🧾 List of Most Upside Dividend Stocks

Wall Street Price Targets Revealed 🎯

The real alpha lies in AI bottlenecks.

Most investors are late to the Mag-7 party. While these companies continue to get all the attention, Market Sentiment focuses on identifying the second-order effects early.

They were the first to cover the Optics Trade with the basket now up 53%. Their Advanced Packaging Thesis is also now playing out in real time with the portfolio up 62% in three months. They predicted the AI energy bottleneck last year.

Tomorrow, they are launching the Agentic Basket where they cover the second-order winners of the agent buildout.

For the next 24 hours, Dividendology readers can now unlock full access to Market Sentiment at a special discounted rate.

Thanks to Market Sentiment for sponsoring.

🎯 Most Upside Dividend Stocks

Every month, I compile data on the dividend stocks with the most upside based on Wall Street analysts price targets.

Members will get access to the full list every month, as well as all other Dividendology features.

This month, only 47 stocks made the list.

Let’s dive in.

1.🛒 Dollar General (DG)

Wall St. Price Target: $151.06 | Upside: 44.37%

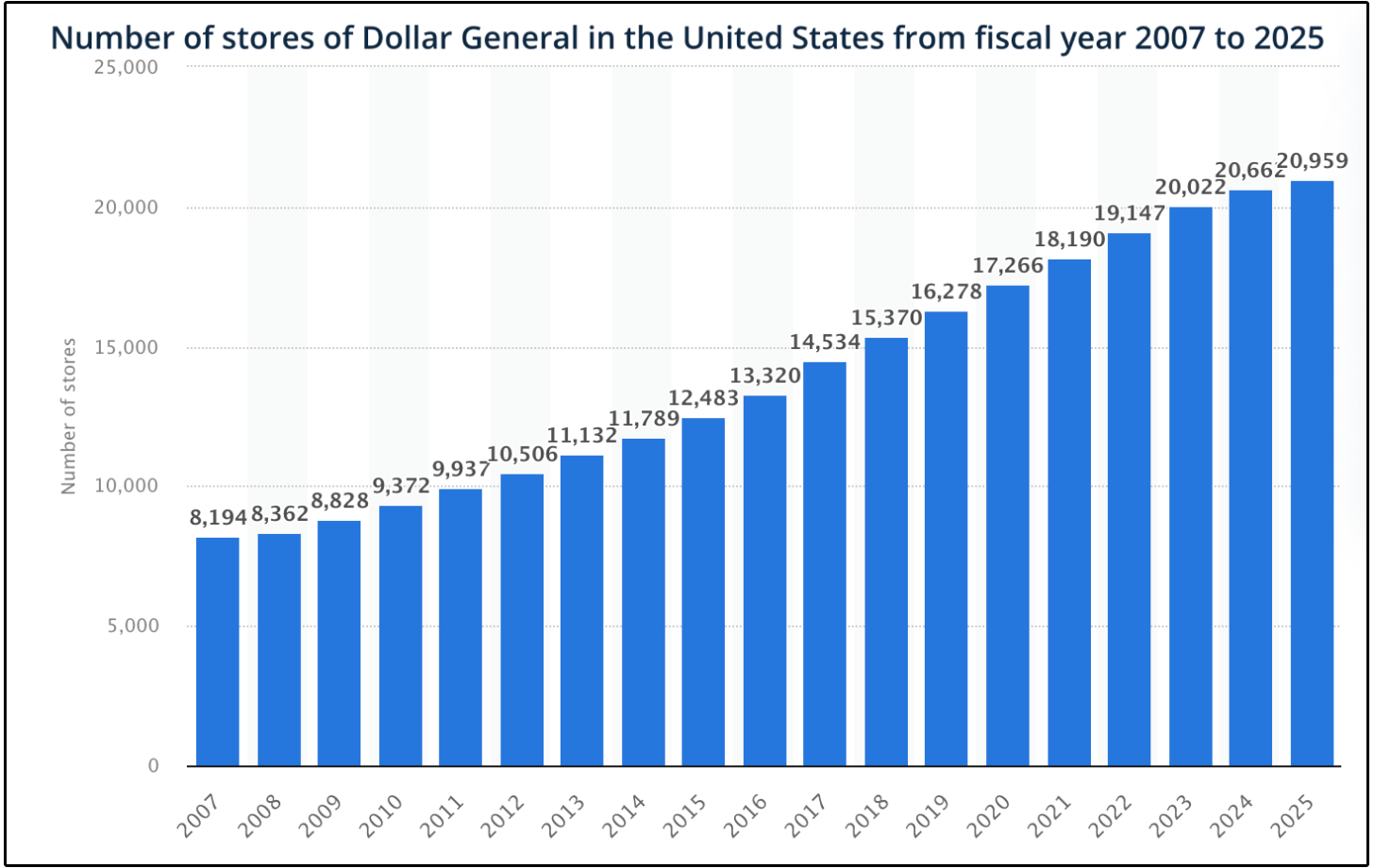

Dollar General is one of the largest discount retailers in the United States, with over 20,893 stores nationwide as of fiscal year-end 2025.

The business model is incredibly simple:

Sell everyday essentials, at low price points, in small-format stores, in places larger retailers won’t go.

Roughly 80% of Dollar General’s stores are located in towns with populations of 20,000 or less, with their core customer base being lower to middle-income households, particularly in rural and small-town America.

This is a customer base that competitors like Walmart, Target, and Amazon have historically struggled to reach efficiently.

Dollar stores have been one of the most quietly powerful growth stories in U.S. retail.

Over the past decade, the total number of dollar stores in the U.S. has roughly doubled from 20,000 to over 40,000, and 88% of Americans now report having shopped at one.

Dollar General has gone from 8,194 stores in 2007 to 20,959 as of 2025, which is around a 156% increase in store count.

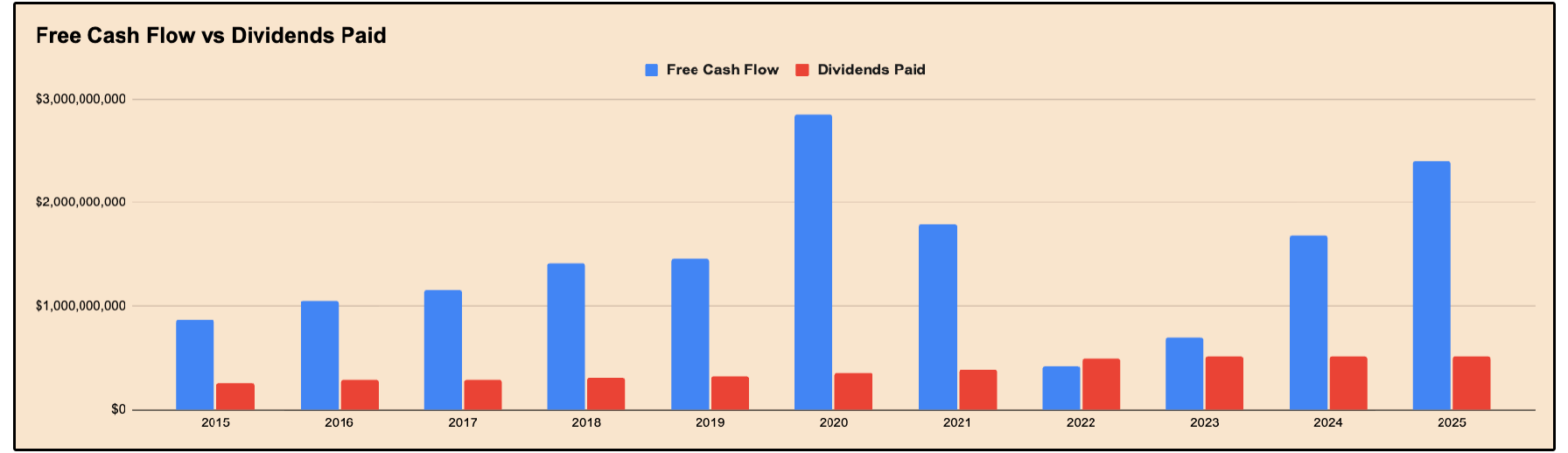

DG’s free cash flow over the last decade doesn’t look like a smooth compounder.

In fact, it’s been a bit of a roller coaster:

~$870M in 2015

~$1.45B in 2019

~$2.85B in 2020 (pandemic boost)

$430M in 2022 when working capital reversed, shrink hit, and capex ramped.

This is exactly why management held the dividend flat through 2022–2023.

FCF has now recovered to ~$1.7B in FY24 and ~$2.4B in FY25.

Despite the volatility in free cash flow in recent years, the long-term story combined with the macro environment we are operating in makes DG quite interesting.

Take a few things into consideration:

Inflation just ramped up to its highest level in over 3 years

Consumer budgets are becoming increasingly stretched

Credit card delinquencies and consumer debt levels remain elevated

All of these macro factors are contributing to the widening of the ‘K-shaped’ economy.

And ironically enough, Dollar General is set to benefit from this.

Dollar General operates in one of the most resilient areas of retail, value-focused consumer spending.

And historically, periods of economic pressure have often strengthened the company’s positioning as consumers trade down and become more price conscious.

That’s part of why the market may be underestimating the business today.

At the same time, Dollar General still has a massive physical footprint advantage.

The company estimates that roughly 75% of the U.S. population lives within five miles of a Dollar General location, giving it one of the most accessible retail networks in the country.

And unlike many traditional retailers, Dollar General’s smaller-box model allows stores to operate profitably in lower-density rural markets where competitors often cannot justify expansion.

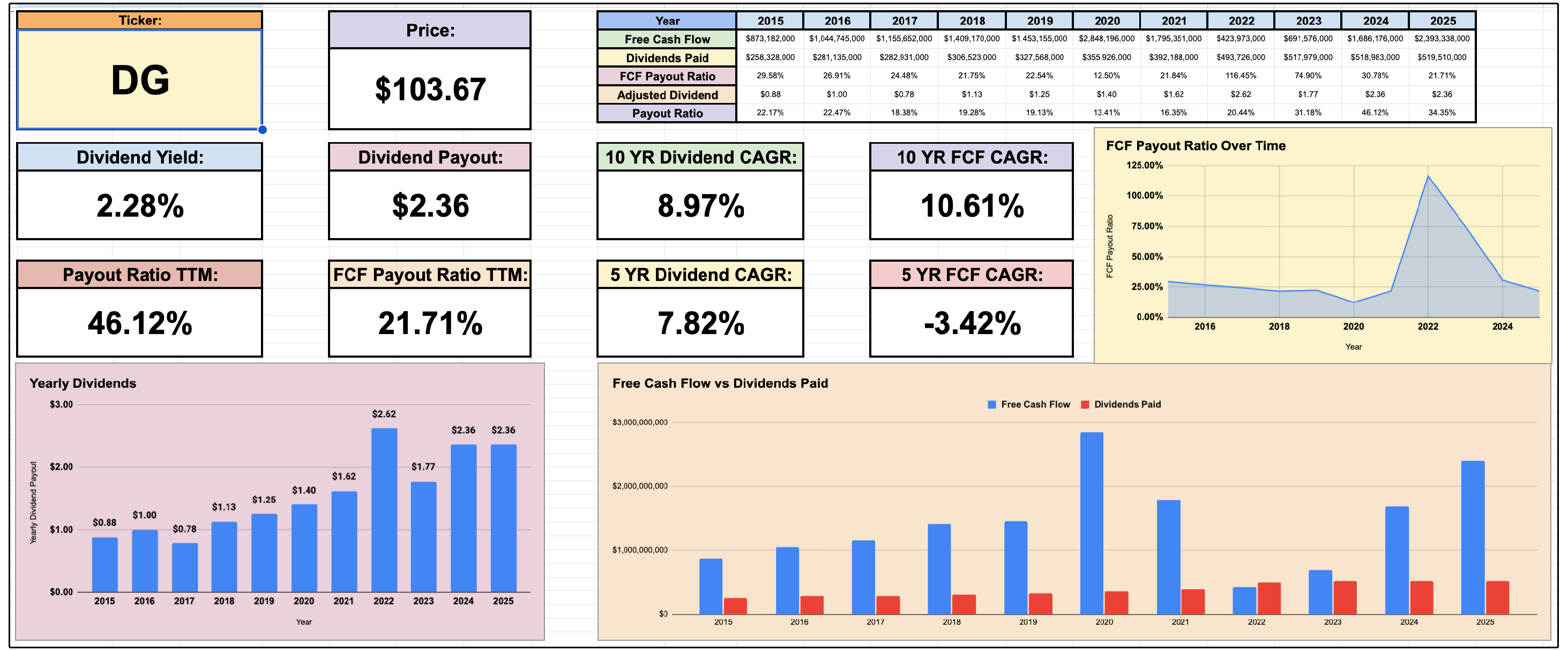

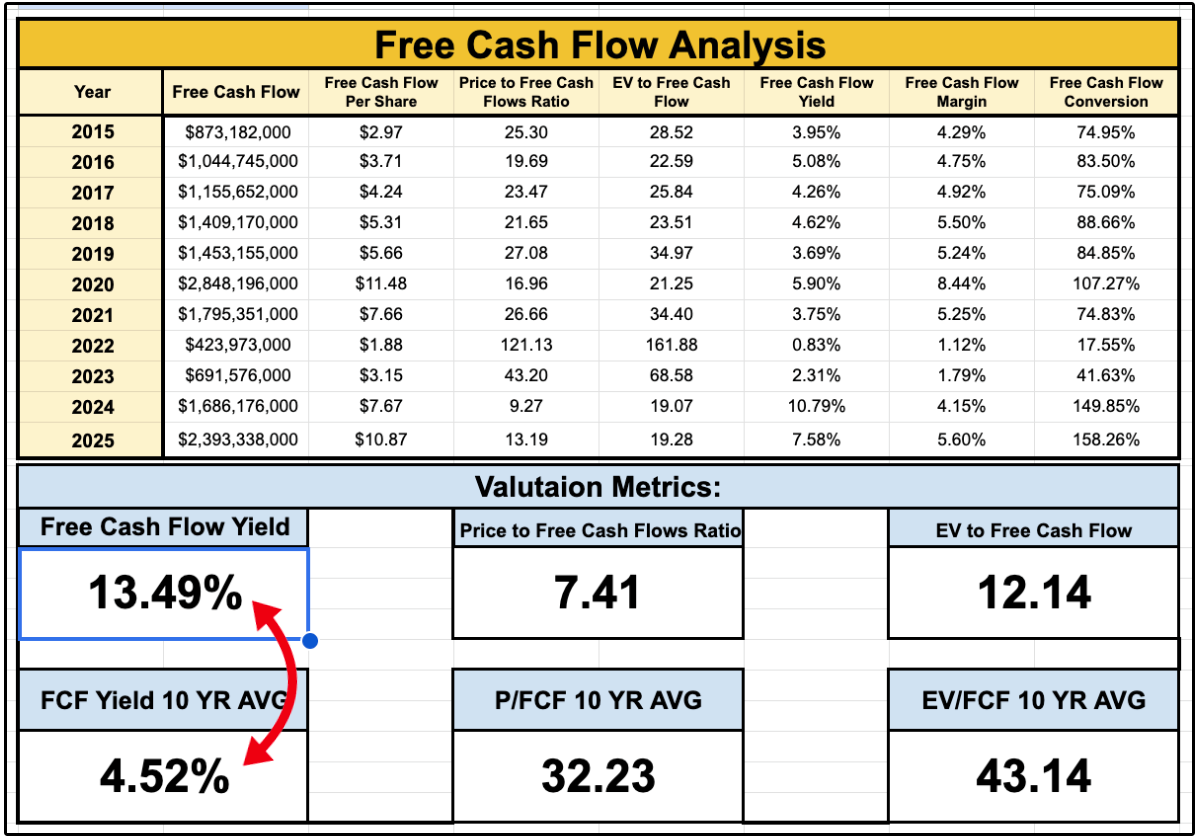

The stock currently yields around 2.28%, which is 40% above its historical average yield, while the payout ratio remains conservative compared to many mature retailers.

But perhaps what is most interesting, is if we look at their free cash flow from a valuation standpoint.

The 10 year average free cash flow yield sits at 4.52%, meaning every $100 you invest into the stock would generate around $4.52 in free cash flow in year one.

However, their current free cash flow yield now sits way above their 10 year average, at 13.49%!

With earnings and free cash flow projected to grow at mid to high single digits in the next couple of years, combined with the fact they have macro factors working in their favor, DG could be a hidden gem over the next few years.

And with Wall Street currently projecting over 44% upside from current levels, Dollar General may be one of the more interesting contrarian dividend growth opportunities in today’s market.

2. 💊 Merck & Co. (MRK)

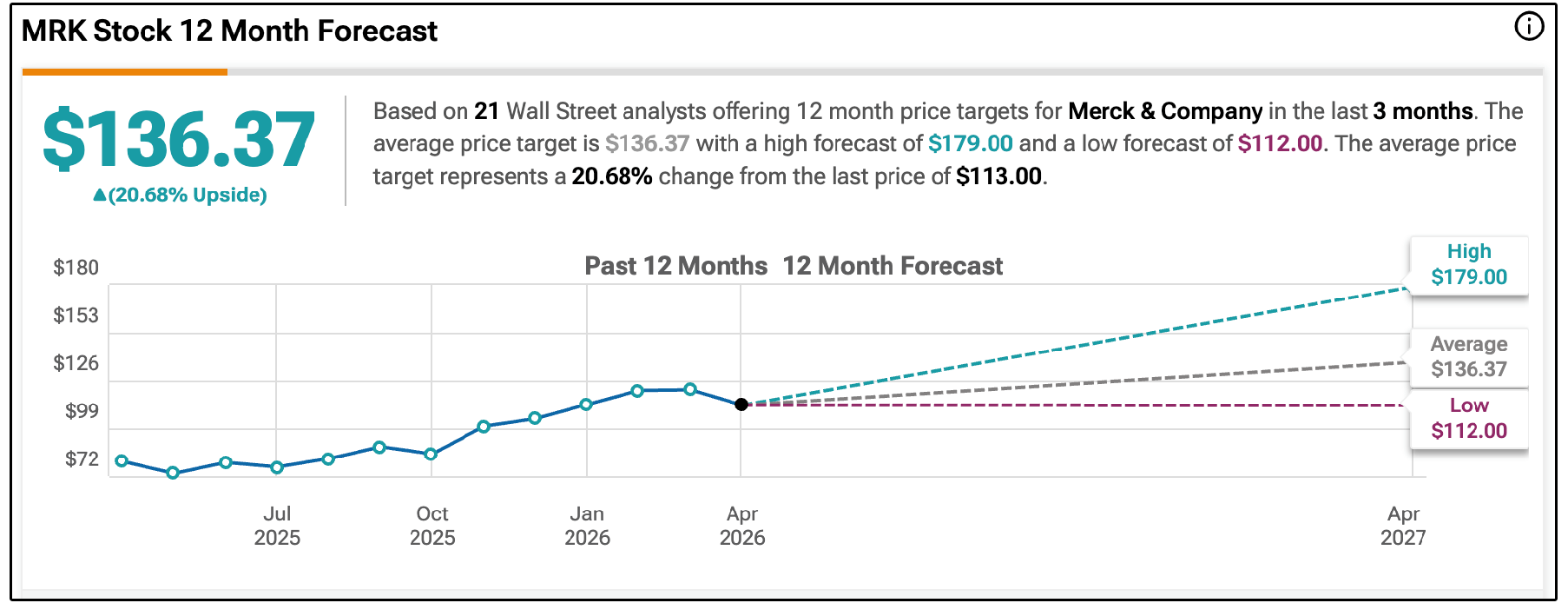

Wall St. Price Target: $136.37 | Upside: 20.68%

Merck is one of the largest pharmaceutical companies in the world, and right now it is also one of the most controversial stocks in the entire dividend universe.

Most of the controversy comes down to one drug: Keytruda.

Keytruda is Merck’s blockbuster cancer immunotherapy and currently the best-selling prescription drug in the world.

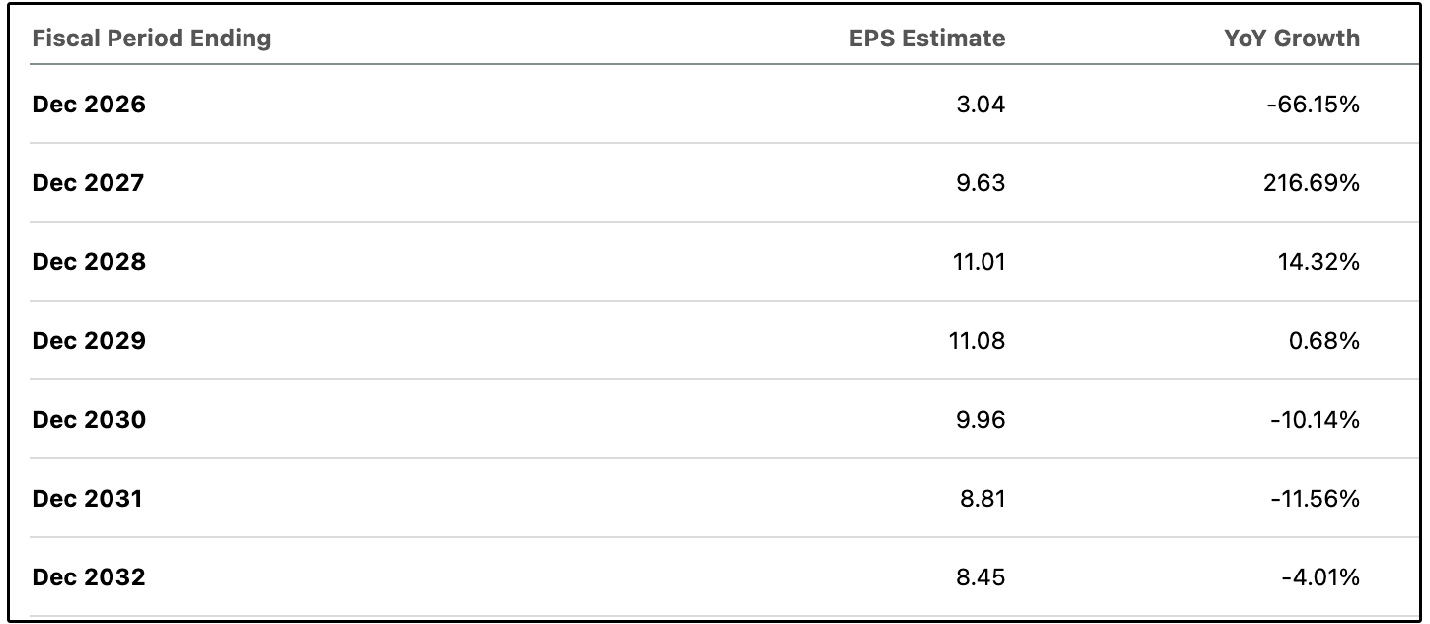

In 2025, it generated over $30B in sales, representing nearly half of Merck’s total revenue, and its primary patents begin expiring in 2028.

As a result, take a look at what EPS growth projections look like starting in 2029…

That is the entire bear case in one sentence.

Wall Street has been pricing this in for two years, which is why MRK is currently still in a drawdown of 16% over the last 3 years-

But to be fair, it was once in a drawdown of over 44% in Summer of last year.

Of course, as a result of this sell off, the starting dividend yield is now around 3%, with a 5 year dividend CAGR of 4.93%.

But with the free cash flow payout ratio already at 66%, replacing the cash flows from Keytruda becomes incredibly important for the dividend to remain sustainable.

The reason Wall Street currently seems bullish is because Merck has been preparing for this patent cliff for years.

Management understands exactly how important Keytruda is to the business, and they have aggressively used the company’s massive cash flows to build what they hope becomes the next generation of growth drivers.

That includes:

Expanding Keytruda into additional cancer indications before patent expiration

Developing a subcutaneous version of Keytruda that could extend exclusivity beyond the current patent window

Acquiring new assets and pipeline candidates

Rapidly scaling newer growth platforms outside of oncology

One of the biggest areas investors are watching is Winrevair, Merck’s recently launched pulmonary arterial hypertension drug acquired through the Acceleron deal.

Many analysts believe Winrevair could eventually become a multi-billion-dollar blockbuster on its own, with some estimates projecting peak annual sales north of $5B.

The company also continues to see strong growth from drugs and segments like:

Gardasil

Animal Health

New oncology assets

Cardiovascular treatments

Wall Street is currently giving them a price target of $136, implying 20% upside.

However, I’m personally not convinced, especially from a risk adjusted basis.

Losing exclusivity on the best-selling drug in the world is a major event for any pharmaceutical company, and revenue growth will likely become much more challenging later this decade.

Future cash flows for pharmaceutical companies are incredibly hard to project, and while the pipeline is being expanded, I’m not quite sure it will be at a level where they can completely replace the cash flows from keytruda in just a few years.

Merck trades at a forward P/E of 18.19 according to TIKR, which is to high for my liking for a stock with declining EPS and unpredictable future cash flows.

3. 📊 Intercontinental Exchange (ICE)

Wall St. Price Target: $199.91 | Upside: 26.67%

If you’ve ever bought a stock listed on the New York Stock Exchange, traded a Brent crude futures contract, or taken out a mortgage in the U.S. in the last few years, there is a very strong chance Intercontinental Exchange touched that transaction.

ICE is one of those rare businesses that quietly owns the rails the rest of the financial system runs on.

The company operates three core segments:

Exchanges (~54% of revenue):

The New York Stock Exchange, ICE Brent (the global oil benchmark), natural gas markets, agricultural futures, and interest rate products. In full year 2025, this segment generated $5.4B in revenue with a 75% adjusted operating margin.

Fixed Income & Data Services (~24% of revenue):

Bond pricing, indices, reference data, analytics. A sticky, subscription-style business that did $2.4B in 2025 revenue with a 45% adjusted operating margin. This is one of the more attractive segments in my opinion.

Mortgage Technology (~22% of revenue):

Built through Ellie Mae (2020) and Black Knight for $11.9B in 2023. ICE now powers a meaningful percentage of U.S. mortgage origination and servicing software.

The key thing to understand about ICE is the moat.

Exchanges have extreme network effects: liquidity attracts liquidity.

Once a futures contract becomes the global benchmark for something like Brent crude, it is almost impossible to displace.

That dynamic creates one of the strongest competitive advantages in all of finance.

Because once market participants, institutions, and hedgers standardize around a benchmark, switching becomes incredibly difficult.

That is why ICE’s exchange business consistently produces extremely high margins and recurring cash flows.

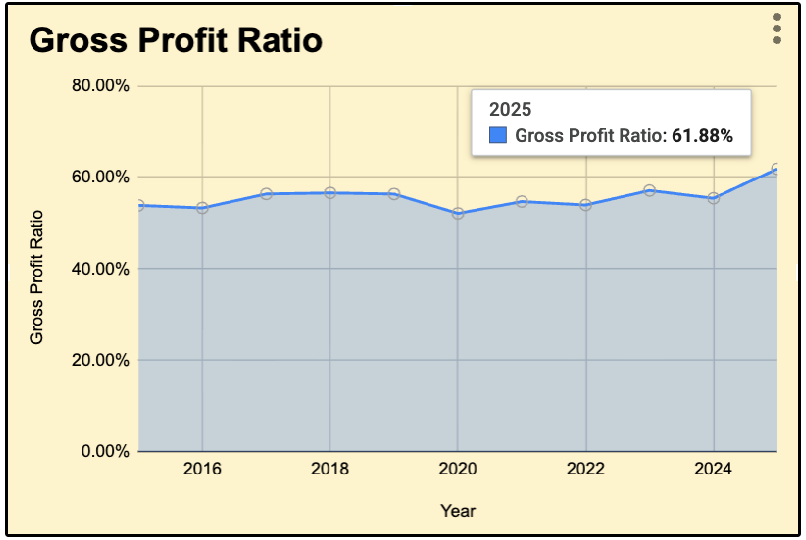

Their gross profit margins have gone from 53.91% to 61.88% in just one decade.

And importantly, much of the business is not directly dependent on whether the stock market goes up or down.

In many cases, volatility itself can actually increase trading volumes across futures, commodities, energy, and fixed income markets.

That creates a very different dynamic than traditional asset managers or investment banks whose revenues are often more tied to rising markets.

And like I mentioned above, the data services portion of the business is becoming even more attractive because of its recurring subscription-style revenue model and high switching costs.

Companies with highly predictable cash flows almost always trade at a premium, assuming they are growing those cash flows at a healthy rate.

The growing, predictable cash flows make ICE a great dividend grower.

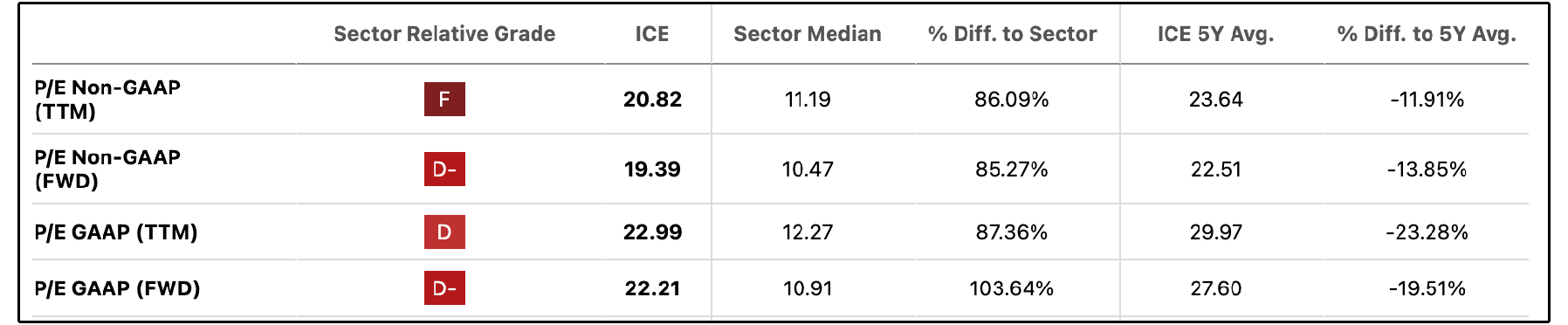

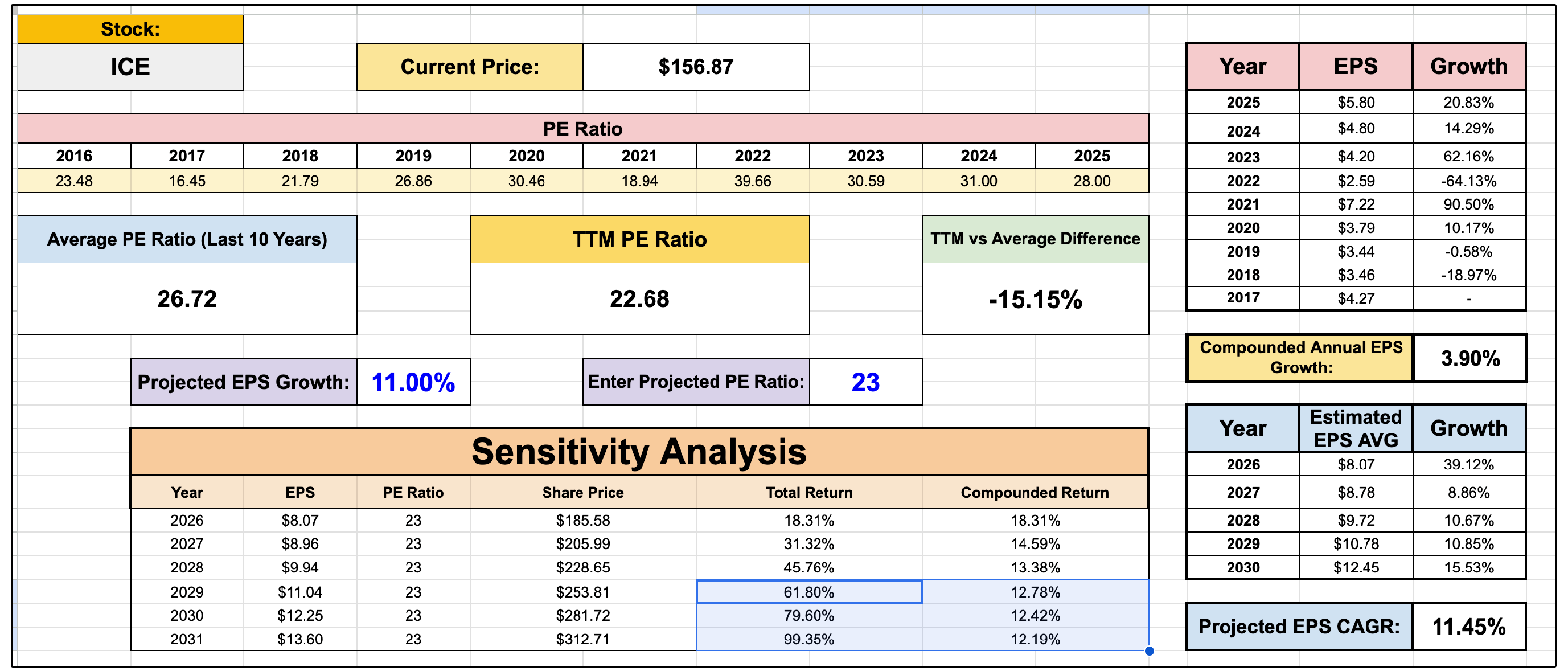

From a valuation perspective, ICE is trading well below its historical valuation multiples.

If we look at them from a sensitivity analysis perspective, even if we assume:

The P/E multiple does not revert back to its historic average

EPS growth comes in slightly below analyst estimates

We can still see compounded growth rates of above 12% by 2029, not including dividends.

This of course provides returns well above historic market averages.

Now, let’s dive into the full list of dividend stocks with the most upside according to Wall Street.