🧾 List of Most Upside Dividend Stocks

Wall Street Price Targets Revealed 🎯

Every month, I compile data on the dividend stocks with the most upside based on Wall Street analysts price targets.

Members will get access to the full list every month, as well as all other Dividendology features.

This month, only 48 stocks made the list.

To make the list, each stock must:

Pay a dividend

Have a PEG ratio of below 2

Have 20%+ upside based on Wall Street analysts ratings

Let’s dive in.

1. 🖥️ Meta Platforms (Meta)

Wall St. Price Target: $858 | Upside: 39.95%

Despite being one of the most dominant technology companies in the world, the stock has been relatively flat recently.

Every Mag7 stock is currently down year to date, with Meta currently down slightly over 5%.

The company’s core business remains extremely straightforward:

Digital advertising.

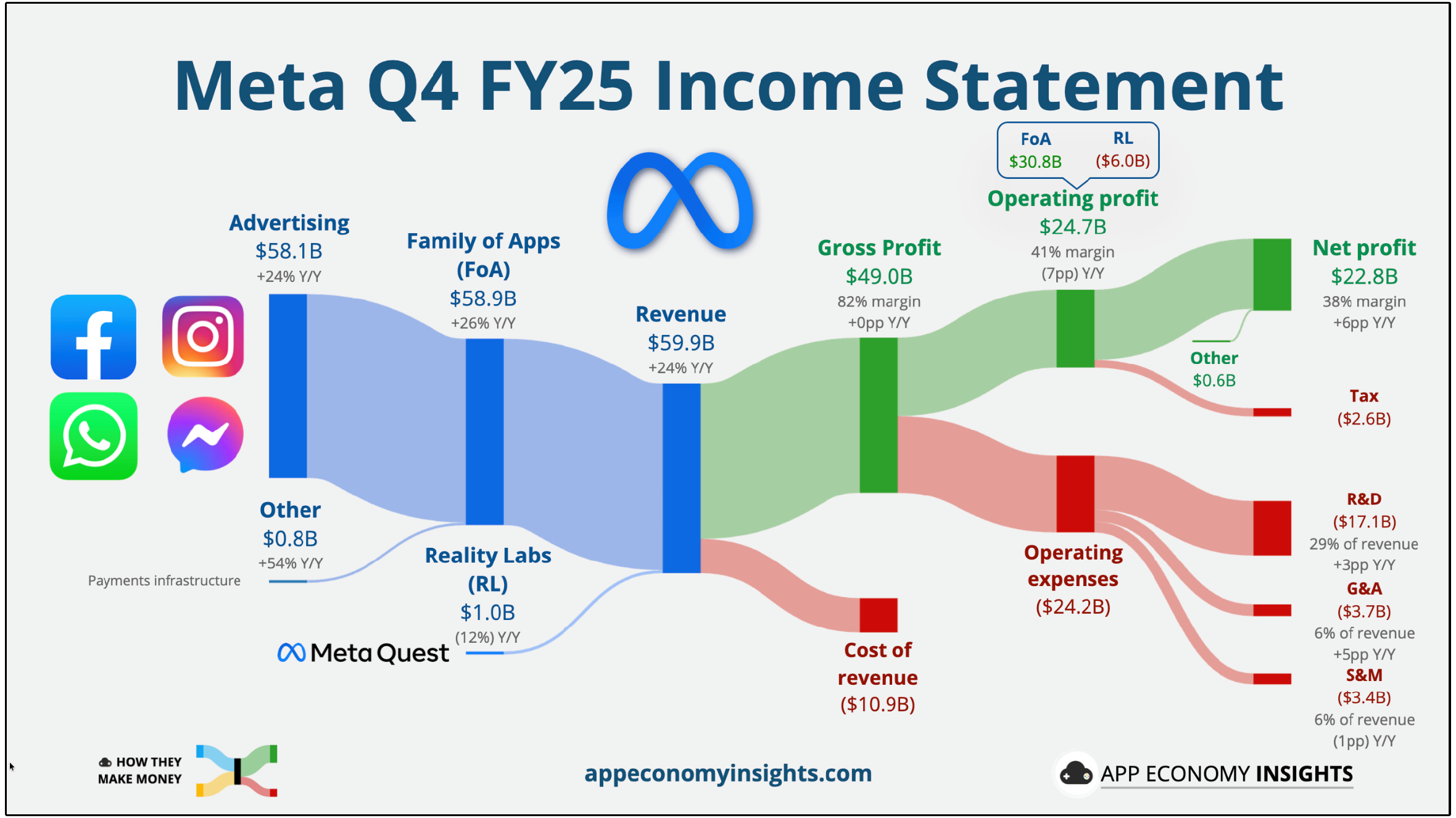

Roughly 99% of Meta’s revenue comes from advertising across platforms like:

Facebook

Instagram

WhatsApp

Historically, this business has compounded at extraordinary rates.

Over the past decade, Meta grew revenue from roughly $17.9 billion in 2015 to more than $200 billion in 2025, representing a 10-year revenue CAGR of about 27%.

The company also operates an extremely efficient business model, with relatively low leverage and consistently strong returns on invested capital, often approaching or exceeding 20%.

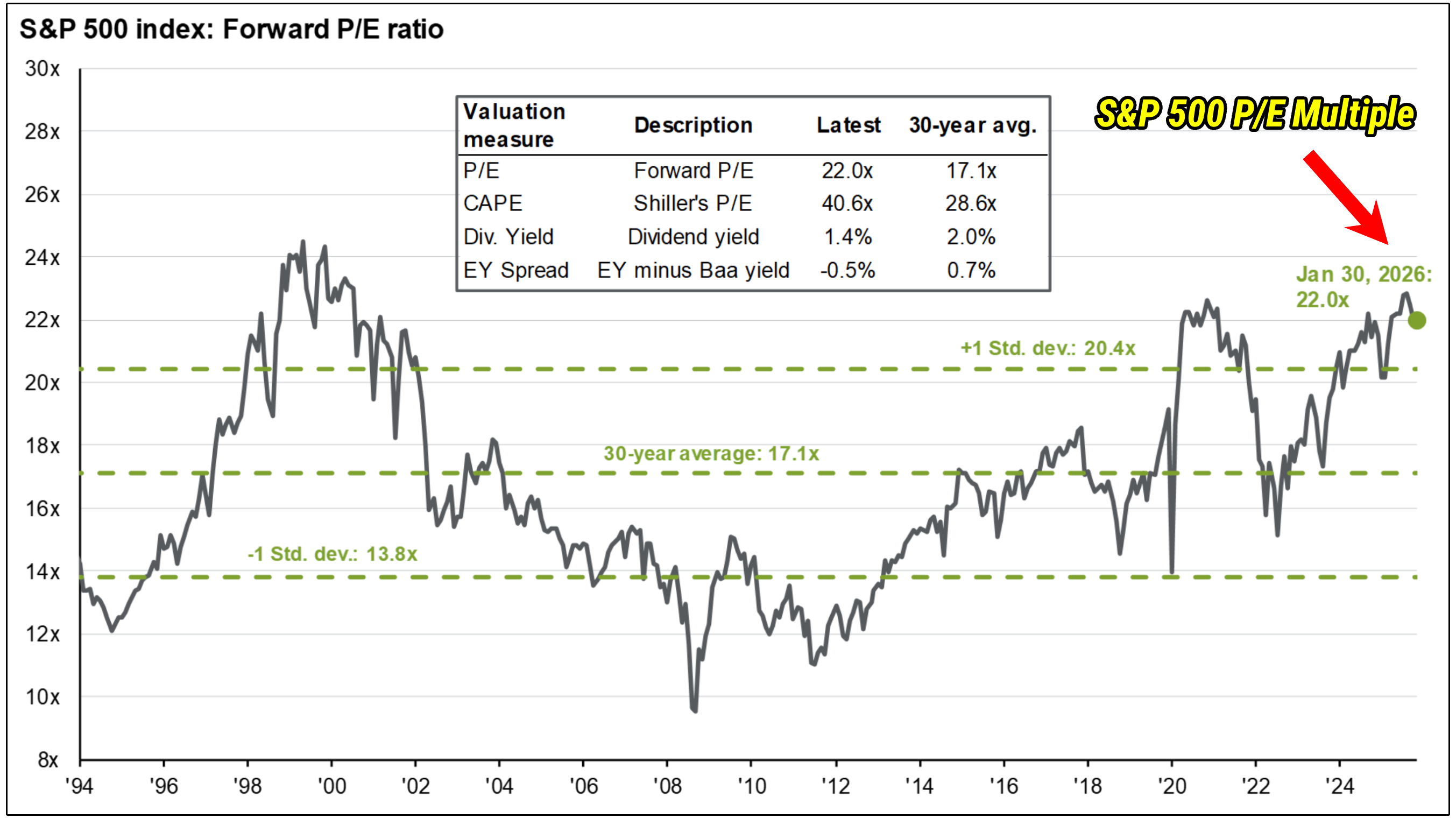

What makes Meta particularly interesting today is its valuation.

The stock currently trades at a forward P/E ratio of about 20.3, which is actually slightly cheaper than the S&P 500, which recently traded at roughly 22x forward earnings.

In other words, investors can buy Meta, a company expected to grow far faster than the overall market, at a valuation below the market average.

According to analyst estimates, Meta’s projected EPS growth over the next 3–5 years is around 22.4% annually.

This combination of strong expected earnings growth and a market-level valuation is one of the main reasons analysts remain highly bullish.

The average Wall Street price target currently sits around $858, implying roughly 34% upside from current prices.

It isn’t just analysts who are paying attention either.

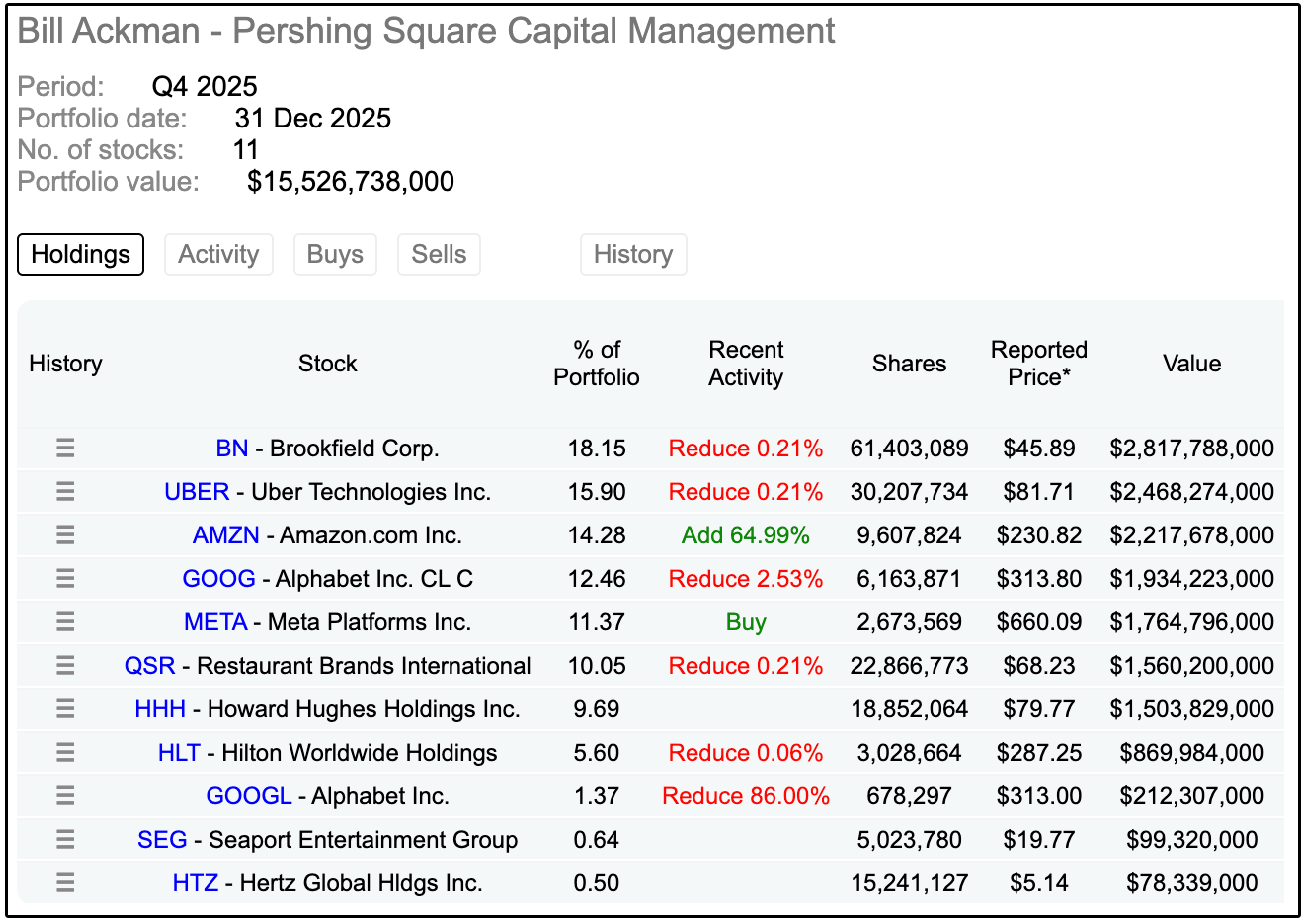

Hedge fund manager Bill Ackman recently initiated a position in Meta, making it over 11% of his portfolio.

More broadly, Meta is also the 6th most widely owned stock among “super investors” (investors managing over $100 million in assets).

Looking ahead, Meta still has several powerful growth drivers.

Revenue growth is largely determined by three factors:

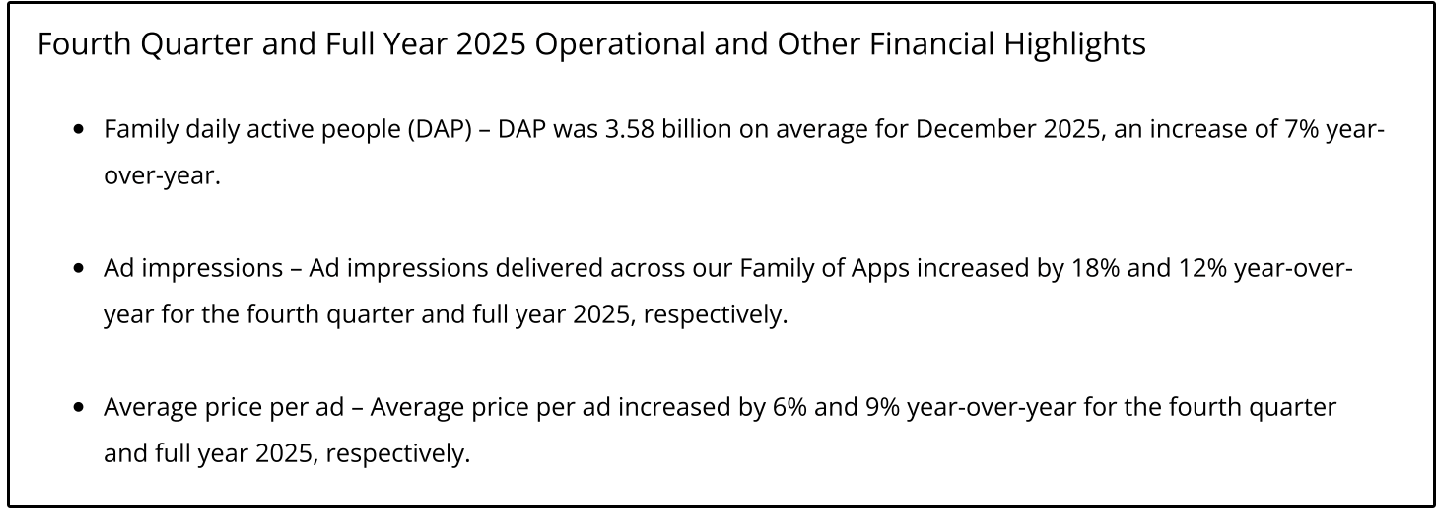

Daily active users

Ad impressions

Average price per ad

In Meta’s most recent results, all three metrics moved in the right direction. Daily active users grew 7% year-over-year, ad impressions increased 18%, and the average price per ad rose between 6% and 9%.

The main concern investors have today is Meta’s rising capital expenditures, largely driven by the company’s aggressive investment in AI infrastructure.

However, the path to monetizing this capex spending is more clear than some of their big tech peers.

AI could ultimately strengthen Meta’s advertising engine by improving ad targeting, increasing engagement, and raising the price advertisers are willing to pay.

Meta also recently introduced a dividend, though the yield remains small at roughly 0.3%. With a payout ratio of only about 11% of free cash flow, the company has substantial room for dividend growth in the years ahead.

Even using conservative assumptions, Meta appears capable of delivering market-beating returns, which is why many analysts continue to view the stock as one of the most attractive opportunities among large-cap tech today.

2. 💼 Accenture (ACN)

Wall St. Price Target: $278 | Upside: 41.79%

Accenture is one of the largest consulting and technology services firms in the world.

The company helps businesses adopt new technologies, improve efficiency, and modernize their operations.

Its services span strategy consulting, technology implementation, operations outsourcing, engineering solutions, and digital marketing.

Its revenue base is also diversified geographically:

50% coming from the Americas

35% from Europe, the Middle East, and Africa

14% from Asia Pacific

Historically, this company has been a phenomenal dividend grower.

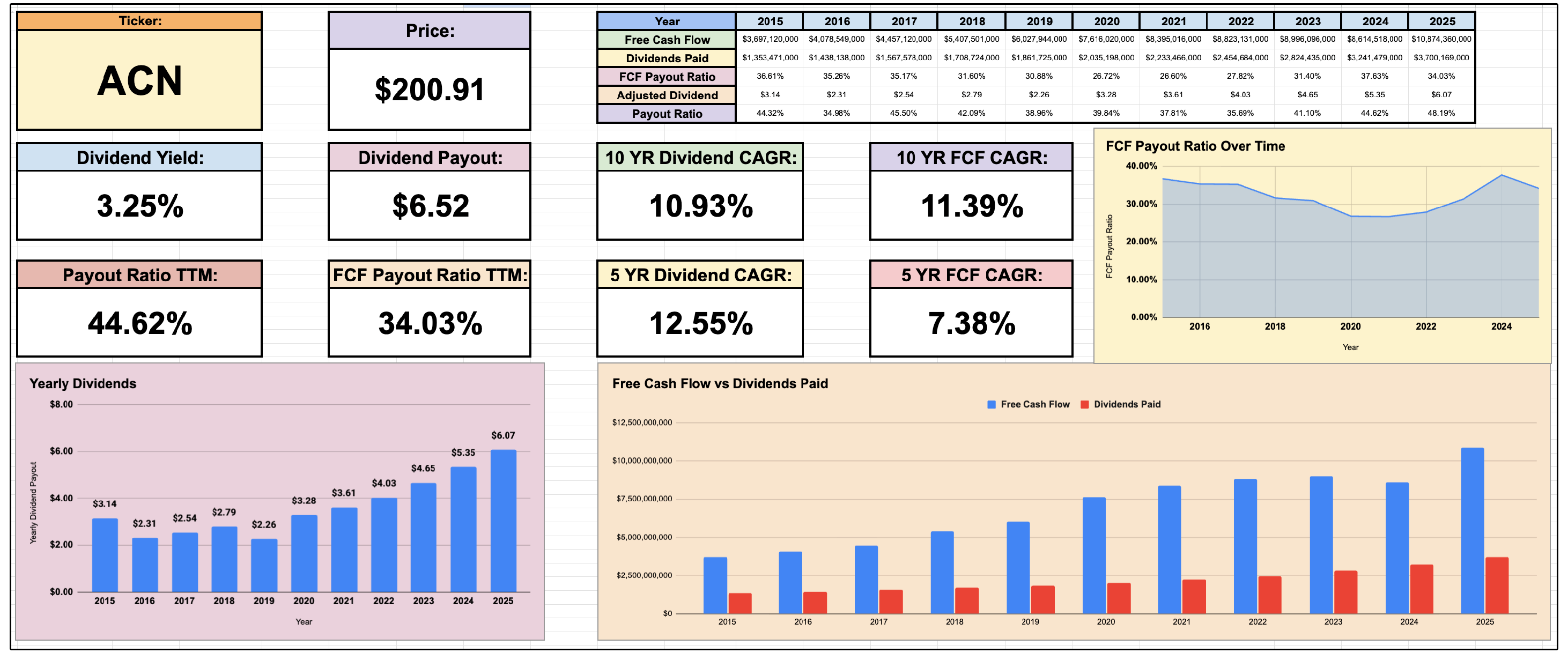

Their current yield is above 3.2%, with an over 12% dividend compounded annual growth rate.

Importantly, this dividend growth has been backed by free cash flow, keeping the free cash flow ratio below 35%.

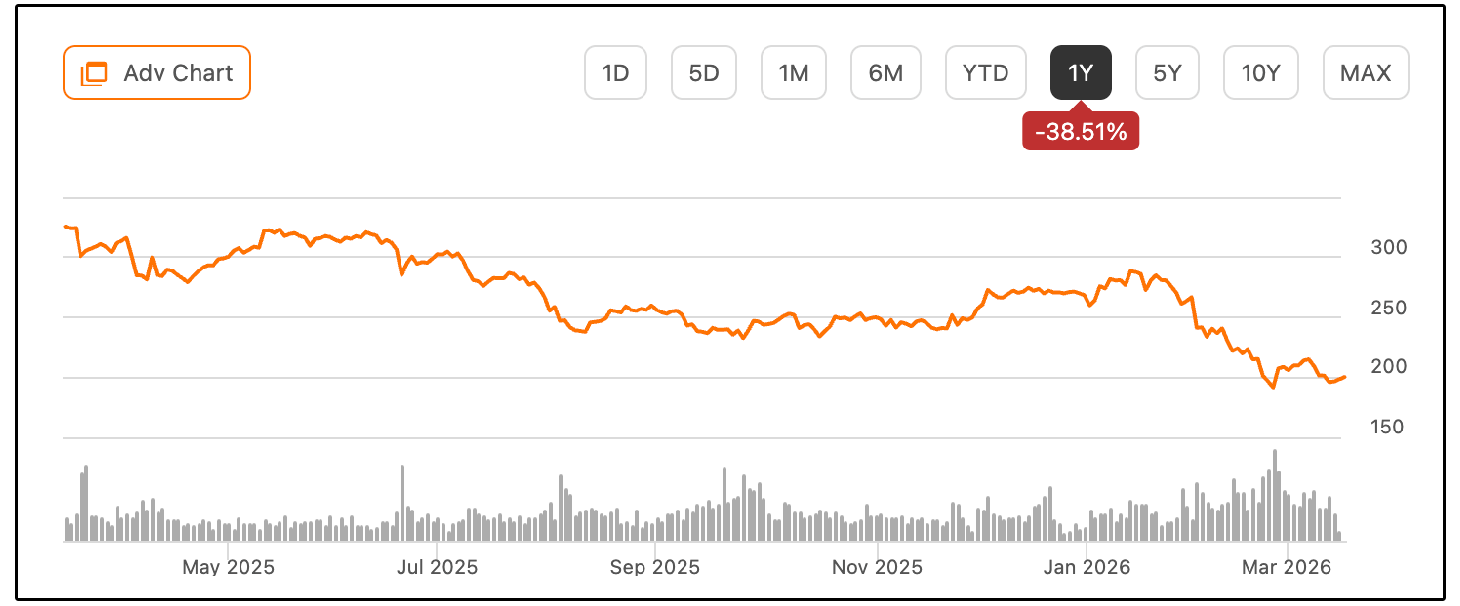

In the last year, ACN is now down by over 38%.

Much of the concern centers around the rise of generative AI.

However, Accenture is already seeing strong momentum in AI-related services.

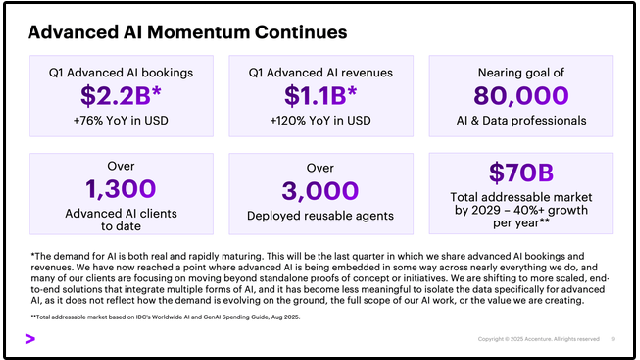

In the company’s most recent quarter, AI revenue increased 120% year-over-year to $1.1 billion, while AI bookings rose 76% to $2.2 billion.

While still a relatively small portion of overall revenue, these numbers do highlight the potential opportunity ahead.

Right now, their 3-5 EPS growth projections sit at around 7% annually.

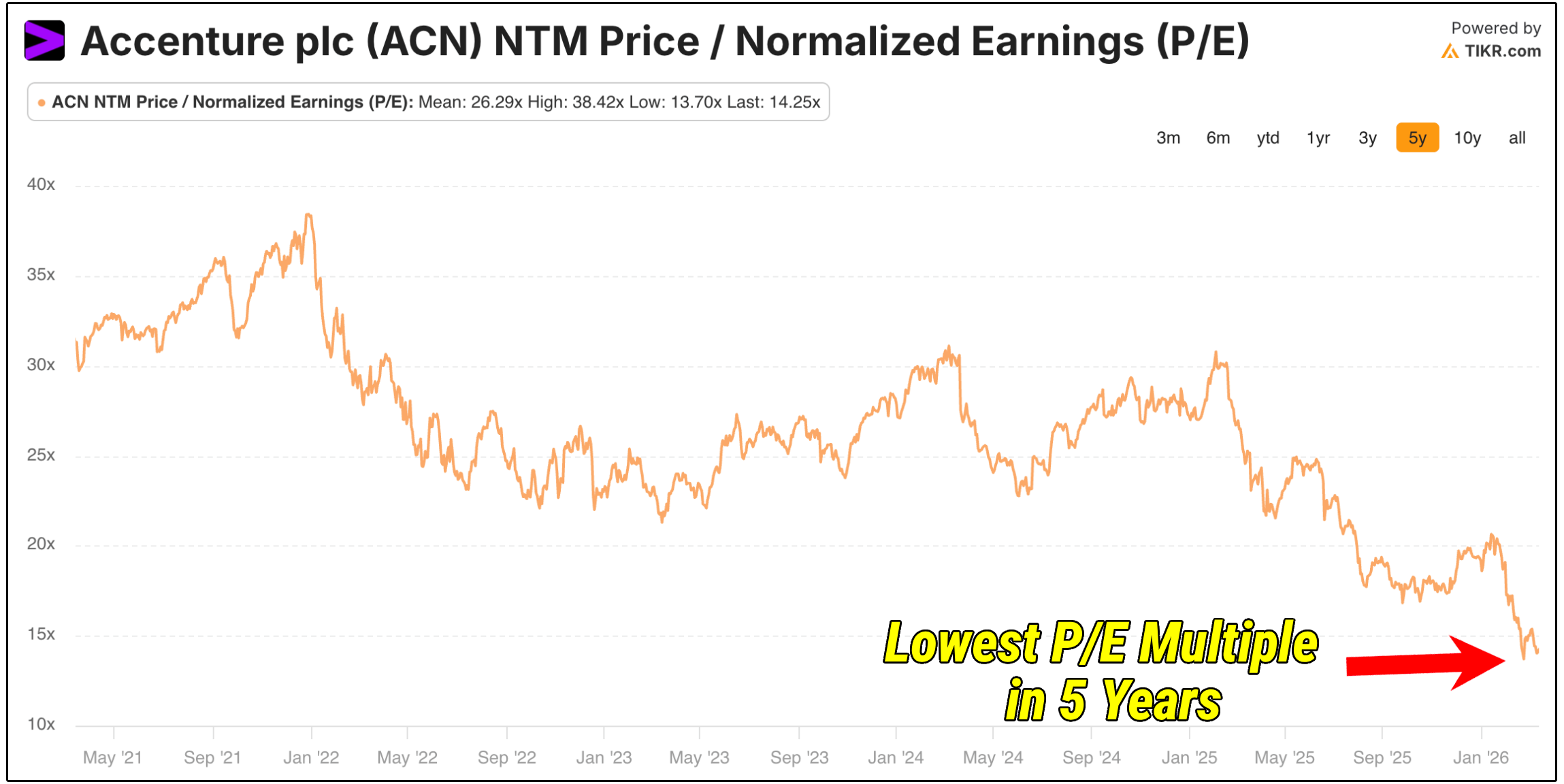

Despite this, they’re currently trading at their lowest P/E multiple in the last five years, sitting at 14.25.

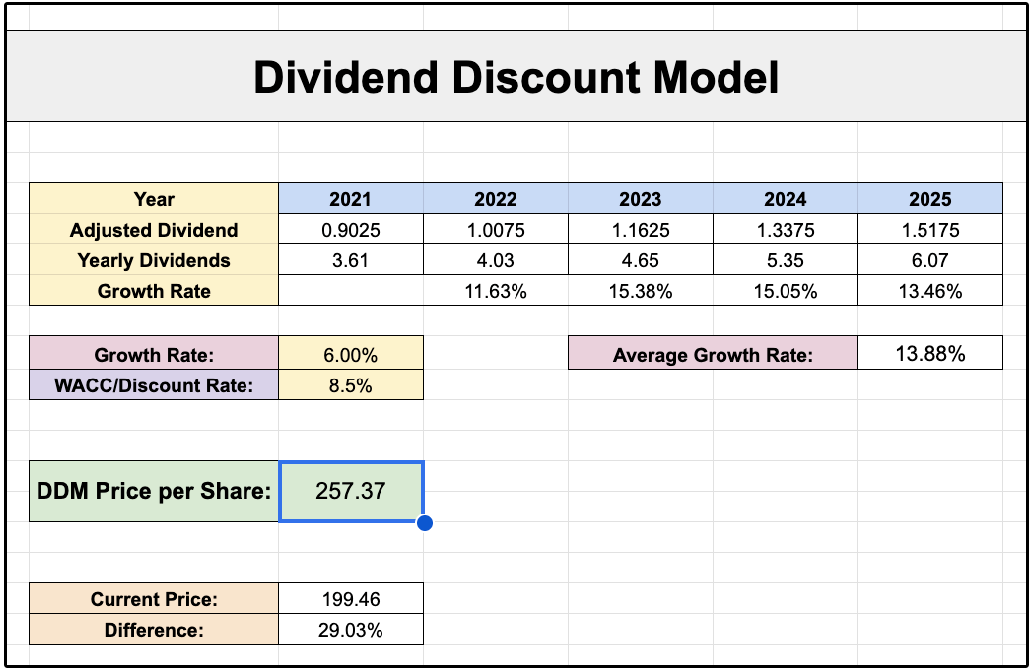

Let’s value ACN with a dividend discount model.

If we assume 6% dividend growth, which should be sustainable moving forward with a low payout ratio and 7% EPS growth projected-

Then we come to a fair value of $257.37.

Accenture clearly faces real risks as AI reshapes the consulting industry.

However, its global brand, deep enterprise relationships, and leadership in digital transformation suggest it is far more likely to benefit from AI adoption than be displaced by it.

3. 🛡️ Brown and Brown (BRO)

Wall St. Price Target: $82 | Upside: 19.82%

Brown & Brown operates a very different type of business than traditional insurance companies.

Rather than underwriting insurance policies and taking on risk themselves, Brown & Brown acts as an insurance broker.

The company connects businesses and individuals with insurance carriers and earns commissions and service fees in the process.

This model is attractive because it is highly capital-light.

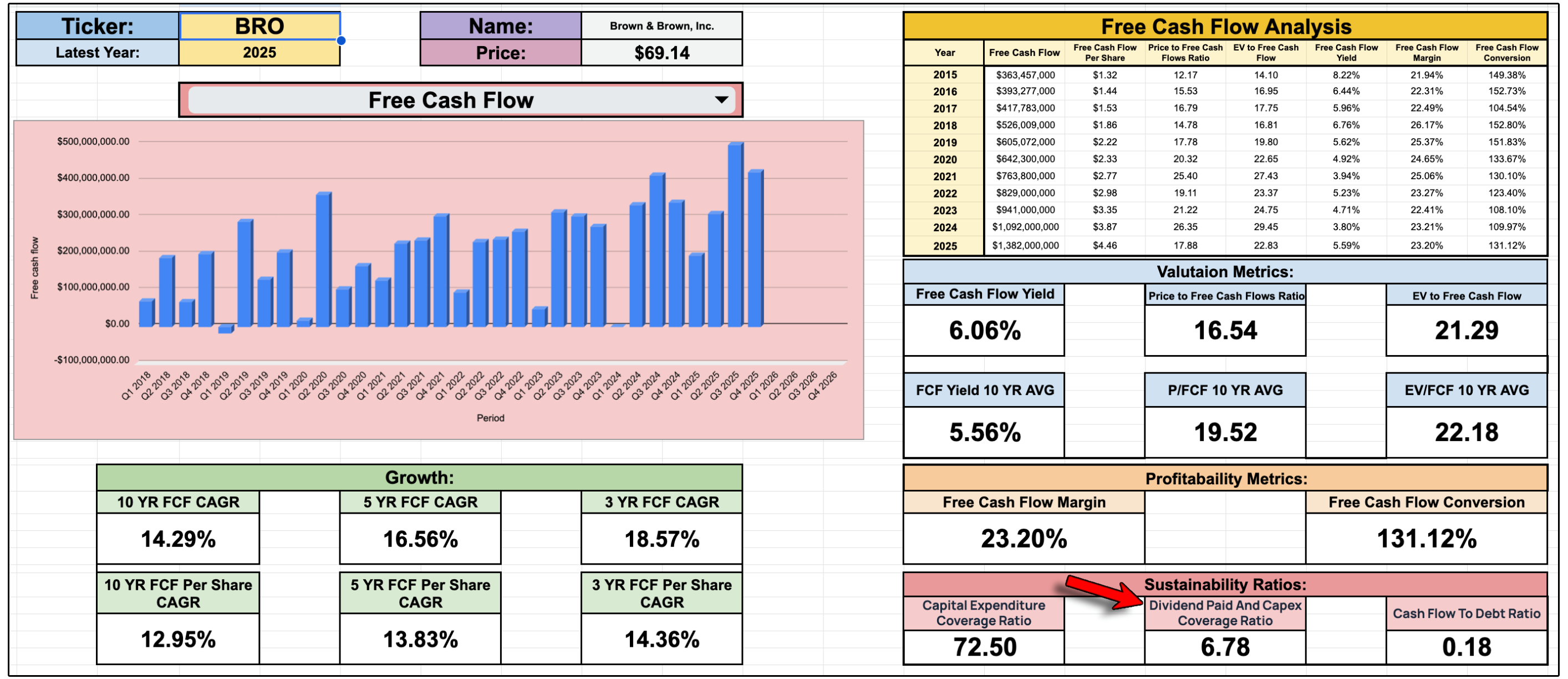

In fact, this model is so capital light that BRO has a dividend and Capex coverage ratio of 6.78!

They can cover the company’s capital expenditures and dividend nearly 7 times over.

Since Brown & Brown does not underwrite policies, it avoids the balance sheet risk that traditional insurers face while still benefiting from long-term growth in insurance premiums.

There are two primary sources of revenue for the company.

Commissions (70% of revenue)

BRO earns a commission (typically 10–15% of the annual premium) every time they place a customer with an insurance carrier.

Fees (30% of revenue)

BRO charges fees directly to customers for specialized services like risk management, employee benefits consulting or claims administration.

This combination creates a highly scalable business model that generates strong margins and consistent cash flow.

Today, more than 90% of Brown & Brown’s revenue is generated in the United States, and the business is organized into four primary operating segments:

Retail (58%) – Directly serving businesses and individuals with insurance solutions

National Programs (24%) – Specialized insurance programs tailored to specific industries

Wholesale Brokerage (13%) – Connecting retail brokers with insurance carriers for hard-to-place risks

Services (5%) – Administrative and consulting services related to insurance

One of the key drivers of Brown & Brown’s long-term growth has been acquisitions.

The company has a long history of acquiring smaller insurance brokers and integrating them into its platform.

Recently, Brown & Brown completed its largest acquisition ever, purchasing Accession Risk Management Group in a $9.8 billion cash-and-stock transaction.

The deal is expected to add approximately $1.7 billion in annual revenue and significantly expand Brown & Brown’s specialty distribution business, which tends to generate higher margins than traditional brokerage operations.

Over time, this acquisition strategy has allowed Brown & Brown to steadily expand its market share while maintaining strong profitability.

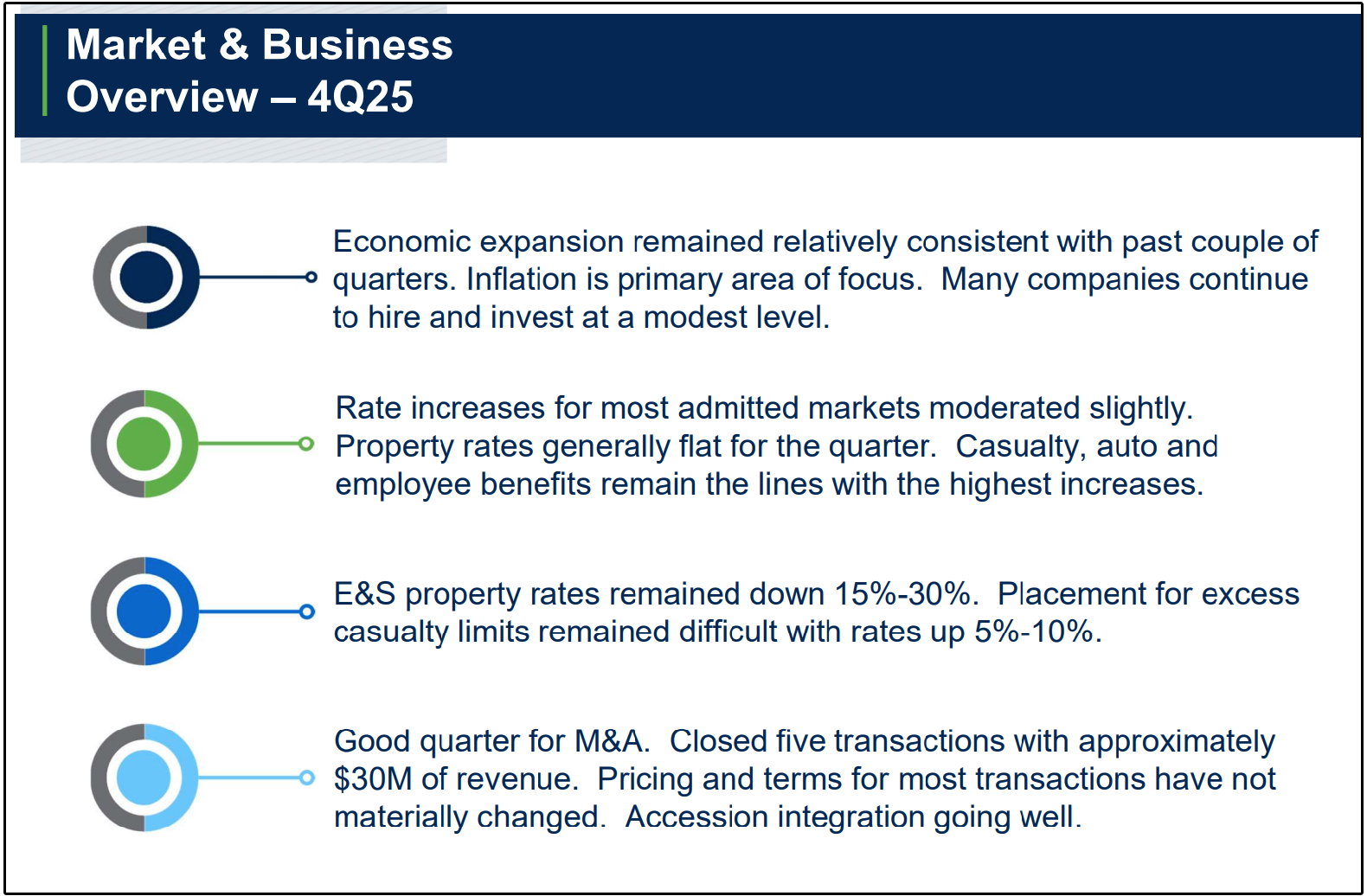

Looking ahead, management expects insurance pricing trends in 2026 to be somewhat mixed. According to CEO J. Powell Brown, casualty insurance rates (the largest segment of the market) are expected to continue rising, while property insurance rates may soften slightly due to the lack of major hurricane losses in 2025 and an increase in available capital.

For Brown & Brown, this matters because brokerage revenue is often tied directly to insurance premium levels.

When premiums rise, brokers typically earn higher commissions.

Conversely, softer pricing environments can create modest pressure on organic growth.

However, the company continues to see steady demand from its customer base, with most clients still investing in their businesses and hiring at a modest pace.

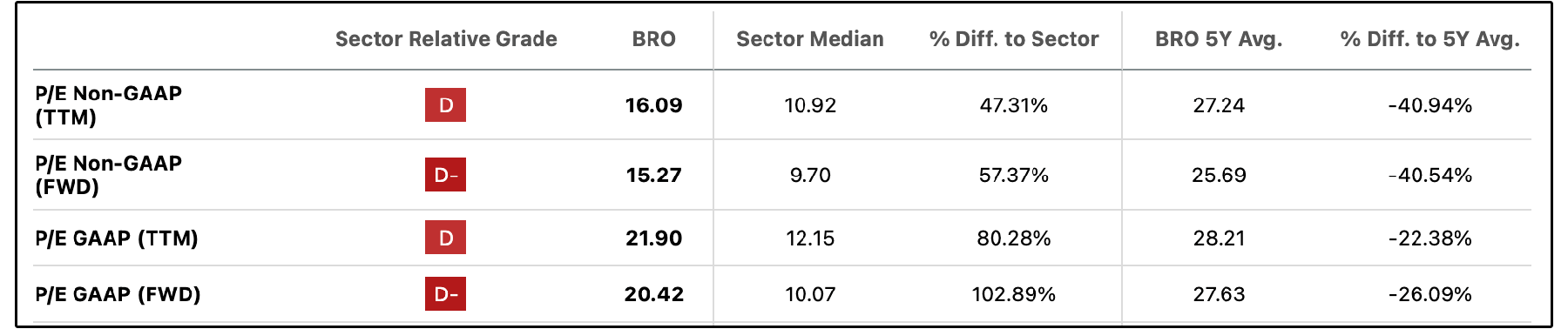

BRO currently trades at a significant discount to its historical valuation multiples.

Now, let’s dive into the full list of dividend stocks with the most upside according to Wall Street.

As a reminder, this list is updated monthly, and is always available on Dividendology.com by visiting our database.