🌍 Don't Miss The BIGGEST Market Shift Right Now

Japan Bond Yields, Equity Risk Premiums, & BIG Dividends ⚠️

I’ve always hated how ‘sensational’ financial media has been.

Of course, there is a clear reason as to why this is.

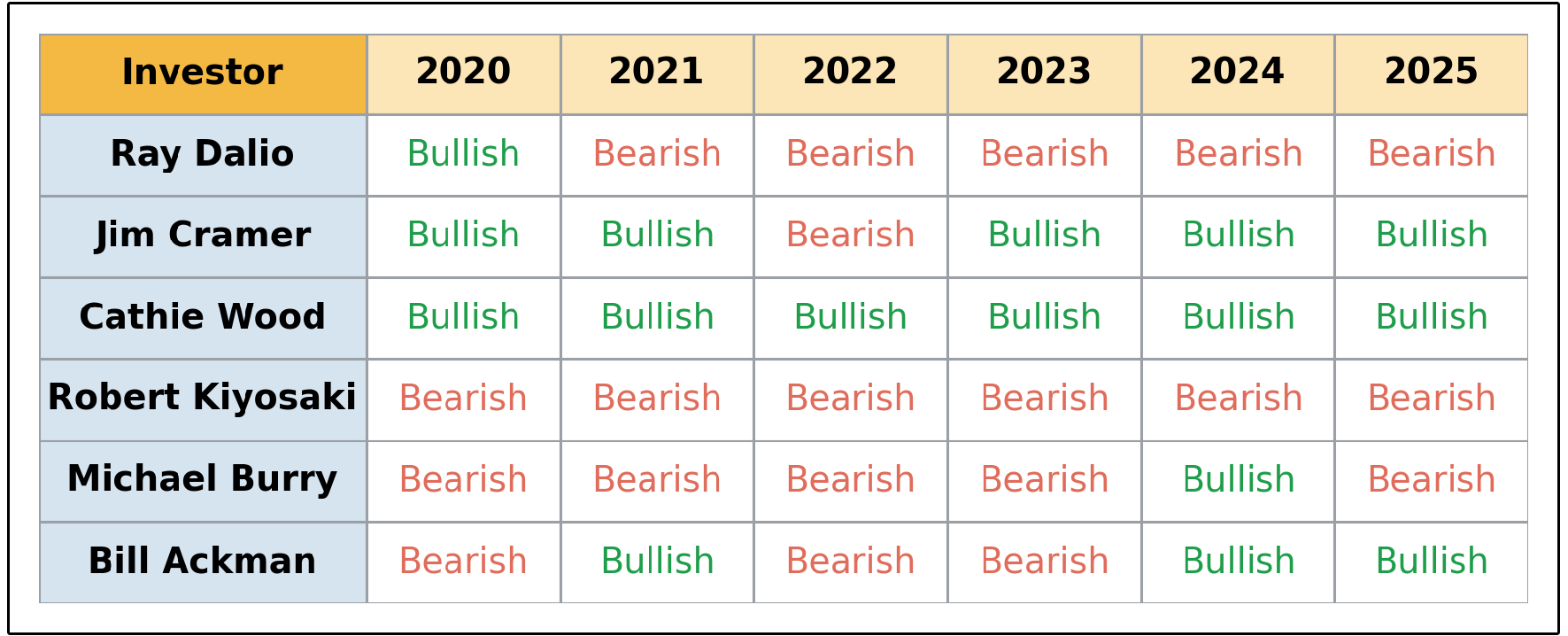

Why is Cathie Wood perpetually bullish?

Perhaps so people invest in her innovation fund.

Why is Ray Dalio so bearish?

So people invest in his ‘All Weather Portfolio’ fund.

As the old Charlie Munger quote goes:

That’s the problem with most market commentary.

It is not designed to make you a better investor.

And because of that, I am usually very skeptical of dramatic market warnings.

But here is the uncomfortable truth:

The market is shifting dramatically right now, but it is happening slowly beneath the surface, in a way most investors do not fully recognize yet, and may not feel until the consequences become much more obvious.

Today, I will reveal the cracks as concisely as I can.

🇯🇵 Japanese Bond Yields

Bond yields in Japan!?

Does it get any more boring and irrelevant?

Stay with me, because this is quietly becoming one of the most important macroeconomic shifts happening in the world right now.

For decades, Japan helped shape the global financial system in a way most investors never realized.

Japanese interest rates were essentially pinned near zero for years.

Money in Japan was extraordinarily cheap.

And because of that, enormous amounts of global capital borrowed in Japanese yen and flowed into higher-yielding assets around the world.

US stocks

US Treasuries

Emerging markets

Private equity

Corporate bonds

Real estate

Practically every major asset class benefited from this backdrop in some way.

But now, something is changing.

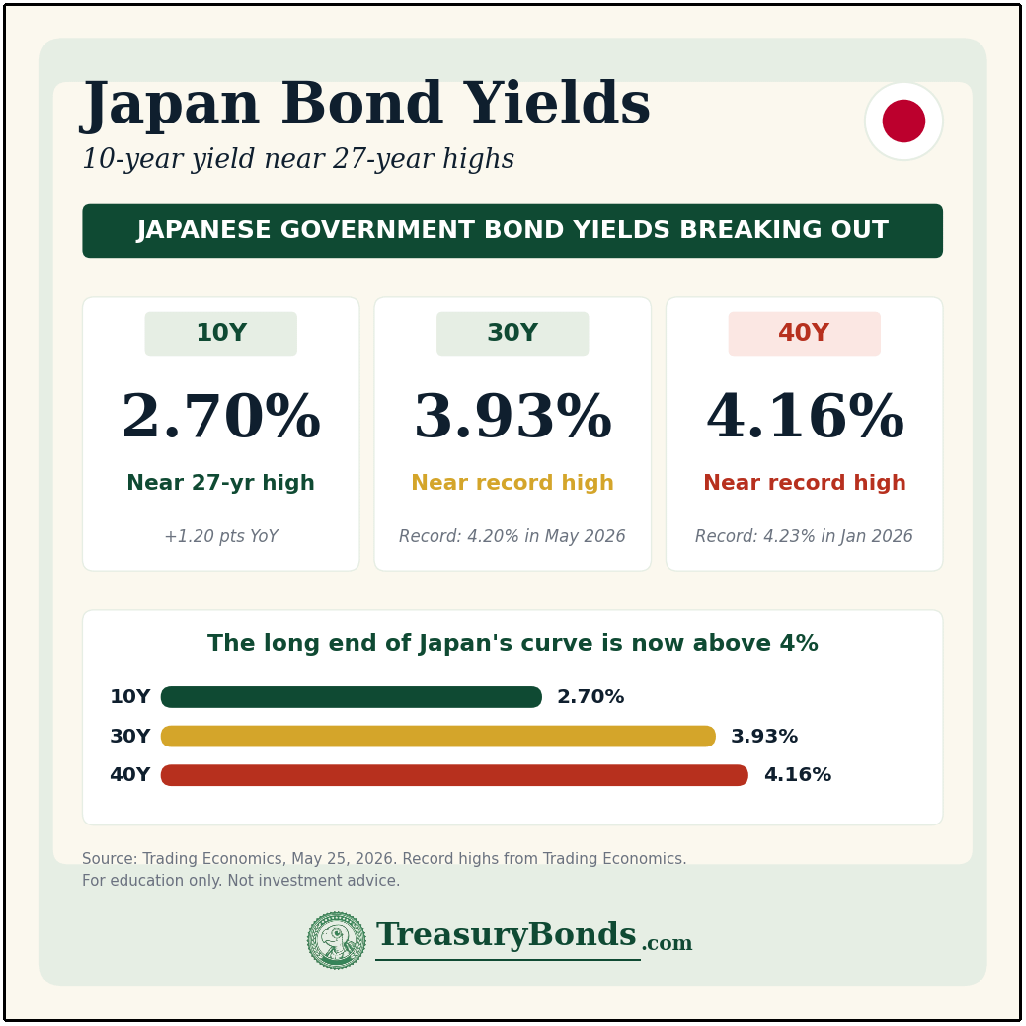

Japanese government bond yields are breaking out:

The 10-year Japanese government bond yield is now near 27-year highs.

The 30-year yield is near record highs.

And the 40-year Japanese government bond yield has now moved above 4%.

That may not sound dramatic compared to US rates.

But for Japan, this is a seismic shift.

For years, global markets operated under the assumption that Japanese rates would stay permanently suppressed.

That assumption helped fuel one of the most important liquidity engines in modern financial history:

The Yen Carry Trade.

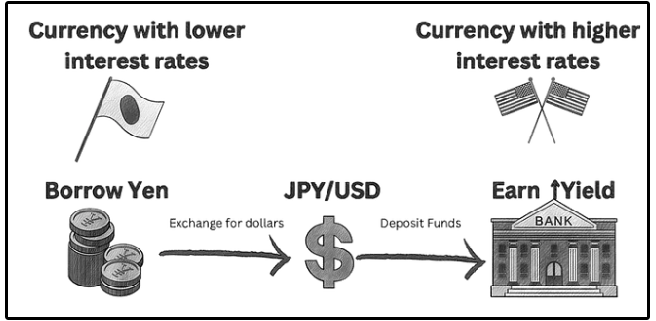

💴 The Yen Carry Trade

The yen carry trade sounds complicated.

In reality, the concept is very simple.

Investors borrow money in Japanese yen at extremely low interest rates-

Then use that borrowed capital to buy higher-yielding assets elsewhere.

As long as Japanese borrowing costs stay low and the yen remains weak or stable, the trade works beautifully.

It became one of the largest liquidity machines in the world.

And for years, it quietly helped support global asset prices.

But now, the setup is changing.

As Japanese bond yields rise, borrowing in yen becomes more expensive.

At the same time, higher Japanese yields create an incentive for Japanese capital to stay home instead of flowing abroad.

And if the yen strengthens, the trade becomes even more dangerous, because suddenly investors are not just dealing with higher borrowing costs-

They are also facing currency losses.

That can force large investors to unwind positions.

And when carry trades unwind, liquidity disappears fast.

This is one of the reasons why Japanese bond yields matter so much more than most investors realize.

This is not just a “Japan story”, it’s a global liquidity story.

For years, markets benefited from an enormous amount of cheap global capital.

Now one of the largest sources of that cheap capital is beginning to disappear.

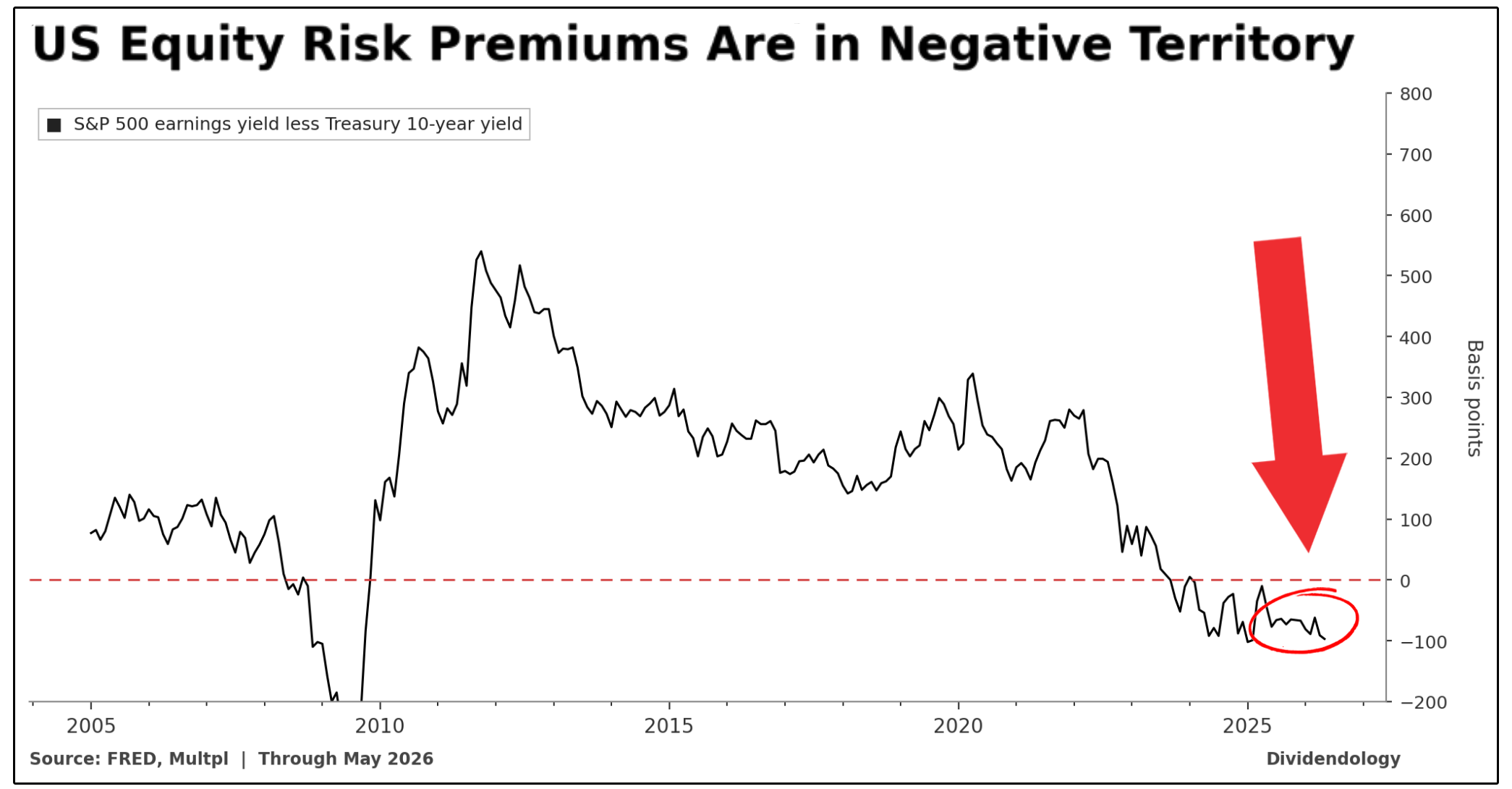

📉 Equity Risk Premiums

One of the results of the ongoing shift in Japan is the change in equity risk premiums in the U.S.

At the exact same time global liquidity is becoming less supportive, US stocks remain historically expensive.

This is the most important chart you'll see today.

It shows the U.S. Equity Risk Premium (ERP), more specifically, the S&P 500 earnings yield minus the 10-year Treasury yield.

In simple terms, it answers one critical question:

How much extra return are investors being paid to own stocks instead of “risk-free” government bonds?

Right now, according to this chart, the answer is almost nothing or even negative.

To start, we must understand the earnings yield and 10-year Treasury yield.

Earnings Yield = inverse of the P/E ratio (If the S&P 500 trades at a 20x P/E, the earnings yield is 5%)

10-year Treasury Yield = what you earn lending money to the U.S. government

The equity risk premium is the spread between the two.

Historically, stocks have offered a 3–5% premium over Treasuries.

That premium compensates investors for volatility, drawdowns, and uncertainty.

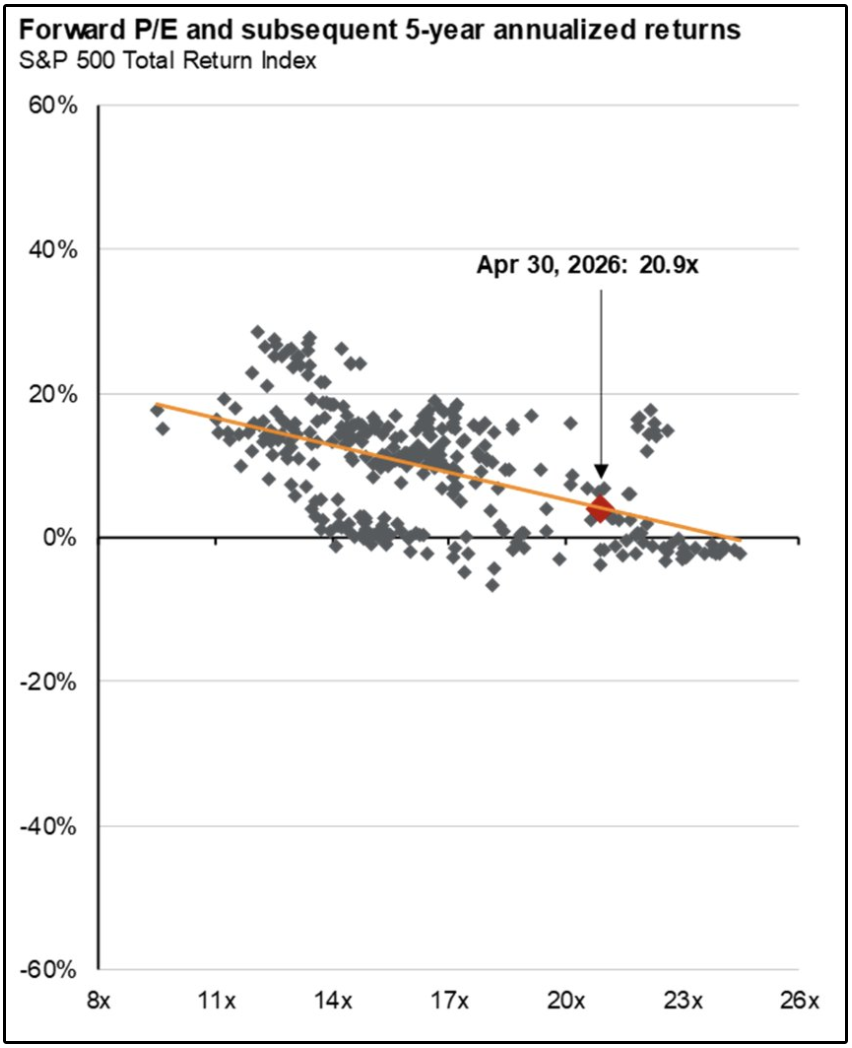

But we now have a scenario where the treasury yield is sitting close to a 5 year high.

And on top of this, the earnings yield of the S&P 500 is hitting its lowest level in over 10 years.

When this has happened in the past, forward returns over the next 5 years have been quite low, or even negative in some cases.

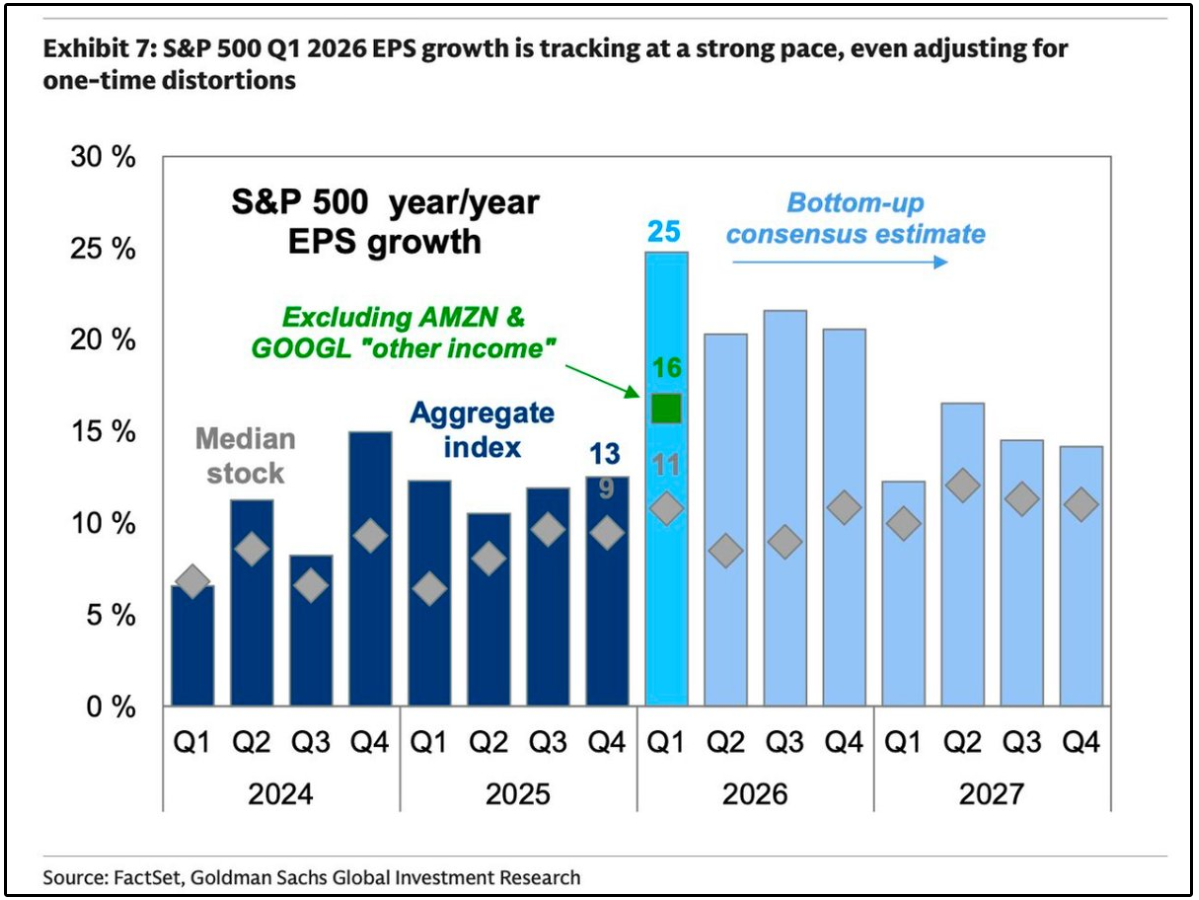

Of course, the counter argument to this is the fact that future earnings growth for the S&P 500 is projected to be higher-

And this is true… somewhat.

Earnings growth has picked up significantly, but a large portion of this growth comes from one-time distortions tied to “other income” from mega-cap companies like Amazon and Google, rather than purely from broad-based operating earnings growth across the index.

Earnings growth is still faster than previous years even if we exclude these items, but it also isn’t nearly as fast as some would have you to believe.

And in the midst of all of this-

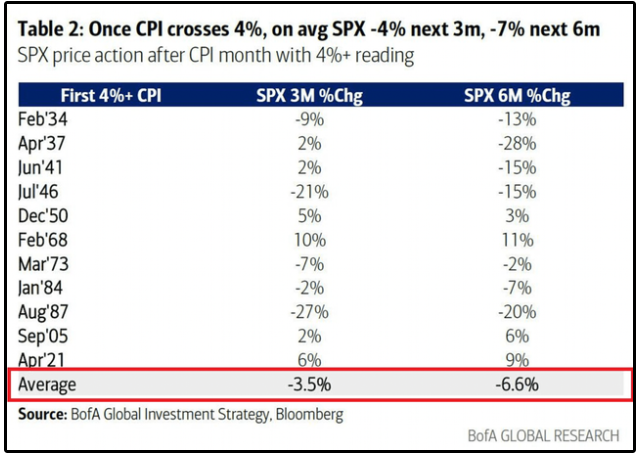

Inflation is now hitting its highest levels in over three years.

According to BofA Global Research, once CPI first crosses above 4%, the S&P 500 has averaged:

-3.5% over the next 3 months

-6.6% over the next 6 months

And of course, as a result of this, the market now expects us to see a rate hike by the end of the year, which is a stark difference from when we were expecting multiple rate cuts as we entered into 2026.

Interest rates are to asset prices what gravity is to the apple. When there are low interest rates, there is a very low gravitational pull on asset prices. - Warren Buffett

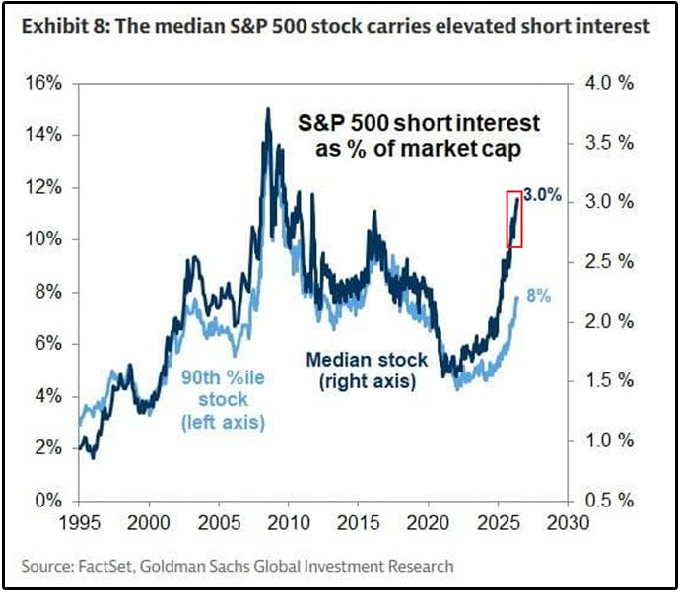

🏦 Institutions See The Cracks

The interesting part is that institutional investors appear to be noticing this shift.

Short interest across the S&P 500 has moved meaningfully higher.

The median S&P 500 stock now has short interest equal to 3.0% of its market cap, the highest level since 2012.

That is twice as high as the levels seen during the 2020 pandemic crash.

For context, short interest in the median S&P 500 stock reached 3.8% at the peak of the 2008 Financial Crisis.

Meanwhile, the most heavily shorted 10% of S&P 500 stocks now have short interest equal to 8.0% of market cap, the highest level since 2018.

📈 So What?

My goal is never to ‘fear monger’-

And I certainly tend to be more bullish generally speaking.

But the reality is there are some abnormalities in the market right now.

So naturally we must ask, how do we position ourselves in light of the changing global economy?

Let’s look at an example.

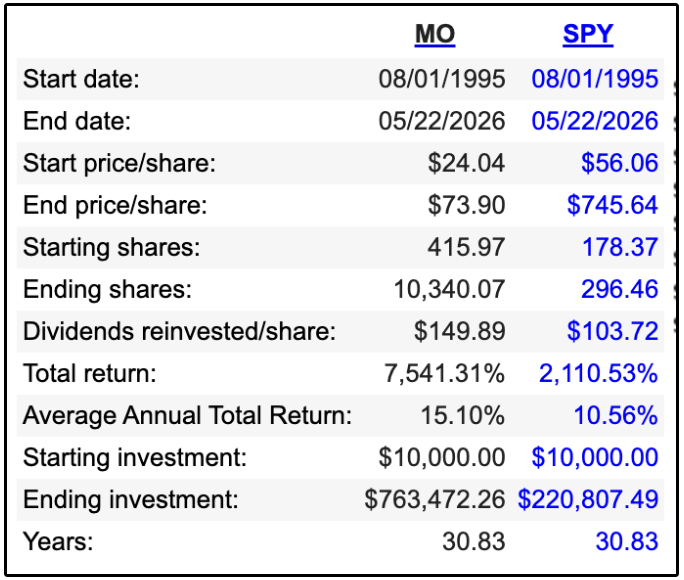

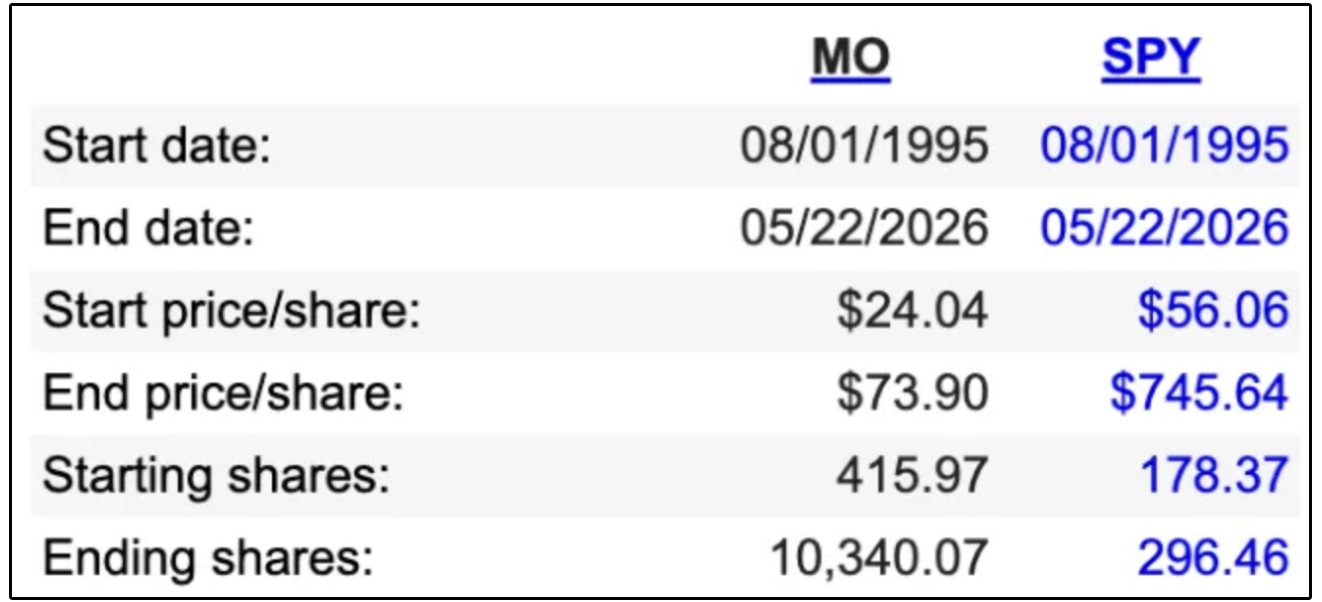

From 1995, to today, Altria outperformed the S&P 500 by a wide margin.

$10k into MO = $763K

$10k into S&P 500 = $220k

And at first glance, it almost does not make sense.

How did this happen?

The answer is actually a perfect case study for the environment we may be entering, and it boils down to three things:

Valuation matters

Dividends matter

Reinvestment matters

Let’s look at each of them.

1. 💸 Starting Valuation Matters

The first reason is simple:

Altria started at a much cheaper valuation.

In 1995, Altria was already a highly profitable business, but investors hated the stock because of litigation and regulatory fears.

The business had real risks.

But those risks were also reflected in the price.

One of the biggest drivers of long-term returns is the valuation you pay at the start.

Altria did not need massive growth to produce great returns.

Investors were buying a cash-generating business at a cheap price.

Meanwhile, the S&P 500 was heading straight into the late-1990s tech bubble.

By 2000, many of the largest stocks in the index were trading at extreme valuations.

A lot of future returns had already been pulled forward.

Altria was the opposite, and it was producing meaningful cash flow relative to its valuation.

2. 🌱 Dividends Did The Heavy Lifting

The second reason is even more important:

Altria paid massive dividends that were reinvested.

This is the part most investors miss.

Altria’s stock price only went from about $24 to $74 over this period.

That alone is not what created the massive outperformance.

The real magic came from the dividends.

According to the data, the original investment bought about 416 shares of Altria in 1995.

But after decades of reinvested dividends, those 416 shares turned into more than 10,000 shares.

That is the power of dividend compounding.

The dividends bought more shares at low valuations (meaning higher yield)

Those shares paid more dividends

Those dividends bought even more shares.

And the cycle continued for more than 30 years.

That is how a “boring” stock can quietly produce extraordinary returns.

And despite this incredible outperformance, the stock is still trading at a forward P/E multiple of just 13x!

3. 📉 Altria During The Lost Decade

This is perhaps the most important reason for us to understand.

The third reason Altria outperformed so dramatically is because it crushed the S&P 500 during the 2000s lost decade.

From 2000 to 2010, the S&P 500 basically went nowhere.

In fact, dividends were the only source of positive returns that decade.

Investors started the decade paying extreme valuations during the dot-com bubble.

Then the market got hit by:

The dot-com crash

9/11

Accounting scandals

The housing bubble

The Great Financial Crisis

It was an incredibly difficult decade for the broad market.

It was an incredibly difficult decade for the broad market.

However, Altria was producing and growing real cash flow.

It had a dividend yield of 9.8% in the year 2000, that was fully backed by cash flow!

And because the cash flow kept growing, the company kept growing their dividend as well.

Its business was not very economically sensitive, people kept buying cigarettes regardless of recessions. Yes, cigarette volumes declined over time, But Altria had enormous pricing power.

It could raise prices, protect margins, and continue returning capital to shareholders.

To put it simply, it was producing real returns.

⚠️ The Lesson

Let me be clear, I’m not ‘anti-AI’.

In fact, I’ve seen incredible gains from stocks benefiting from the AI boom:

AVGO: +700%+

CAT: +400%+

ASML: +150%+

TXN: +100%+

However, the ultimate hedge to the current market environment is asking yourself this question:

What assets can keep producing cash flow even if the market environment gets harder?

The dominant AI narrative assumes almost every company will benefit, but the underlying economics may point in the opposite direction.

AI lowers barriers to entry, increases competition, floods markets with cheap output, and compresses margins across many industries.

If every business can suddenly create more content, software, services, and products with fewer resources, pricing power becomes harder to maintain.

But real assets sit on the other side of this trend.

AI cannot create land, buildings, pipelines, power infrastructure, data centers, or scarce physical locations out of thin air.

As digital output becomes more abundant, the assets that cannot be copied may become more valuable.

That is why real assets and dividend growth should matter much more going forward:

They are built around scarcity, cash flow, and income that can survive even as many traditional businesses face more competition and weaker margins.

Most REITs have inflation-linked contracts with their tenants.

MLPs have long term contracts and fee based revenue, making future cash flow very predictable.

Stocks like Altria have recession proof cash flows.

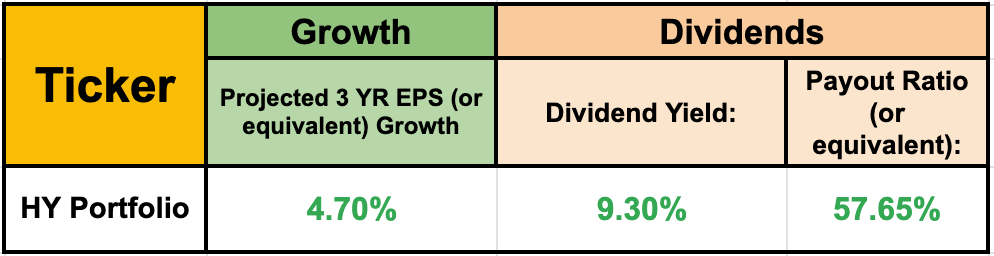

In fact, this is exactly how we’ve outperformed the market in 2026 with our High Yield Portfolio that yields 9.3%!

If you want to get access to the Dividend Growth and High Yield Portfolio’s we are building out and all the features mentioned below, you can do so here:

Check out these resources:

Tickerdata 🚀 (My automated spreadsheets and instant stock data for Google Sheets!)

Interactive Brokers 💰 (My favorite place to buy and sell stocks all around the world!)

Seeking Alpha 🔥 (Research stocks $30 off! + 7 day free trial)

HYSA 📊 (Get Access to the Best High Yield Savings Accounts!)

Great article, Eli. This is a lesson I have learned over the 20 years of trying to educate myself. The most reliable, tried and true safe growth seems to be dividend growth investing. I love to follow the YOC, yield on cost, as a metric for success. This would be the yield on the original investment so I would be curious to see on your original MO investment in 1995, how much your annual dividend today is in terms of % div yield.That original investment of 460 shares at 25 would be approximately $11500. And today with 10000 shares at 75, that is a balance of around $750000, and a dividend yield of 7% produces a yearly deposit of $52500. So the YOC on this is a cool 450%. EVERY YEAR. And it will probably grow from there too. Now put that in an infographic for the visual learners to see.

Excellent article!