🧾 List of Most Upside Dividend Stocks

These Stocks are Undervalued! 🔥

Every month, I compile data on the dividend stocks with the most upside based on Wall Street analysts price targets.

Members will get access to the full list every month, as well as all other Dividendology features.

This month, only 53 stocks made the list.

Let’s dive in.

1. 💻 Microsoft (MSFT)

Wall St. Price Target: $560.42 | Upside: 45.53%

Microsoft has been the worst performing MAG7 stock in 2026.

When looking at a heat map of the S&P 500, they stand out significantly, now down nearly 20% year to date.

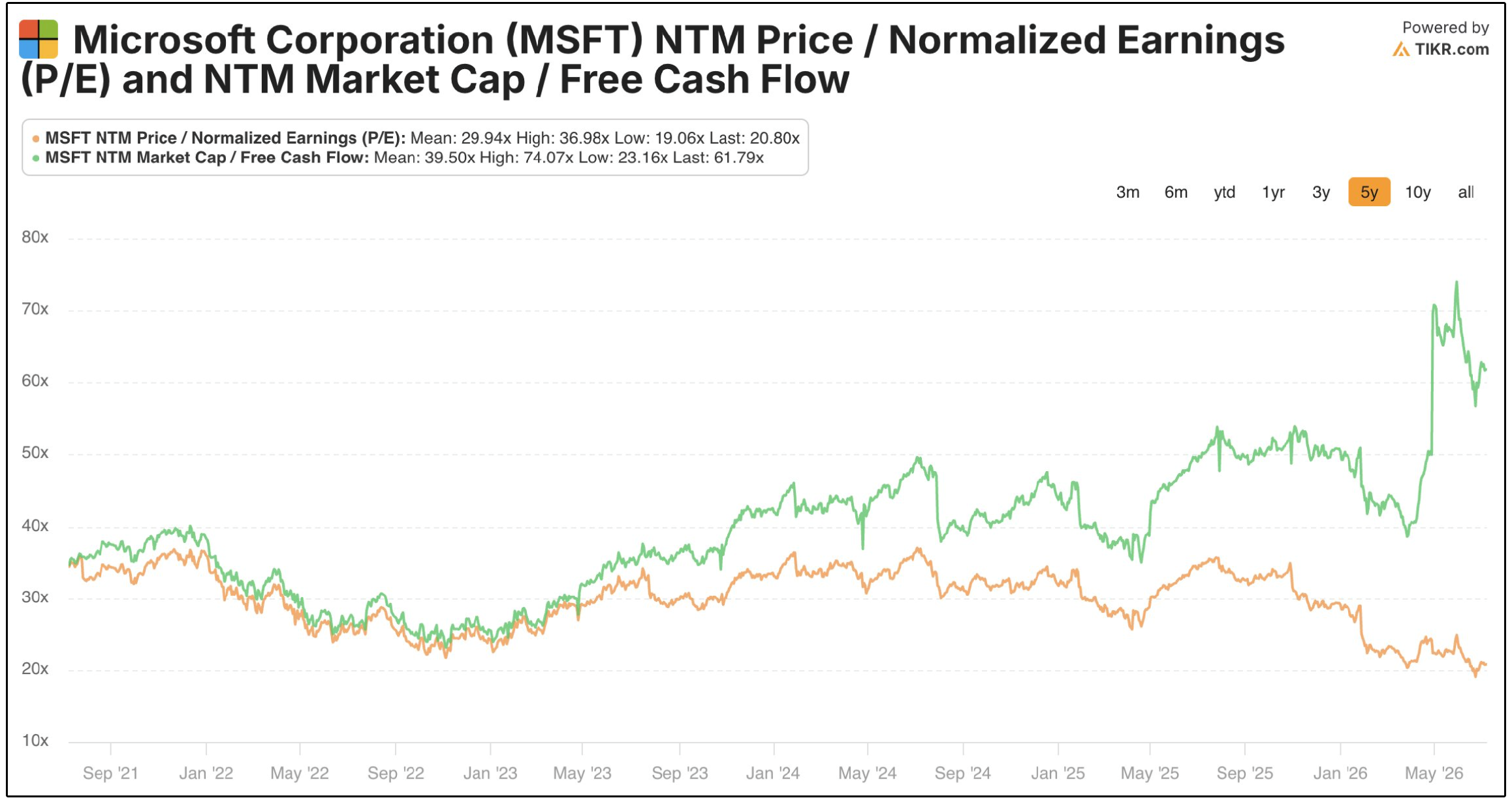

The result of this is that Microsoft is now trading at its lowest P/E multiple in the last 5 years-

But at the same time, its near its highest FCF multiple in the last 5 years.

Of course, the cause behind the climbing free cash flow multiple is not any issues with the cash flows the core business is generating.

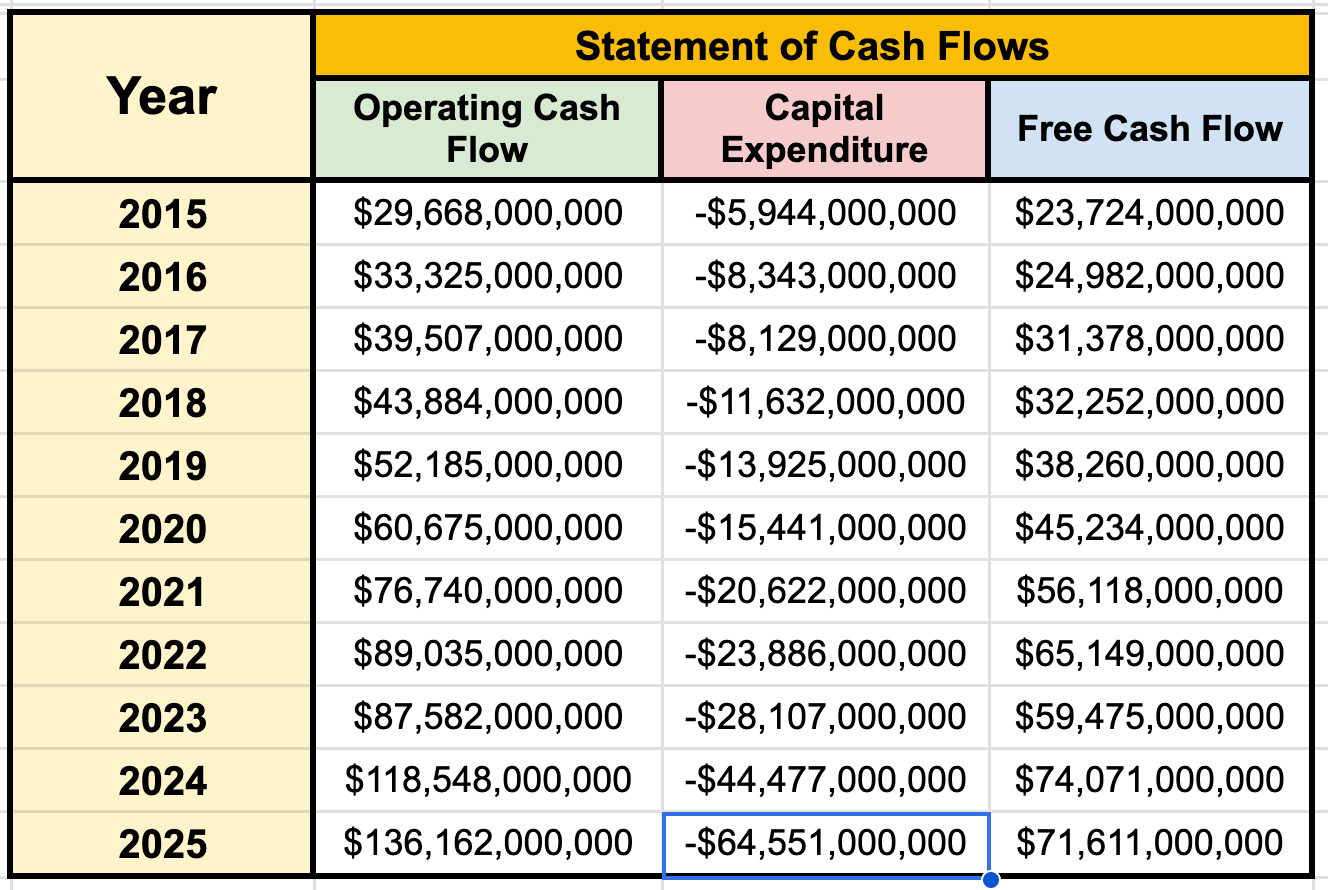

In fact, operating cash flows grew from $118 billion in 2024 to over $136 billion in 2025.

However, capex spending increased by over $20 billion, leading to a rare decline in free cash flow.

This of course is because the company is spending aggressively to construct data centers, purchase advanced chips and expand the infrastructure supporting Azure and artificial intelligence.

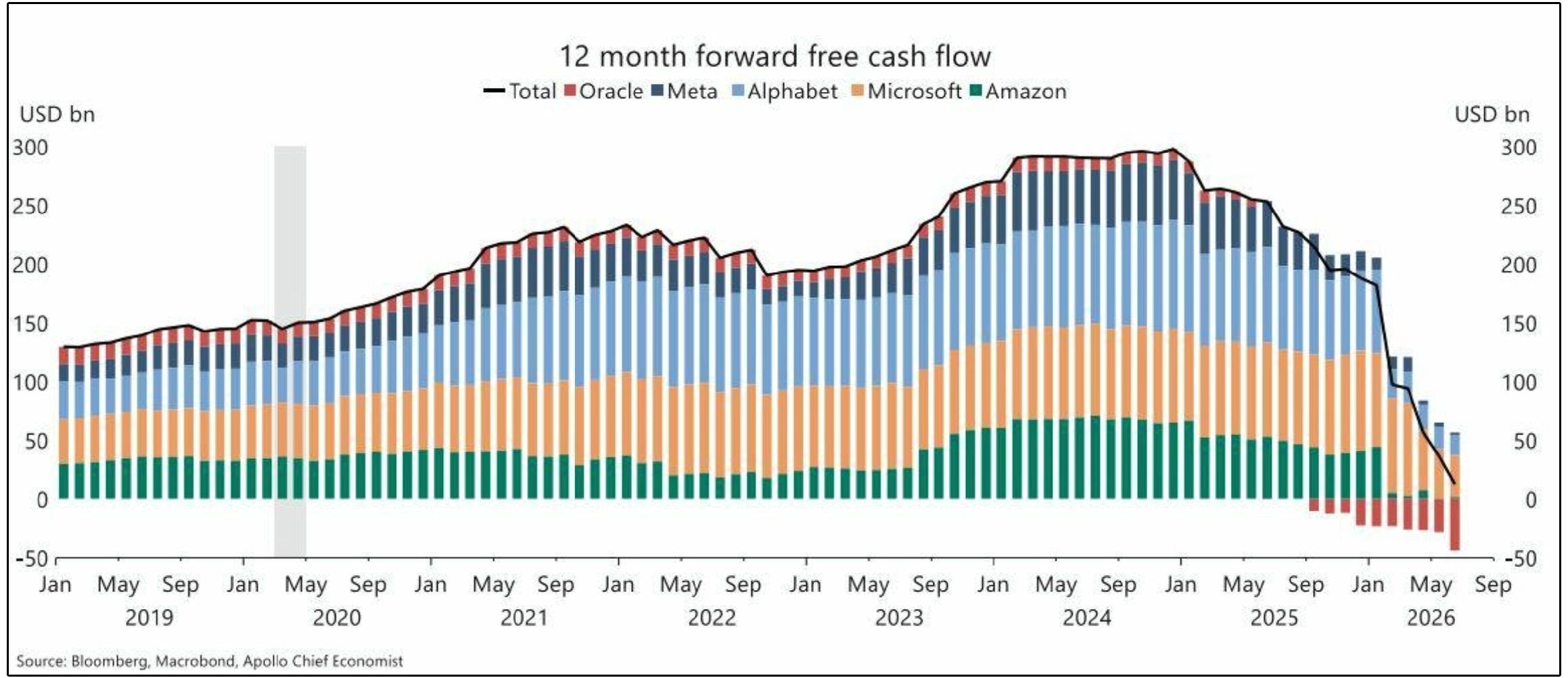

They are competing in the exact same AI race as other hyperscaler stocks, such as:

Meta

Amazon

Oracle

Google

All of these companies have dramatically increased capex spending to the degree where free cash flow between the five of them is projected to be nearly zero over the next 12 months.

However, one of the companies is continuing to generate meaningful positive free cash flow, and that’s Microsoft.

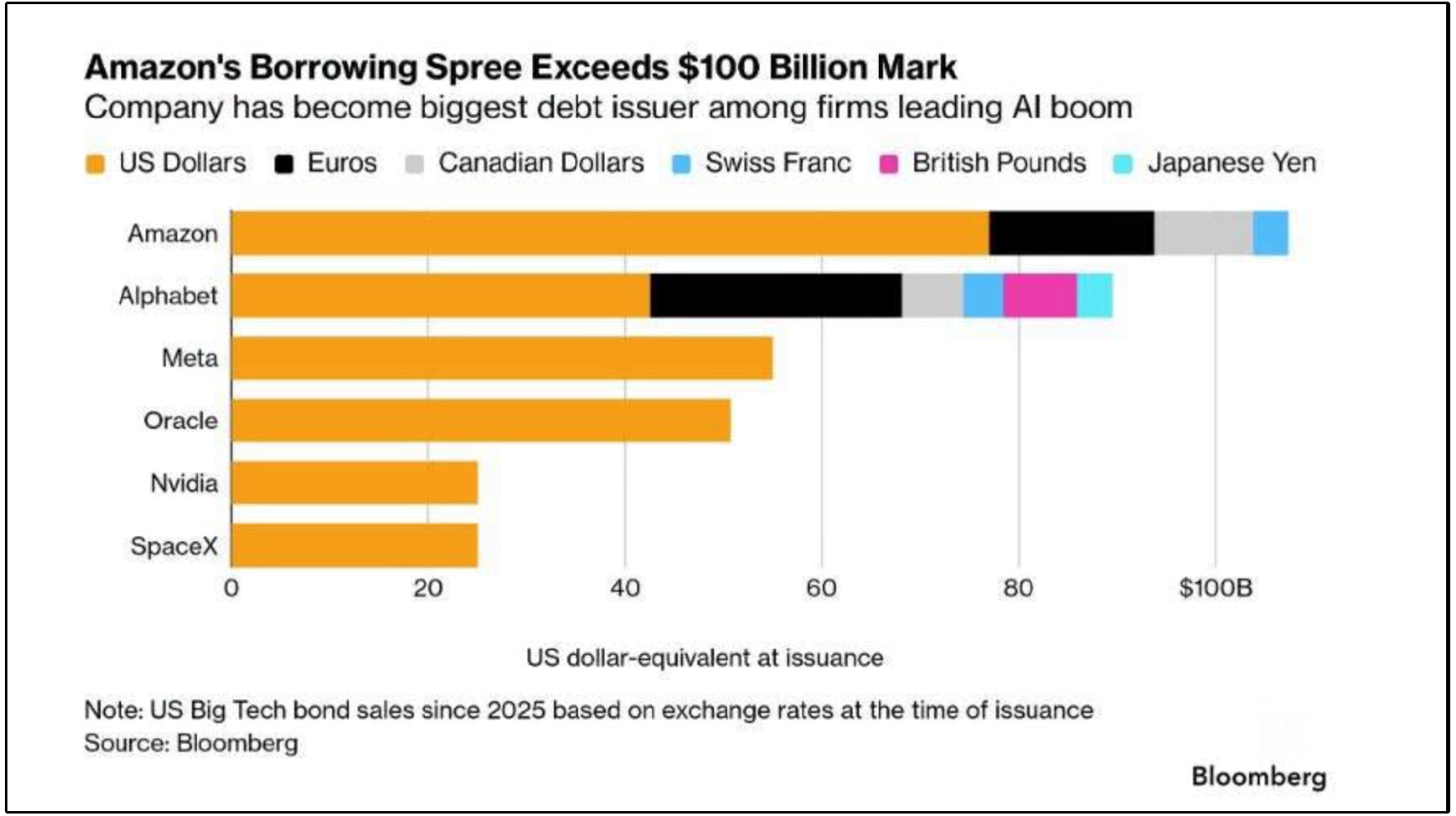

In fact, since essentially all of these companies are spending all of their operating cash flows on capex spending, they are simultaneously having to issue debt to raise capital.

Again however, you won’t see MSFT on this list.

Hyperscalers have issued $350B+ in debt since 2025 to fund AI capex, while Microsoft has issued none.

Microsoft’s biggest advantage is that it can fund this investment cycle more comfortably than most of its competitors.

Other hyperscalers have increasingly relied on bond issuance as their AI spending absorbs or exceeds internally generated cash flow.

Microsoft, by comparison, is expected to remain solidly free-cash-flow positive throughout the investment cycle.

Microsoft can continue investing without taking on the same level of interest expense, refinancing exposure or balance-sheet risk.

Its enormous base of recurring revenue from Microsoft 365, Azure, enterprise software and cybersecurity provides the financial foundation needed to fund AI infrastructure internally.

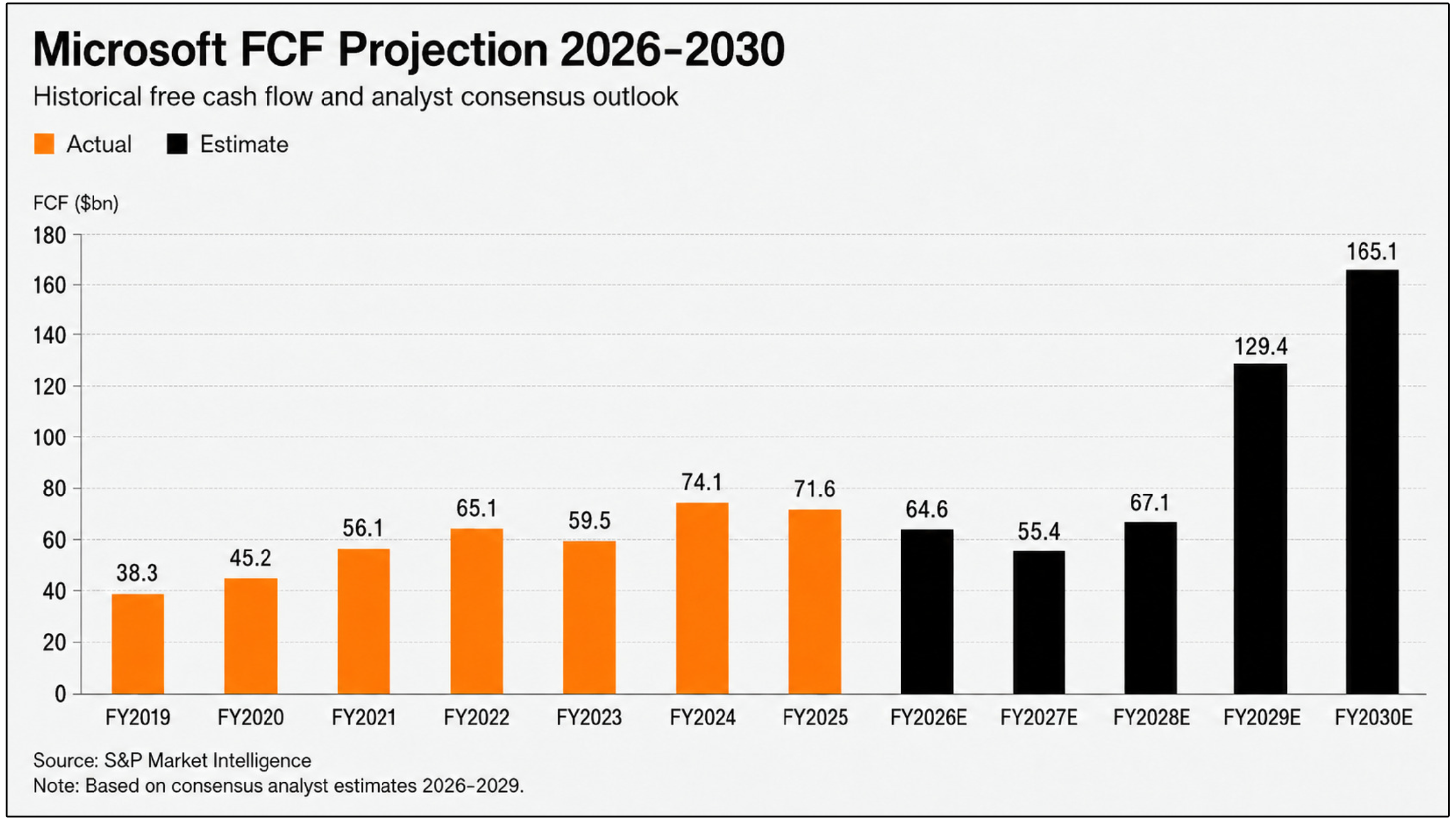

Consensus projections from S&P Market Intelligence suggest Microsoft’s free cash flow will remain above $50 billion during the investment trough before beginning to spike in 2028.

By 2029, free cash flow could potentially surpass $129 billion as spending growth slows and revenue from the new capacity accelerates.

This creates a potential free-cash-flow inflection point similar to what other capital-intensive technology companies (like TXN) have experienced after completing major investment cycles.

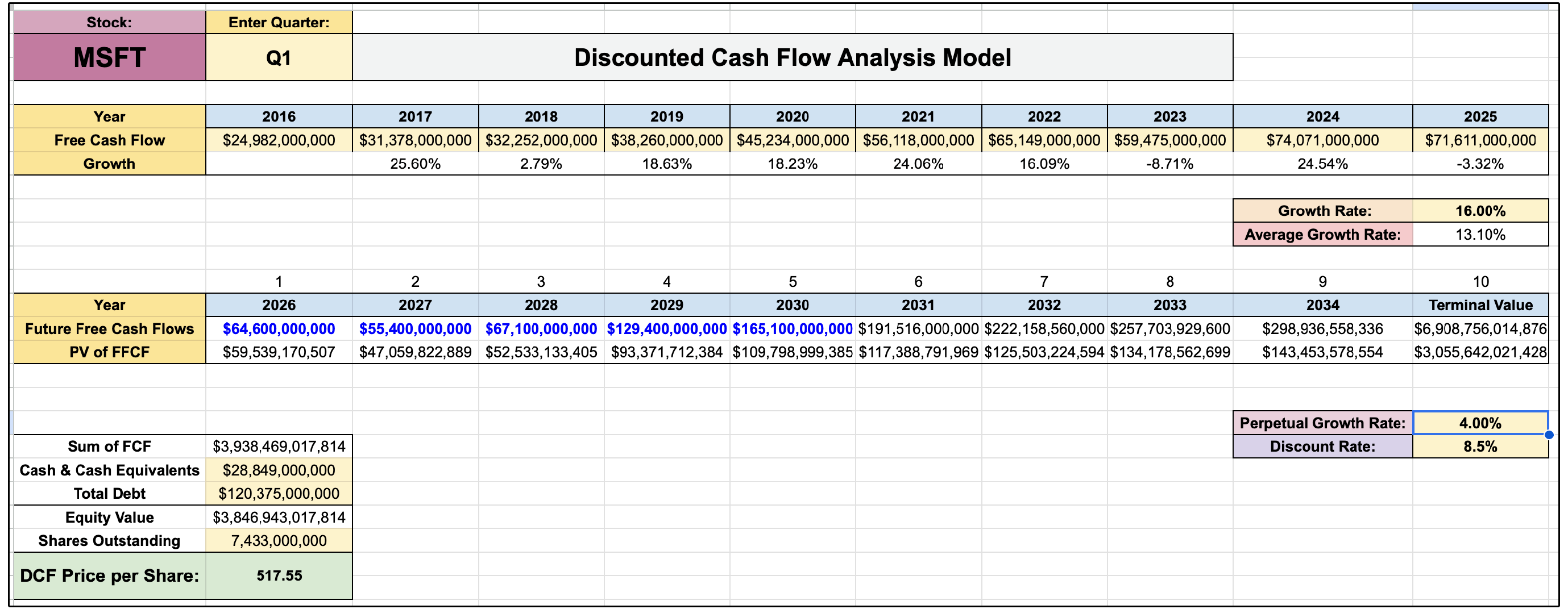

But with the free cash flow projections from S&P Market Intelligence, we can create a very detailed discounted cash flow model.

According to our model, we can see Microsoft would have over 33% upside from current prices.

2. 🏢 Digital Realty Trust (DLR)

Wall St. Price Target: $219.85 | Upside: 25.71%

Digital Realty is a REIT yielding around 2.74%.

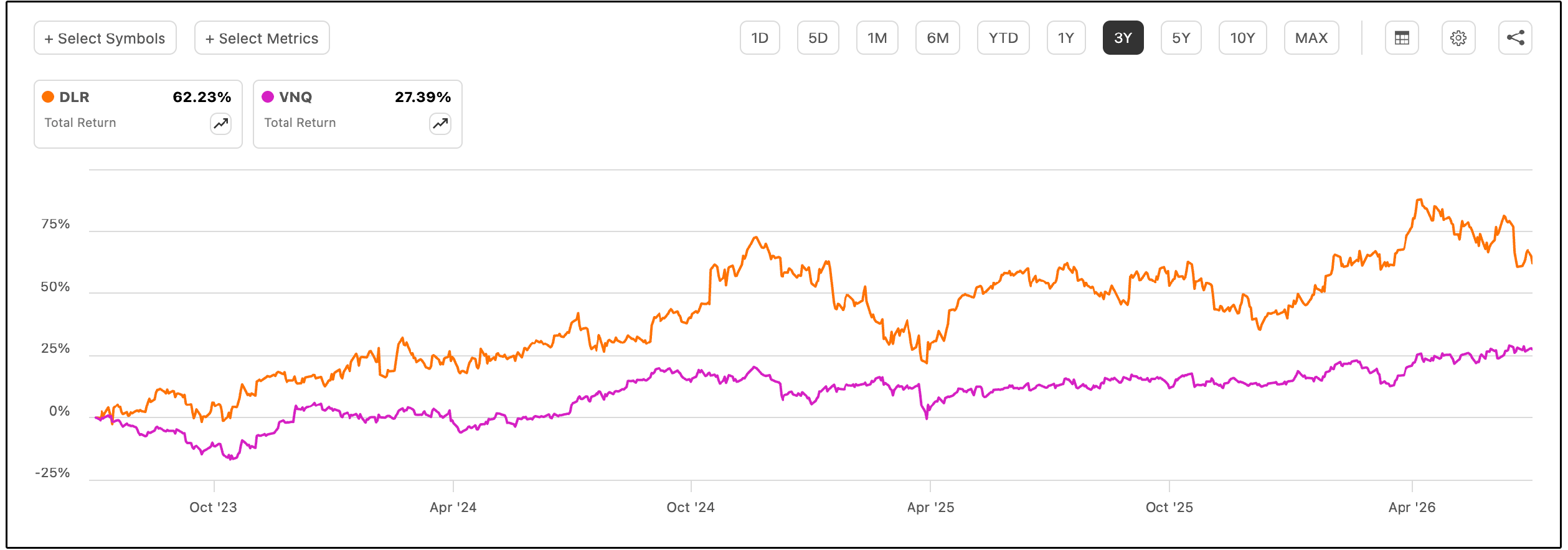

While most of the REIT market has been left behind over the last three years, DLR has vastly outperform the Vanguard real estate index.

DLR is a unique REIT, in that it is positioned directly at the intersection of real estate, cloud computing, and artificial intelligence.

The company owns and operates data centers that provide the power, connectivity, and physical infrastructure required by hyperscalers and other large technology customers.

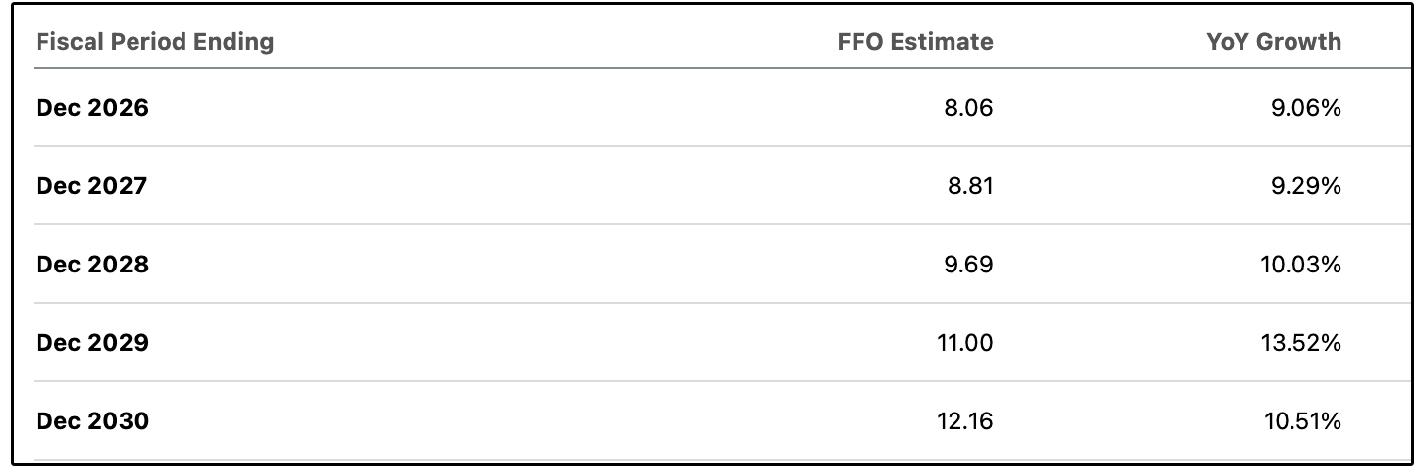

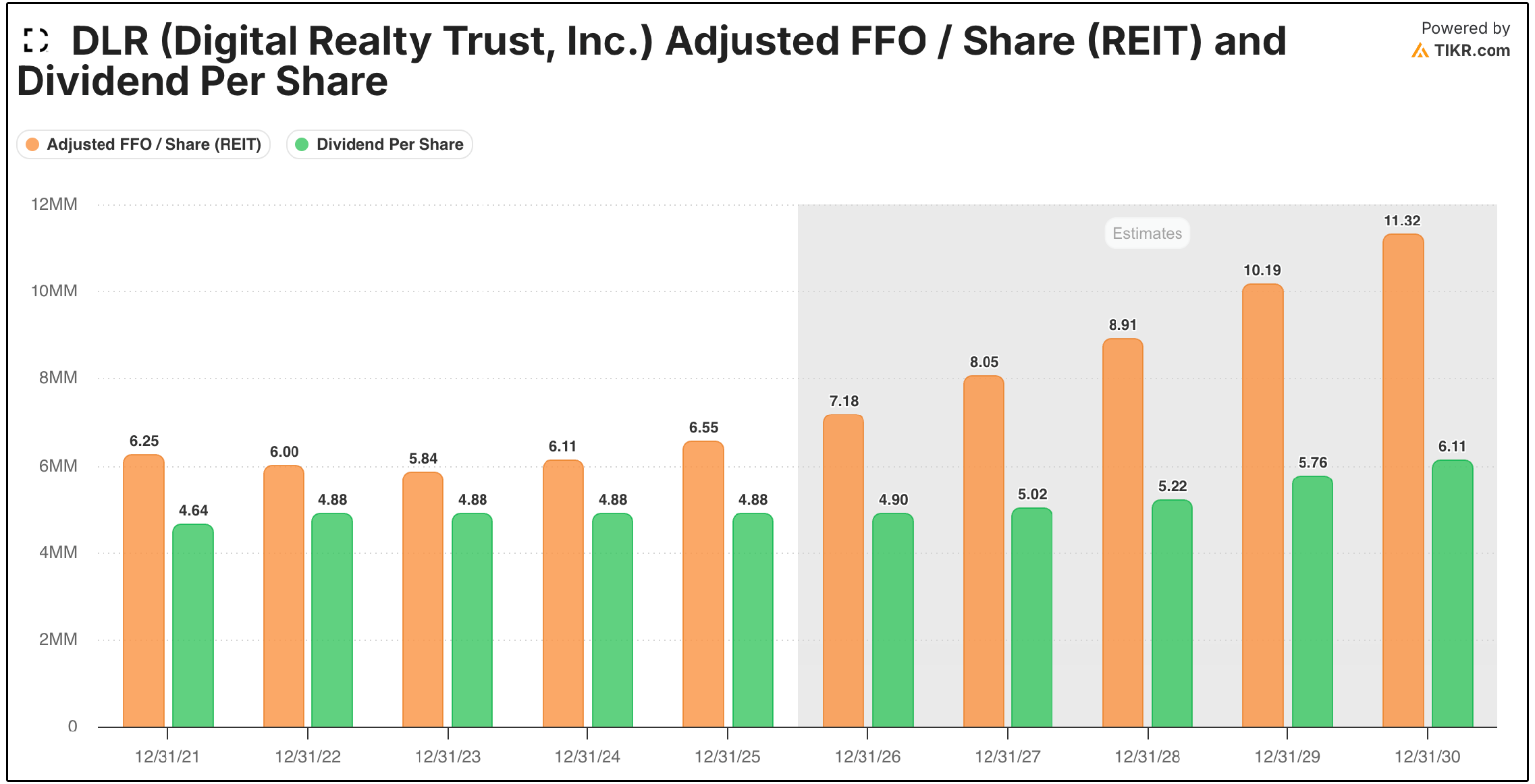

As a result, their projected FFO growth is quite strong, especially relative to the REIT market as a whole.

The recent decline following Digital Realty’s transaction with Blackstone appears to have created an attractive entry point.

Digital Realty agreed to acquire Blackstone’s remaining 64% interest in three data center developments in Northern Virginia.

The properties represent 96 megawatts of capacity and are already fully leased to hyperscale customers under 15-year contracts containing annual rent escalators of approximately 3.6%.

Although Digital Realty is paying a substantial price, the properties are expected to generate an initial stabilized return of above 6.5%.

But here’s what is interesting.

The market currently values Digital Realty’s existing portfolio at an implied return of roughly 5%.

In effect, the company is acquiring new cash flows more cheaply than investors are valuing its own cash flows.

The transaction also allows Digital Realty to bypass one of the industry’s biggest constraints: access to power.

Vacancy in Northern Virginia, the world’s largest data center market, is exceptionally limited.

Acquiring facilities that are already powered, leased and under construction will be considerably more valuable than starting new projects that could face years of permitting, utility and construction delays.

This is in part why AFFO per share is projected to start growing at a faster rate.

On top of this, the dividend is very well covered, and should see strong dividend growth moving forward as AFFO continues to grow at a near double-digit rate.

The primary risk is that Digital Realty must continue issuing shares, forming joint ventures or borrowing money to fund its enormous development pipeline.

However, dilution has been productive so far as core FFO per share has grown faster than the share count.

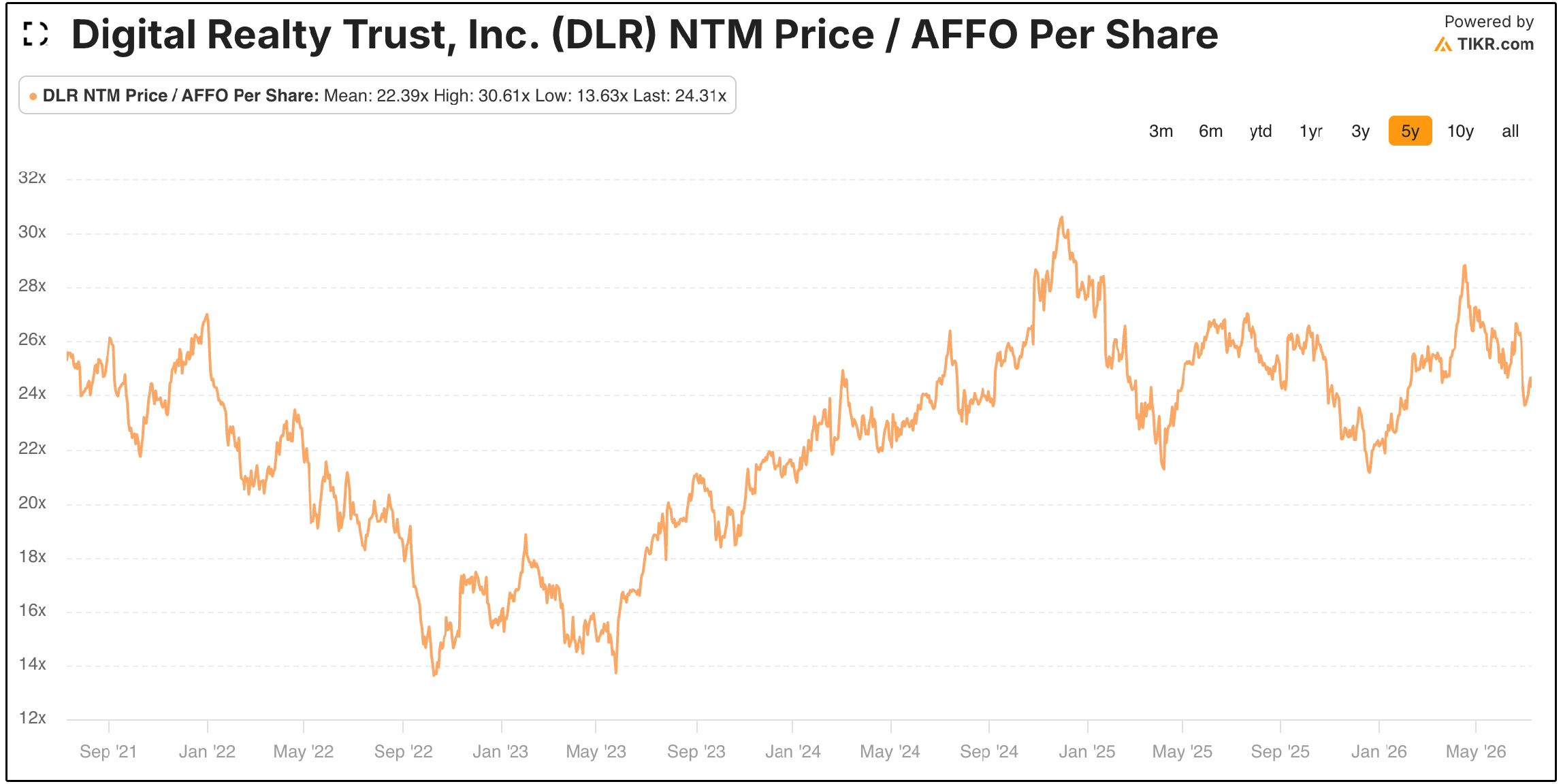

With record leasing, scarce available capacity and a large contracted backlog, Digital Realty trades at a premium relative to the rest of the REIT market.

They offer a combination of growing dividend income and AI-related growth that very few REITs can match.

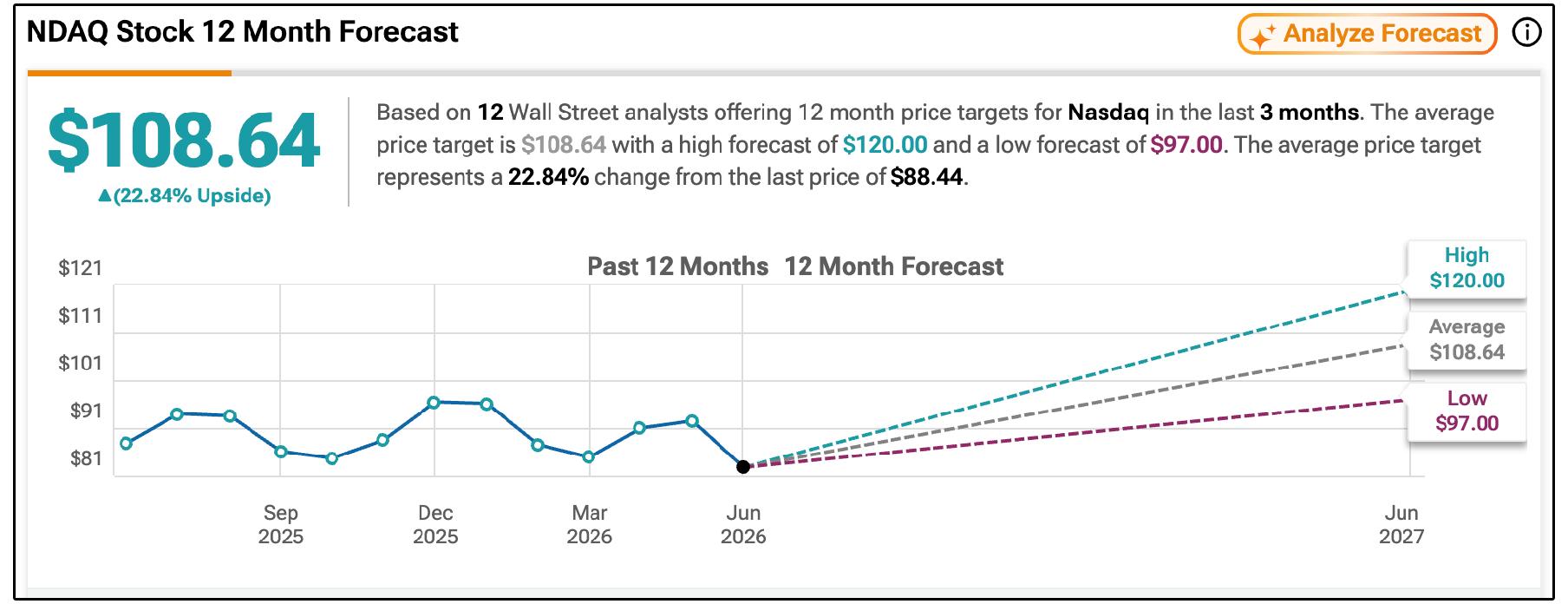

3. 📈 Nasdaq (NDAQ)

Wall St. Price Target: $108.64 | Upside: 22.02%

Nasdaq is best known as the exchange where many of the world’s largest technology companies are listed.

However, that increasingly understates what the company has become.

Nasdaq now operates through three primary business segments:

Capital Access Platforms

Capital Access Platforms helps companies and investors access public and private capital markets. This segment includes Nasdaq’s stock-exchange listings, corporate services, real-time and historical market data, investment analytics, and corporate-governance tools. It also owns Nasdaq’s index business, including the Nasdaq-100, and collects licensing fees from ETFs, mutual funds, derivatives and structured products tied to its indexes.

Financial Technology

Financial Technology provides mission-critical software to banks, brokers, exchanges, regulators and other financial institutions. This includes Verafin’s fraud-detection and anti-money-laundering tools, AxiomSL’s regulatory-reporting software, trade-surveillance systems, and Calypso’s trading, clearing, treasury and risk-management technology.

Market Services

Market Services contains Nasdaq’s transaction-based businesses, including U.S. equity and options trading, European markets, fixed-income and commodity platforms, clearing services, trade-management tools and market-data revenue connected to trading activity.

This increasing diversification is important, because Nasdaq is gradually becoming less dependent on trading volume and more reliant on recurring software, data and licensing revenue.

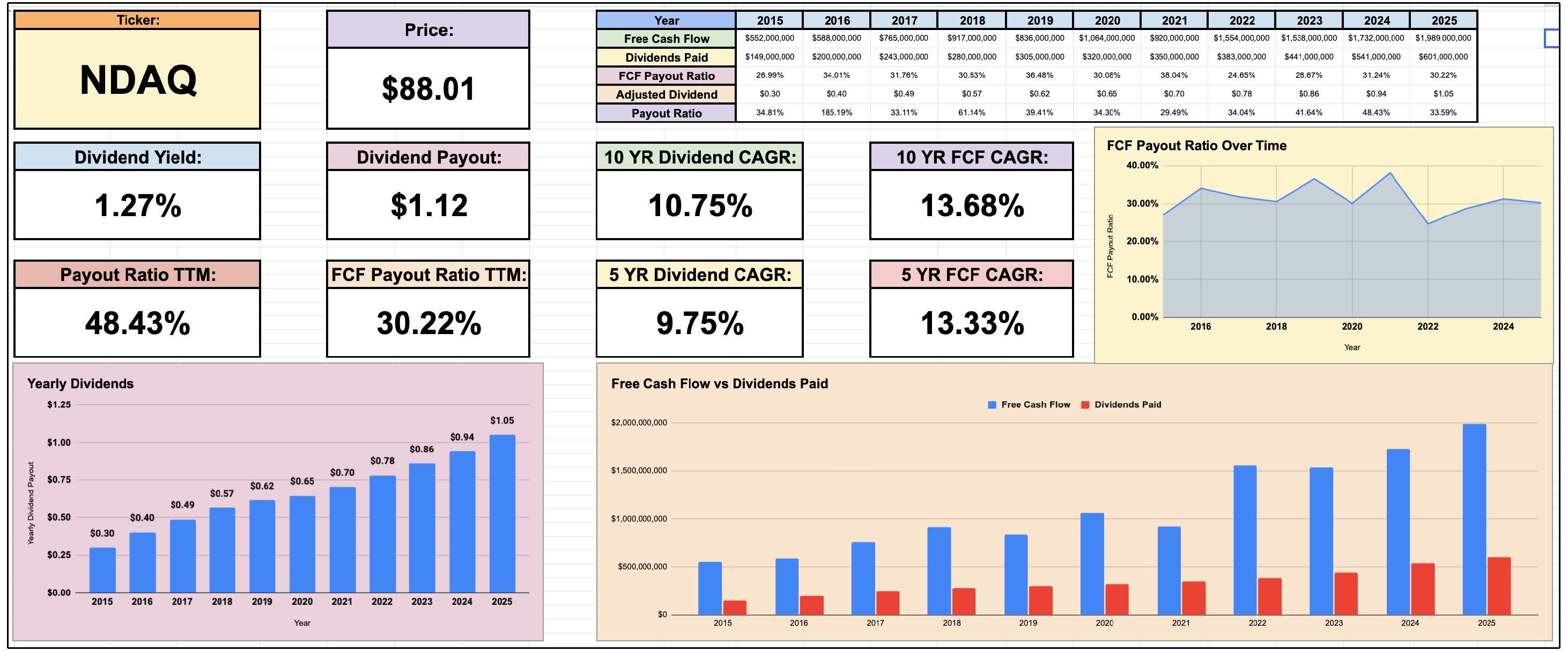

As a result of recurring cash flows, Nasdaq has been an incredibly reliable dividend grower.

They’ve managed to grow dividends at a double-digit rate over the last decade, while keeping the free cash flow payout ratio at just 30%.

At the same time, the business landscape for Nasdaq is shifting dramatically.

The next phase of Nasdaq’s transformation could come from agentic artificial intelligence.

Through Verafin, Nasdaq has introduced AI-powered fraud and anti-money-laundering analysts designed to automate work traditionally performed by compliance employees.

These products are expected to operate as overlays on top of competing legacy systems, allowing financial institutions to adopt Nasdaq’s AI tools without replacing their existing infrastructure.

That could shorten sales cycles and significantly expand Nasdaq’s addressable market.

Instead of selling an entirely new software platform, Nasdaq can offer a digital workforce that improves the systems banks already use.

Nasdaq also possesses a valuable data advantage.

Verafin’s consortium network includes thousands of financial institutions and hundreds of millions of accounts, giving its AI systems access to proprietary financial-crime data that general-purpose models cannot easily replicate.

Early deployments have reportedly reduced sanctions-alert workloads by as much as 90% and enhanced due-diligence time by approximately 50%.

If Nasdaq can price these products according to the labor and operating expenses they eliminate, Financial Technology margins could expand considerably.

If that transformation continues, I believe the company will command a higher valuation multiple that is typically assigned to financial technology platforms rather than traditional exchange operators.

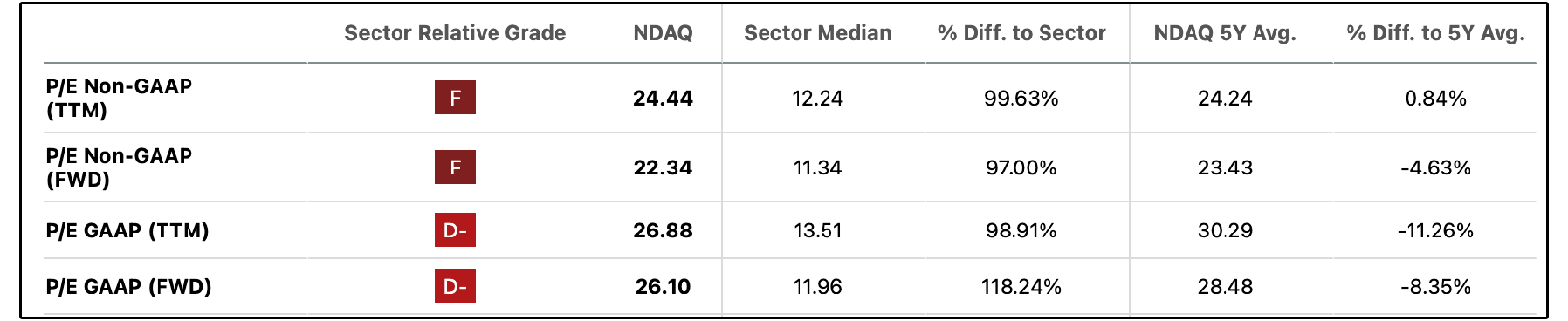

Nasdaq is already trading slightly below their historic valuation multiples.

The average analyst is projecting over 22% upside from current prices.

Now, let’s dive into the full list of dividend stocks with the most upside according to Wall Street.