🧾 List of Most Upside Dividend Stocks

Wall Street Price Targets Revealed 🎯

Every month, I compile data on the dividend stocks with the most upside based on Wall Street analysts price targets.

Members will get access to the full list every month, as well as all other Dividendology features.

This month, only 36 stocks made the list.

Let’s dive in.

🚨 Something Big is Coming…

I have a confession.

I’m obsessed with increasing the value that Dividendology provides.

That’s why I’ve been working on something big recently.

We recently added an 11%+ yielding ETF to our High Yield Portfolio that actually grows its dividend payments over time-

And our position is already up around 9%!

Why did I feel so confident in adding a fund with such a high yield?

Because I’ve spoken directly with the fund manager 4 times in the last 6 months to get in depth insights on what to expect from the fund.

And in my recent call, he even let me know I should expect another dividend increase from the fund this year!

Why do I bring this up?

Because speaking with the fund manager gave me an edge-

And I want to bring that edge to you.

That’s why I’m creating the ETF database.

I’ve been conducting interviews with fund managers in search of the best dividend growth and high yield opportunities, and will be releasing all of them into the ETF database, while also adding all future interviews there as well.

This will be an incredible resource for investors looking for deeper insights into income oriented funds.

And on top of this, anytime I’m conducting an interview with a fund manager, members of Dividendology will get to submit their own questions to me to ask the fund manager.

Along with this, we will be making multiple additions to the Dividend Growth Portfolio next week!

That’s why I’ve officially declared next week ‘Dividend Week’.

There’s more to share, but I’ll leave it at that for now.

Now let’s dive into our most upside dividend stocks.

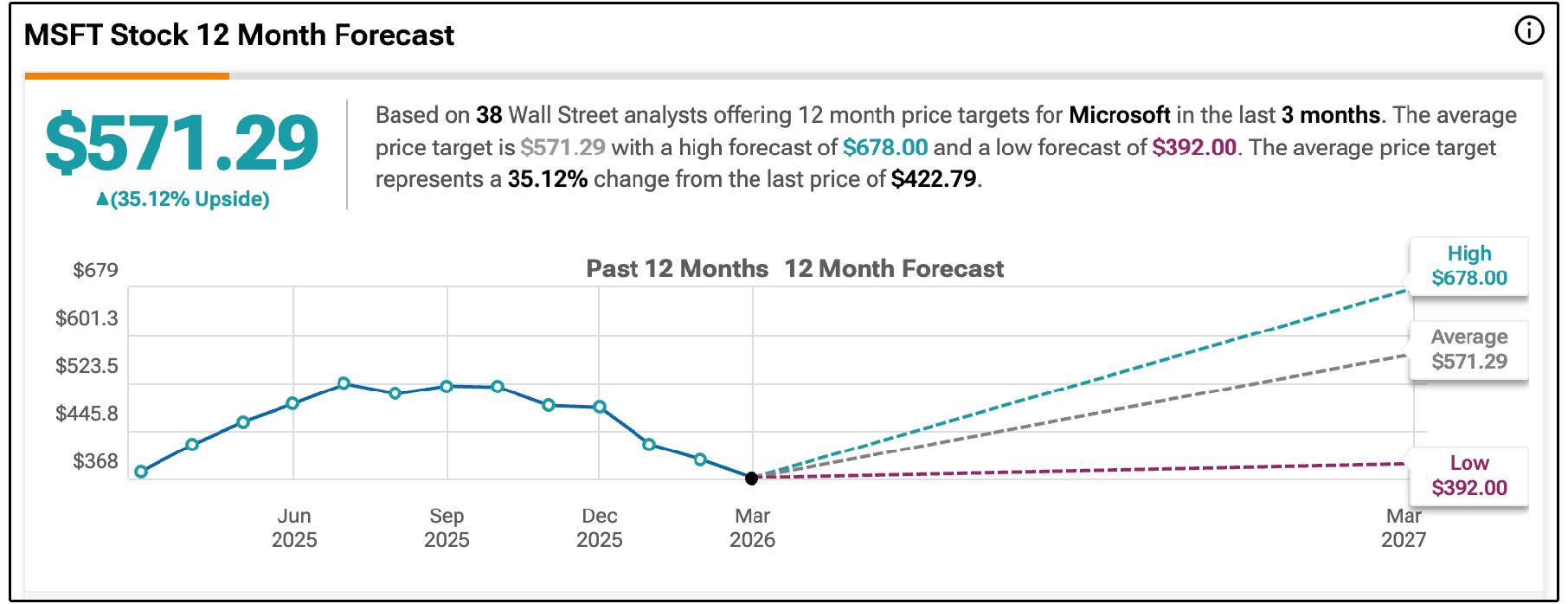

1. 💻 Microsoft (MSFT)

Wall St. Price Target: $571 | Upside: 33.24%

The market saw a pull back to start 2026, with the majority of the drop coming from the tech sector.

But the S&P 500 is now sitting comfortably at new all time highs, up 3.9% year to date.

Many would see this and assume that they ‘missed the dip buying opportunity’-

But that couldn’t be further from the truth.

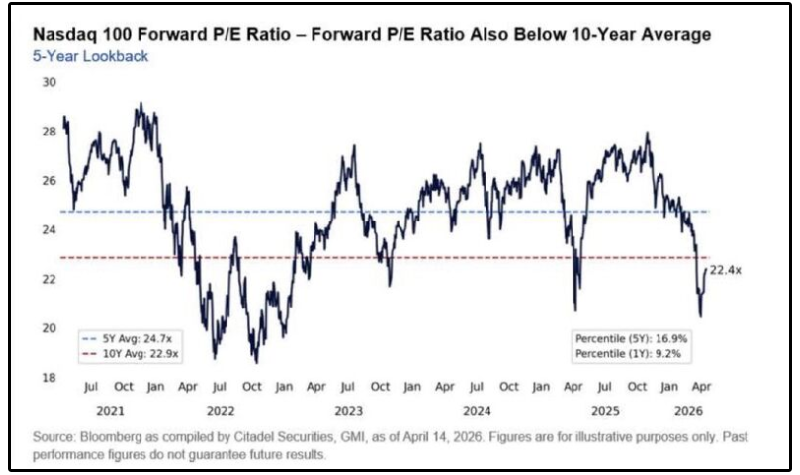

Only 2.4% of S&P 500 stocks are currently at a 52-week high, and perhaps even more interesting, the Nasdaq 100 Forward P/E is now ~22.4x, below its 10-year average (22.9x) and well under the 5-year average (24.7x).

Trailing valuation multiples are higher, but so are earnings growth estimates.

In other words, there are likely opportunities in the tech sector.

According to Wall Street analysts, one of those opportunities is Microsoft.

Microsoft generates revenue in three ways:

Software subscriptions (Microsoft 365)

Cloud computing infrastructure (Azure)

Enterprise software licenses spanning Dynamics, LinkedIn, GitHub, and Windows

The result is a recurring-revenue engine, with over 450 million commercial seats on Microsoft 365, multi-year enterprise contracts, and consumption-based Azure billing that scales with customer usage.

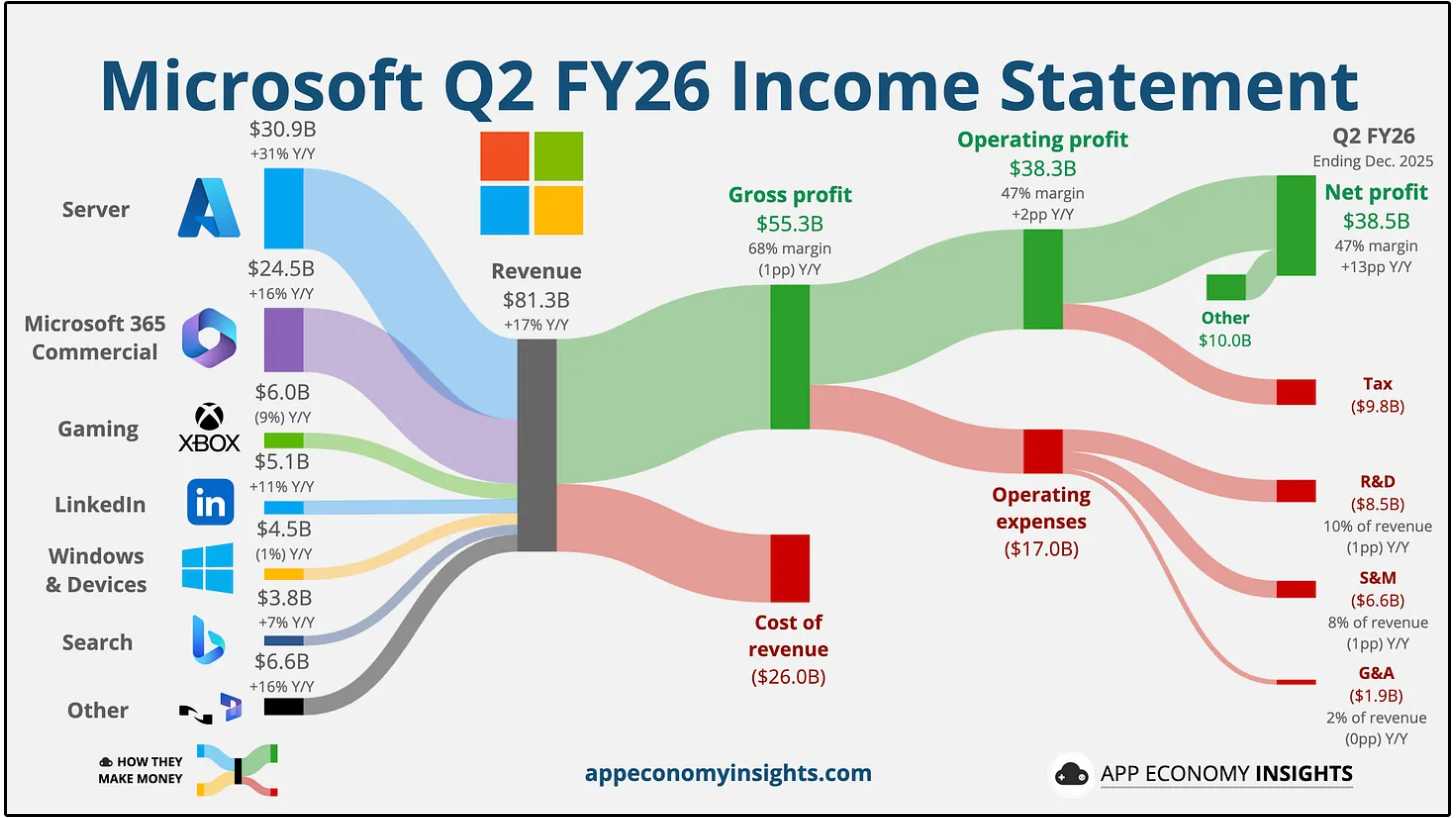

In Q2 FY2026 (ended December 2025), Microsoft reported $81.3 billion in revenue, up 17% year-over-year.

The AI monetization opportunity is real and accelerating.

Microsoft 365 Copilot now has 15 million paid seats, up over 160% year-over-year, though that still represents only about 3% of the 450 million seat installed base, meaning the monetization runway is enormous.

GitHub Copilot hit 4.7 million paid subscribers, up 75%.

Operating margin expanded to 47%, and the company returned $12.7 billion to shareholders through dividends and buybacks in the quarter alone.

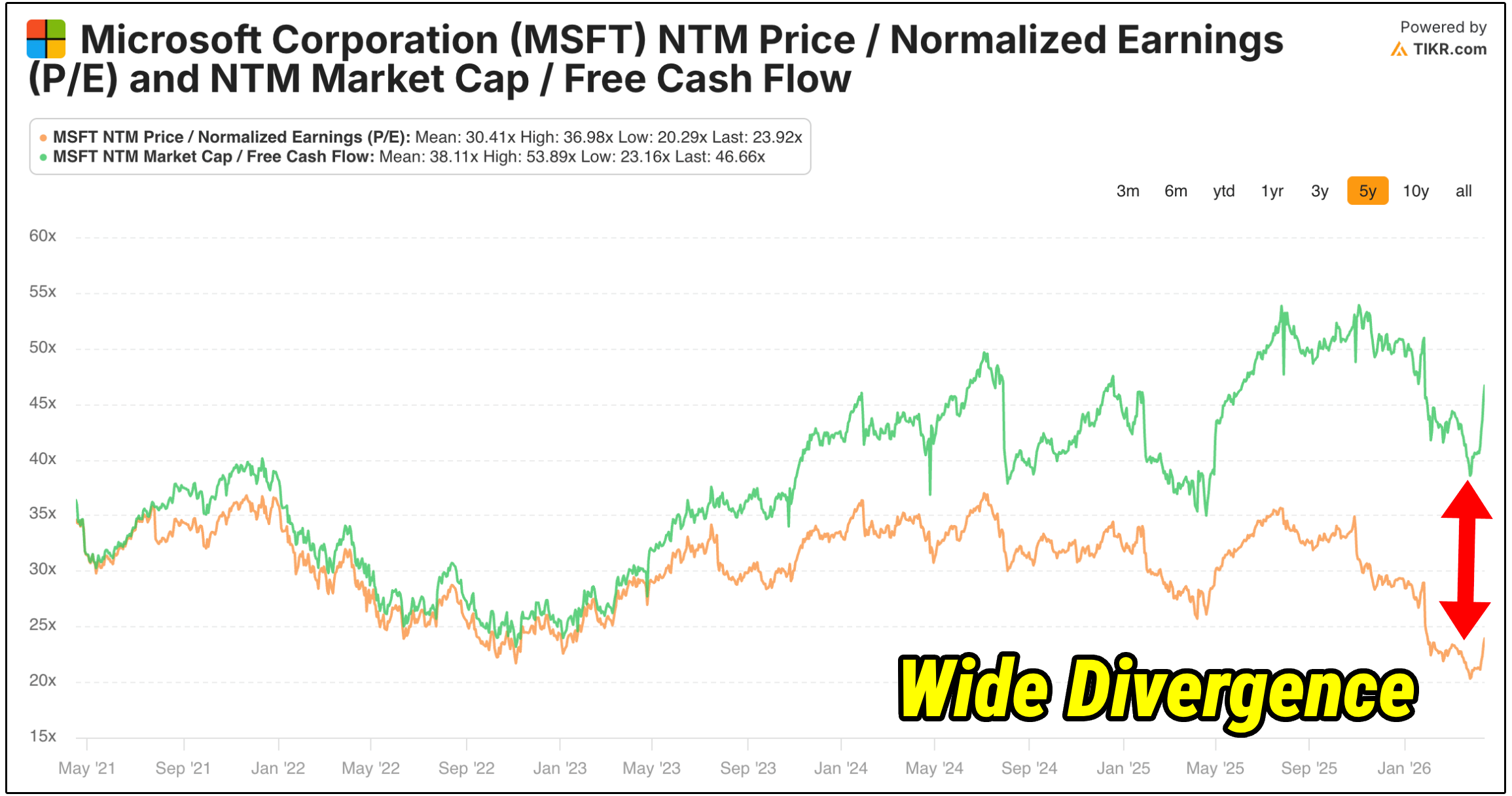

From a valuation standpoint, something incredibly interesting has happened.

We’ve seen a wide divergence in the price to earnings valuation multiple and the price to cash flow multiple valuation.

Why would this happen?

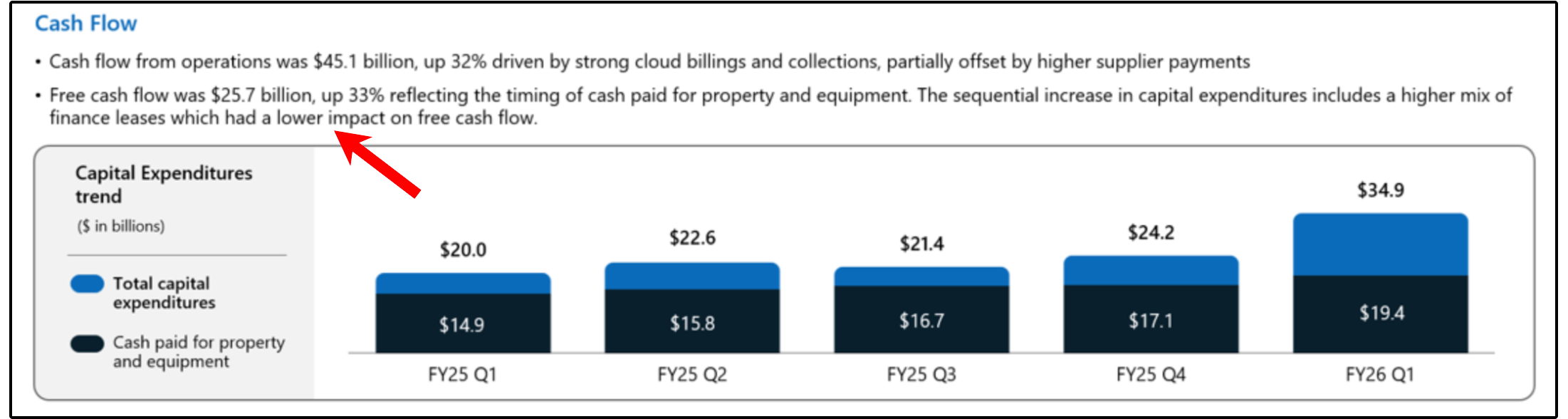

That elevated valuation is largely a function of temporarily depressed free cash flow, driven by unusually high capital expenditures tied to AI infrastructure build-out.

In other words, Microsoft does not look expensive from a cash flow perspective because the business is weakening, it looks expensive because the company is investing far more aggressively than normal.

Not all capex is created equal.

In general, there are two types of capital expenditures:

Maintenance capex is spending required simply to keep the business running at its current level. It preserves existing revenue but does not meaningfully increase future earnings power.

Growth capex, on the other hand, is discretionary investment aimed at expanding capacity, unlocking new revenue streams, and increasing long-term cash flow.

The vast majority of Microsoft’s elevated capex today falls firmly into the growth capex category.

Microsoft is building out global data center capacity, AI infrastructure, and long-lived cloud assets to meet demand that already exists.

How do we know that demand exists?

Microsoft now has one of the strongest forward revenue backlogs in all of big tech.

Commercial remaining performance obligations (RPOs, which represent signed customer contracts that have not yet been recognized as revenue) have surged to $392B (+51% YoY), nearly doubling in just two years, with a weighted average duration of ~2 years.

A large portion of their RPOs are directly tied to OpenAi which doesn’t create a customer concentration risk, but sentiment around MSFT finally seems to be shifting in a bullish direction again.

22 of 24 analysts rate MSFT a Strong Buy with an average price target of $571, implying over 35% upside from current levels.

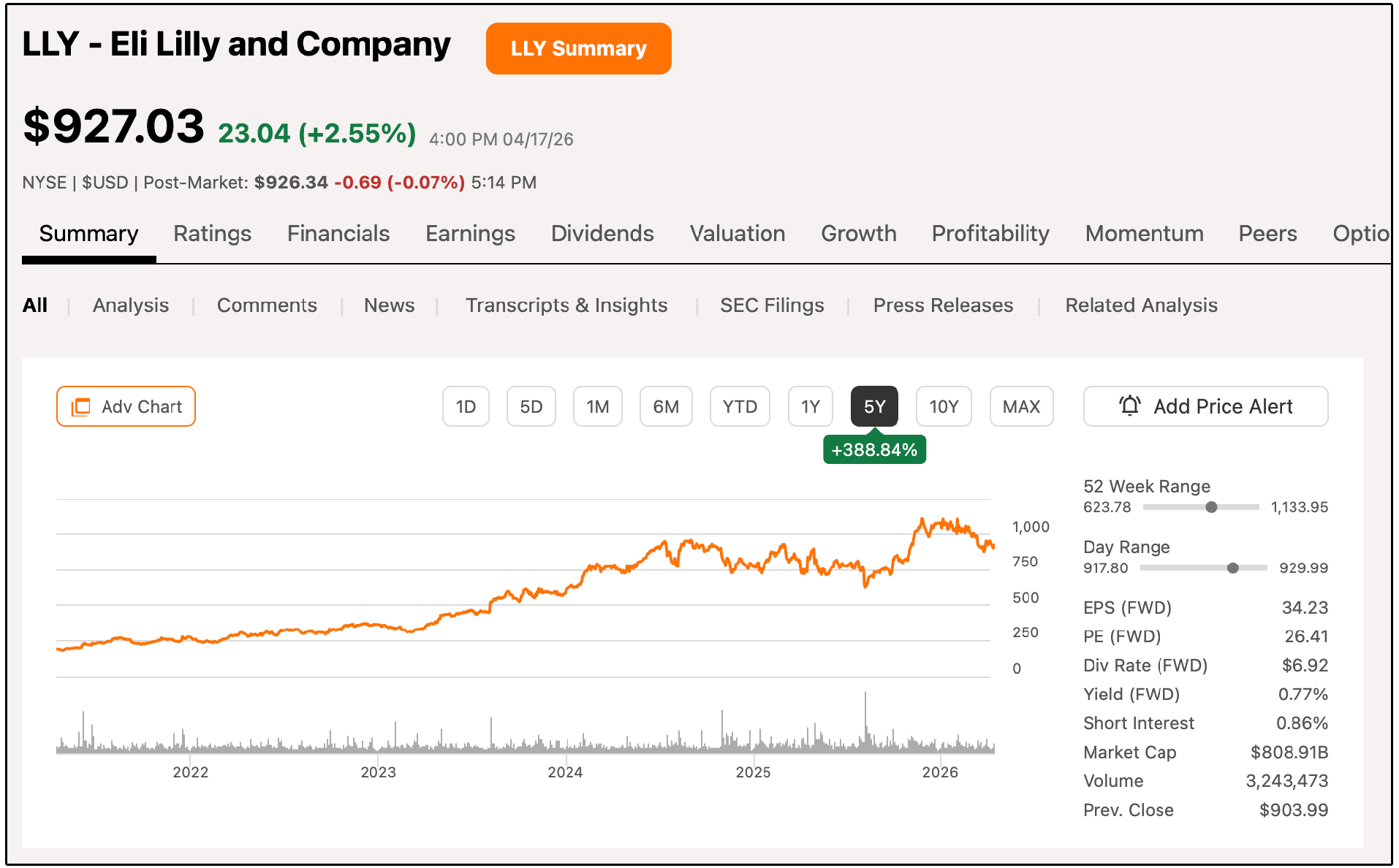

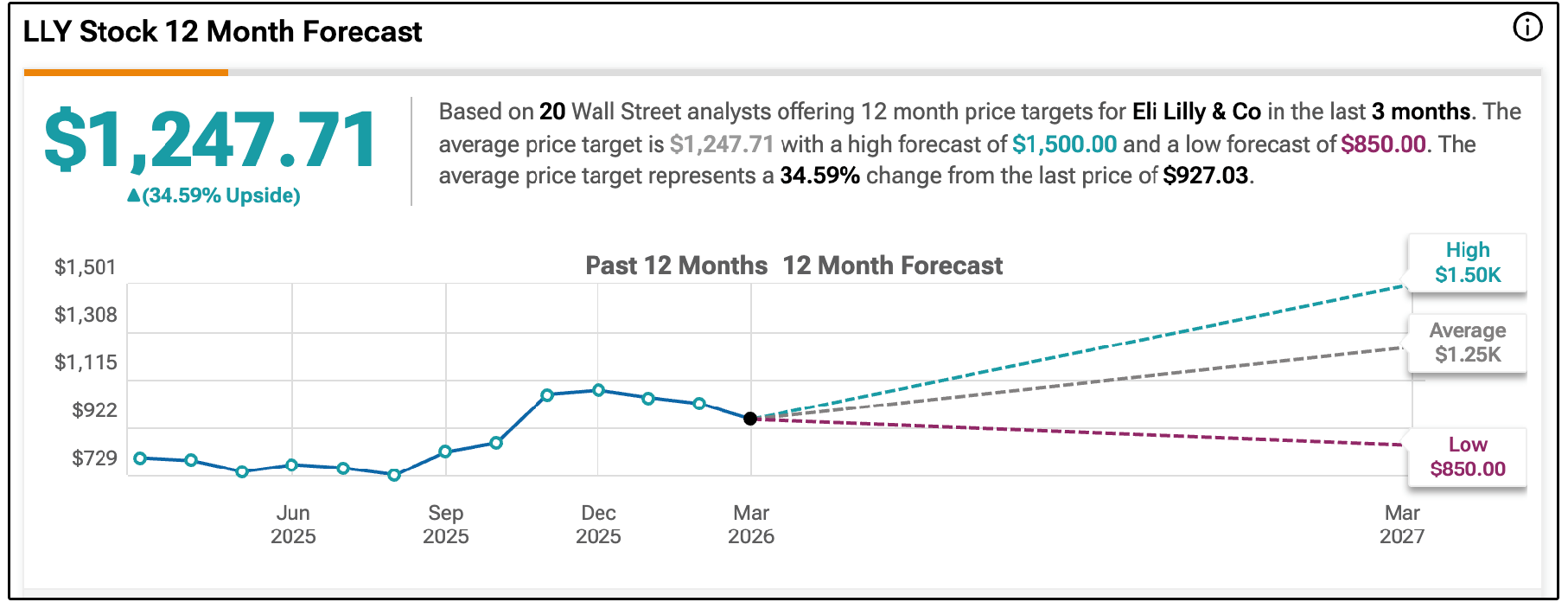

2. 💊 Eli Lilly (LLY)

Wall St. Price Target: $1,248 | Upside: 35.01%

Eli Lilly is a global pharmaceutical company that discovers, develops, and commercializes branded prescription drugs.

Founded in 1876, the company has operated for nearly 150 years, but its current growth trajectory is unlike anything in its history.

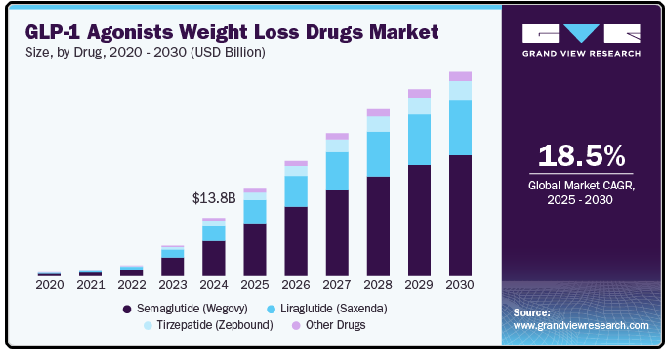

Lilly’s GLP-1 franchise, Mounjaro for type 2 diabetes and Zepbound for obesity, generated a combined $36.5 billion in FY2025 revenue, representing 56% of total company sales.

These drugs work by mimicking a gut hormone that suppresses appetite and regulates blood sugar, producing dramatic weight loss of 15-25% of body weight in clinical trials.

As you probably know, the addressable market is massive:

Roughly 1 billion people globally are classified as obese, and U.S. penetration among eligible adults remains in the mid-single digits.

In Q4 2025 (reported February 2026), Lilly posted $19.3 billion in revenue, up 43% year-over-year, beating estimates by $1.35 billion.

Full-year FY2025 revenue hit $65.2 billion (+45%), with EPS nearly doubling, with gross margins sitting very high at 83%.

And recently, the pipeline has continued to strengthen.

On April 1, 2026, the FDA approved Foundayo (orforglipron), an oral GLP-1 pill that can be taken any time of day without food or water restrictions.

That’s a meaningful convenience advantage over Novo Nordisk’s oral Wegovy, which requires 30 minutes of fasting.

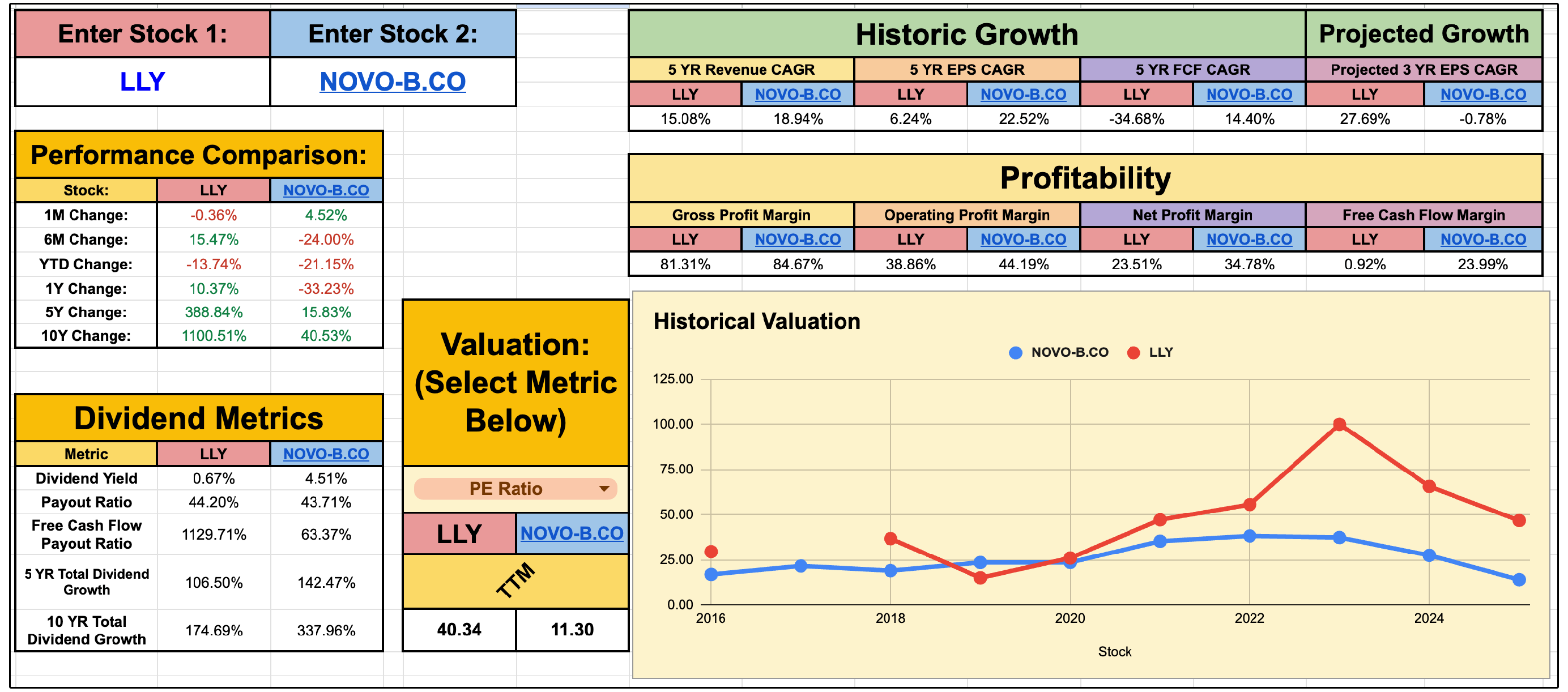

The outlook between LLY and NVO has dramatically shifted towards LLY, which is evident when looking at EPS growth projections:

NVO Projected 3 YR EPS CAGR: -0.78%

LLY Projected 3 YR EPS CAGR: 27.69%

Behind that, Retatrutide, a triple agonist targeting GLP-1, GIP, and glucagon receptors, demonstrated 29% body weight loss in Phase III trials and has the potential to become the next blockbuster.

Lilly now holds over 60% of the U.S. incretin market and roughly 70% of branded obesity prescriptions.

The dividend yields only 0.67% at current prices, but that’s because the stock has appreciated so dramatically, not because the dividend is small.

Lilly pays $6.92 per share annually, has increased the dividend for 11 consecutive years, and the 5-year dividend CAGR almost 13%.

With 14 of 16 analysts rating LLY a Strong Buy and an average target of $1,204, Wall Street sees roughly 30% upside.

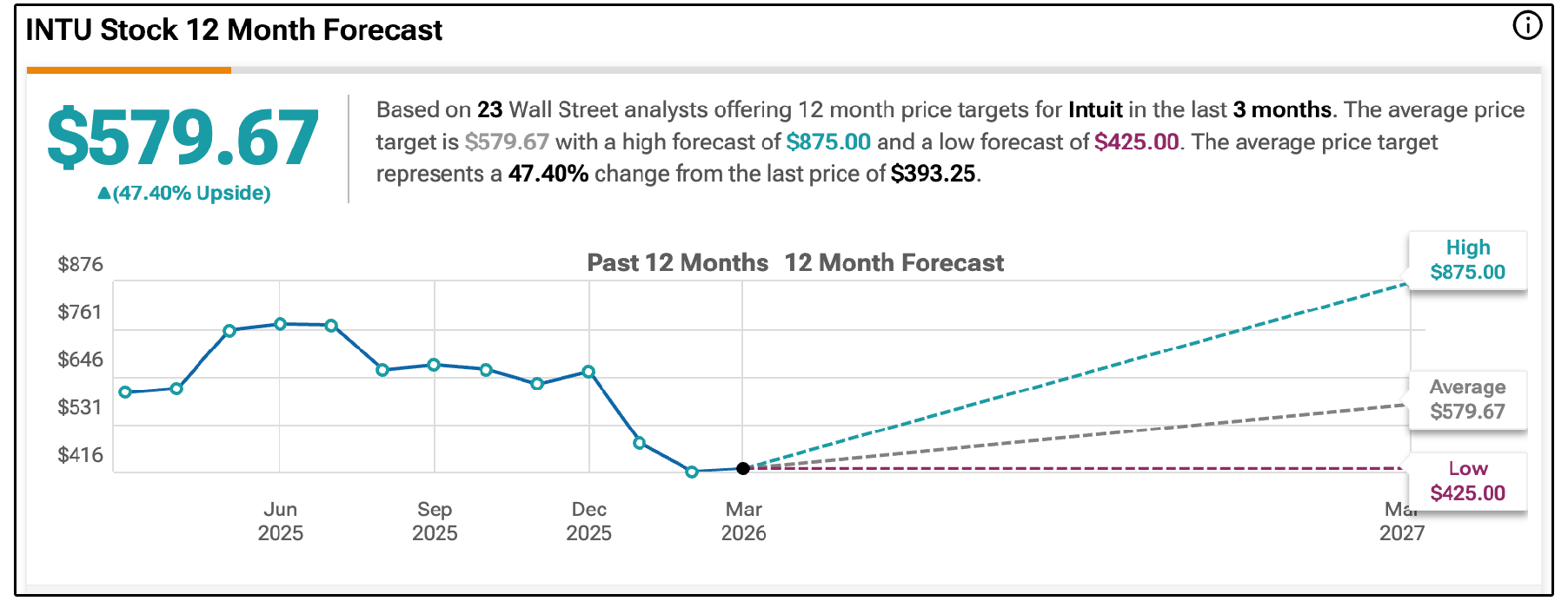

3. 🧮 Intuit (INTU)

Wall St. Price Target: $580 | Upside: 47.81%

This is an interesting pick from Wall Street, but fears surrounding the way Intuit will be impacted by AI has continued to ramp up in recent months.

Intuit operates four major financial software platforms:

TurboTax

TurboTax is the dominant consumer tax preparation platform in the U.S.

QuickBooks

QuickBooks serves as the leading accounting solution for small businesses, processing approximately $174 billion in payment volumes annually.

Credit Karma

Credit Karma is a free financial health platform with over 100 million members that generates revenue through referral commissions.

Mailchimp

Mailchimp provides email marketing and CRM tools for small businesses.

If you’ve filed your own taxes or managed payroll for a small business, you’ve likely used one of their products.

The business model is predominantly subscription-based, which has historically led to incredible predictable and stable revenue and earnings growth, with exceptional profit margins.

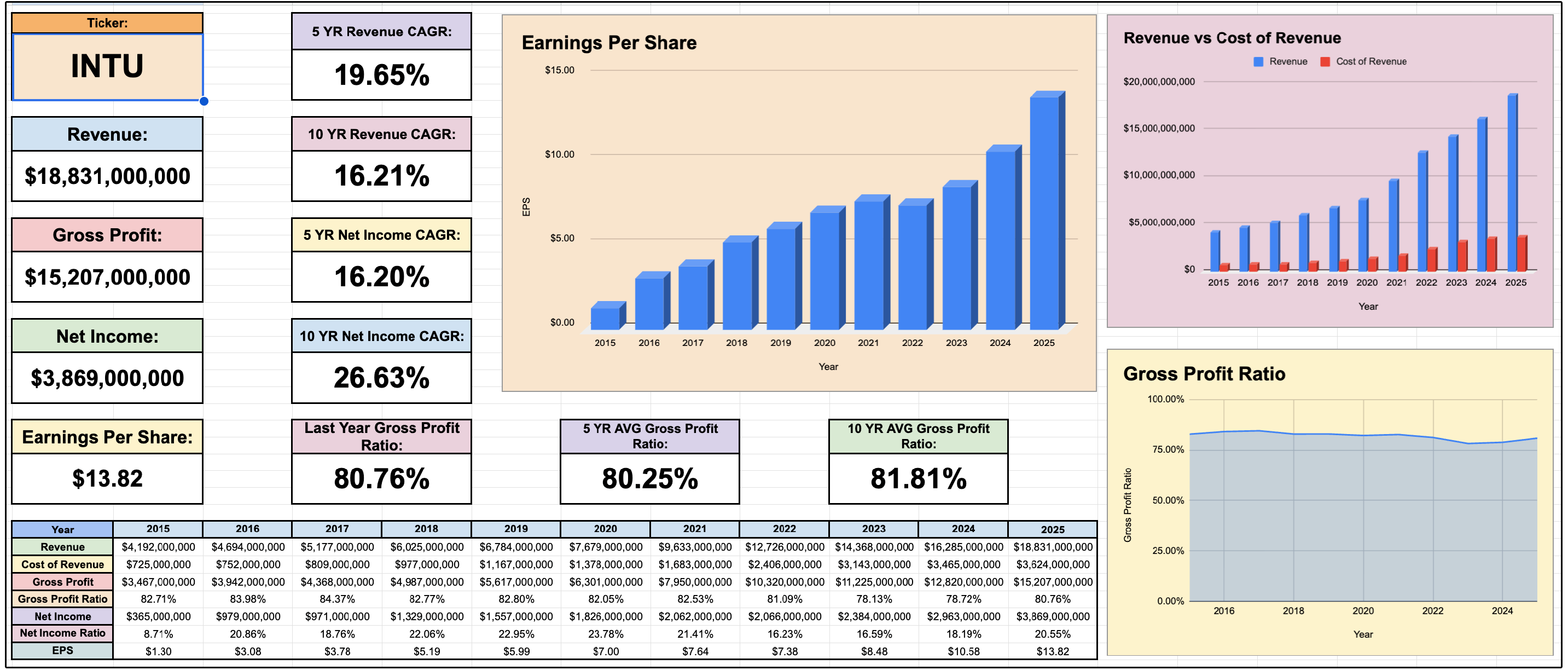

In Q2 FY2026 (ended January 2026), Intuit reported $4.65 billion in revenue, up 17% year-over-year.

Non-GAAP EPS came in at $4.15, beating consensus by $0.49. Credit Karma grew 23%, and the online QuickBooks ecosystem grew 21%.

For the full year, the company guided $21.0-21.2 billion in revenue (+12-13%) and non-GAAP EPS of $22.98-$23.18.

So with strong historic fundamentals and solid guidance-

Why is the stock down 34% over the past year?

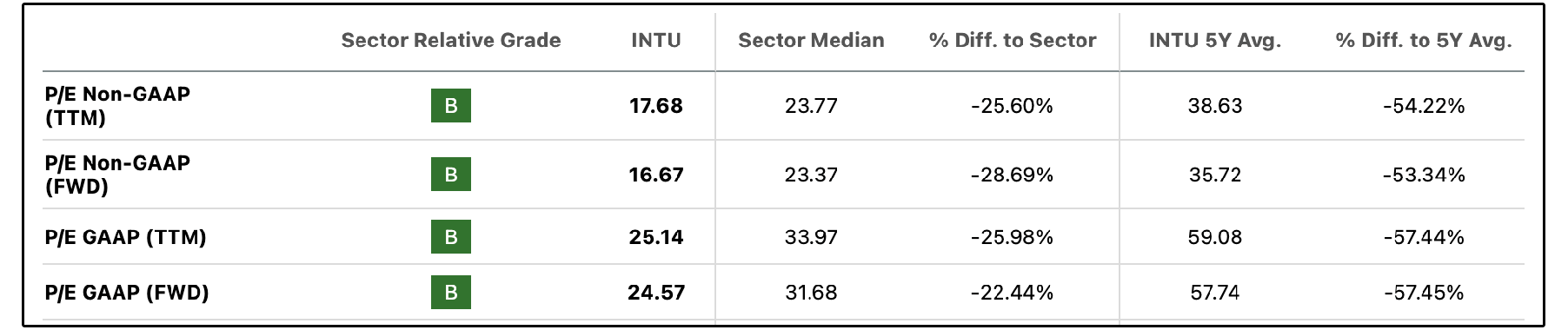

Two words: multiple compression.

The stock traded above 50x earnings at its peak and has been cut roughly in half to around 17x non-GAAP forward earnings.

A broad selloff in SaaS stocks accelerated in early 2026 after Anthropic’s Claude model announcements raised concerns that AI agents could replace seat-based software entirely.

Intuit was hit especially hard because the market fears that LLMs could eventually handle tax prep and bookkeeping without dedicated software-

And I must say, I’ve seen some incredible use cases personally when it comes to AI doing tax prep.

However, the counterargument is certainly worth considering.

Intuit has been investing in AI since 2020, which was well before the current hype cycle.

The company has partnerships with both OpenAI and Anthropic, its Intuit Assist platform automates 93% of tax forms, and TurboTax Live (which pairs AI with human CPAs) grew 47% last year.

As CEO Sasan Goodarzi has stated-

“Customers don’t want to do anything that has to do with their money, they want us to do it for them.”

At a forward non-GAAP P/E of roughly 17x, Intuit is trading at its cheapest valuation in over a decade.

The question is obviously whether the market’s AI disruption fears are justified.

Right now, Wall Street doesn’t seem to think so.

29 of 35 analysts rate it a ‘Buy’ with a median price target of $579, implying nearly 47% upside.

Now, let’s dive into the full list of dividend stocks with the most upside according to Wall Street.