🧾 List of Most Upside Dividend Stocks

Wall Street Price Targets Revealed 🎯

Every month, I compile data on the dividend stocks with the most upside based on Wall Street analysts price targets.

Members will get access to the full list every month, as well as all other Dividendology features.

This month, only 32 stocks made the list.

Let’s dive in.

1. 🧳 Booking Holdings (BKNG)

Wall St. Price Target: $6,172 | Upside: 19.83%

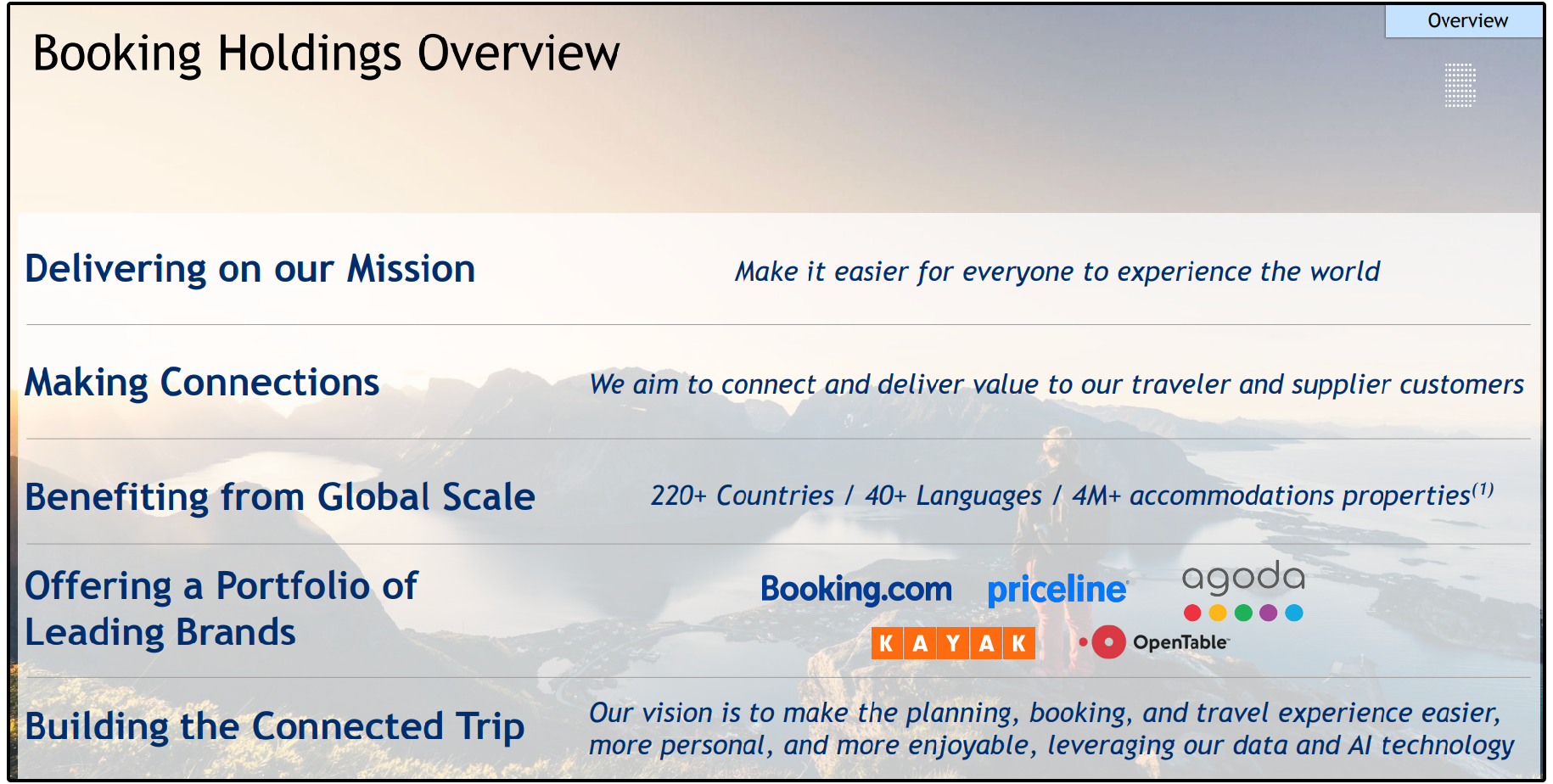

Booking Holdings is the largest online travel agency in the world, operating 5 major platforms most people already use:

Booking.com

Priceline

Agoda

Kayak

OpenTable

Across these brands, Booking offers access to 4+ million accommodation properties, 31 million total listings, and serves travelers in 220+ countries across 40+ languages.

The global online travel market is projected to grow from $613B in 2024 to over $1T by 2030, compounding at around 8.6% annually.

Booking Holdings is positioned to benefit from this secular tailwind perhaps more than anyone else.

This growth is being driven by:

Increased smartphone usage

A continued shift from offline to online bookings

Growing preference for self-service travel planning

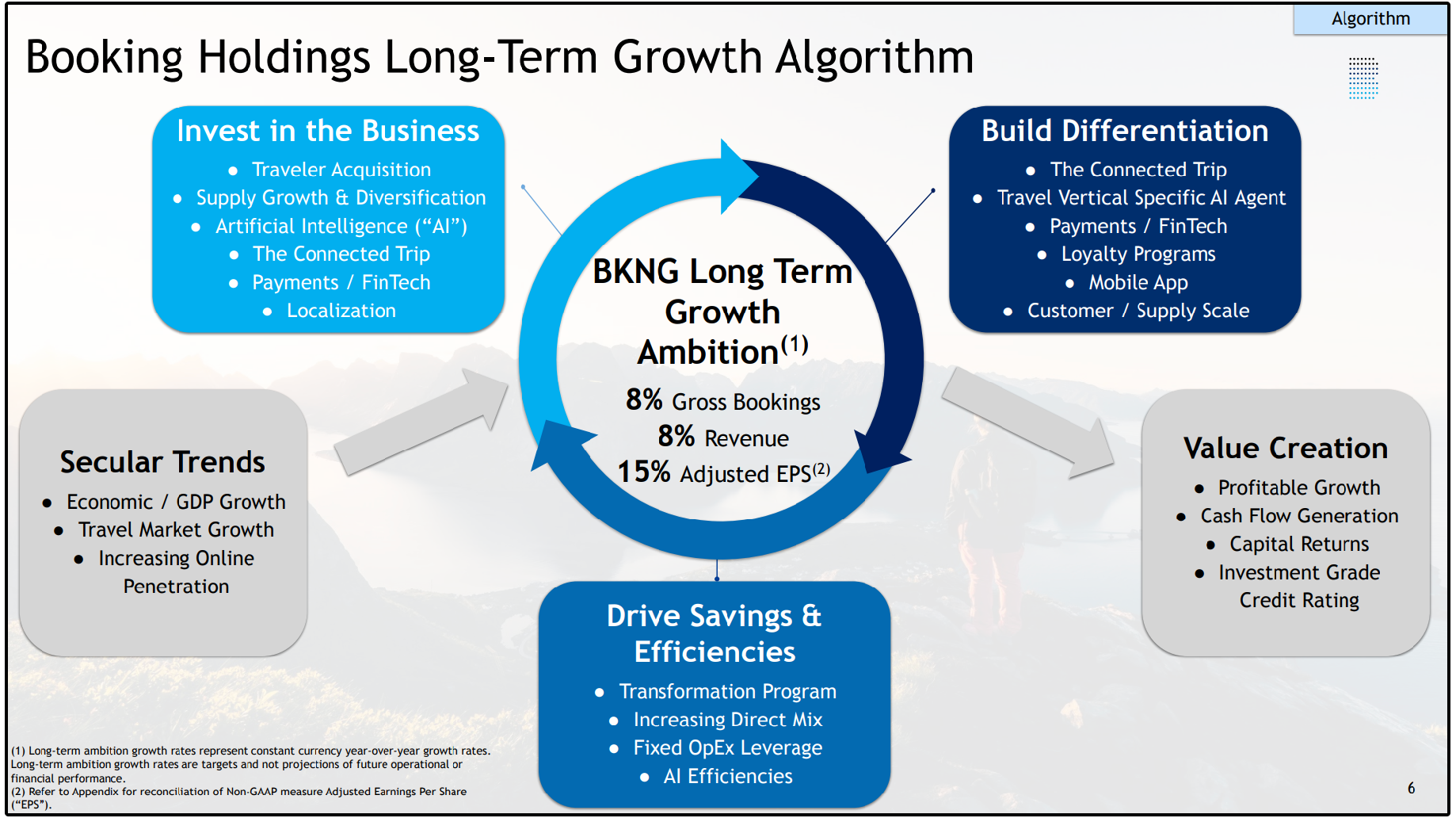

Booking’s long-term strategy is built around what management calls the Connected Trip.

Instead of just booking a hotel, users increasingly book things like accommodations, flights, rental cars, and dining together.

Connected Trip transactions are now growing at a mid-20% rate, and while still a low double-digit percentage of total transactions, this vertical can dramatically increase the lifetime value of customers.

The more of a trip that flows through Booking, the harder it becomes for users to leave the ecosystem.

This strategy is best illustrated by Booking’s long-term growth algorithm.

At the center of the framework is management’s ambition to grow revenue by 8% and adjusted EPS by 15% over the long term.

Every major initiative at the company feeds into this flywheel.

At the same time, growth is paired with efficiency.

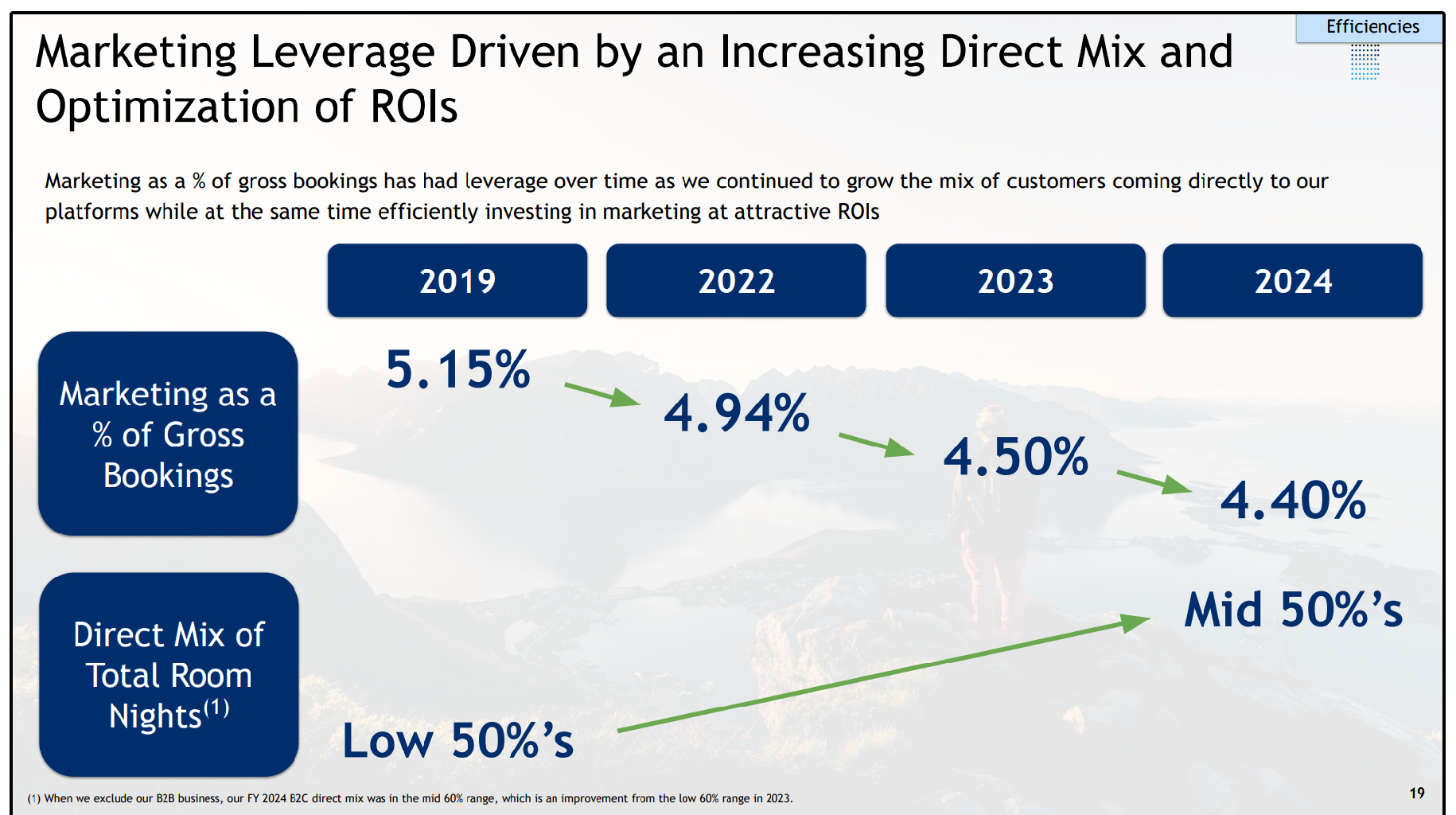

For example, Booking Holdings has recently increased the direct mix of total room nights while also seeing a decrease in marketing as a % of gross bookings:

The result is strong free cash flow generation, consistent capital returns via buybacks and dividends, and earnings that compound faster than revenue over time.

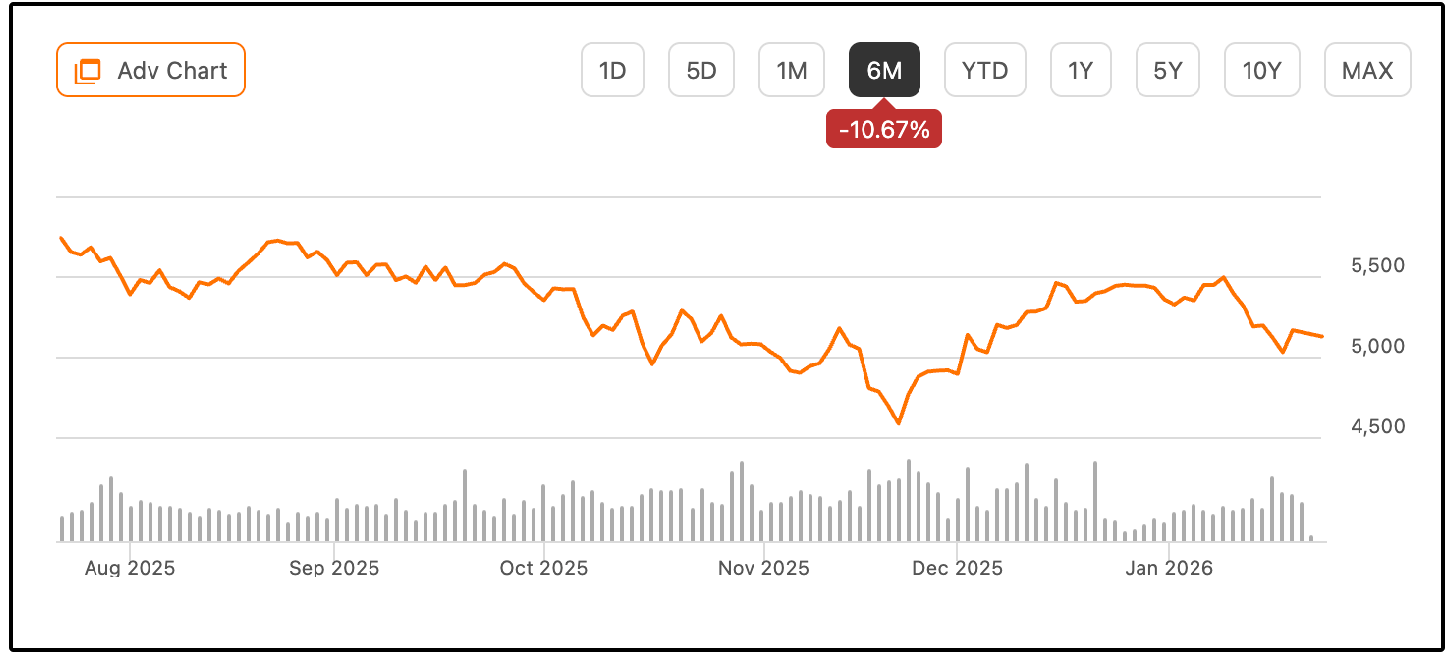

Despite this dominant position, the stock has meaningfully underperformed the market over the last 6 months, selling off by over 10%.

However, this seems to be presenting opportunity.

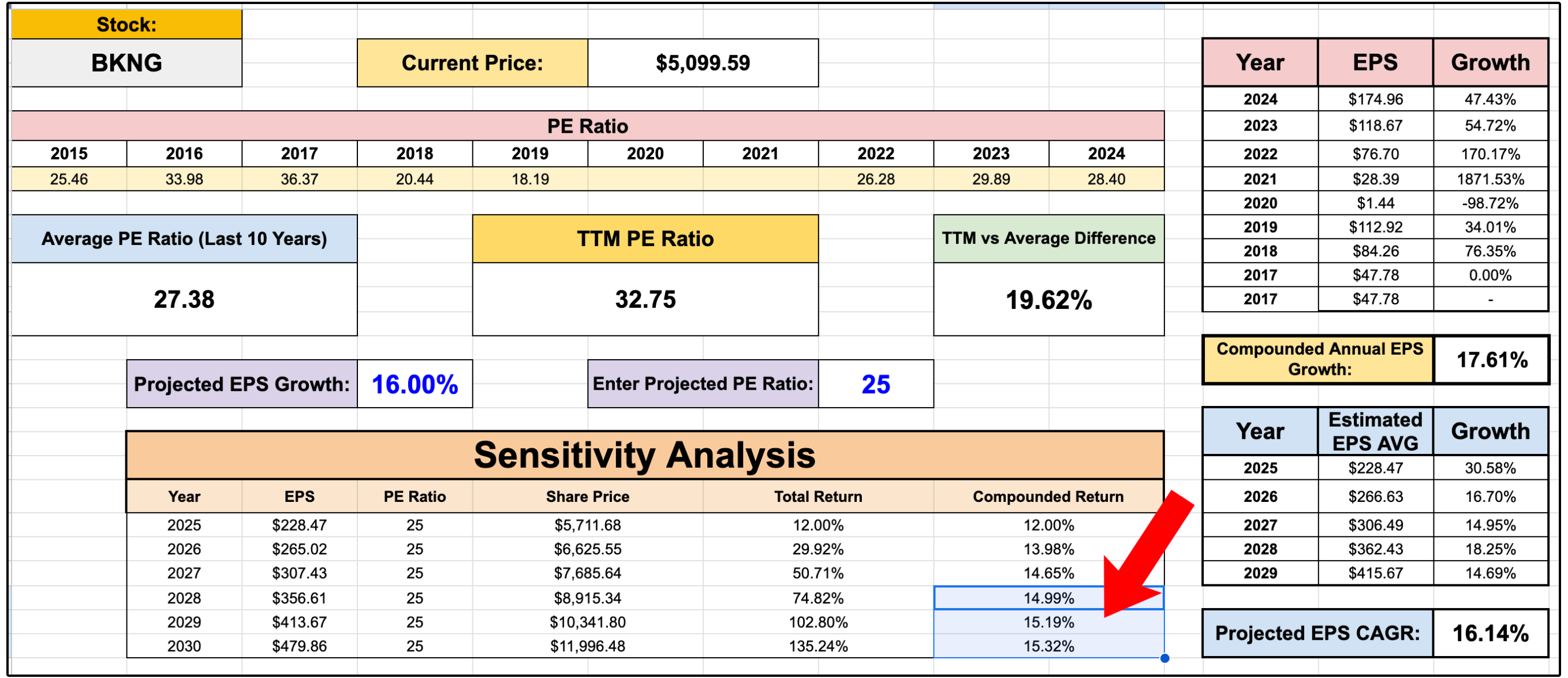

Assuming:

16% EPS CAGR (analysts estimates)

P/E multiple falls back to 25

You would be looking at a 15.3% CAGR through the year 2030.

The yield is low at 0.75%, but there is clearly massive dividend growth potential.

2. 🛡️ Allstate (ALL)

Wall St. Price Target: $238 | Upside: 23.48%

At its core, insurance is simple.

Customers pay premiums today to protect against potential future losses.

Insurers are then able to hold and invest this money (known as float) until claims are paid.

Eventually, insurers pay out claims to policyholders who experience losses.

The profit comes from two primary sources:

Underwriting profit

When premiums collected exceed claims and operating expenses.

Investment profit

From investing the float until claims come due.

When executed well, this business model can be incredibly powerful.

So naturally, one of the key drivers of profitability is how accurate their underwriting is-

And this is one of the areas where Allstate currently sees a massive opportunity.

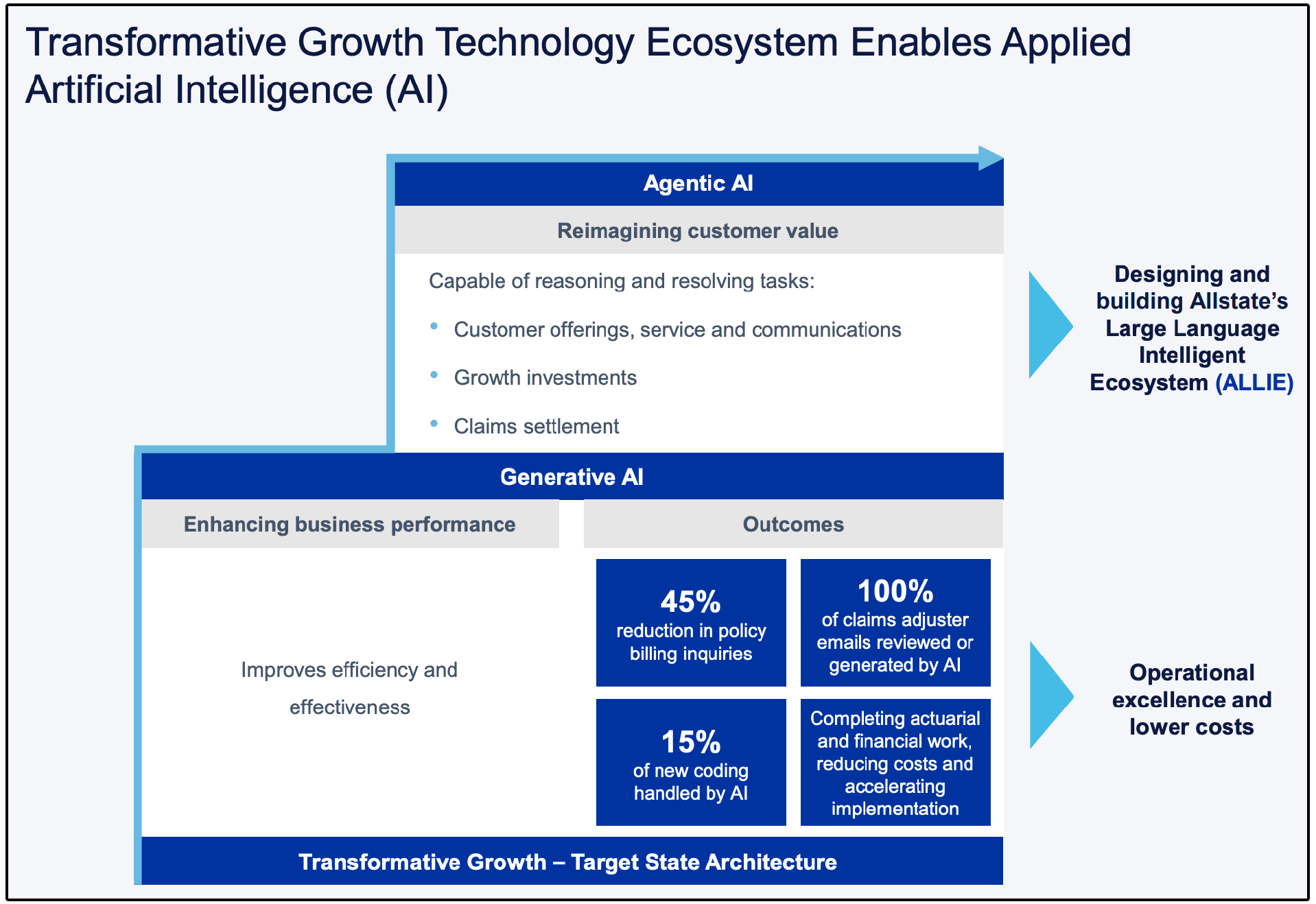

Allstate is aggressively applying artificial intelligence across its business to drive operational efficiency.

As shown in the image above, the company is building a layered AI ecosystem that spans both generative AI and agentic AI, all powered by its internal platform, ALLIE (Allstate’s Large Language Intelligent Ecosystem).

On the generative AI side, Allstate is already seeing tangible results: fewer policy billing inquiries, faster claims processing, and meaningful reductions in manual work across actuarial, financial, and operational functions.

These tools improve efficiency and lower costs, which of course directly supports margin expansion over time.

Agentic AI takes this a step further by enabling systems that can reason, resolve tasks, and interact with customers autonomously, and improving customer service.

This improves customer retention.

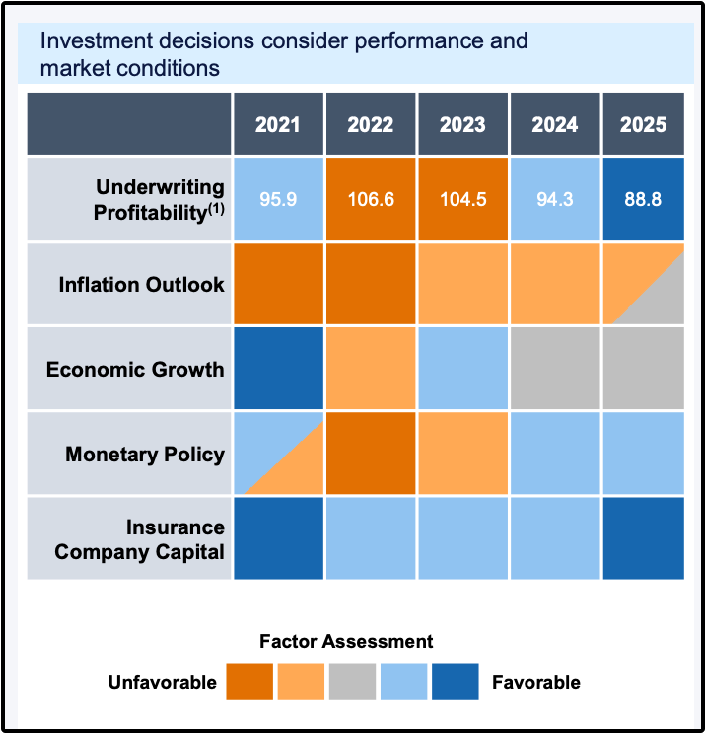

Perhaps even more importantly, Allstate’s underwriting profitability has moved from unfavorable to highly favorable over the past few years.

The chart below reveals this.

The numbers in the underwriting profitability row represent Allstate’s underwriting profitability, measured by the combined ratio, which tracks claims paid plus operating expenses as a percentage of premiums collected.

A combined ratio below 100% indicates underwriting profit, while a ratio above 100% signals underwriting losses.

After struggling in 2022–2023 with combined ratios of 106.6 and 104.5, Allstate’s underwriting has improved significantly, falling to 94.3 in 2024 and 88.8 in 2025.

The bull case is that AI will be able to continue to improve the combined ratio through more accurate risk pricing and faster and more efficient claims processing.

Despite the sharp improvement in underwriting profitability and rising EPS expectations, Allstate’s valuation has moved in the opposite direction.

The stock currently trades well below both the broader market and its historical average.

Allstate boasts a dividend yield of slightly over 2% with dividend growth in the 15% range over the past 5 years.

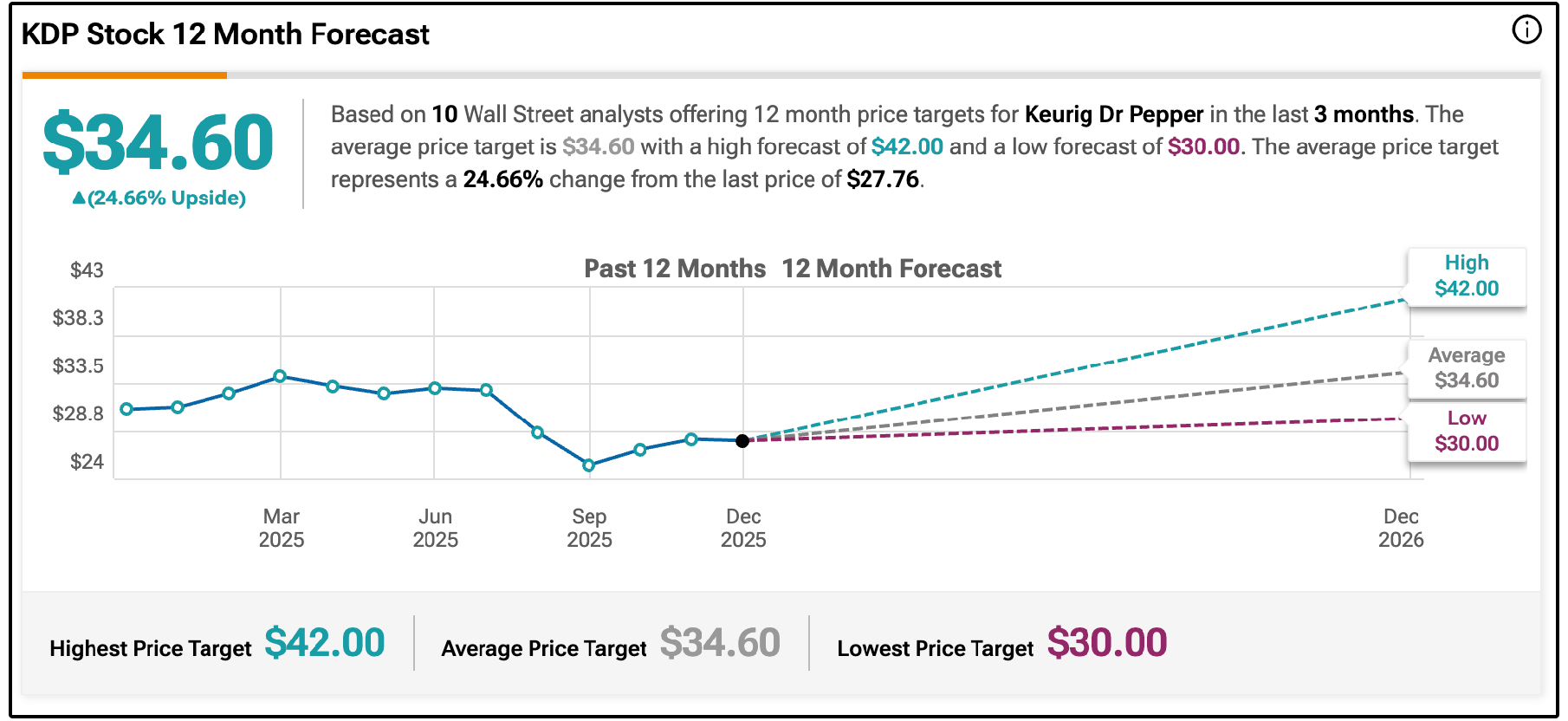

3. 🥤 Keurig Dr Pepper Inc. (KDP)

Wall St. Price Target: $35 | Upside: 24.66%

Keurig Dr Pepper is one of the largest beverage companies in North America, owning a portfolio of iconic brands including Dr Pepper, Canada Dry, Snapple, 7UP, and Keurig.

Despite the defensive nature of the business, KDP stock sold off sharply in late 2025, falling nearly 30% after management announced a major strategic shift involving:

The acquisition of European coffee giant JDE Peet’s

A subsequent breakup of the company into two standalone businesses

KDP announced it would acquire JDE Peet’s in an all-cash transaction valuing the company at roughly $18 billion, which is a meaningful premium to the pre-announcement price.

The main concern is that the deal requires taking on additional debt, which raises concerns surrounding leverage and execution risk.

Following the acquisition, KDP plans to separate into:

Beverage Co. – the high-growth U.S. beverage business

Global Coffee Co. – combining Keurig and JDE Peet’s into a global coffee pure play

KDP’s U.S. beverage business is the clear primary growth engine, growing mid-to-high single digits and recently posting double-digit growth driven by both volume and pricing.

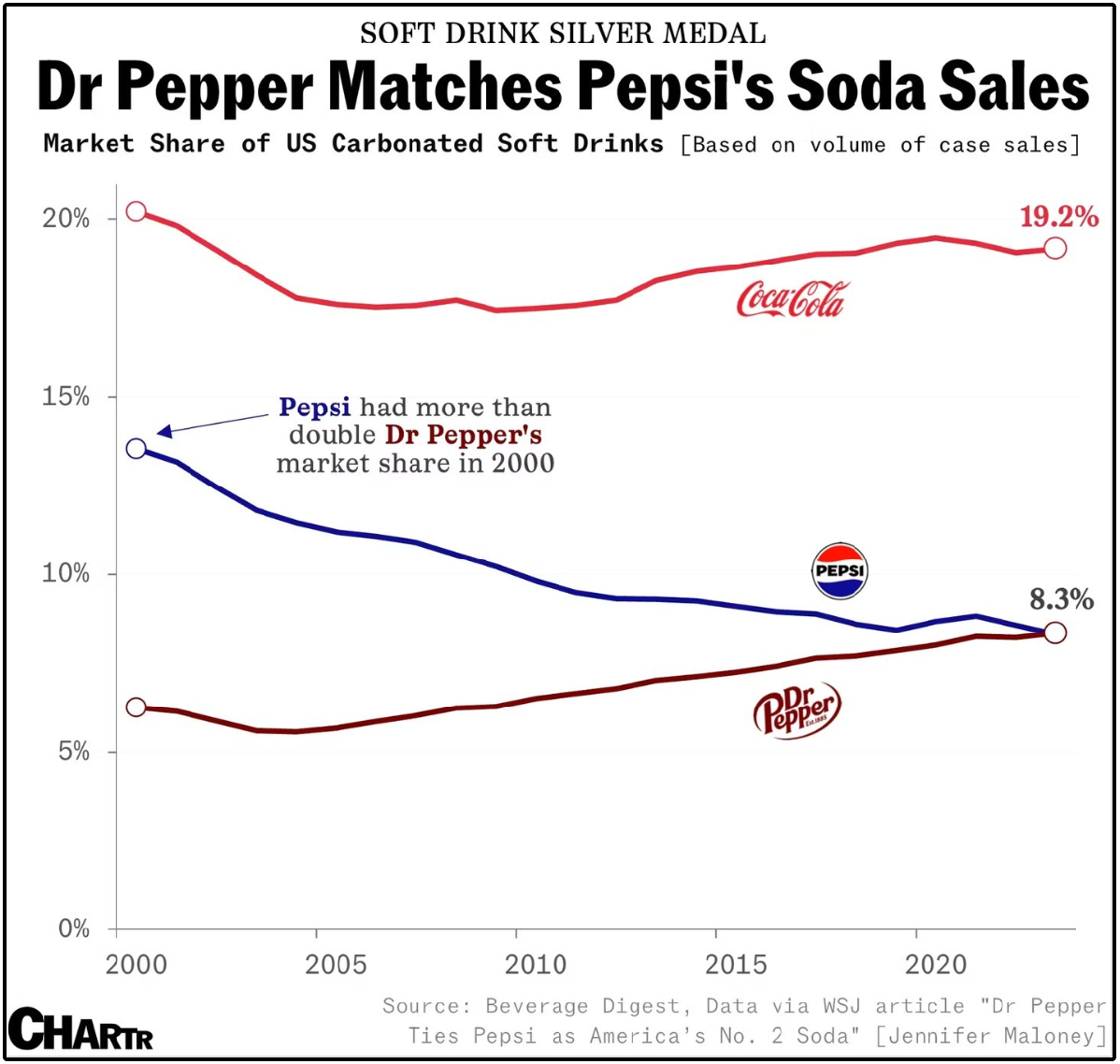

Dr Pepper continues to gain market share and is now the most popular soda brand among U.S. teens, even ahead of Coca-Cola.

However, KDP’s U.S. coffee segment has been underperforming, pressured by volume declines and commodity volatility.

JDE Peet’s brings:

Faster coffee growth

Strong #1 or #2 market positions across Europe

Well-known brands like Peet’s, Jacobs, and L’OR

Post-separation, each business becomes more focused, easier to value, and better aligned with its growth profile.

Wall Street seems to believe this deal will unlock significant value for KDP, with the average analyst price target implying 24.66% upside.

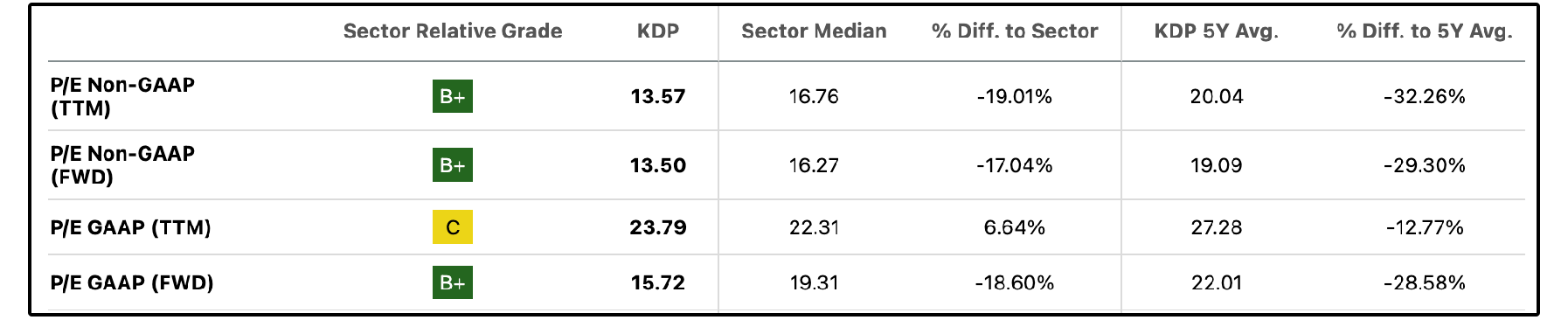

They currently trade at a forward P/E multiple of just 13.5-

Which is well below their sector average and their historic average.

KDP currently yields 3.32% with dividend growth of around 9% over the last 5 years.

Now, let’s dive into the full list of dividend stocks with the most upside according to Wall Street.

As a reminder, this list is updated monthly, and is always available on Dividendology.com by visiting our database.