🧾 List of Most Upside Dividend Stocks

Wall Street Price Targets Revealed 🎯

Every month, I compile data on the dividend stocks with the most upside based on Wall Street analysts price targets.

Members will get access to the full list every month, as well as all other Dividendology features.

This month, only 35 stocks made the list.

Let’s dive in.

1. 🖥️ International Business Machines Corporation (IBM)

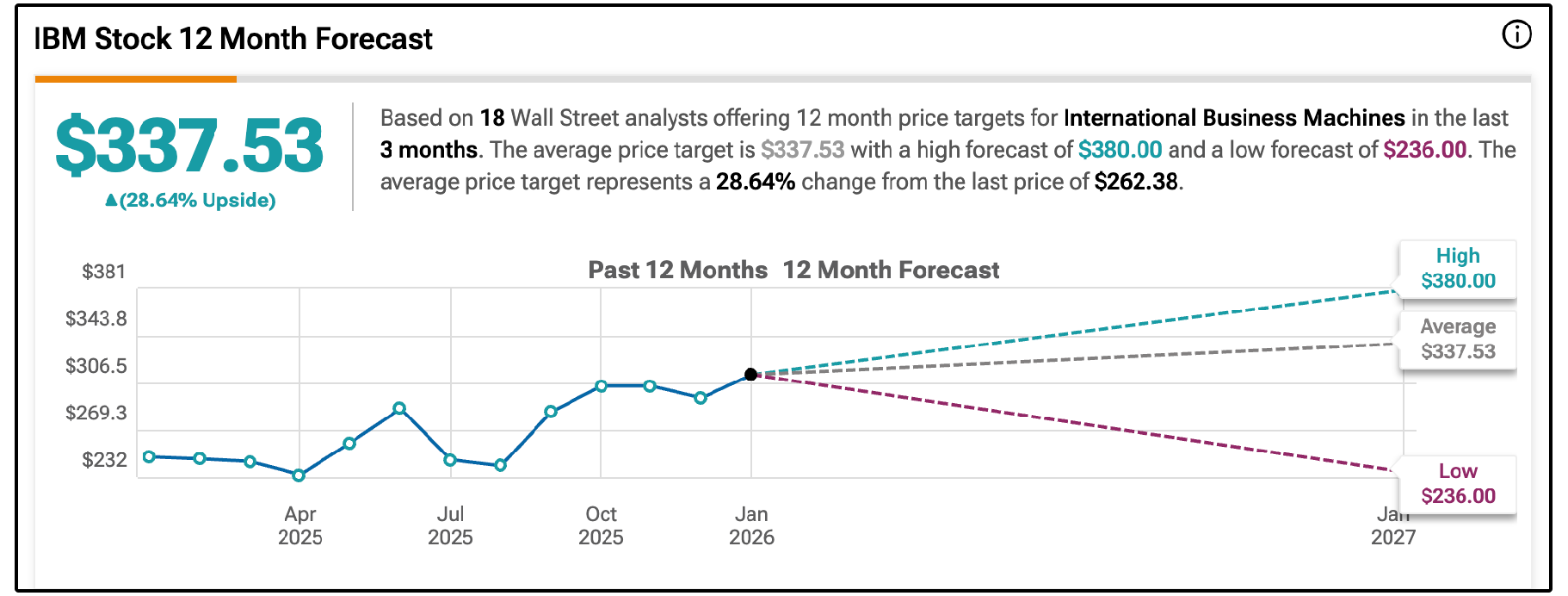

Wall St. Price Target: $338 | Upside: 28.64%

For most of the last decade, IBM was viewed as a slow-moving legacy tech company.

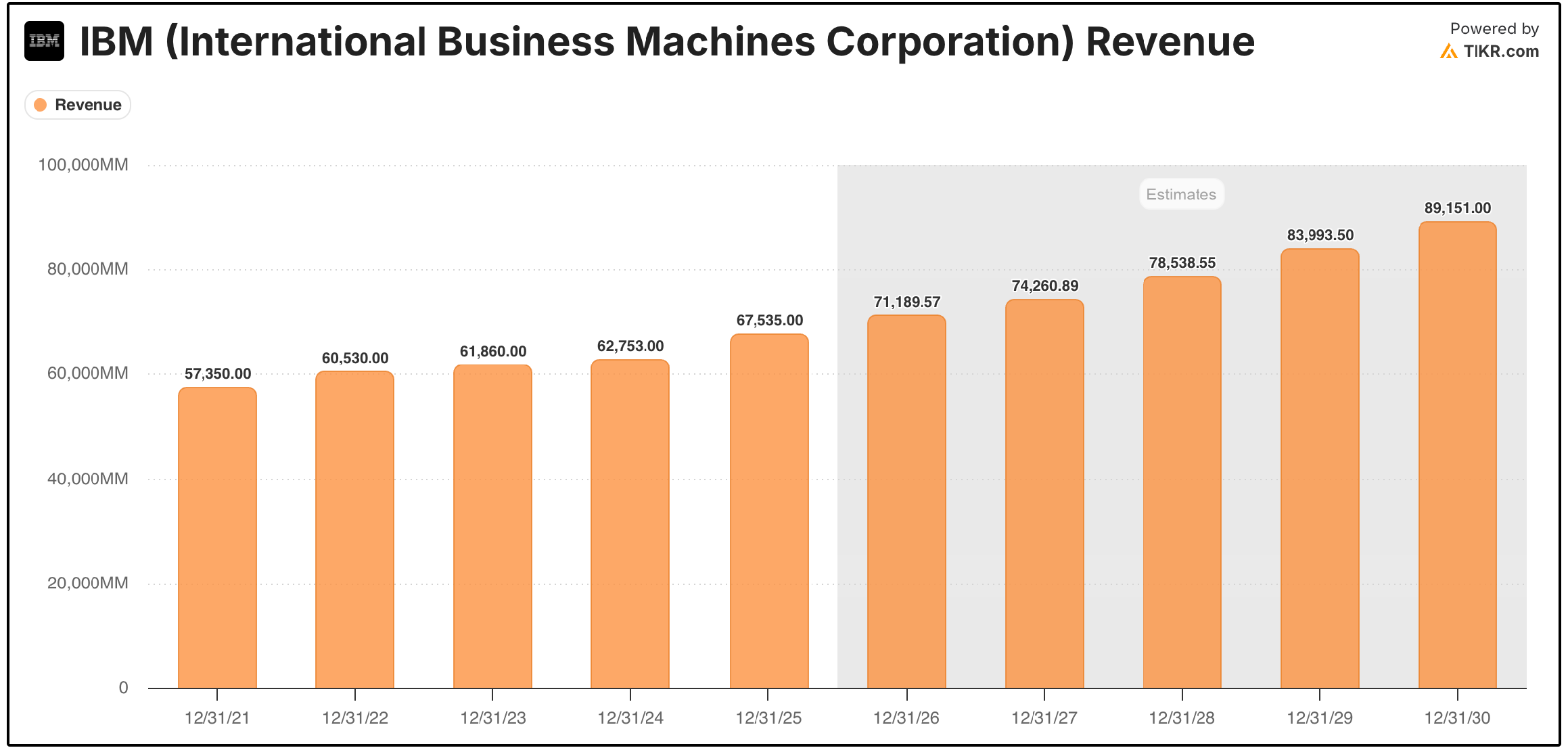

And to be fair, the revenue compounded annual growth rate from 2021 to 2025 was only 4.1%.

This is no longer that IBM.

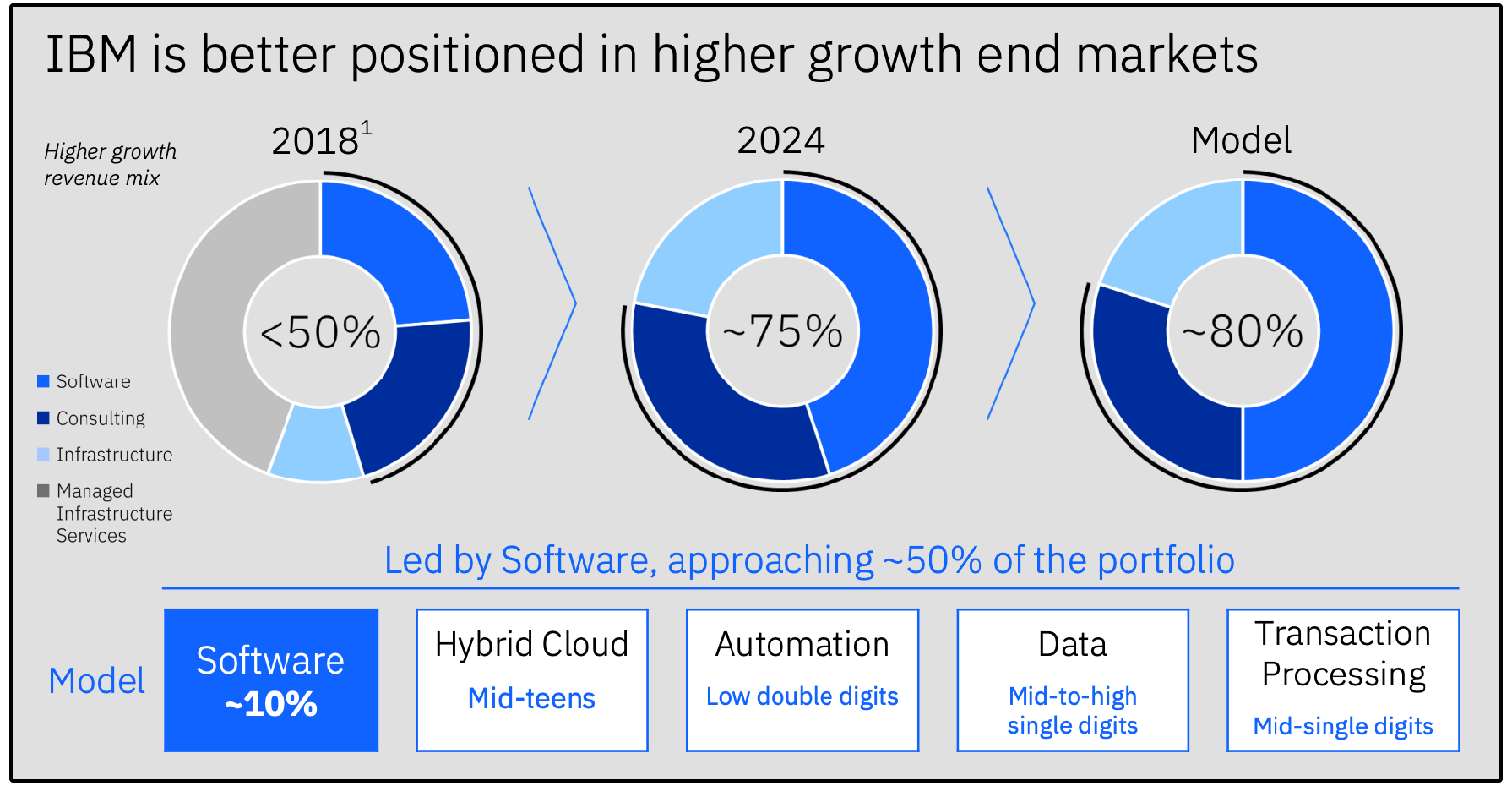

Under CEO Arvind Krishna, the company has repositioned itself around Hybrid Cloud + AI, with three primary business segments:

Software (~44% of revenue | $30B FY25)

Hybrid cloud, automation, data, and transaction processing software. This is IBM’s AI platform layer and grew 9% in 2025.Consulting (~31% of revenue | $21B FY25)

AI and hybrid cloud implementation services for enterprises. Revenue was flat for the year but margins improved.Infrastructure (~23% of revenue | $16B FY25)

Mainframes (IBM Z), Power servers, and support services. This segment grew 10% in 2025, driven by strong demand for the new AI-enabled mainframe cycle.

Software is now clearly the growth engine, but all three segments contributed to 2025’s acceleration.

Management now expects:

• 5%+ revenue growth in 2026

• Software accelerating towards around 10% growth

• Free cash flow increasing another $1B

IBM also reports $12.5B+ in cumulative generative AI bookings, suggesting enterprise demand is building.

However, not everyone (including myself) is convinced.

Despite the $12.5B AI book of business, the majority sits inside Consulting, which only grew 1% in Q4. Backlog rose just 2% to $32B.

In other words, many investors would argue that AI consulting wins may be replacing legacy contracts rather than creating true incremental growth.

Guidance for 2026 revenue growth of ~5% (4.5% constant currency) is decent, but not enough to justify their current valuation in my opinion, which is about 22% higher than they’ve historically traded.

The stock has sold off by around 13% in the last month putting them at a forward P/E of around 21, but their mid-term EPS growth projections only sit at around 6% annually.

Despite this, Wall Street seems to be caught up in the AI hype, giving this stock a price target that gives IBM 28.64% upside.

2. 🔌 PG&E Corporation (PCG)

Wall St. Price Target: $22 | Upside: 18.39%

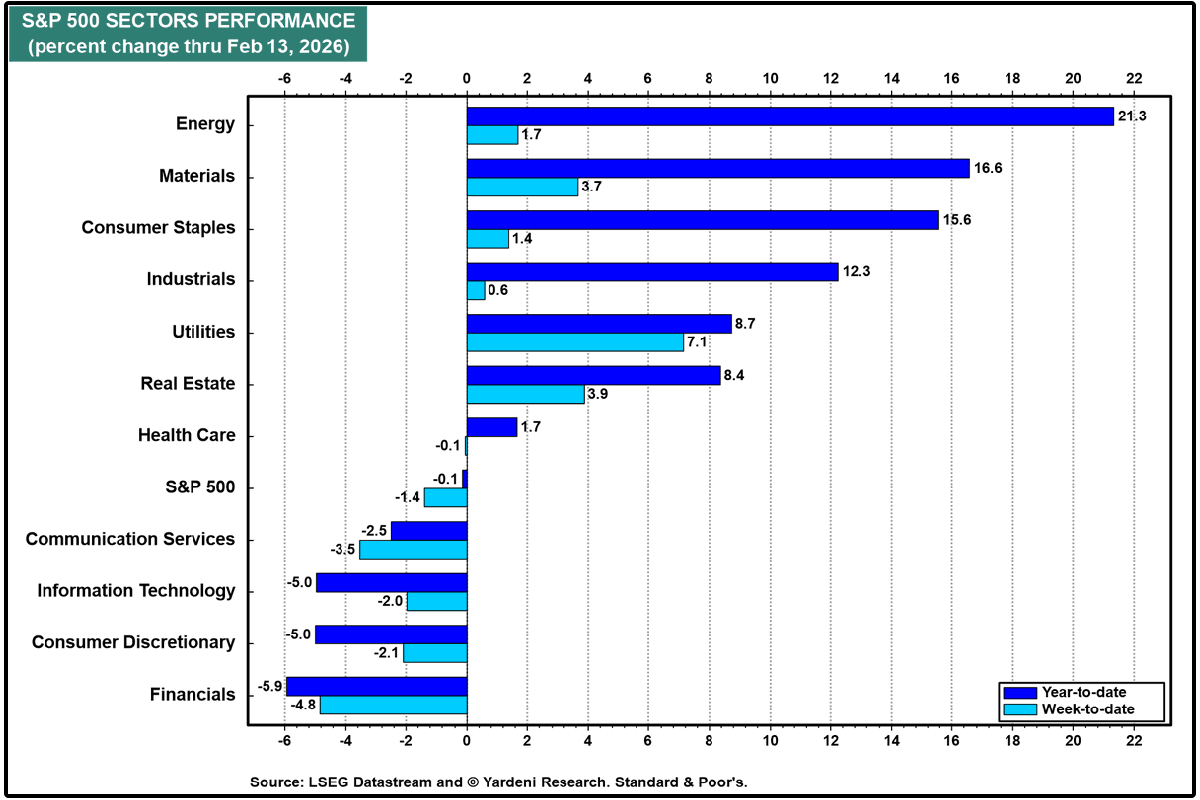

Utility stocks in general have been off to a hot start in 2026, and were the best performing sector last week as well.

PCG is no different, and is already up over 12% year to date.

After years of wildfire liabilities, bankruptcy, and restructuring, PG&E is now in the middle of a multi-year operational and financial turnaround-

And the numbers are finally starting to reflect it.

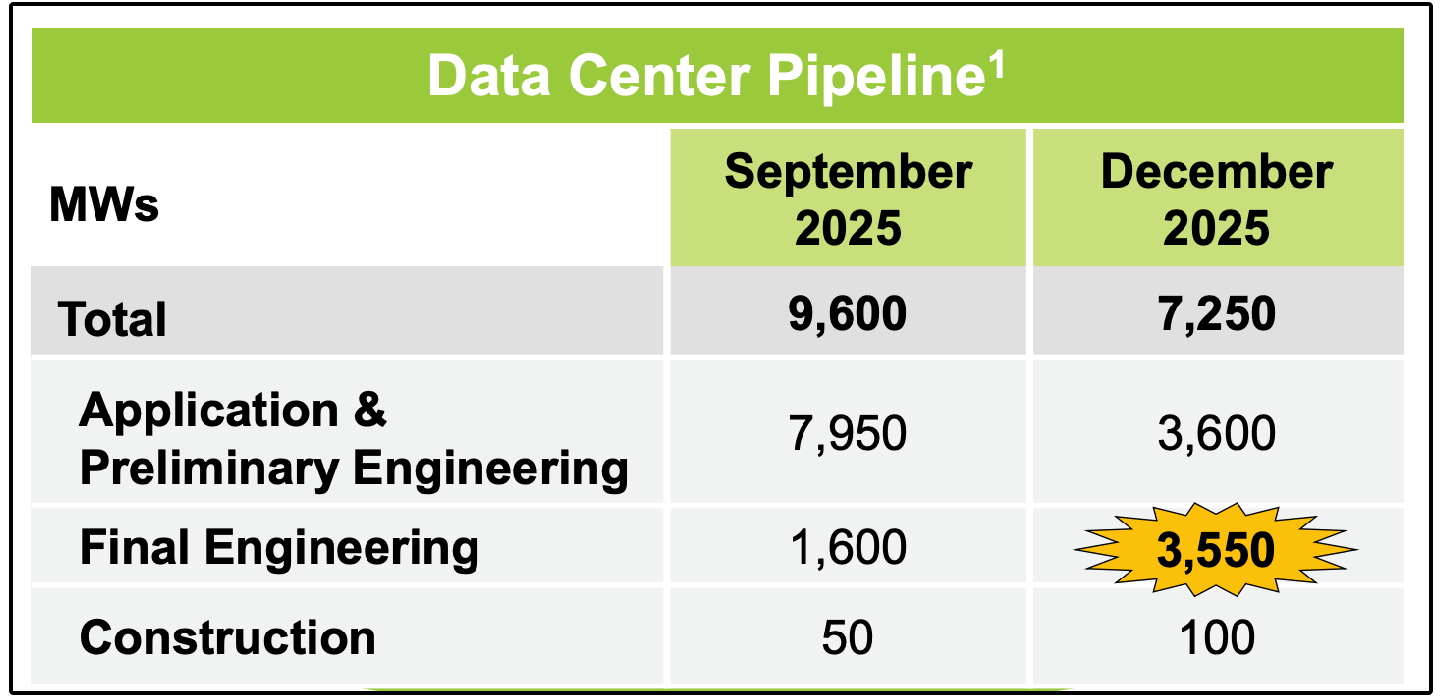

One of the most important developments this quarter was PG&E’s updated data center pipeline.

While total megawatts requested declined from 9,600 MW in September to 7,250 MW in December, the quality of those projects improved significantly.

Projects in final engineering, meaning they are much closer to construction and actual power usage, more than doubled from 1,600 MW to 3,550 MW.

In other words, the pipeline is developing quite nicely.

That matters because utilities only earn returns when electricity is actually delivered.

As more data center projects move from “application” to “final engineering” to “construction,” PG&E gains clearer visibility into real load growth.

And real load growth supports their 9–10% long-term EPS outlook.

On top of this, the company:

Doubled its annual dividend to $0.20 for 2026 (current yield is 1.1%)

Management expects consistent increases over the next two years.

Management is targeting investment-grade credit metrics.

The biggest risk/variable is California legislature, as California lawmakers continue debating how future wildfire costs will be shared between utilities, insurers, and the state.

Wildfire liability reform under SB 254 Phase 2 remains critical.

Management has been clear that if progress stalls or outcomes are unfavorable, all aspects of the capital plan could be revisited.

In other words, while operational performance is improving, Sacramento unfortunately still holds meaningful influence over valuation and risk perception.

This is reflected in the valuation, as PCG is trading at a discount to their historical valuation multiples, despite the fact they are now growing earnings at a higher rate.

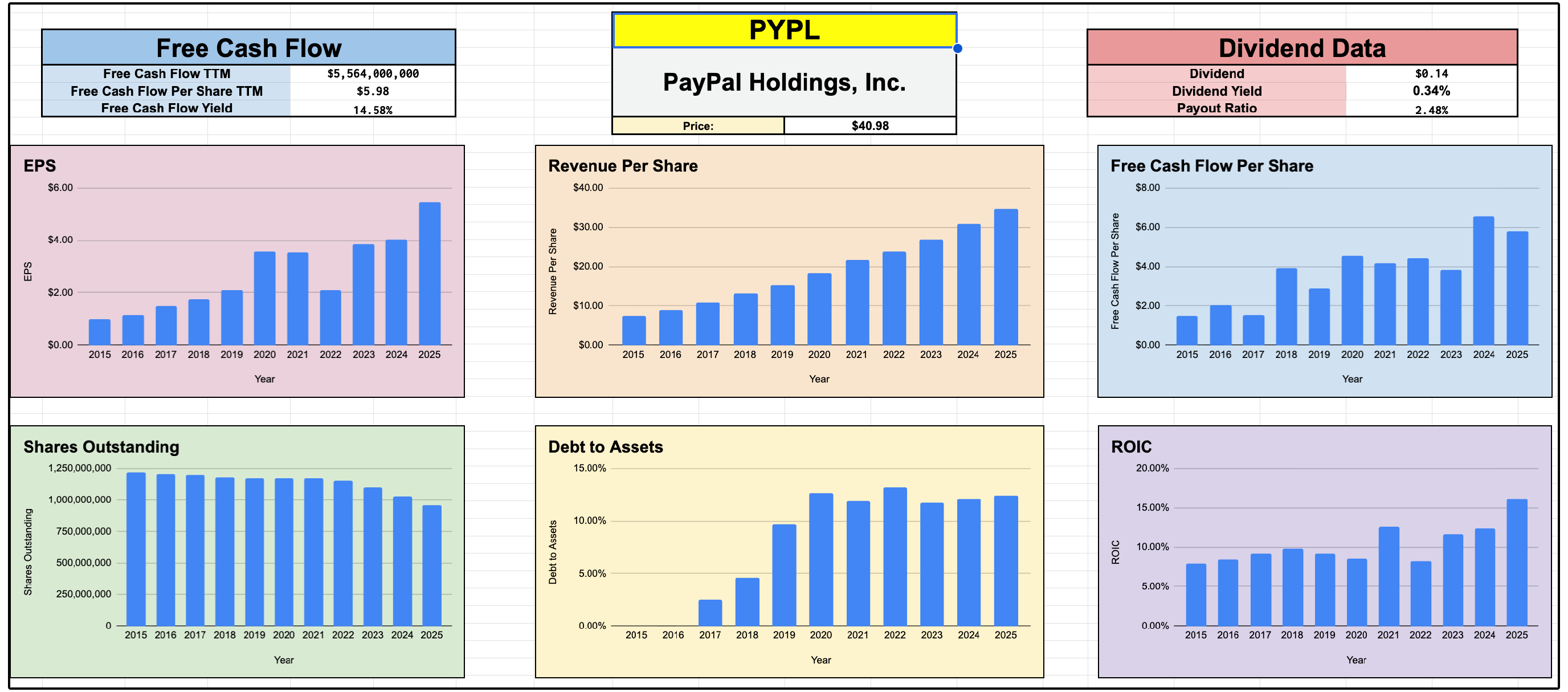

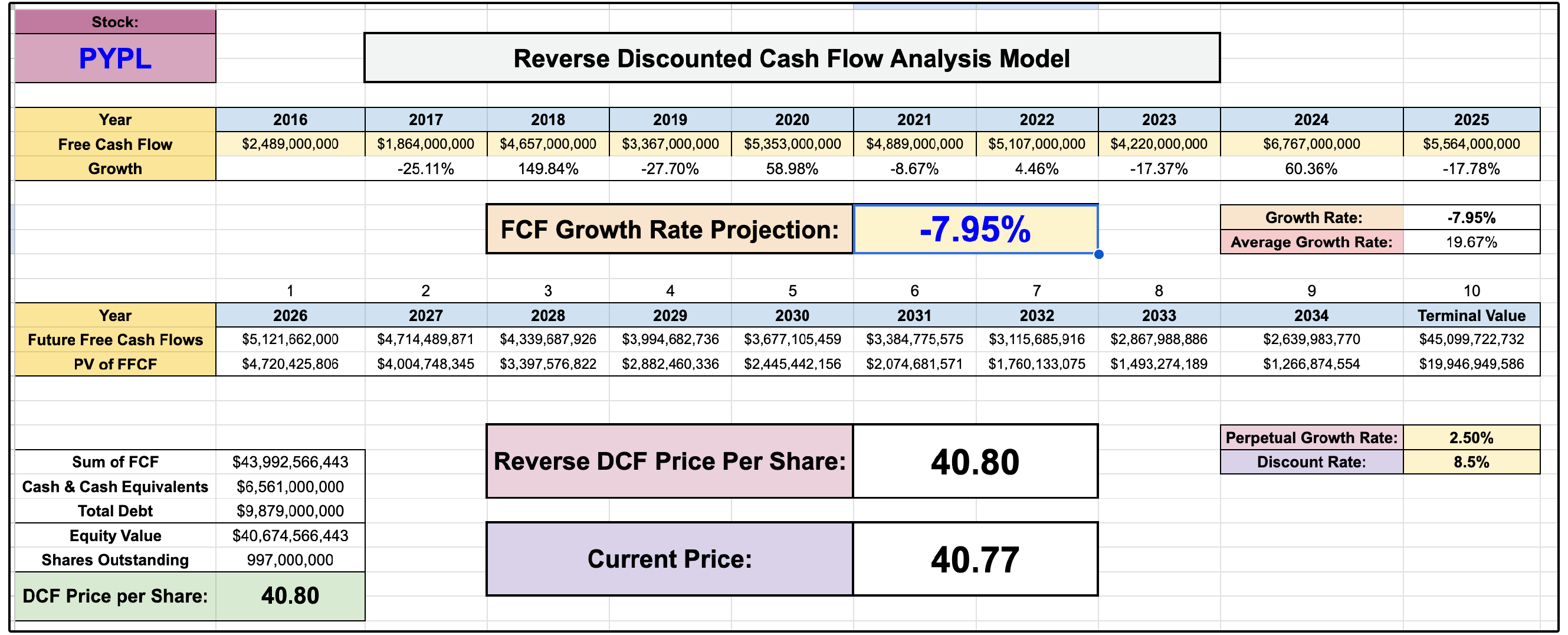

3. 💳 PayPal (PYPL)

Wall St. Price Target: $51 | Upside: 27.3%

PayPal is now down over 86% in the last 5 years, and 47% in the last year.

The performance has been so bad, they’ve started to become the butt of ‘finance jokes’…

For example, I present to you, the new fear & greed index:

PayPal recently reported earnings, and the stock dropped 20%.

They also replaced CEO Alex Chriss with Enrique Lores, HP’s current CEO.

Is PayPal Failing?

A failing business usually shows:

• Falling revenue

• Collapsing margins

• Shrinking user base

• Weak cash generation

PayPal shows none of those… Yet.

So what’s the problem?

PayPal generates most of its revenue from e-commerce.

E-commerce is growing ~7% annually-

But PayPal’s branded checkout volume grew only 1% this quarter.

Investors fear PayPal is losing market share to Apple Pay, Shopify, and others.

Under new leadership, PayPal is now:

• Deploying full feature packages instead of rolling out one tool at a time

• Creating dedicated teams for top merchants

• Aligning merchant incentives to share in conversion upside

• Investing $1.5–$2B back into growth in 2026

That investment will pressure margins short-term, but it’s aimed directly at stopping market share erosion.

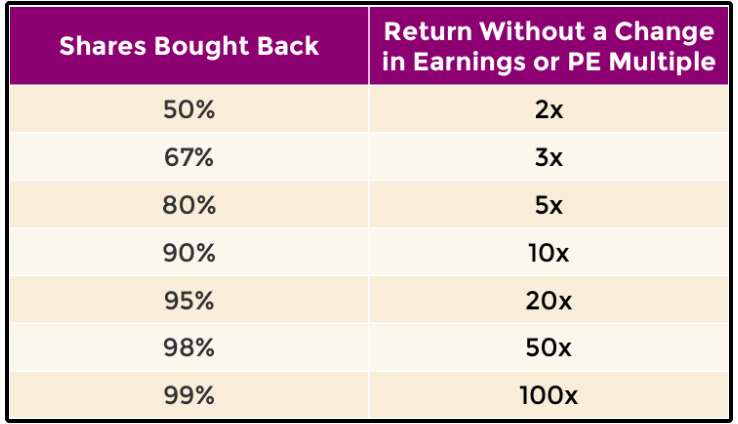

But in my opinion, the real bull case for PayPal right now is the math behind its share buybacks.

As a quick refresher, if a company bought back 50% of its outstanding shares, even without earnings growing or a change in the valuation multiple-

The stock would still double.

So what does this mean for PayPal?

Well, management recently guided towards $6 billion of share repurchases in 2026 alone.

At today’s price of roughly $41 per share, that math becomes very interesting.

$6,000,000,000 ÷ $41 = 146 million sharesThat means if the stock price stayed around current levels, PayPal could retire approximately 146 million shares in just one year.

At the end of 2025, they had 959 million shares outstanding.

That’s a reduction of approximately 15% of the entire company in a single year.

Let that sink in.

That means even if:

Revenue doesn’t grow

Margins don’t expand

The valuation multiple doesn’t change

The stock would climb by 15%.

Ironically enough, reducing shares through buybacks also makes it easier for companies to grow their dividend payments over time.

With that being said, PayPal is priced at peak fear, with the market currently pricing in nearly -8% annual free cash flow growth over the next decade.

While the company is undoubtedly facing serious issues and has lost market share, they seem to be priced as if the company is quite literally set to die.

Now, let’s dive into the full list of dividend stocks with the most upside according to Wall Street.