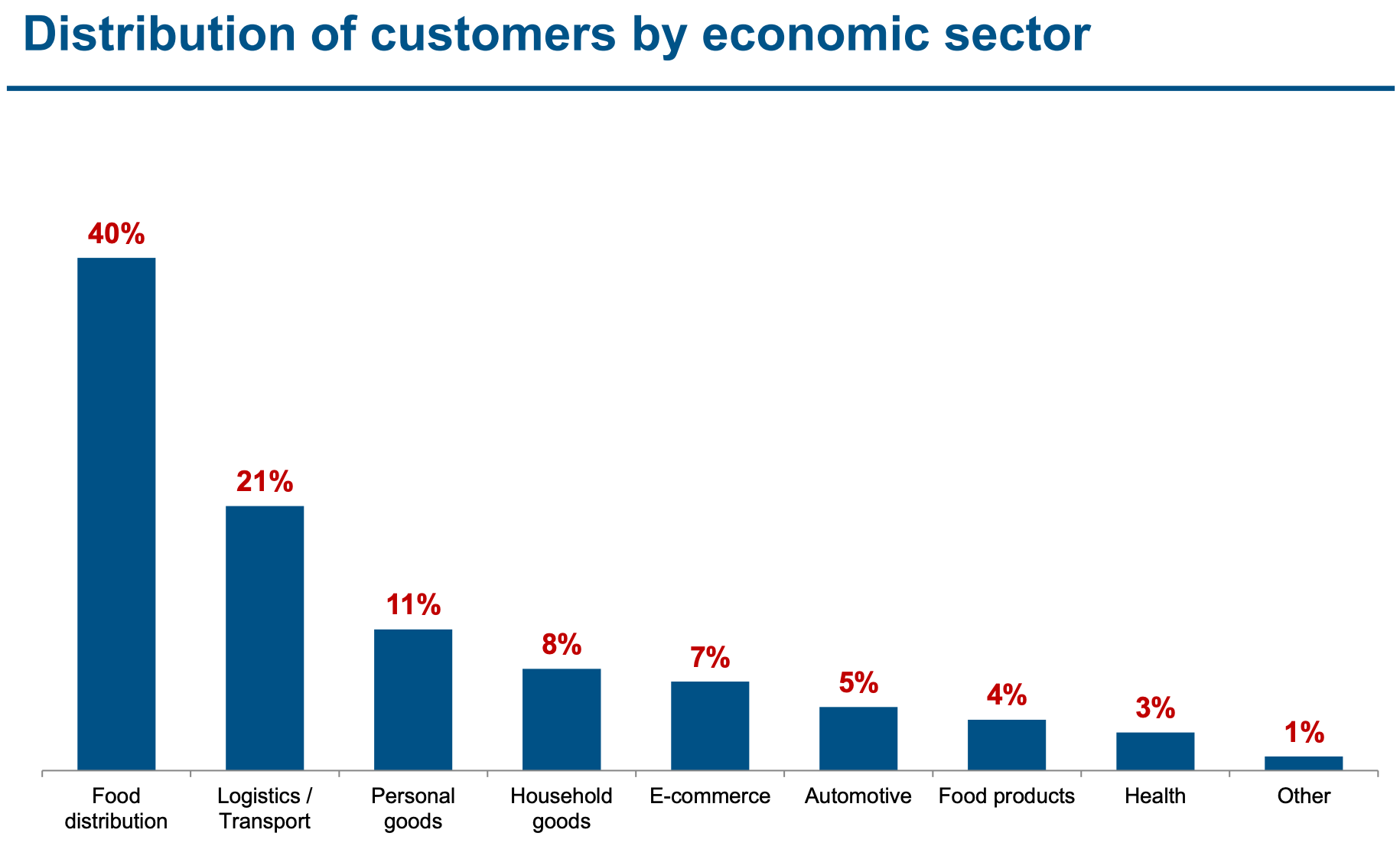

Revenue Split

Argan makes 100% of its money from renting its warehouses.

Most of Argan SA’s customers are in the food distribution sector.

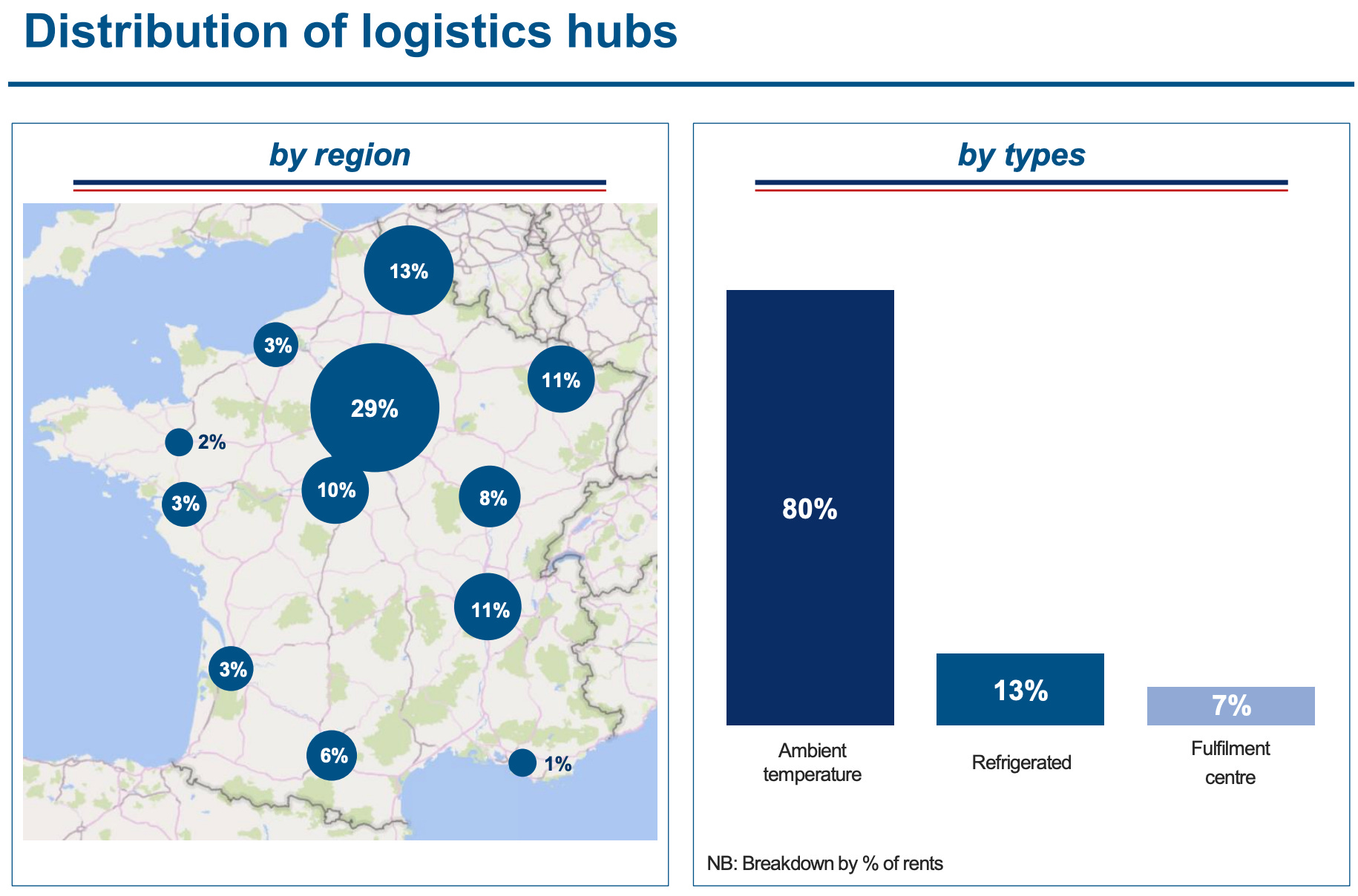

Geographic Split

Argan is 100% concentrated in France.

80% of its warehouses are ambient temperature.

13% of their warehouses are refrigerated and 7% are fulfillment centers.

Who are the customers?

Argan leases to massive companies that need reliable, high-tech distribution hubs.

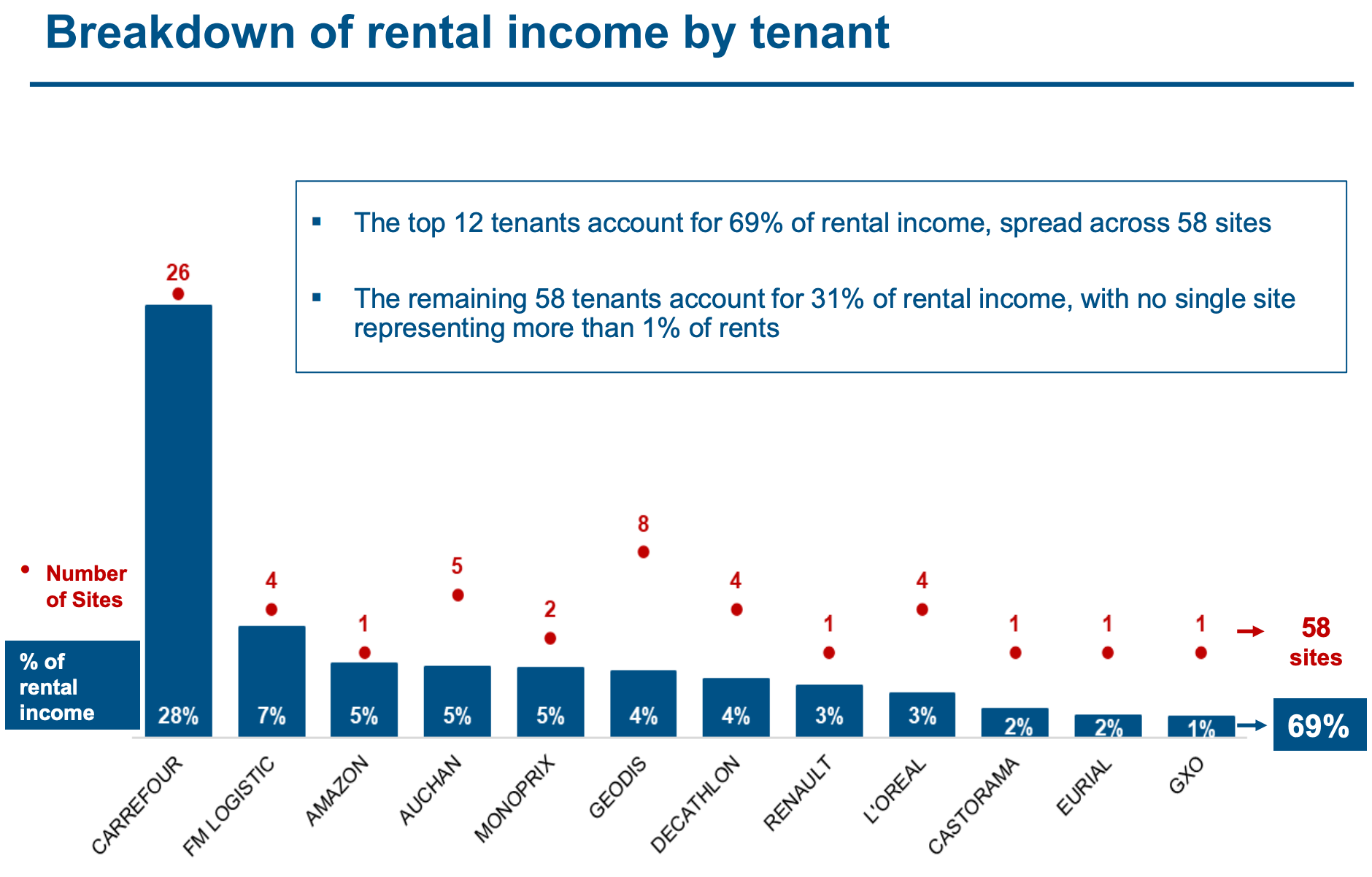

The tenant list is a “Who’s Who” of European business:

Carrefour: Their largest tenant, making up 28% of rent.

Blue Chips: Amazon, L’Oréal, DHL, Decathlon, and Coca-Cola.

Because these companies are so large and financially stable, Argan almost never has to worry about a tenant failing to pay rent.

What’s the moat?

Argan SA specializes in premium warehouses.

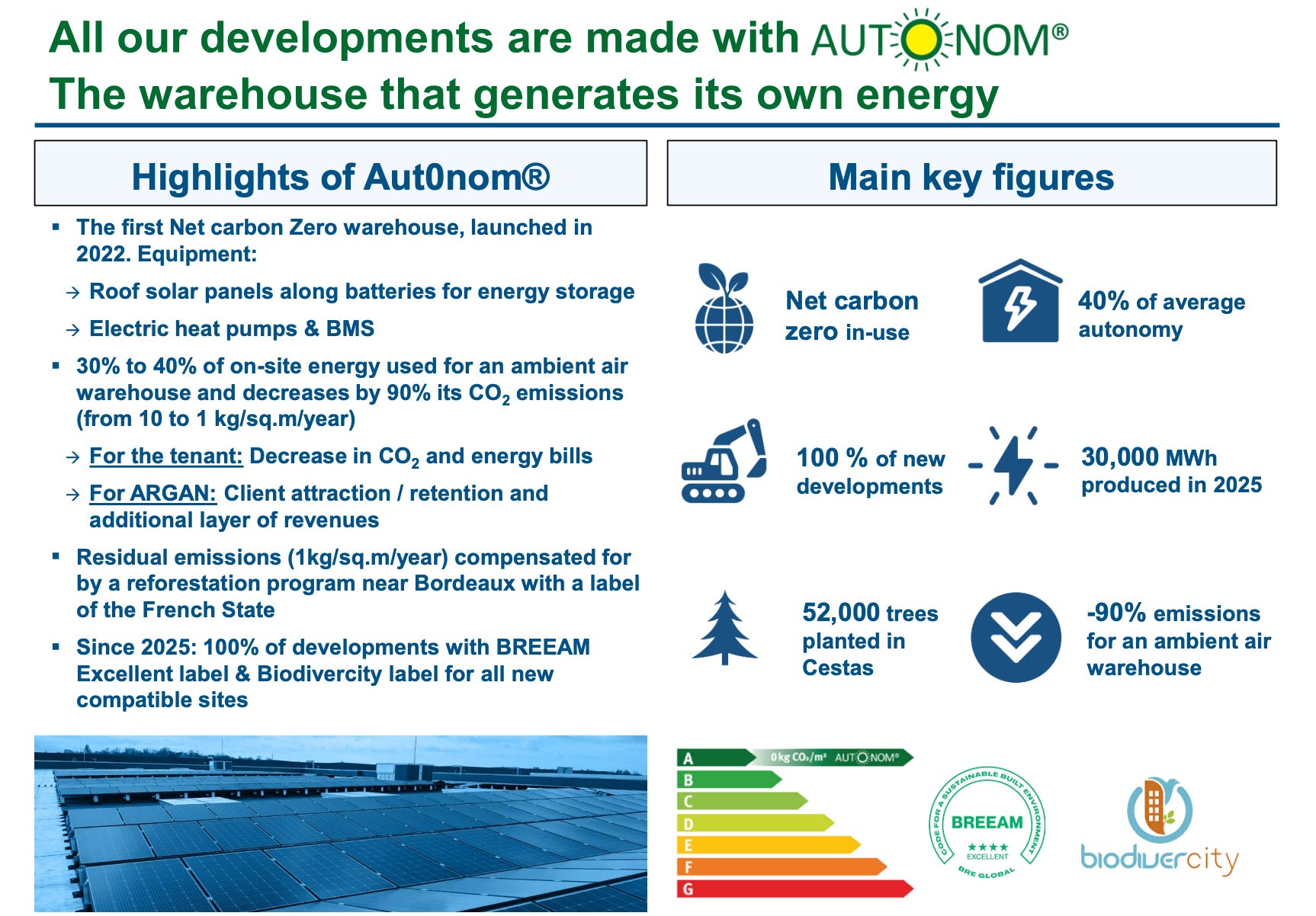

Their tenants aren’t just looking for four walls and a roof, they are looking for efficiency and ESG compliance.

Argan has pioneered warehouses that produce their own green energy via rooftop solar and heat pumps, that they have branded as AutOnom.

For a company like Amazon or L’Oréal that has strict “Net Zero” targets, an Argan warehouse helps them meet their corporate climate goals.

It also reduces the the energy costs for the warehouses, which the tenants typically pay.

Second, scarcity of land.

France has strict laws that make it very difficult to get permits for new large-scale buildings.

Argan already owns the best land in France, they have a land bank that competitors can’t easily replicate.

Third, Switching Costs.

When a tenant like Decathlon moves into a custom-built 100,000-square-meter facility, they spend millions on their own internal automation and robotics.

They sign long leases because the cost of moving their robots and staff is too high.

We can see evidence of Argan’s competitive advantages through their occupancy rates above 99%.

2. Is management capable?

Argan SA is a family-owned company.

The company was founded in 2000 by Jean-Claude Le Lan, who currently serves as the Chairman of the Supervisory Board.

The leadership is multi-generational, with family members roles across the organization:

Ronan Le Lan (Son): Chairman of the Executive Board (effectively the CEO).

Jean-Claude Le Lan Junior (Son): Member of the Supervisory Board and Head of Management Control and Treasury.

Nicolas Le Lan (Son): Member of the Supervisory Board (until early 2025) and Head of Asset Disposals and Acquisitions.

Ronan Le Lan - Chairman of the Executive Board

Mr. Le Lan has been at Argan since 2001. He has overseen its growth into the leading French logistics REIT.

Under his leadership, Argan achieved its “Plan 2025” goals early, reaching a €4 billion portfolio value.

Francis Albertinelli - CFO

Mr. Albertinelli has Argan SA’s CFO since 2004.

He has managed to keep Argan’s average cost of debt incredibly low (~2.10%) despite rising market rates.

Insiders own more than 37% of the company. The La Lan family has a lot of skin in the game.

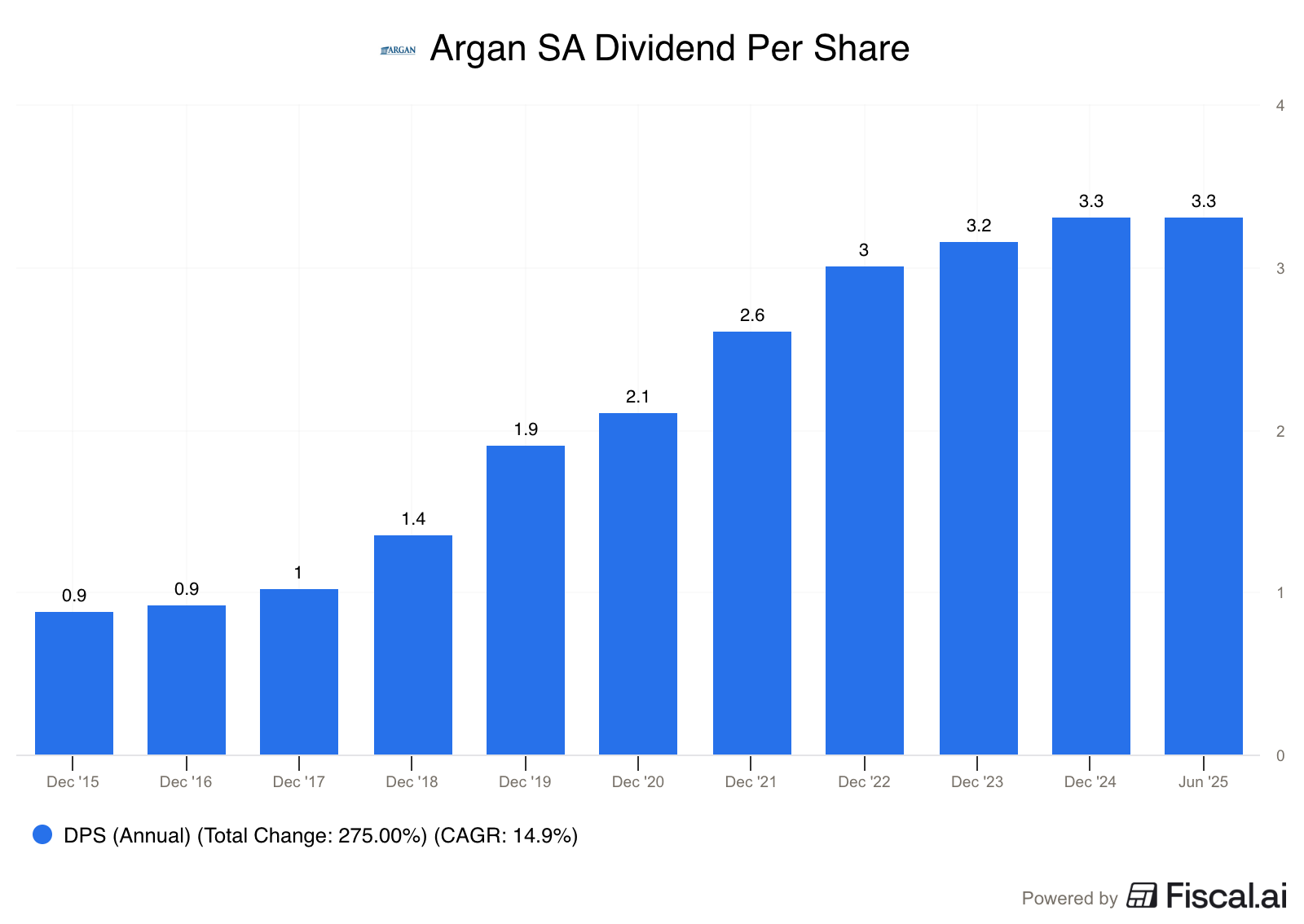

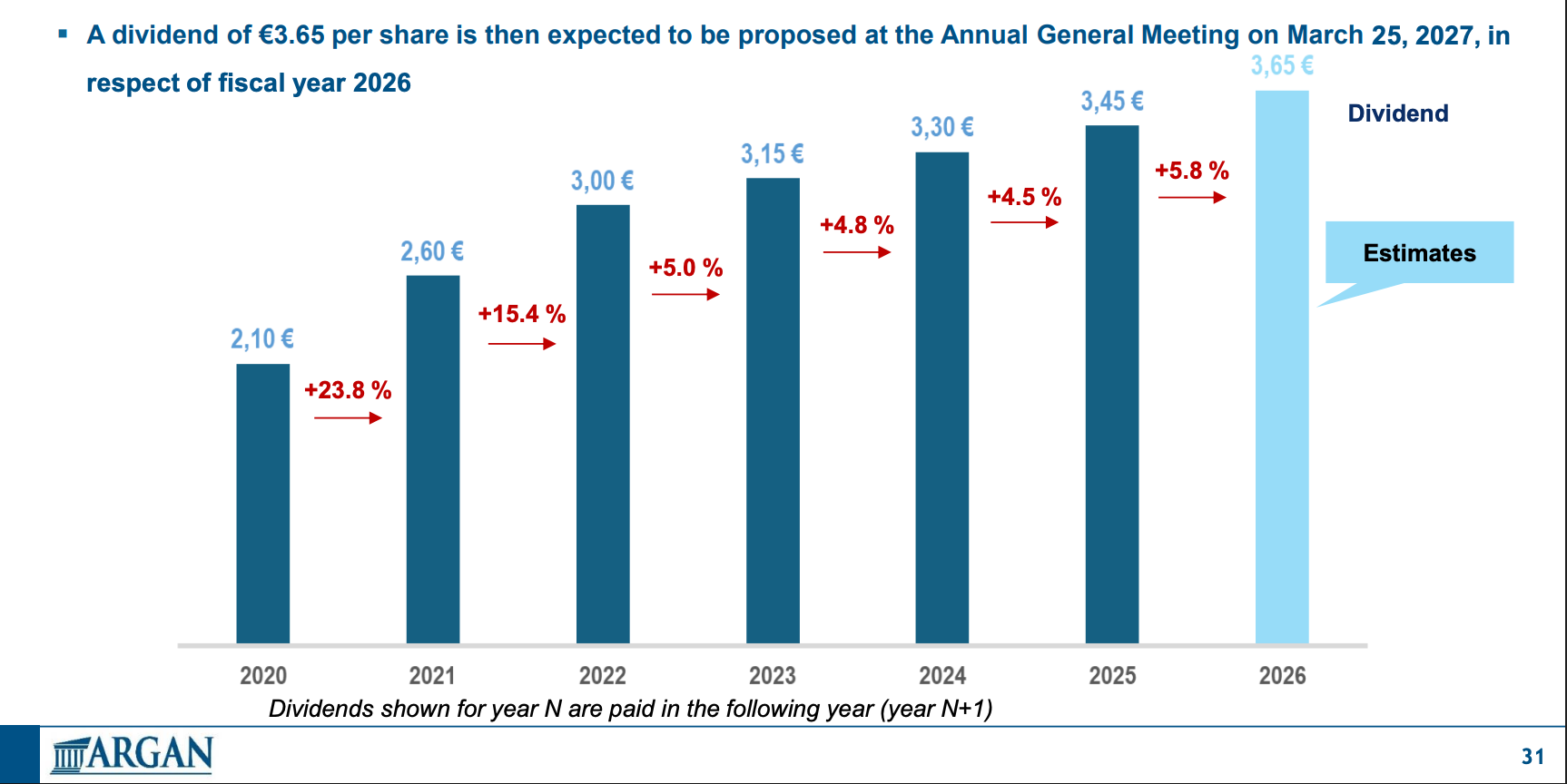

3. Has the company grown the dividend attractively?

We look for:

At least 10 years of dividend growth

5-year dividend growth >5%

Argan has grown its dividend consistently for over 15 years.

5-year CAGR: 11.7% per year.

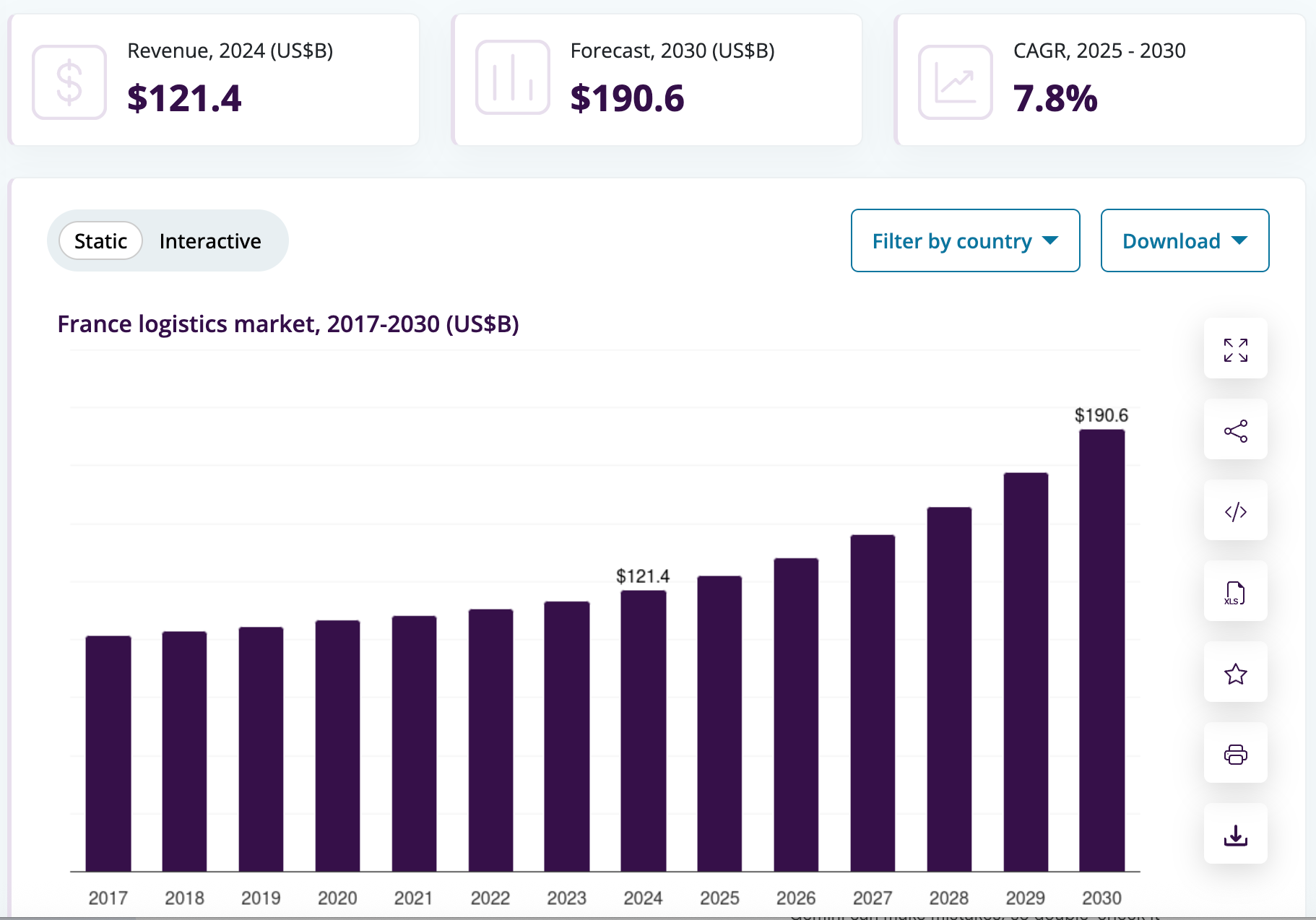

4. Is the company active in an attractive end market?

The French logistics market is very attractive because of two massive tailwinds:

E-commerce: Online shopping requires much more warehouse space than traditional retail.

Green Transition: Companies are moving out of old, gas-heated warehouses and into green Net Zero buildings like Argan’s AutOnom sites. With limited new land available to build on, the demand for Argan’s existing space remains incredibly high, keeping occupancy at 99%+.

The market is projected to grow at 7.8% per year until 2030.

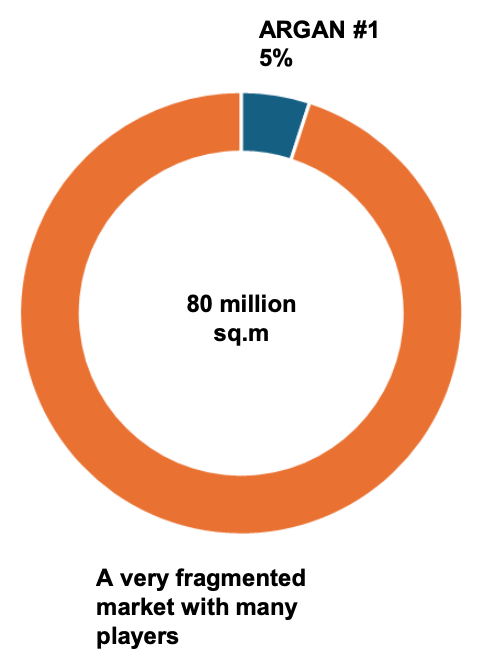

It’s a very fragmented market.

Argan SA is the #1 player, but only has about 5% market share.

5. What are the main risks for the company?

Tenant Concentration

One tenant, Carrefour, makes up 29% of Argan’s rent. If Carrefour had major financial trouble, Argan would have a massive hole to fill.

Mitigation: Carrefour is a National Champion in France and highly solvent. Furthermore, Argan is diversifying by signing new deals with names like Amazon and L’Oréal to bring that percentage down over time.

Interest Rate Risk

REITs borrow a lot of money. When interest rates go up, the cost to refinance debt can eat into dividends.

Mitigation:Argan has 98% of its debt at fixed or hedged rates. They also have an investment-grade credit rating, which allows them to borrow money cheaper than smaller competitors.

6. Does the company have a healthy balance sheet?

We typically look at Debt/Equity, but that number can get skewed in a company that owns a lot of real estate.

Why? Depreciation.

Accounting rules make properties lose a lot of value on paper, even if they don’t in real life.

That can make equity look artificially low and Debt/Equity artificially high.

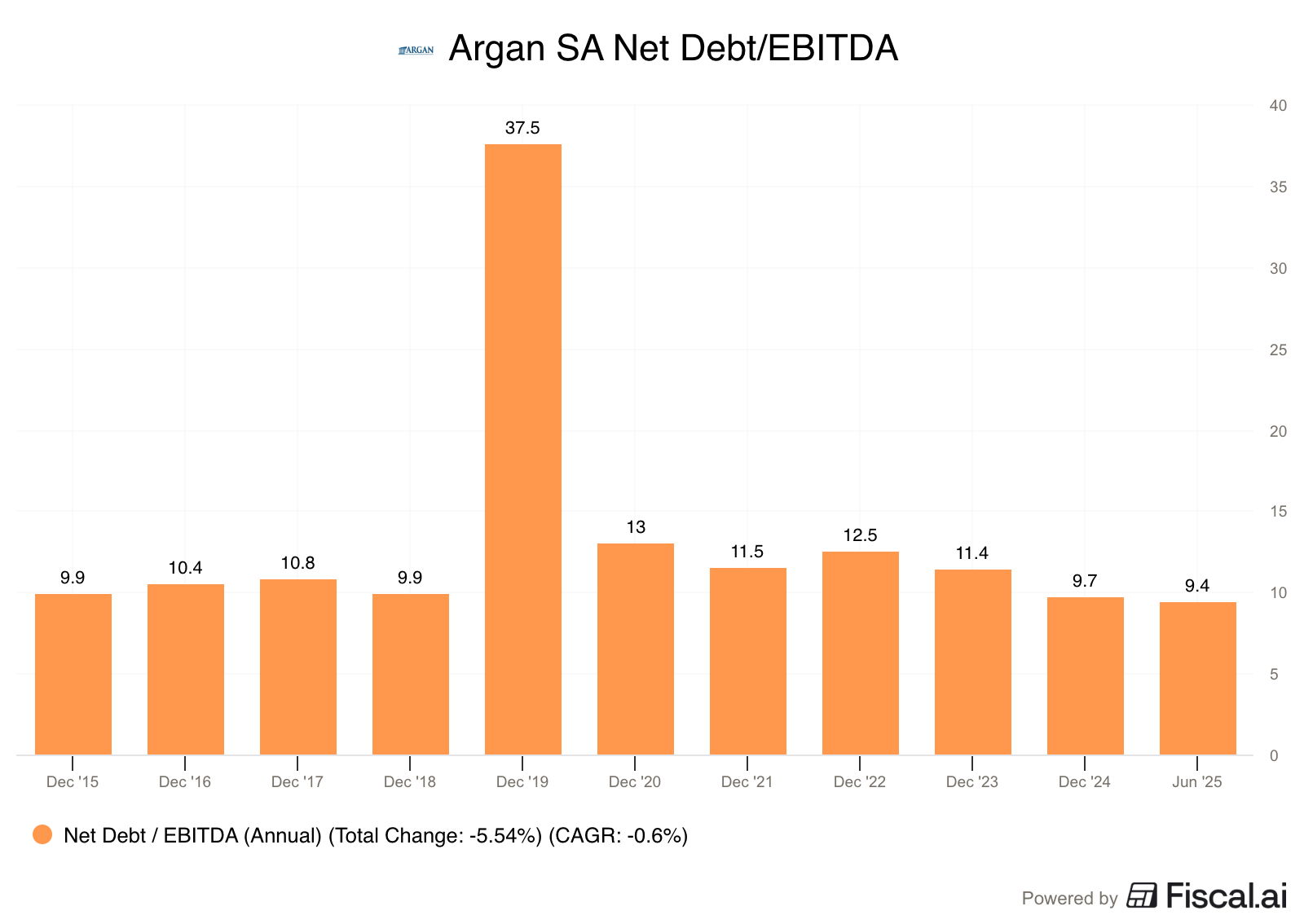

So what do we look at instead? Debt / EBITDA (leverage ratio)

The rule of thumb for REITs is that a Debt/EBITDA that’s 6x or lower is generally safe. Argan is currently higher than this at 9.4x, but they are actively paying down debt.

Also, don’t forget that Argan is a developer , which means they carry debt on buildings that aren’t yet producing earnings, making this number look high.

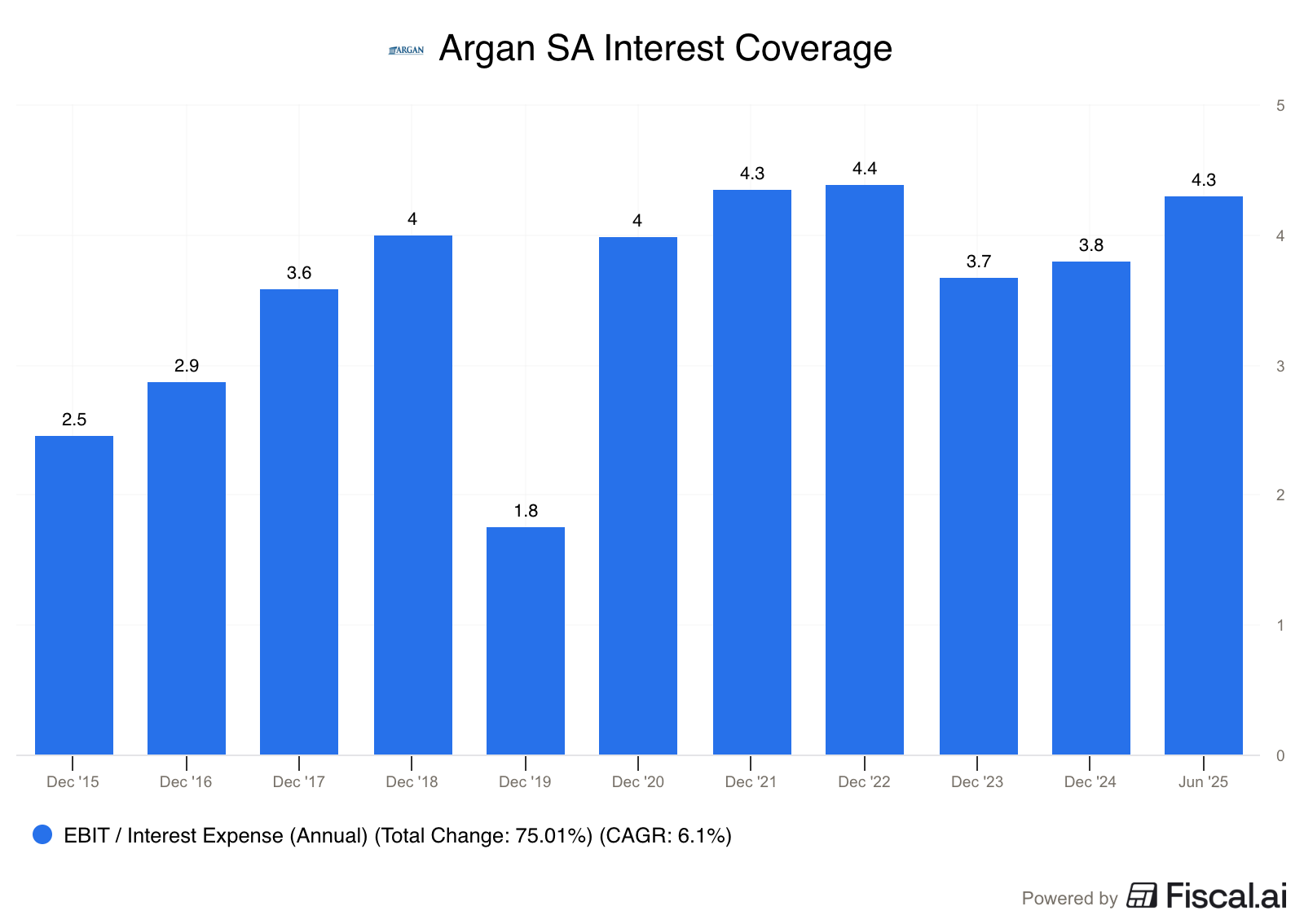

We also want to know how easily the REIT can pay its interest with its cash flow.

European companies typically report this as an Interest Coverage Ratio (ICR). We want to see at least 2.5x.

Argan’s is strong at 4.3x.

Other Debt Characteristics

Argan’s balance sheet is solid:

Cost of debt: 2.10% (very low)

LTV (Loan to Value): 41.1% (Target is <40%)

Credit Rating: BBB- (Investment Grade)

7. Is the company a great capital allocator?

Key signs:

Payout Ratio <80% (Recurring Net Income)

Effective equity issuance or buybacks

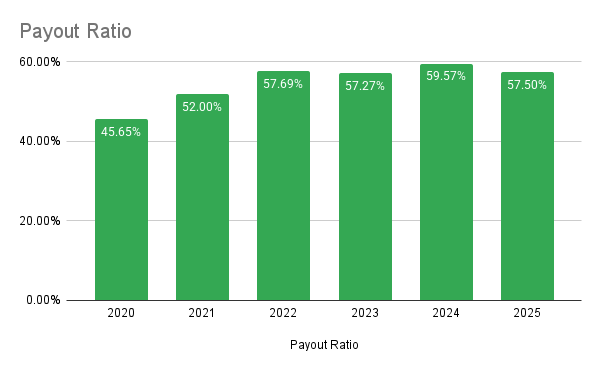

Payout Ratio:

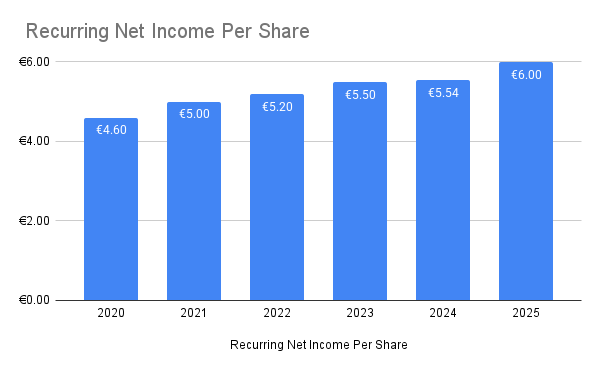

Argan is very conservative here. They paid out only 57.5% of their Recurring Net Income (€3.45 dividend / €6.00 earnings), leaving them plenty of cash to reinvest.

We should define Recurring Net Income here.

It measures the profit Argan makes strictly from its core business - renting out warehouses - after paying all operating bills and mortgage interest.

Argan SA excludes anything that doesn’t represent regular cash flow, like:

Paper Value Changes. If the estimated market value of a building goes up on paper (fair value adjustment), it doesn’t generate cash, so it is ignored for this metric

One-Time Sales. Profits from selling a building (disposal income) are excluded because you can only sell a specific building once

Recurring Net Income is very similar to Core FFO for a U.S. REIT.

Equity Issuance

Like any REIT, Argan SA issues shares to raise capital to grow.

But remember that insiders own nearly 38% of the company.

Management focuses heavily on growing Recurring Net Income per Share.

In 2025, this grew by more than 8%, showing that the growth is actually reaching the shareholders.

8. How does the past and future growth of the company look?

5-year revenue growth: 14.5% per year

5-year Recurring Net Income per Share growth: 5.5% per year

Future Growth

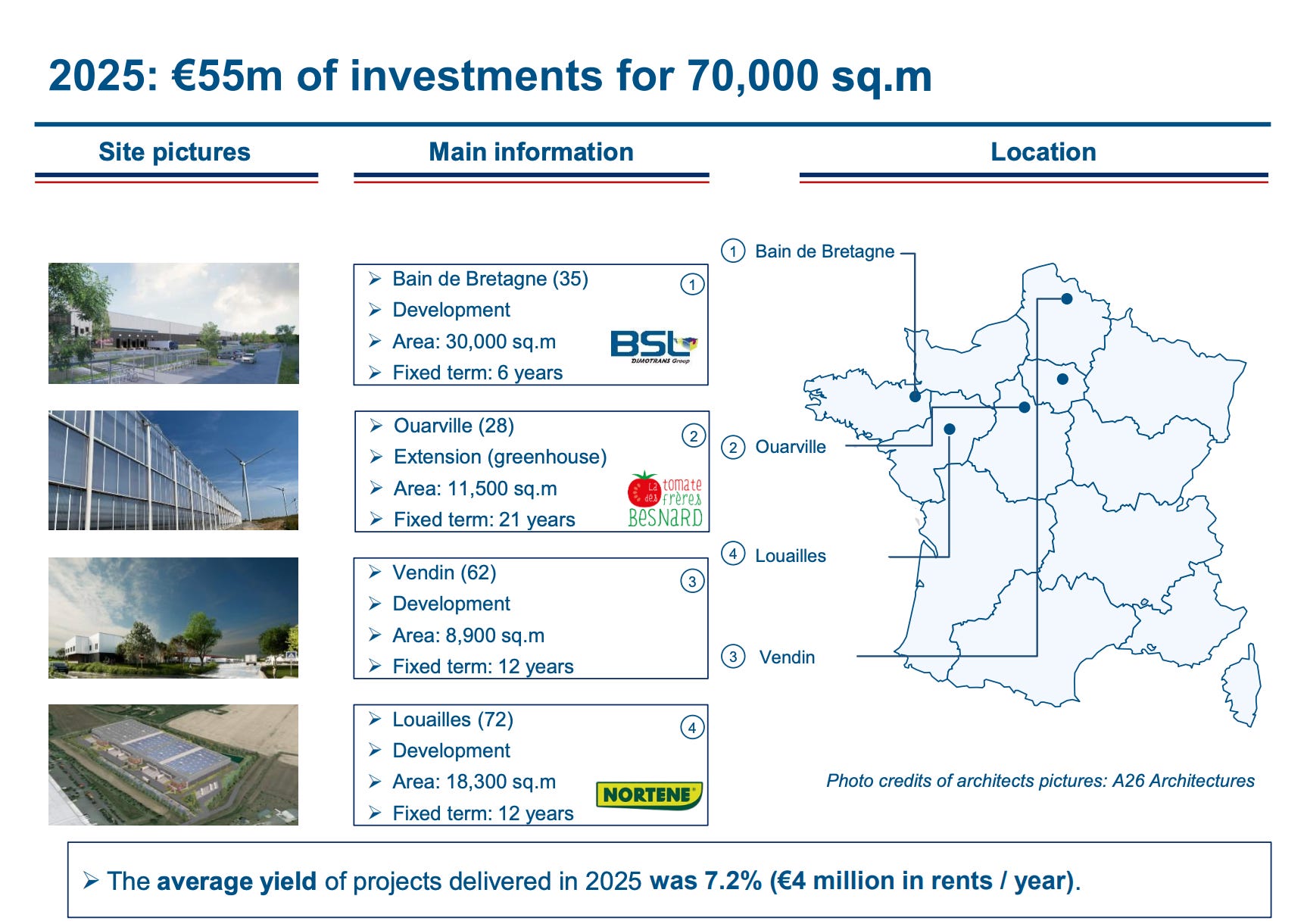

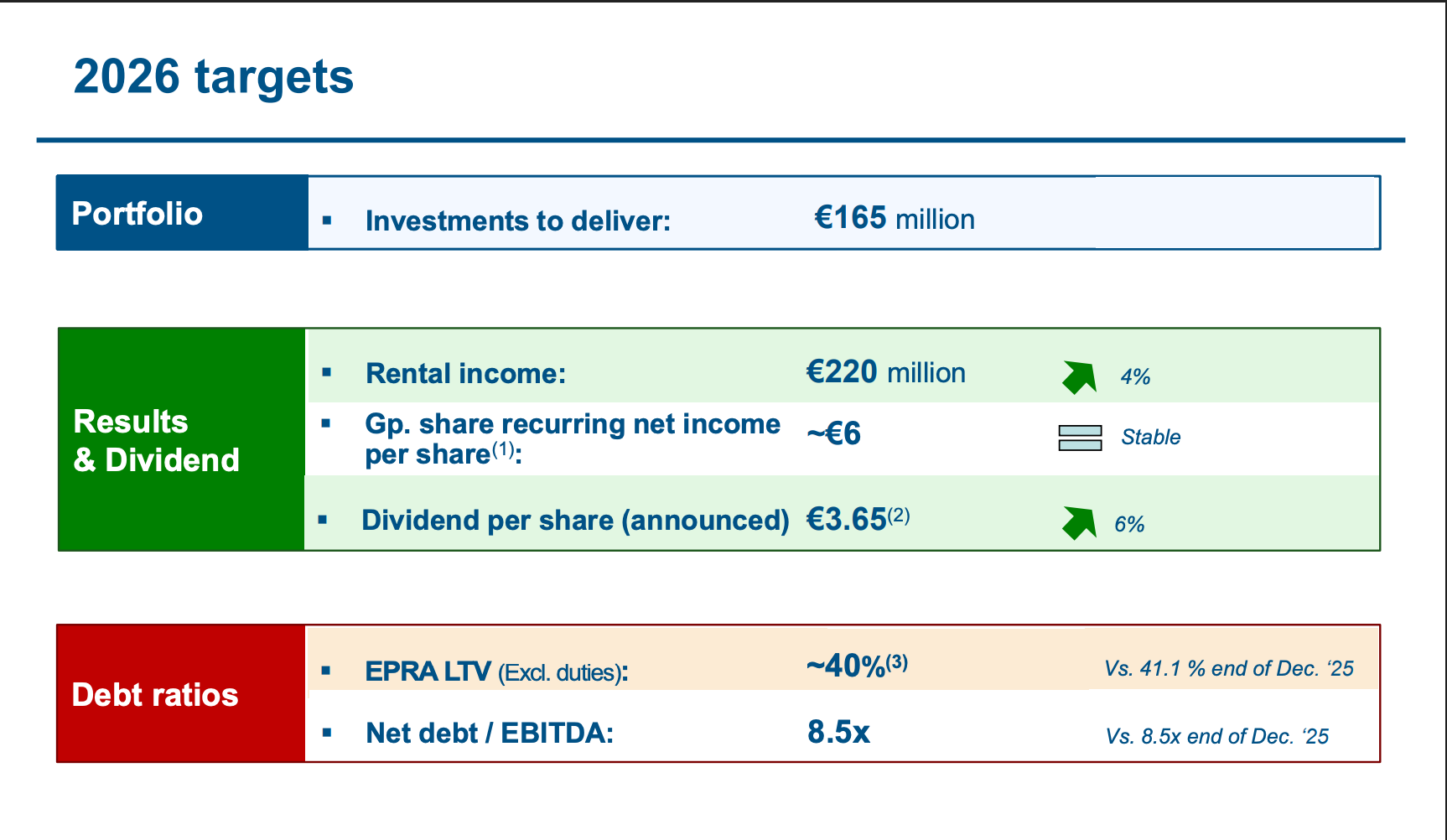

In 2025, Argan SA made €55 million in investments, with a yield of 7.2%.

In 2026 they aim to make €165 million in investments.

The goal is to stop borrowing by the end of 2026, so these investments will be funded by selling mature properties.

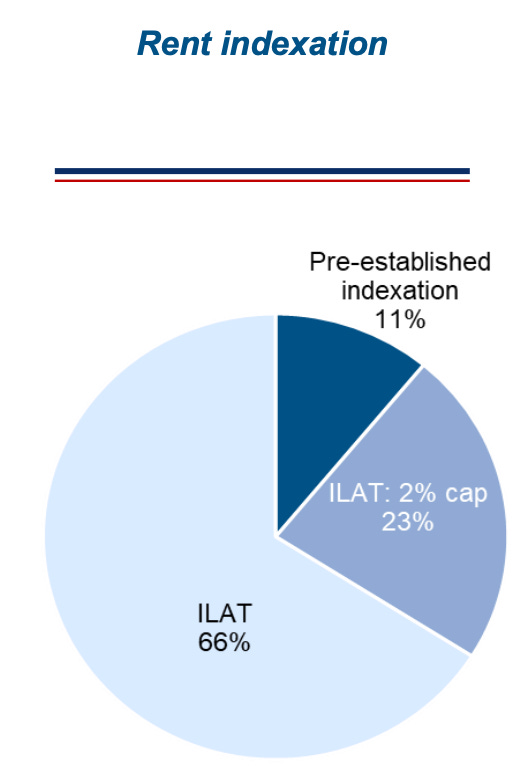

Argan SA also indexes its leases to inflation.

9. Can the company grow dividends into the future?

Let’s check:

Current yield: 4.7%

Payout ratio: 57.5%

With a payout ratio of only 58%, Argan has lots of room to continue raising dividends even if growth slows down.

But with their focus on reducing debt, and growing Recurring Net Income per Share, I don’t see a reason that Argan SA can’t keep sustainably raising the dividend.

An increase of nearly 6% will be proposed in March.

10. Does the company trade at a fair valuation level?

We value every company 3 different ways:

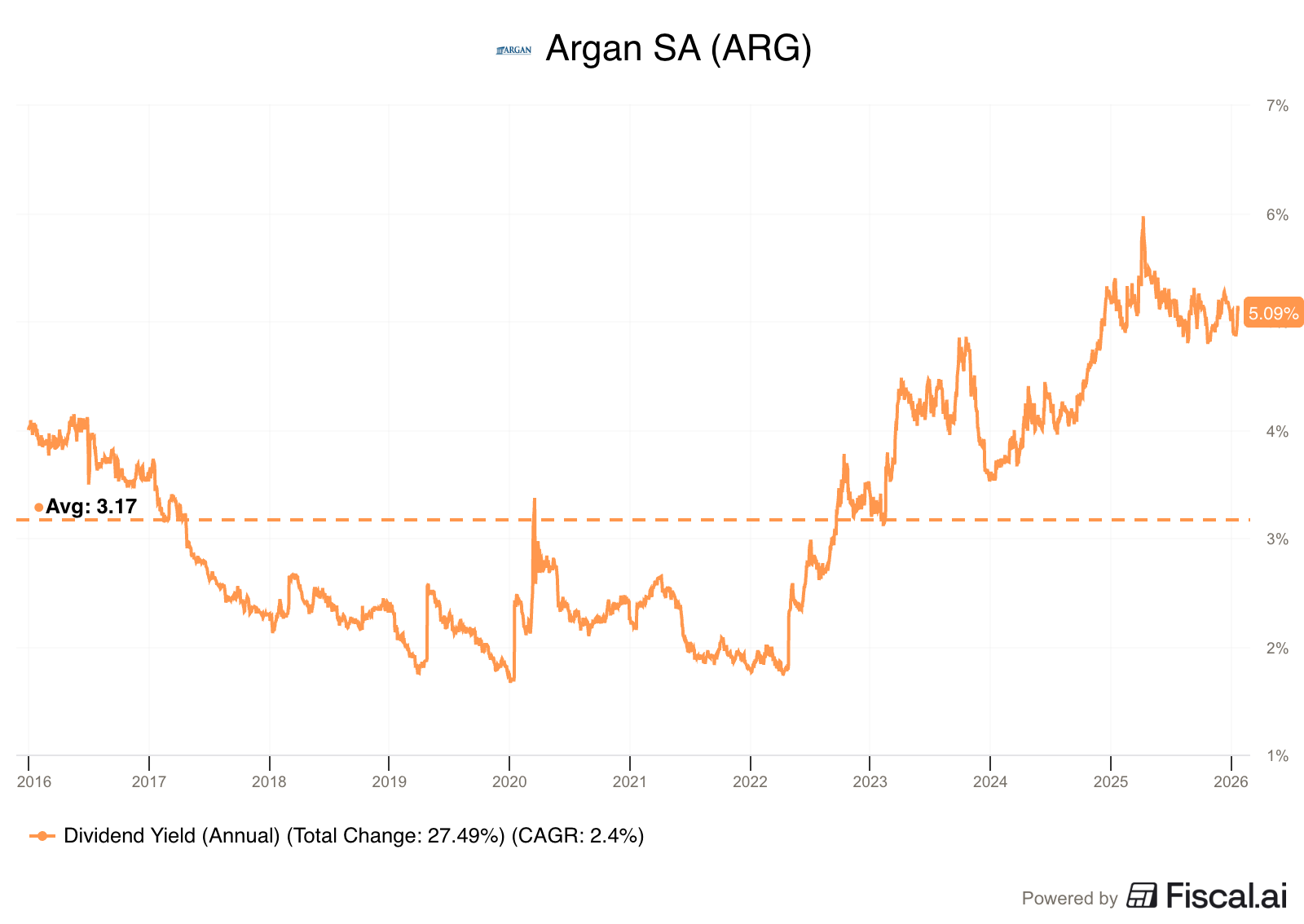

1. Dividend Yield vs History

Historical average dividend yield: 3.2%

Current yield: 4.7%

Using this metric, Argan looks undervalued.

2. Earnings Growth Model

This shows us the yearly return we can expect from a company.

We’ll take into account Recurring Net Income per Share growth, the dividend yield, and multiple contraction or expansion.

The formula looks like this:

Expected return = Recurring Net Income/Share Growth + Dividend Yield + Multiple Expansion (or contraction).

Here are the numbers for Argan:

RNI/Share Growth: 5.3%

Dividend Yield: 4.7%

Change in P/RNI: Argan is currently trading at 11.6x Recurring Net Income per Share, let’s be conservative and assume this remains flat.

Expected return = 5.3% + 4.7% + 0% = 10% return per year

3. Reverse Dividend Discount Model

As Charlie Munger says, “Invert, always invert!”

Solving complex problems is often easier backward. That’s exactly what we do with the Reverse DDM.

Solving the DDM for growth tells us how much dividend growth is priced in by the market.

Here’s the formula:

Expected growth = Required return – (DPS next year / Current share price)

Let’s put some numbers in for Argan:

Required return: 10%

DPS next year: €3.65

Current share price: €69.80

Expected growth = 10% - (3.65/69.80) = 4.8%

This tells us that the market is pricing in a 4.8% growth in Argan’s dividend.

5-year DPS CAGR: 11.7%

Dividend Score

Argan SA receives a Dividend Score of 8.5/10. This is another very high quality company in my opinion. It offers a rare combination of a healthy 4%+ yield and high single-digit growth, all backed by the most stable tenants in Europe.

Conclusion

Argan SA is a boring business with exciting profits and dividends.

Their focus on developing high-end French warehouses has built a moat around their portfolio.

The investment case comes down to three simple things:

Necessary Assets: Companies like Amazon and Carrefour can’t easily move out of custom-built, robotic-heavy warehouses that produce their own renewable energy. That’s why Argan’s occupancy rate is above 99%.

Inflation Protection: Every lease is indexed to inflation, and their “AutOnom” warehouses protect tenants from rising energy costs.

Safe Yield: You are getting a starting yield of 4.7%, which is well above the historical average, backed by a family management team that owns nearly 38% of the company. With a payout ratio of just 57.5%, the dividend looks safe now, with plenty of room to grow.

Argan is a high-yield stock that still offers double-digit total return potential.

One Dividend At A Time,

-TJ

Check out these resources:

Tickerdata 🚀 (My automated spreadsheets and instant stock data for Google Sheets!)

Interactive Brokers 💰 (My favorite place to buy and sell stocks all around the world!)

Seeking Alpha 🔥 (Research stocks $30 off! + 7 day free trial)

HYSA 📊 (Get Access to the Best High Yield Savings Accounts!)

Disclaimer: As a reader of Dividendology, you agree to our disclaimer. You can read the full disclaimer here.

| A guest post by

|

Worth noting the foreign withholding tax in retirement accounts.

Amazing read!