💰 How to Pay $0 in Dividend Taxes in 2026!

Living Off Dividends & Paying $0 Taxes 🔥

One of the best kept secrets of the tax code in 2026?

The fact that under the right circumstances…

You could pay $0 in taxes on dividends.

To verify exactly how this is possible, I teamed up with my CPA friend, “The Money Cruncher”.

If you enjoy this breakdown, be sure to subscribe to his free newsletter!

💰 Pay $0 in Dividend Taxes

Dividends are one of the most efficient investment returns.

Did you know that you can actually live off $131,100 of dividend income and pay $0 in federal taxes in 2026?

Here is a screenshot directly from a tax software:

Generating $131,100 of federal tax-free money is equivalent to generating a salary of $165,000.

In other words, you would need to earn $165,000 from your day job to have the exact same net pay of $131,100 with qualified dividends.

Remember, the tax code wasn’t designed for employees.

It was created for business owners and investors to help circulate the economy and get rewarded for the risk they take.

As such, once you invest your capital in dividend producing stocks or ETFs, you are rewarded with preferential tax rates.

Different tax rates than those applied to a regular 9–5 job.

💭 How Does This Work?

Qualified dividends get a preferential tax treatment.

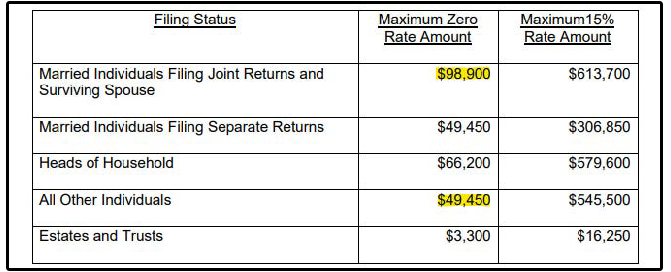

According to the IRS, if your taxable income is less than $98,900 and you file jointly, you will pay $0 in long term capital gains tax.

These numbers are based on the taxable income, which means that it’s after the standard deduction is applied.

Because of the One Big Beautiful Bill Act (OBBBA) the standard deductions have been increased for 2026, and subsequently for future years.

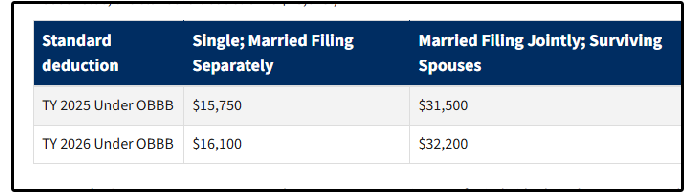

For 2026, these are the standard deduction amounts:

The standard deduction is $32,200 for married individuals, or $16,100 for single individuals.

So here is how you can calculate the maximum amount you can generate in qualified dividends and pay $0 in federal taxes:

If you are filing as single, you can generate $65,550 of qualified dividends and pay $0 in federal taxes. That’s equivalent to almost an $85,000 salary!

The nice part about receiving dividends is that they are not subject to FICA taxes (Social security/medicare), unlike your W-2 wages are.

This is why they are also much more tax efficient than wages.

Because of the new OBBBA, a temporary senior deduction was introduced for 2026-2028.

Taxpayers age 65+ can deduct an extra $6,000 ($12,000 for married couples), on top of the existing standard deduction.

The deduction begins to phase out once gross income exceeds $75,000 ($150,000 for joint filers).

As a result, some seniors could end up paying $0 in taxes even if their dividends exceed $131,100!

Now, this applies only to federal taxes.

You might still need to pay state taxes, unless you live in one of the following states:

Alaska

Florida

Nevada

South Dakota

Tennessee

Texas

Wyoming

These states don’t tax dividend income.

One concern many people have is “What about inflation? I can’t live off this amount forever!”

But, living off dividends can actually be quite sustainable even with inflation.

Tax brackets and deductions get adjusted with inflation

For example, the standard deduction in 2025 was $15,750 instead of 1$6,100.

The tax bracket went from $48,350 to $49,450.

So these numbers always get adjusted with inflation. However, it’s important to note that the future legislation might change the amounts/tax.

Selecting stocks/ETFs with a long record of annual dividend increases

The second way you can protect yourself against inflation is by selecting high quality stocks/ETFs.

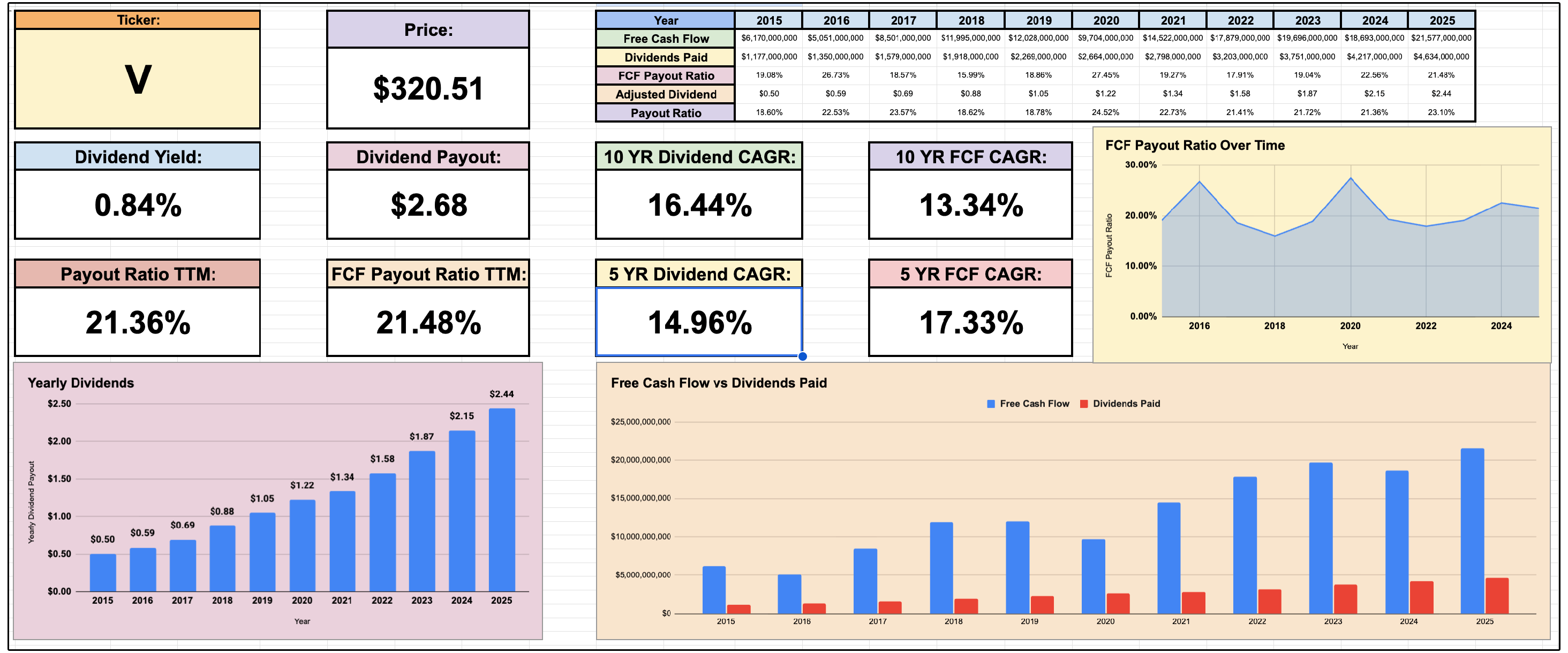

For example, Visa’s average 5 year dividend growth rate is 14.96!

That’s a lot higher than the annual inflation.

Along with tax brackets inflation adjustment, you will outpace inflation easily and shouldn’t be too concerned about it.

⚠️ What if I have other income types?

Even if you have other income types, such as wages, Required Minimum Distributions (RMDs) from retirement accounts, or Social Security income/pension, as long as your taxable income is below the thresholds, your qualified dividends will be taxed at 0%.

This is why it’s important to plan around your other income items!

What if I earn even more dividends?

The nice part is that only the amount above the threshold is taxed at the next rate of 15%.

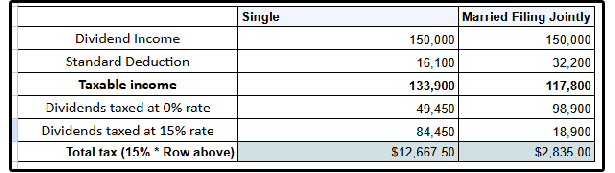

Say you generated $150,000 of qualified dividends, here’s how it would look:

So, if you are single, you would pay a 9.4% effective tax rate, or 2.4% if married.

You would’ve paid a 22-24% marginal tax rate + FICA taxes of 7.65% on a $150,000 salary!

The tax code heavily favors dividend investors.

Quick note: in order for your dividend to be qualified, it must be paid by a U.S. company (or qualified foreign company) and you must hold the stock/ETF for at least 61 days during the 121-day period.

If you to get access to all Dividendology features mentioned below, then consider becoming a member here:

Check out these resources:

Tickerdata 🚀 (My automated spreadsheets and instant stock data for Google Sheets!)

Interactive Brokers 💰 (My favorite place to buy and sell stocks all around the world!)

Seeking Alpha 🔥 (Research stocks $30 off! + 7 day free trial)

HYSA 📊 (Get Access to the Best High Yield Savings Accounts!)

I love having my dividend play in tax advantaged accounts. Anything with dividends goes to Roth IRA

Am I the only person who is having trouble with google sheets. EPS and p/e ration comes up #N/A