💰High Yield Stocks With Sustainable Dividends

Don't Miss These High Yielders With Upside Potential 🔥

On Wednesday, we reviewed the most important task of management:

Capital allocation.

A careful review of the capital allocation of three stocks that have historically been viewed as great dividend payers, revealed some major red flags.

Today, we will do the opposite.

We will look at less popular dividend stocks with high yields that pay out sustainable dividends.

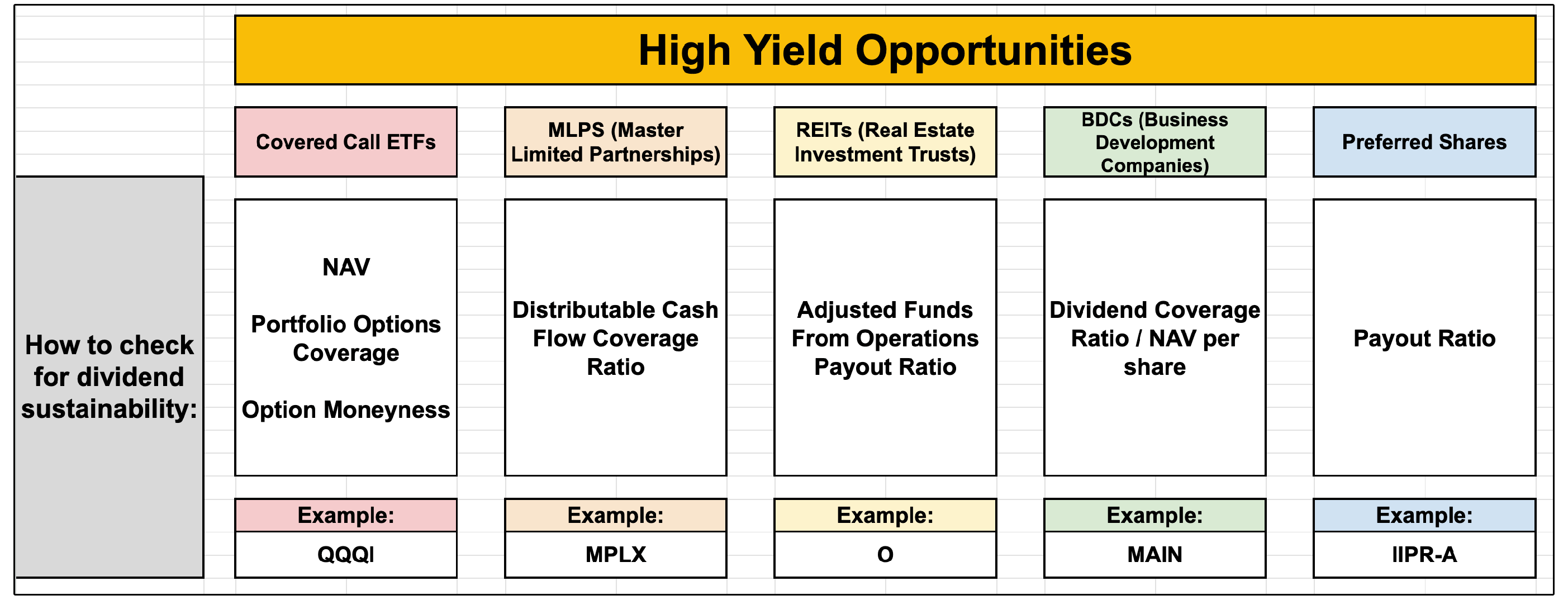

🔍 Where to Look

How many stocks in the S&P 500 currently yield over 5%?

Just fifteen.

How many yield over 6%?

Just five.

The reality of high yield stocks in the S&P 500 is they are often high yield for a reason.

These companies get significant analyst coverage, so there are rarely disconnects with the valuation and the company’s intrinsic value.

And ironically enough, disconnects in valuation are what lead to high yield opportunities that have significant upside.

This is why high yield does not automatically equal high risk.

However, you typically have to turn to alternative high yield asset classes to find these opportunities.

Here are the primary assets we cover to uncover these opportunities:

As you can see, the way we assess dividend sustainability for each of these is different.

In other words, the scarcity of yield in the S&P 500 pushes capital into corners of the market that are less efficient-

Which is exactly where disciplined, income-focused investors can find hidden gems.

Let’s look at just a few examples of sustainable high yields, starting with a stock from the S&P 500.

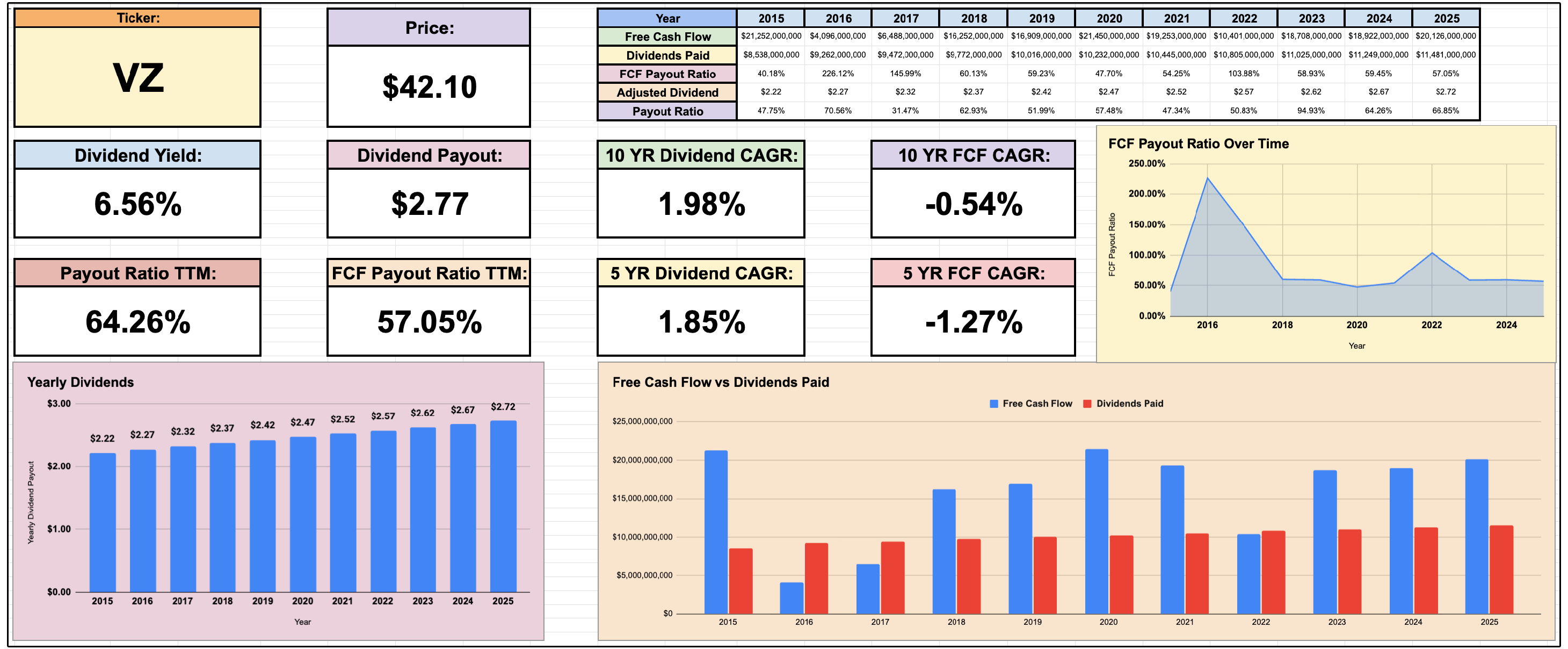

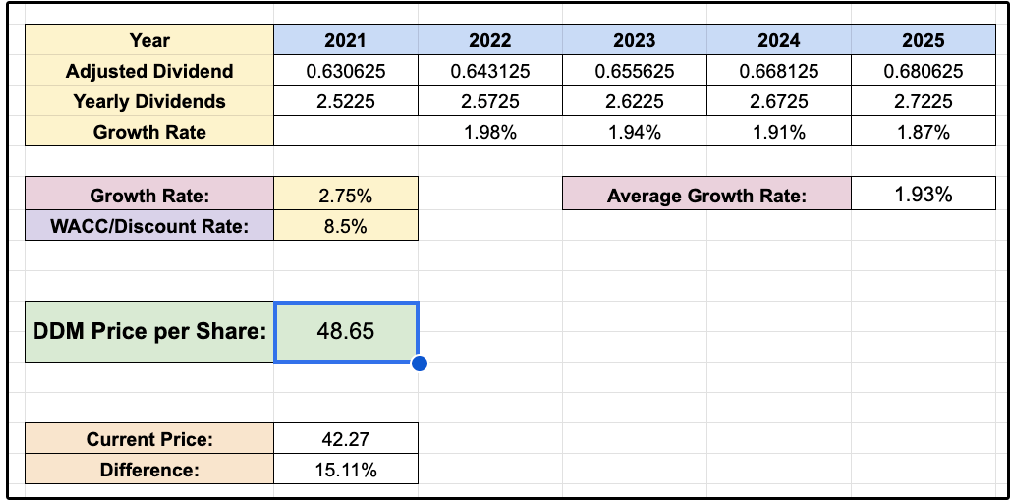

1. 📡 Verizon (S&P 500)

Verizon is one of the few stocks in the S&P 500 that currently yields more than 6%.

The company is currently only using 57% of its free cash flow to payout dividends.

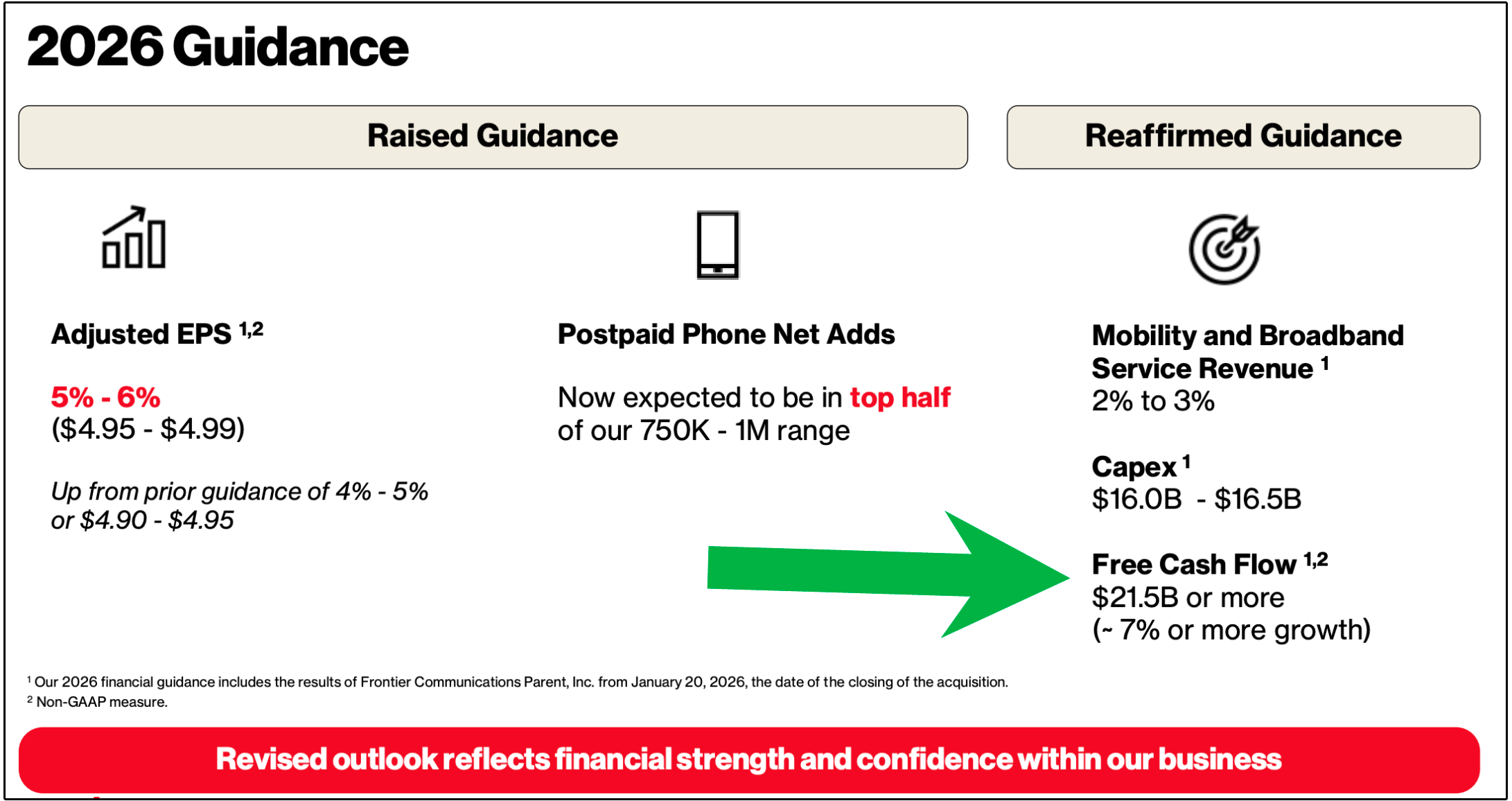

While dividend growth over the last decade has been below the rate of inflation, Verizon’s 2026 guidance is quite promising.

Verizon expects to grow adjusted EPS at 5-6%, while free cash flow is expected to grow at around 7%.

Naturally, this means that Verizon could grow dividends at 7% over the next year without an increase in the free cash flow payout ratio.

However, that isn’t what I expect them to do.

We will likely continue to see modest dividend growth (which will actually strengthen the payout ratios), but Verizon has already started doing something outside the norm for their capital allocation priorities.

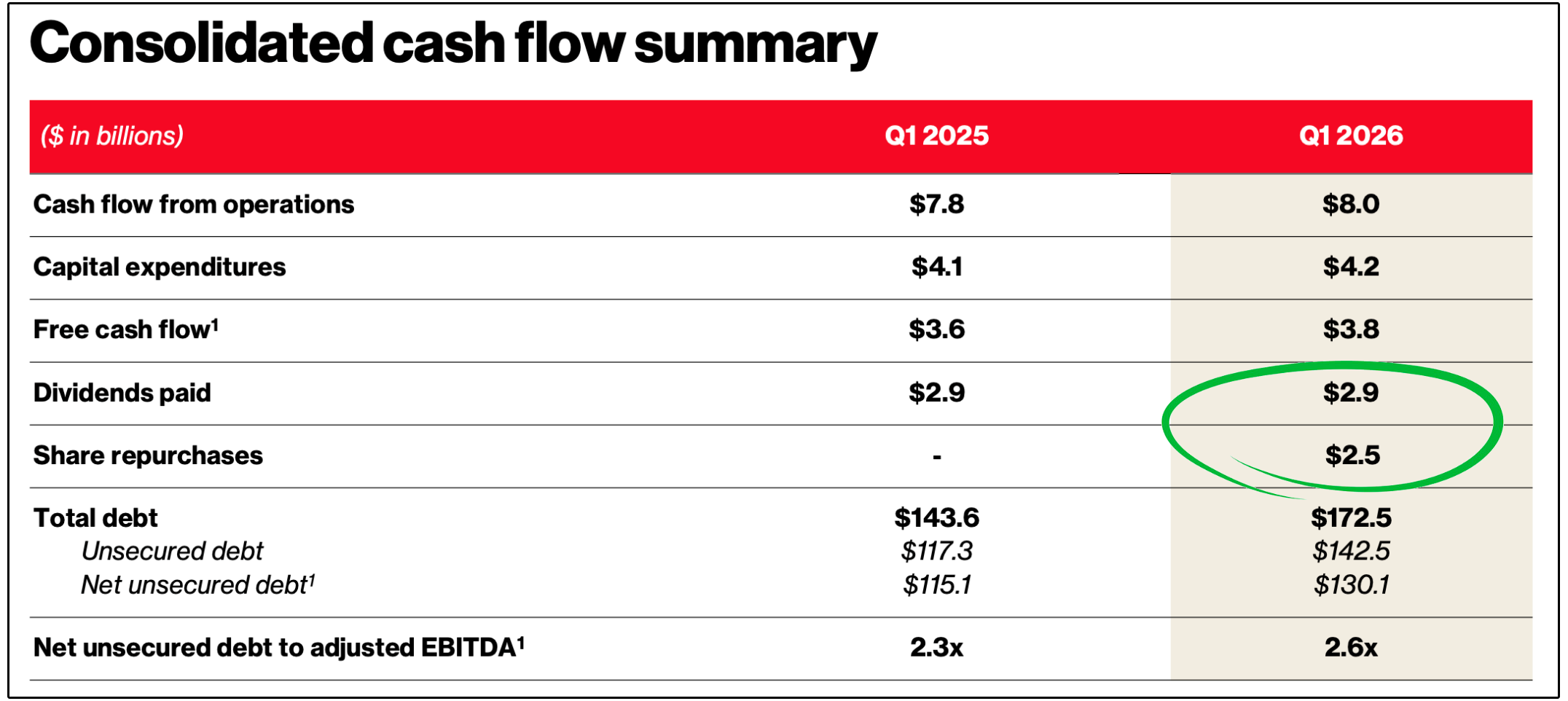

They started buying back shares.

Verizon spent $2.5 billion in share buybacks in Q1 of 2026, compared to $0 last year.

This is a radically different shift compared to the last decade, where shares outstanding were actually increasing.

At the end of 2025, Verizon had approximately 4.226 billion shares outstanding.

Assuming Verizon repurchased shares at an average price of $45:

$2.5 billion ÷ $45 = approximately 55.6 million shares repurchased

That would reduce the share count to approximately 4.170 billion.

Before the buyback:

$2.83 annual dividend × 4.226 billion shares = approximately $11.96 billion in total dividend payments

After the buyback:

$11.96 billion ÷ 4.170 billion shares = approximately $2.87 per share

That means Verizon increased its dividend per share by approximately 1.3% without increasing its total amount of capital it’s using to payout dividends.

Not only are Verizon’s overall dividend payouts strong, their payouts on a per share basis are getting even stronger.

If Verizon achieves just 2.75% dividend growth moving forward, that would imply over 15% upside from current prices.

Now, let’s leave the S&P 500 to find even higher yields with sustainable dividends…

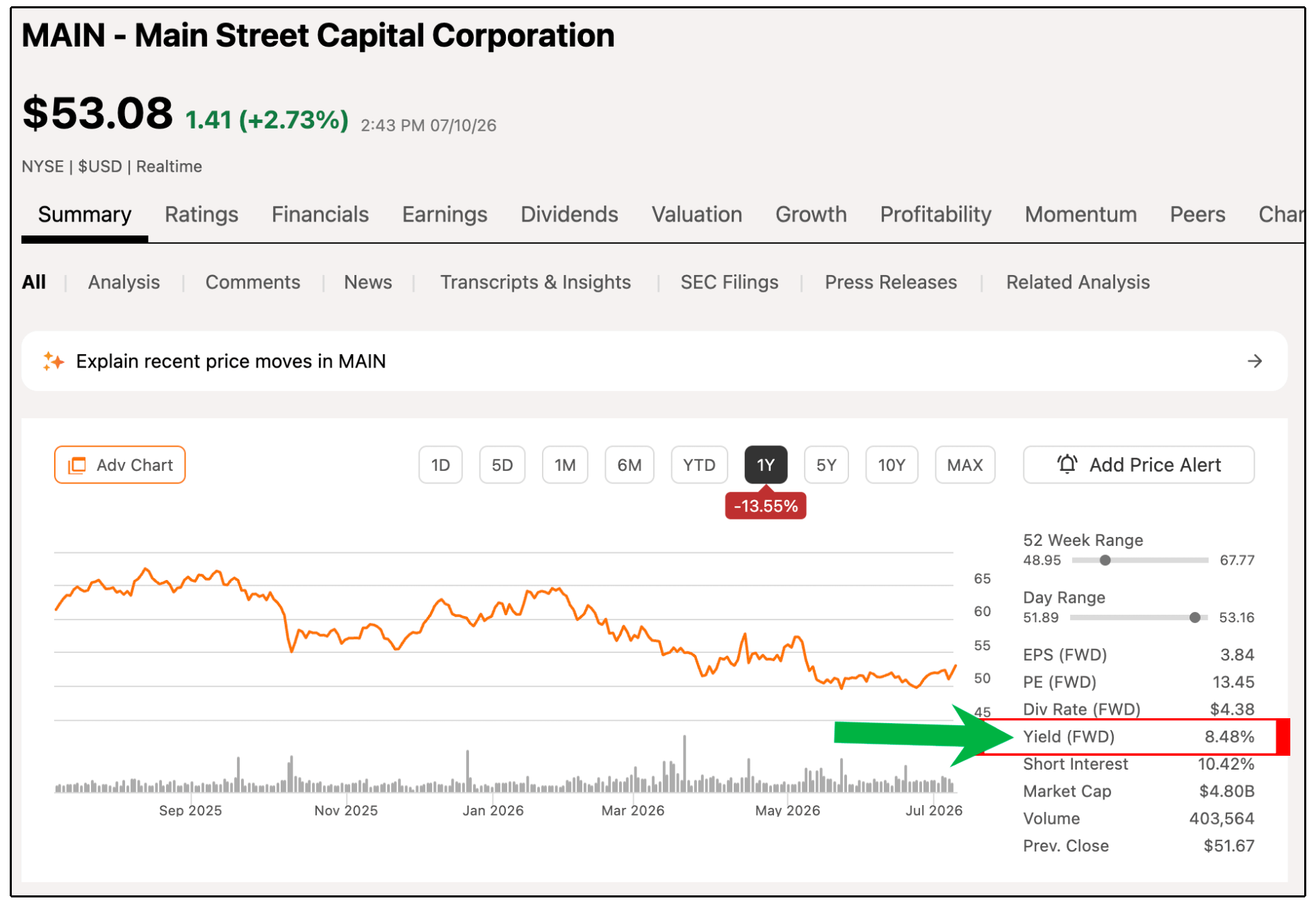

2. 💼 Main Street Capital (BDC)

Main Street Capital is one of the greatest monthly paying dividend stocks of all time, and their historical outperformance proves it.

They’ve paid out monthly dividends since their IPO, and have never cut the base dividend payments.

Right now, their starting yield is sitting at 8.48%.

Main Street Capital is a business development company (BDC), which means they essentially lend money to and invest in small and mid-sized private businesses, then distribute most of the income it earns to shareholders.

This is important to note, as BDCs typically have two yields:

Base dividend yield

Total dividend yield

The base yield is the yield we should (hypothetically) be guaranteed to get.

Anything above that is considered “special dividends” that depends on how much extra income a BDC is generating in the moment.

Here is Main Street Capital’s dividends paid, as well as special dividends in green.

Base dividends should be more stable, special dividends can fluctuate greatly.

BDCs don’t pay dividends out of GAAP earnings-

They pay from Net Investment Income (NII), which reflects the interest and fees collected on their loan portfolios.

Here is the formula for base dividend coverage:

Dividend Coverage Ratio = Net Investment Income (NII) / Dividends Paid

MAIN recently increased its regular monthly dividend to $0.265 per share.

That equals $0.795 per quarter or $3.18 per year.

The company also pays a $0.30 quarterly supplemental dividend, bringing the total annualized payout to $4.38 per share.

But the regular dividend and supplemental dividend should be viewed differently.

Management expects second-quarter DNII of at least $1.00 per share.

Compared to the $0.795 regular quarterly dividend, that gives MAIN base-dividend coverage of approximately 1.26 times.

In other words, the company is generating about $0.205 more per share than it needs to fund the regular dividend.

That is one of the stronger coverage levels in the BDC market.

However, the same can’t be said for the current supplemental dividend.

The regular and supplemental dividends together total $1.095 per quarter, meaning DNII of $1.00 would leave a shortfall of approximately $0.095 per share.

If DNII remained near $1.00 per quarter, MAIN would generate roughly $4.00 per share annually.

That would comfortably cover the $3.18 regular dividend, but fall about $0.38 short of the full $4.38 payout.

So while the base dividend is one of the safest in the BDC market, the supplemental dividend is not currently covered by NII.

Most investors get misled because most investing software platforms simply show the total yield for BDCs, when the total yield isn’t guaranteed and oftentimes not sustainable.

In reality, MAIN’s base yield is around 6%.

Anything above that is the result of supplemental dividends.

Let’s see if we can find even higher yields with sustainable dividends.

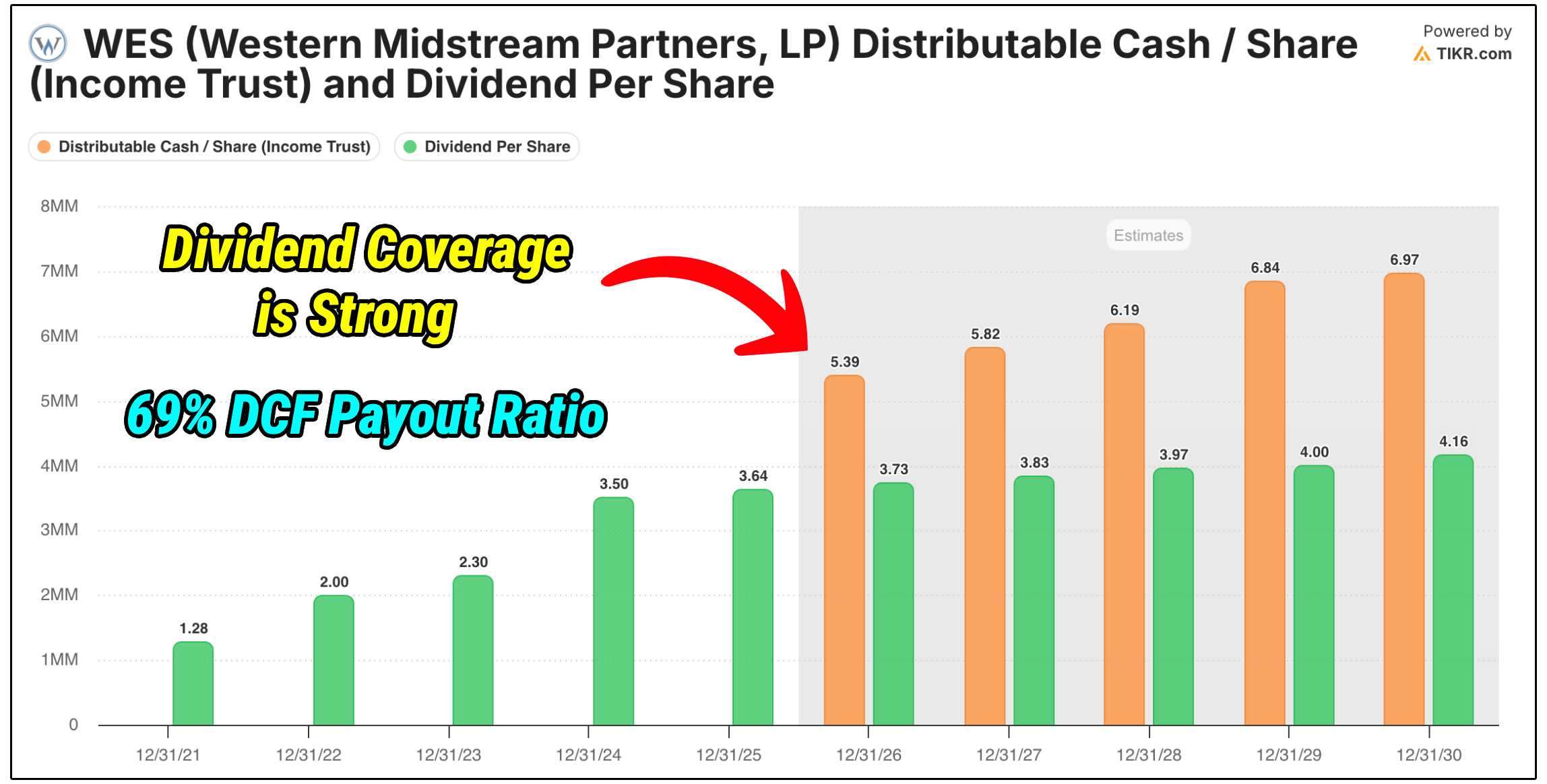

3. 🛢️ Western Midstream Partners (MLP)

Western Midstream Partners was on our list of top high yield stocks to buy going into 2026-

And it’s performed very well since.

The stock was yielding 9.3% at the beginning of the year, yet the stock is already up over 13% in 2026, outperforming the market.

But even with the recent run up in share, the company still yields around 8.3%.

Is that yield sustainable?

For MLPs, we must look at their distributable cash flows.

Western Midstream Partners has strong dividend coverage, with a distributable cash flow payout ratio of just 69%.

With DCF projected to continue to grow, we will likely see some level of distribution growth.

In fact, the company has already announced a distribution increase this year of 2.2%.

WES is a sustainable high yield, that is growing distributions, while outperforming the market.

4. 🏢 Innovative Industrial Properties 9.00% Series A Preferred (Preferred Shares)

Cannabis REITs are considered quite risky due to the weakness of their tenants.

However, the preferred shares, specifically for Innovative Industrial Properties, are a completely different situation.

The preferred shares currently yield 9.2%, and also enjoy some unique advantages:

Priority over common shareholders: Preferred shareholders must receive their dividends before any dividends can be paid to common shareholders.

Cumulative dividends: Any missed preferred dividends accumulate and must be paid before the company can resume distributions to common shareholders.

Greater dividend protection: Innovative Industrial Properties would need to suspend its common dividend before eliminating the preferred dividend, creating an additional layer of protection for preferred shareholders.

Perhaps what is most impressive is this:

The company can currently cover their preferred dividend 48 times over!

Even with some tenant issues, the preferred shares are paying one of the safest 9.2%+ yields I’ve seen.

These are the opportunities that get completely overlooked by the market.

🛡️ The High Yield Lie

It’s true that many high yield stocks are dangerous.

In fact, a majority of them are.

But the idea that all high yields are dangerous couldn’t be further from the truth.

Most people approach high yield investing the same way they play the old game minesweeper.

They start going around randomly clicking on squares, and maybe make a few lucky guesses-

But they are basically guaranteed to hit a mine eventually, ending their game.

Of course, if you know what to look for, you can strategically avoid the mines, and win the game.

This is a perfect metaphor for high yield investing-

And it’s why our High Yield Portfolio has done so well in 2026, while yielding 9.3%.

Like always, if you want to get access to our High Yield Portfolio, as well as the Dividendology Database where we compile in depth data on high yield asset classes-

Then you can join us here:

See you soon.

Dividendology

Check out these resources:

Tickerdata 🚀 (TICKERDATA SUMMER SALE (CODE: ‘HEAT’ FOR 30% OFF)

Interactive Brokers 💰 (My favorite place to buy and sell stocks all around the world!)

Seeking Alpha 🔥 (Research stocks $30 off! + 7 day free trial)

HYSA 📊 (Get Access to the Best High Yield Savings Accounts!)