🧾 List of Most Upside Dividend Stocks

Wall Street Price Targets Revealed 🎯

Every month, I compile data on the dividend stocks with the most upside based on Wall Street analysts price targets.

Members will get access to the full list every month, as well as all other Dividendology features.

This month, only 48 stocks made the list.

Let’s dive in.

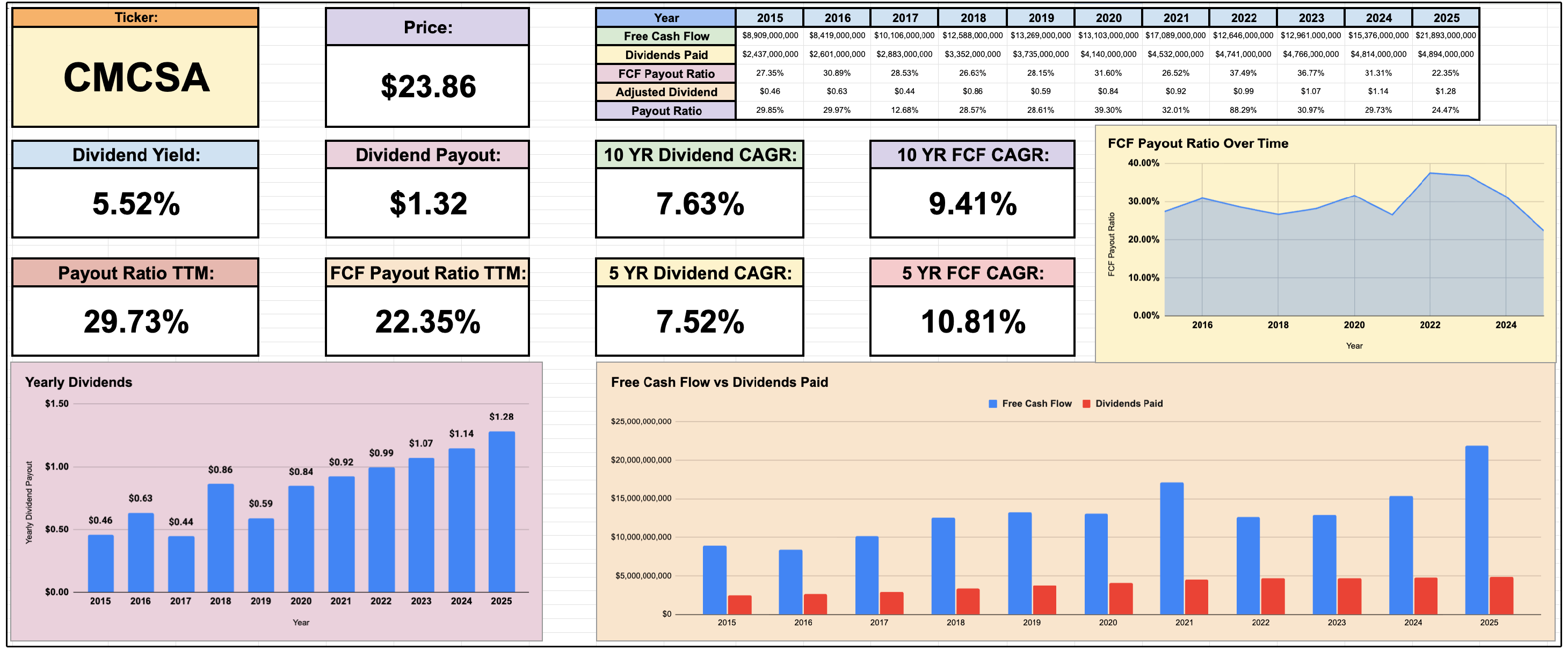

1. 📡 Comcast (CMCSA)

Wall St. Price Target: $33.14 | Upside: 35.25%

Comcast is now down over 58% in the last year-

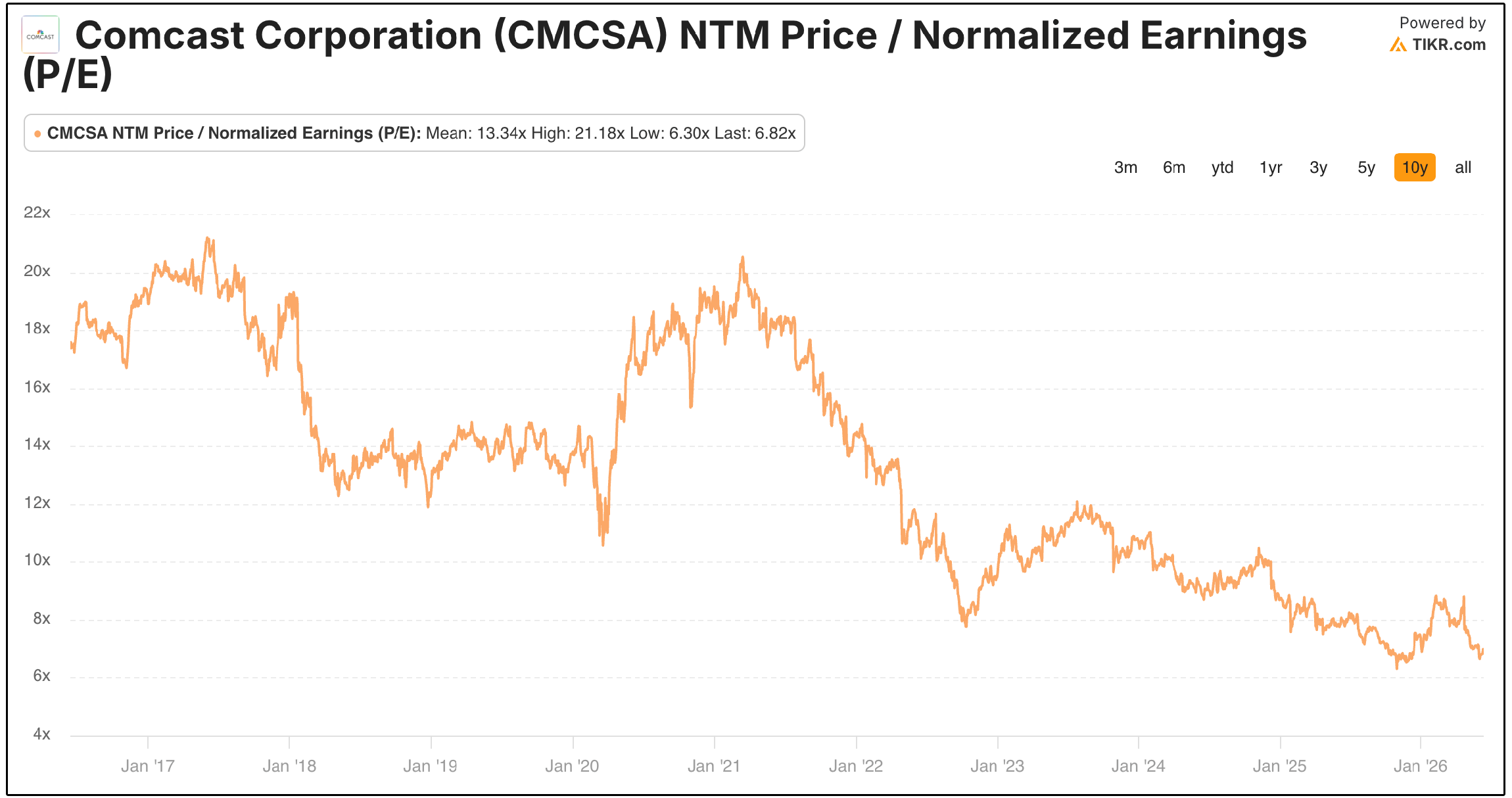

And the valuation multiple is at historically low levels.

Comcast currently trades at a forward P/E of just 6.82x.

However, the market’s pessimism is not entirely unfounded.

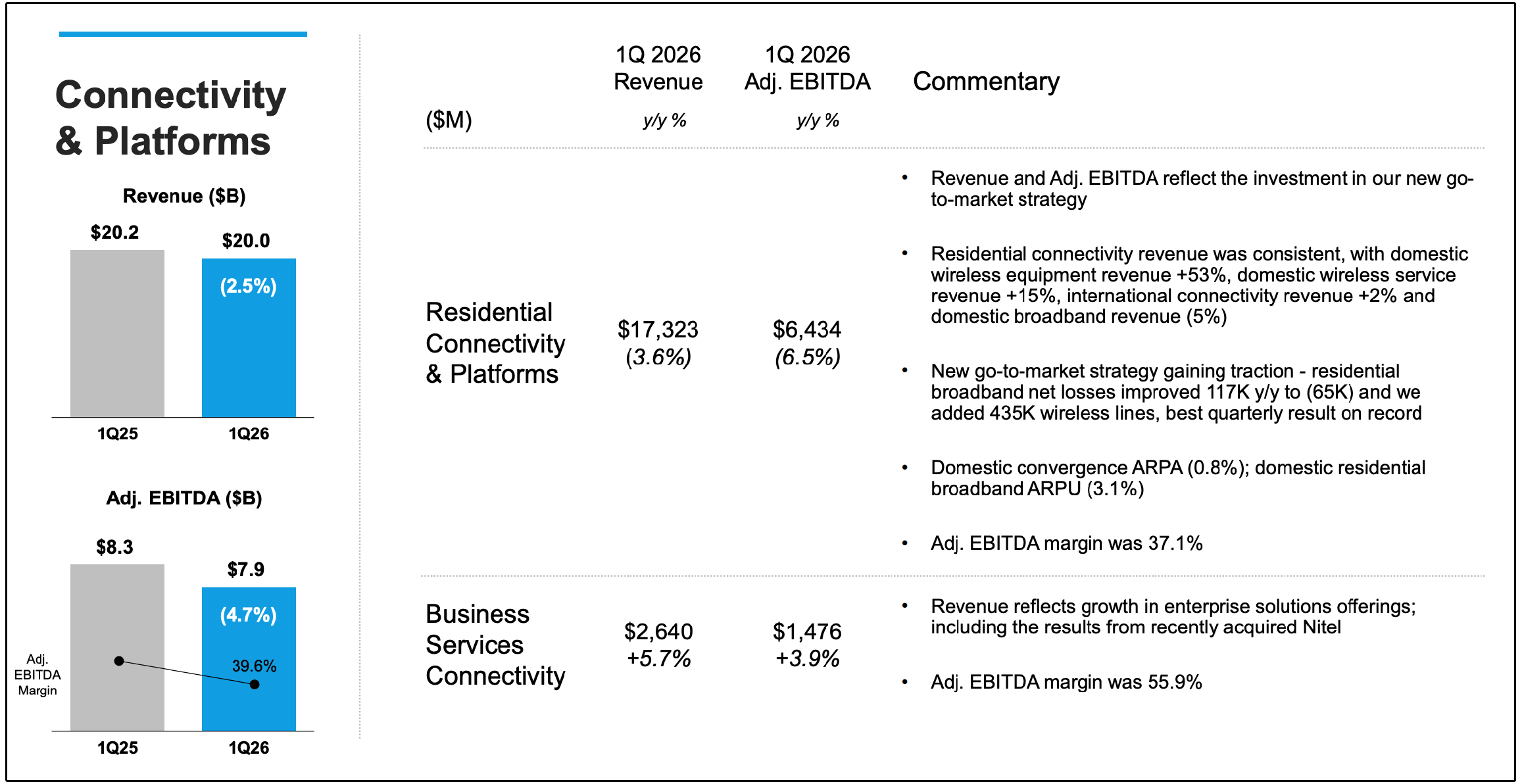

Comcast’s most important business has historically been residential broadband.

Customers pay recurring monthly fees for internet access, creating a sticky, high-margin stream of cash flow.

Unfortunately, increased competition from fiber providers and fixed-wireless services has placed pressure on this business.

During the first quarter of 2026, domestic broadband revenue declined 5% year over year.

The core business is currently in decline, which explains the historically low valuation multiple.

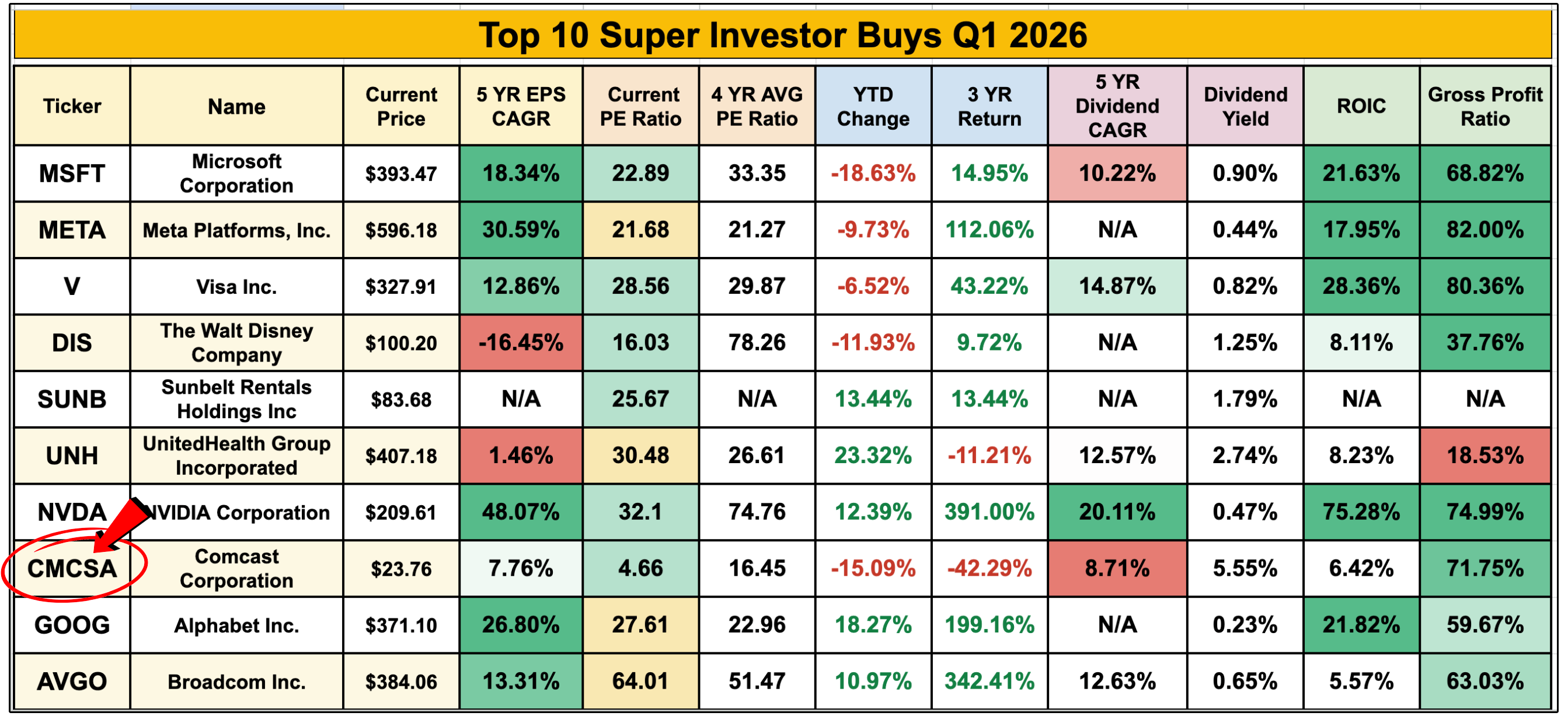

Despite this, Comcast was one of the most frequently bought dividend stocks by super investors ($100M+ in AUM) in the most recent quarter.

While most super investors were buying quality dividend growers like MSFT, Visa, and AVGO-

Comcast was the 8th most bought stock, and by far the highest yielding stock purchased.

Why might this be the case when the core business is in decline?

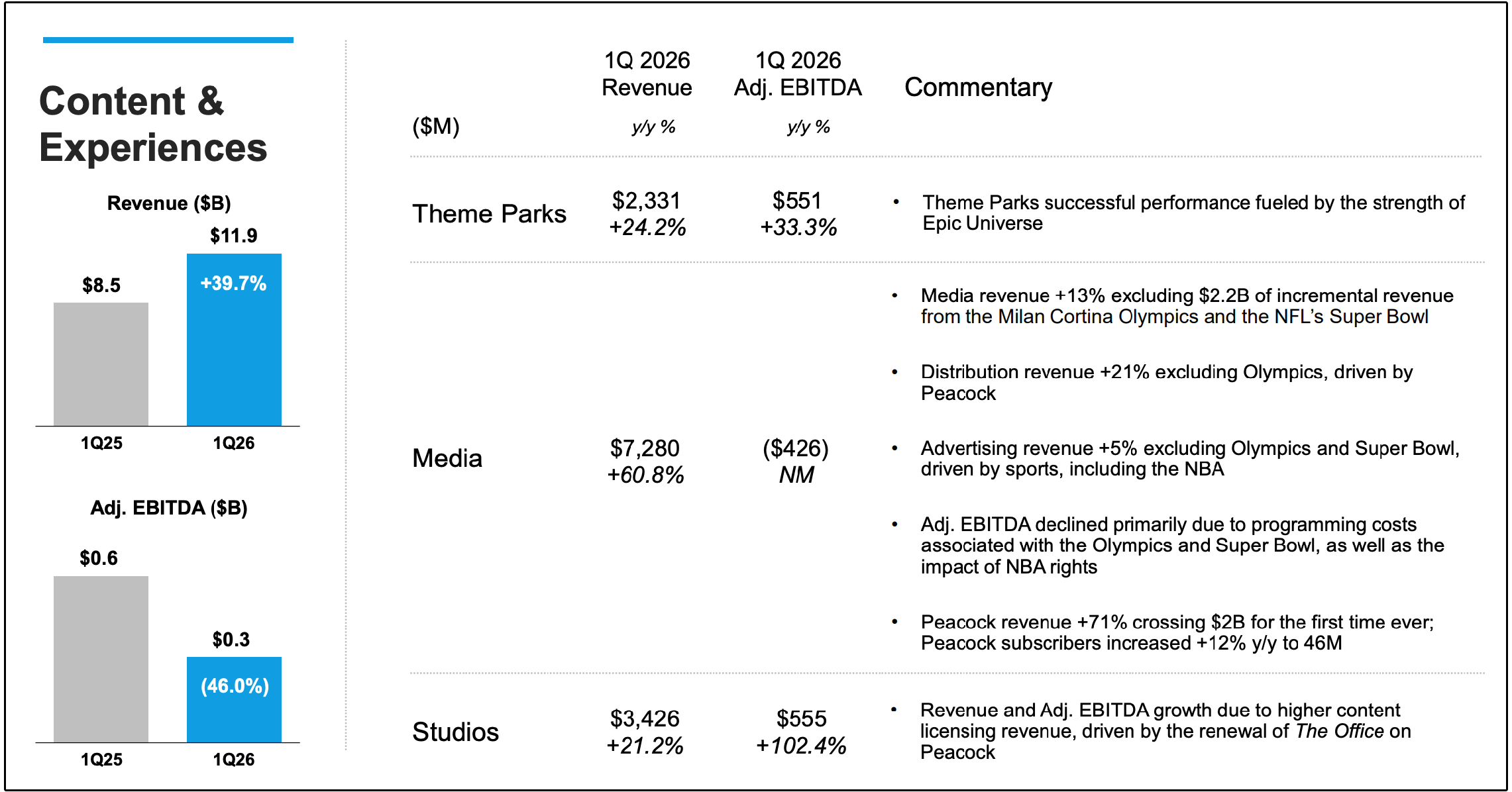

While most investors primarily associate Comcast with cable and internet, the company also owns a valuable collection of media and entertainment assets.

These include NBC, Universal Pictures, DreamWorks, Illumination, Peacock and Universal theme parks.

Peacock’s paid subscribers increased 12% year over year to 46 million during the first quarter, while revenue increased 71% and surpassed $2 billion.

Theme park revenue as well as studios revenue both grew at over 20%.

While these are certainly smaller business segment’s than the core business, they are still helping offset some of the weakness within traditional broadband and cable television.

With the decline in prices, the company now yields over 5.5%, with historical dividend growth rates of above 7.5%.

At the same time, the free cash flow payout ratio remains below 25%.

While earnings growth is expected to be quite low over the next few years, the company has plenty of room to grow dividends in the future.

Growing the dividend at 4% moving forward would imply an intrinsic value of $29.59, implying almost 25% upside.

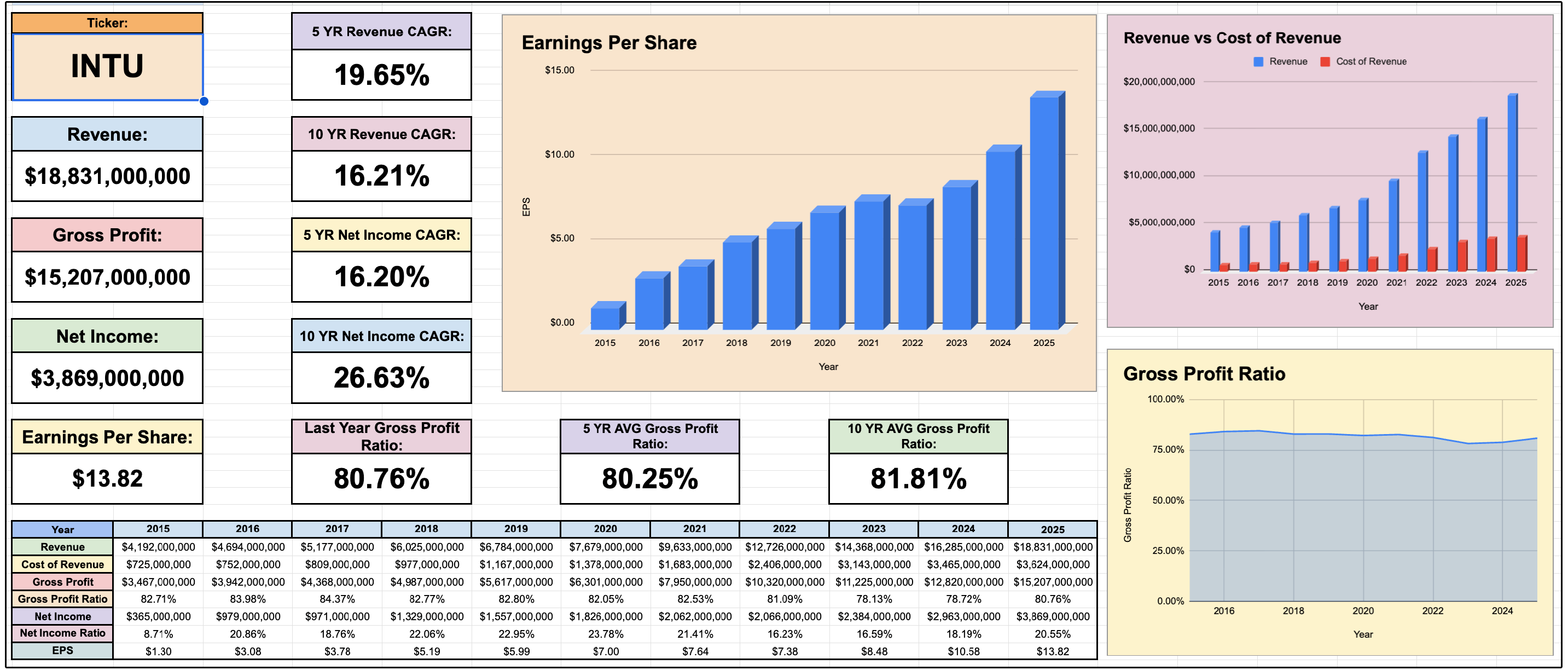

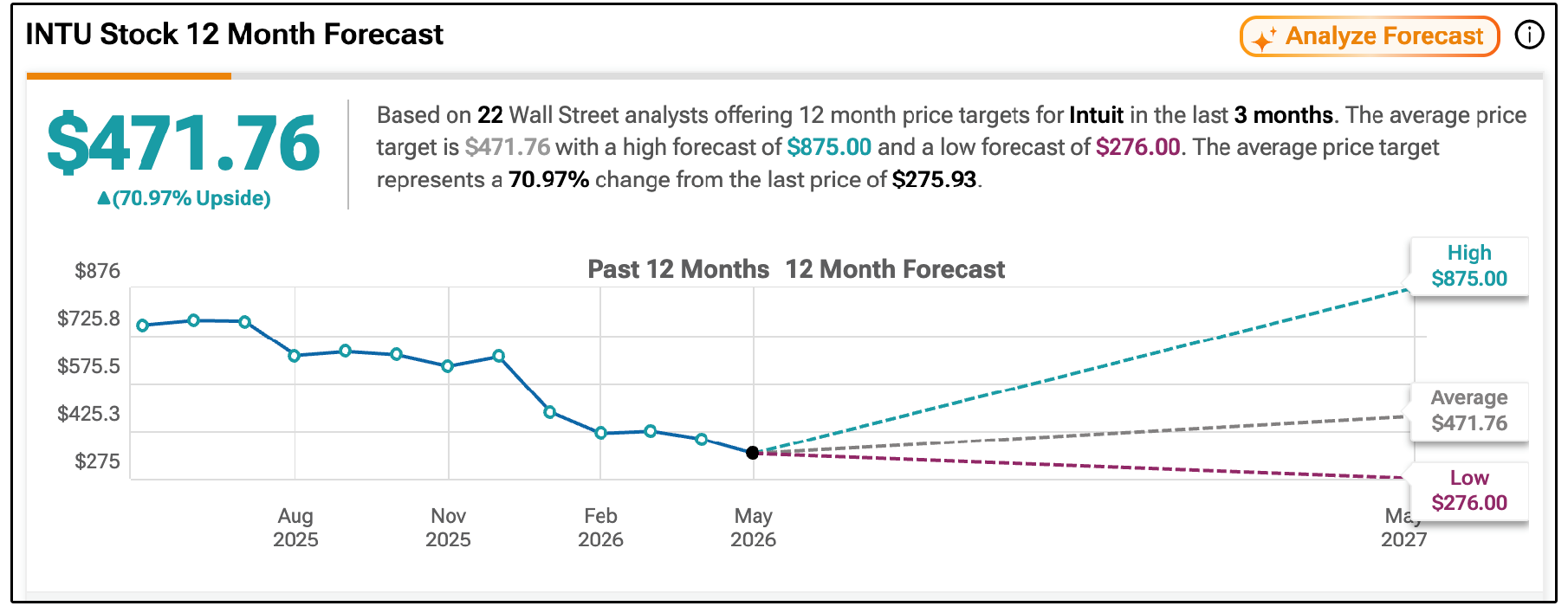

2. 🧮 Intuit (INTU)

Wall St. Price Target: $471.76 | Upside: 70.97%

Intuit is one of the most interesting companies on this month’s list.

Why?

Because they are one of the worst performing stocks in the S&P 500 in the last year, down over 63% due to the threat of AI disruption.

The company operates four major financial platforms:

TurboTax, the leading consumer tax preparation platform in the United States.

QuickBooks, which provides accounting, payroll and payment-processing software to small and midsized businesses.

Credit Karma, a personal finance platform with more than 100 million members that generates revenue through financial product referrals.

Mailchimp, which provides email marketing and customer relationship management tools for small businesses.

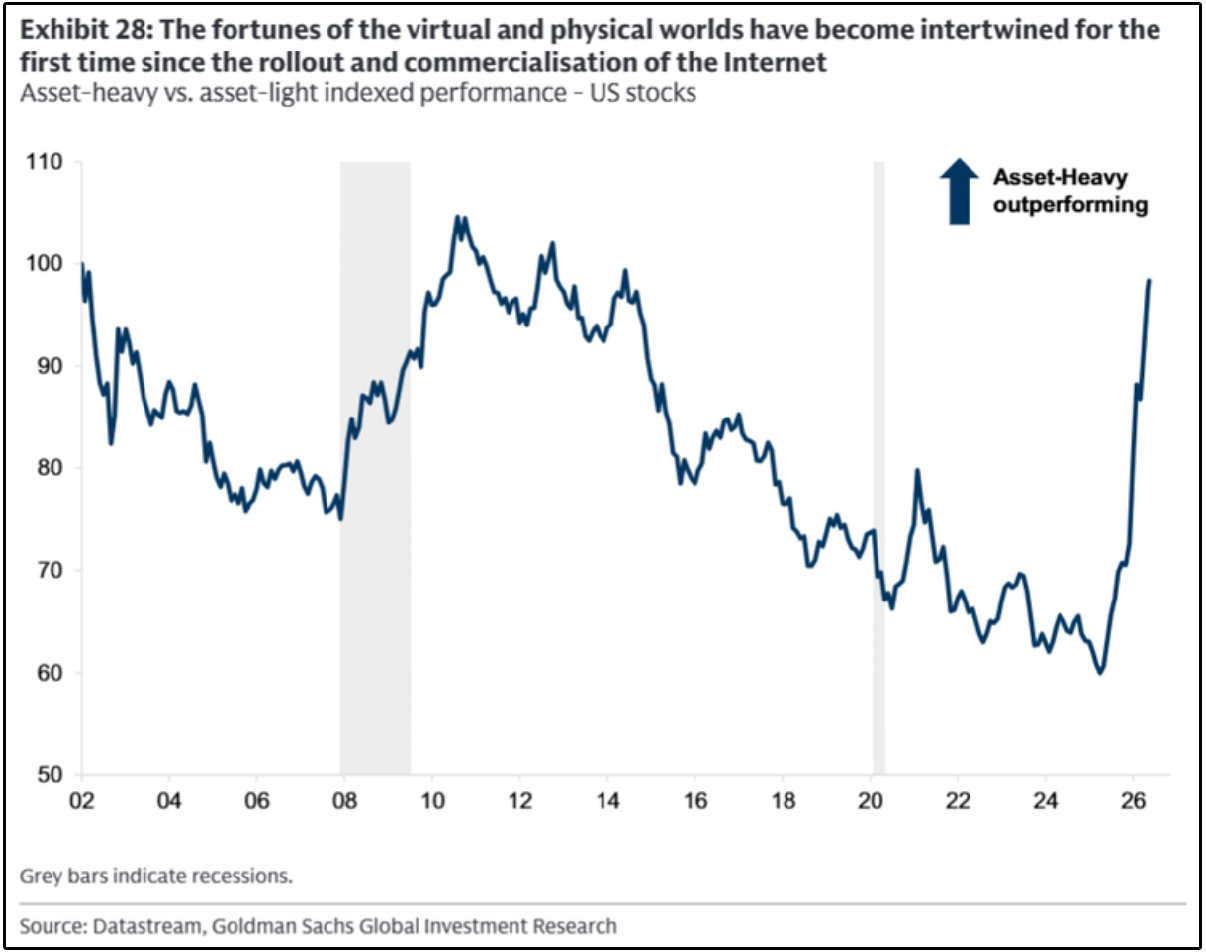

Intuit’s subscription-heavy business model has historically produced highly predictable revenue growth, high margins, and substantial free cash flow.

This is the exact type of capital light business model that has historically outperformed over the last decade.

These are businesses with high margins and generate high returns on invested capital.

However, we seen a drastic shift recently, as asset heavy companies have started to outperform.

In their recent earnings report, management actually raised its full-year outlook to approximately $21.34 billion in revenue and between $23.80 and $23.85 in non-GAAP earnings per share.

However, the concern of business disruption due to artificial intelligence is growing.

In theory, an advanced AI agent could gather information from financial documents, interpret the tax code, identify deductions and prepare a tax return without requiring the customer to navigate traditional tax software.

The same threat applies to QuickBooks.

AI agents could eventually categorize transactions, reconcile accounts, create invoices, manage payroll and produce financial statements.

If these tools become reliable enough, customers may question why they need several separate software subscriptions.

Recent weakness in TurboTax has added to these concerns.

Intuit expects total TurboTax Online units to decline approximately 2% during fiscal 2026, while its share of electronically filed tax returns is expected to decline by roughly one percentage point.

However, the counter argument is that Intuit may also be one of the companies best positioned to benefit from AI.

The company has decades of financial data, trusted relationships with consumers and businesses, and deep integrations with banks, tax authorities and payroll systems.

Intuit has also partnered with OpenAI and Anthropic and is embedding AI throughout TurboTax and QuickBooks.

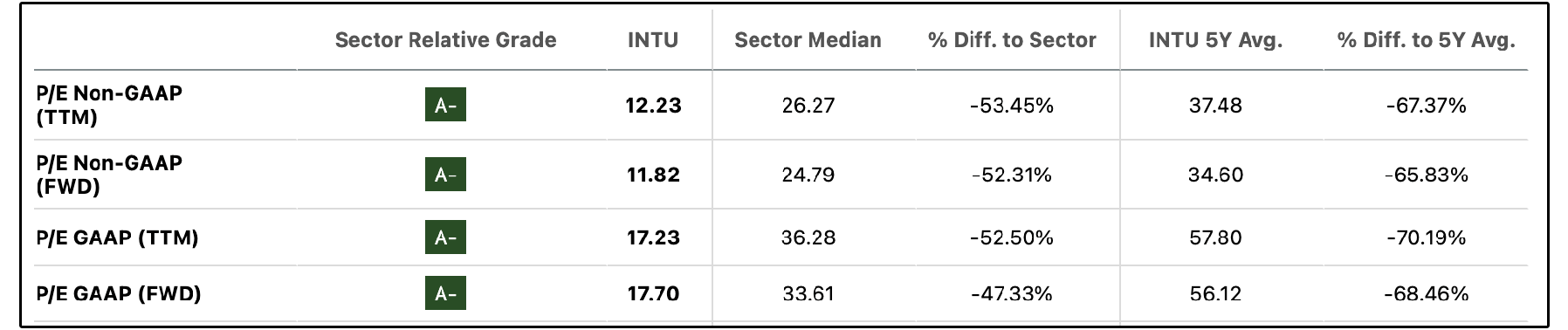

The valuation has also compressed dramatically from its historical average.

While the market seems to be waiting to see if AI will disrupt Intuit, the average Wall Street price target now gives them over 70% upside after significant multiple compression.

3. 📊 S&P Global (SPGI)

Wall St. Price Target: $537.38 | Upside: 26.72%

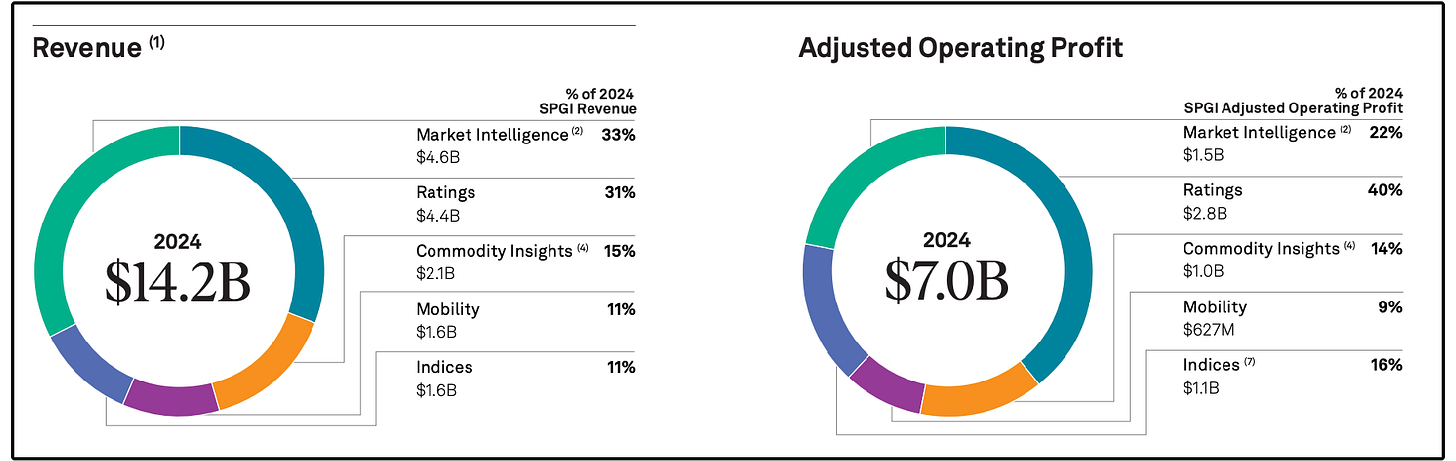

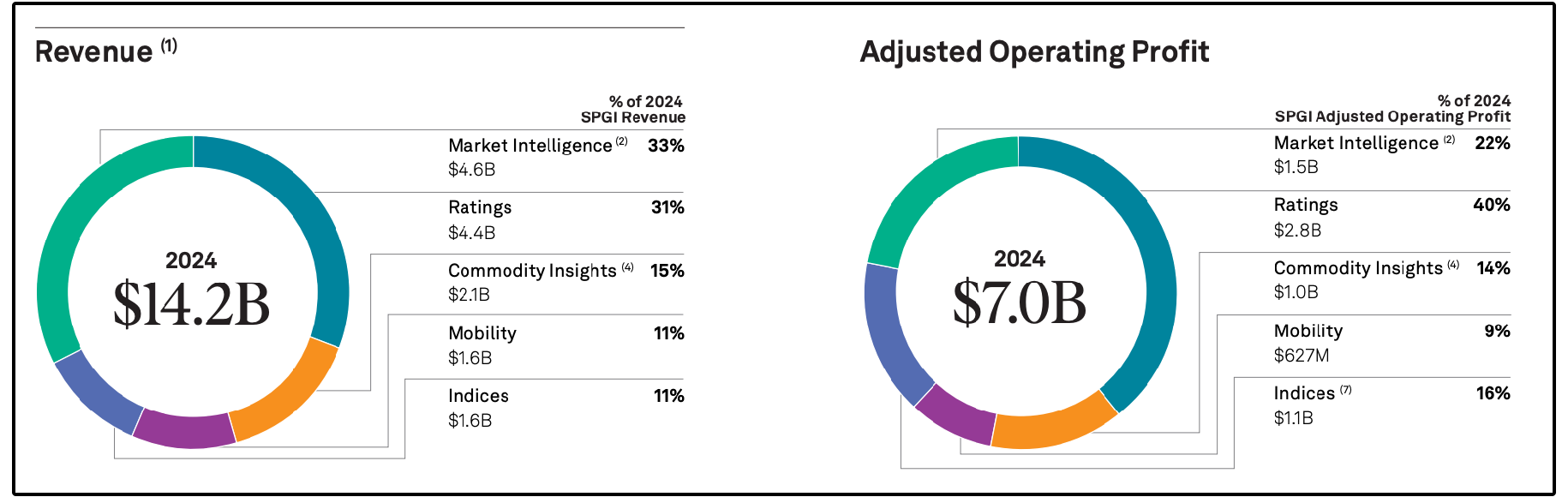

S&P Global provides essential financial infrastructure through four core businesses:

S&P Global Ratings – One of the world’s largest credit-rating agencies, providing ratings and research on corporate, government, municipal, and structured debt. This segment generates roughly 31% of revenue.

S&P Dow Jones Indices – Home to the S&P 500, Dow Jones Industrial Average, and thousands of benchmarks used by ETFs, index funds, pension plans, and derivatives. This segment accounts for roughly 11% of revenue.

S&P Global Market Intelligence – Provides financial data, analytics, and workflow tools through platforms such as Capital IQ Pro. This is the company’s largest segment at roughly 33% of revenue.

S&P Global Energy – Delivers proprietary pricing, benchmarks, data, and analytics for global energy and commodity markets. This segment generates approximately 15% of revenue.

Through these businesses, S&P Global sits at the center of debt issuance, passive investing, commodity markets, and institutional decision-making worldwide.

What makes the business so powerful is its combination of deep entrenchment, recurring revenue, and exceptional cash generation.

Its ratings business benefits from regulatory recognition, decades of credibility, and a highly concentrated competitive landscape.

Its indices are equally difficult to disrupt.

The S&P 500 is not simply a dataset, it’s a globally accepted financial standard embedded into trillions of dollars of ETFs, mutual funds, retirement accounts, derivatives, and investment mandates.

As assets tied to these benchmarks grow, S&P Global collects additional licensing revenue with very little incremental cost.

This creates a beautiful business model.

Despite these advantages, shares have sold off as investors worry that artificial intelligence could disrupt financial data providers.

However, the market may be misunderstanding what S&P Global actually does.

AI can improve data processing and research workflows, but it cannot easily replace regulatory-recognized credit ratings, institutional trust, proprietary datasets, or globally accepted benchmarks.

S&P Global is also set to become a major beneficiary of AI.

The company acquired Kensho in 2018 and has continued investing in AI tools that analyze financial documents, automate workflows, and enhance Capital IQ Pro.

Rather than replacing S&P Global, AI could make its data and platforms more valuable.

S&P Global is also spinning off its Mobility division, which includes CARFAX and other automotive data businesses.

The separation should simplify the company and improve the remaining firm’s growth and margin profile.

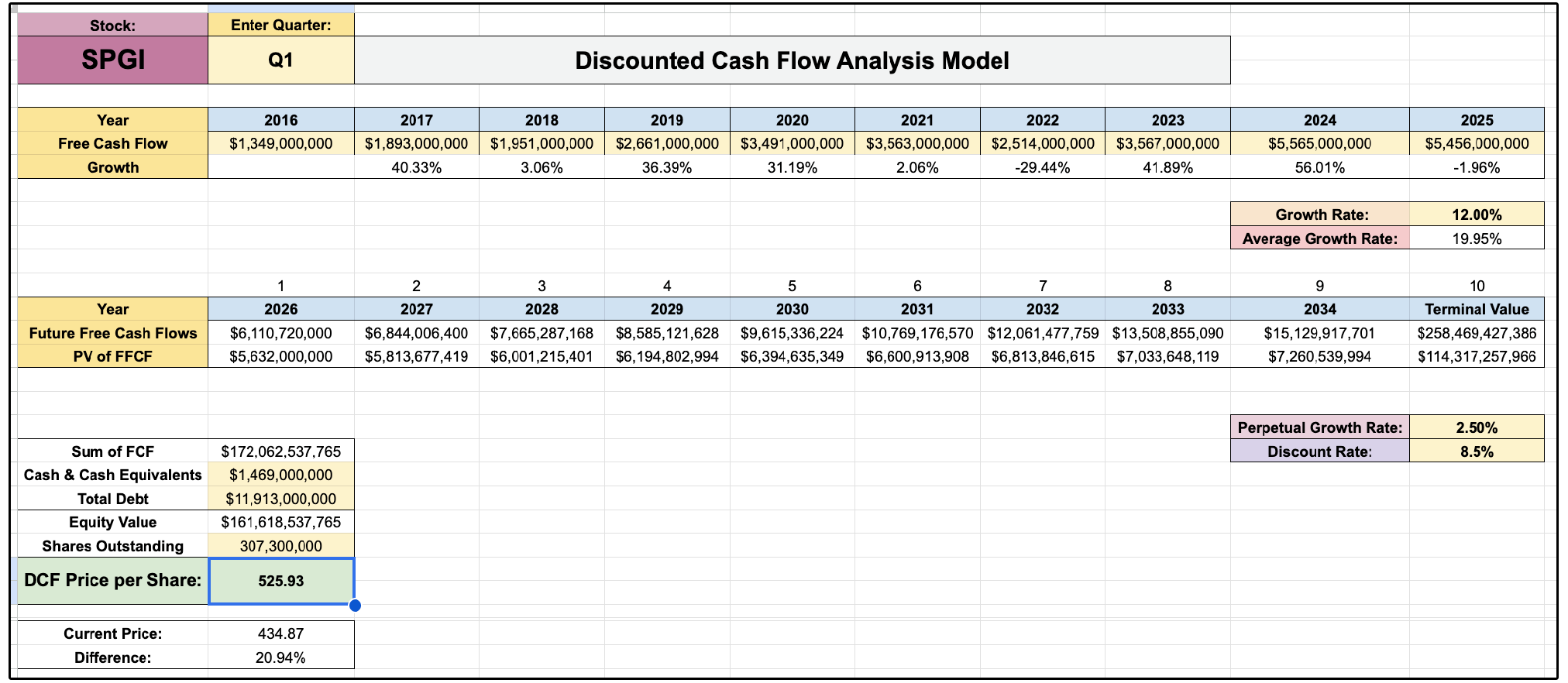

Assuming 12% free cash flow growth, which is in line with estimates, SPGI fair value would be sitting at $525.93 according to our DCF model.

Now, let’s dive into the full list of dividend stocks with the most upside according to Wall Street.