🏆 List of Undervalued Dividend Stocks (March '26)

These Stocks are Undervalued! 🔥

At the beginning of each month, I send out a spreadsheet that lists out the dividend stocks that I believe to be undervalued.

This is the end result of 100’s of hours of research every month.

It’s time to dive in.

1. 🏢 AH REALTY TRUST (AHRT)

*NOTE: This REIT was previously under the name Armada Hoffler Properties (AHH)

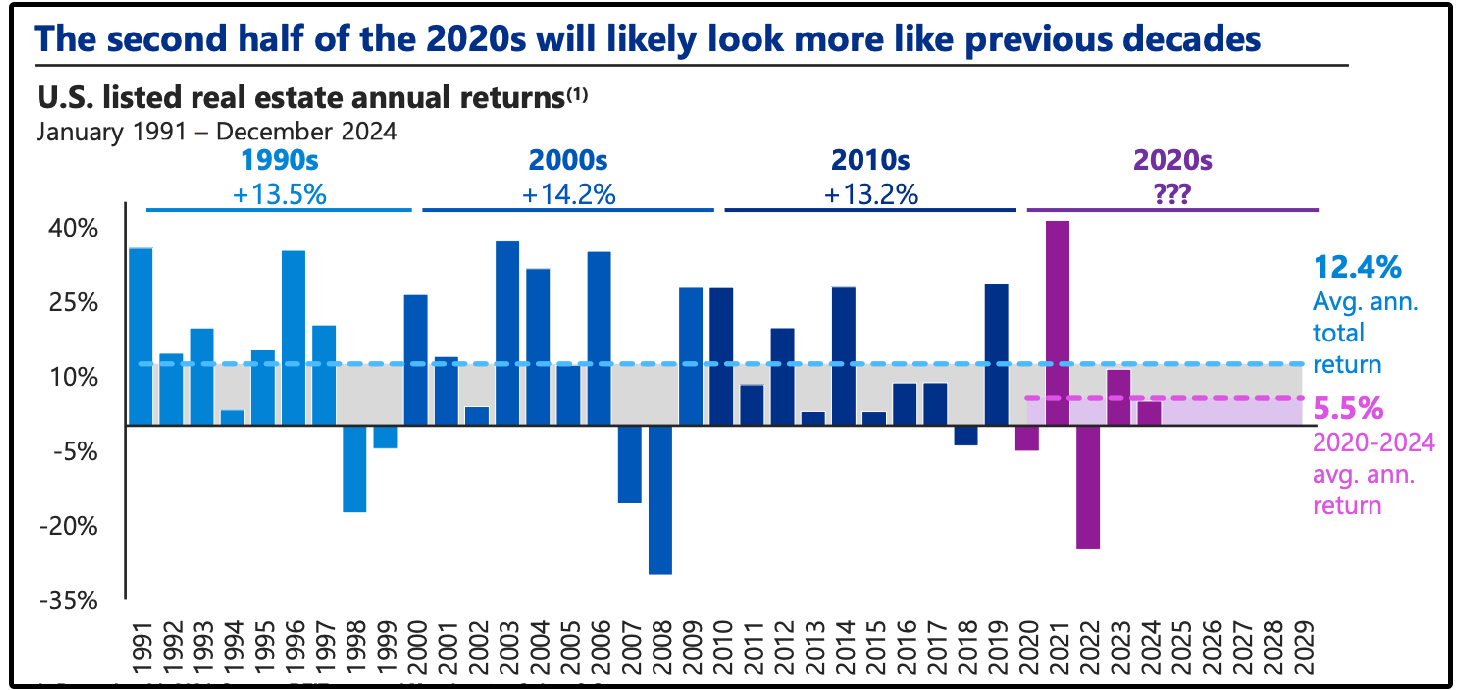

I highlighted the REIT sector as a major opportunity heading into 2026, and so far that thesis has played out very well.

REITs had underperformed over the last few years, but are currently outperforming the S&P 500 by over 5% in 2026.

AH Realty Trust (formerly Armada Hoffler Properties) has become one of the more controversial names in the REIT sector.

Today, the REIT is:

Yielding around 9% and

Trading at roughly a 50% discount to estimated net asset value

Seeing heavy insider buying/ownership

Insiders currently own over 10% of the business.

Much of that discount stems from the major strategic transformation currently underway.

Historically, AHRT (formerly AHH) had a development-first model.

For decades, Armada Hoffler leaned heavily on its identity as a developer, earning a meaningful portion of income from construction contracts, development fees, and one-off transactions.

That model worked well in boom times but created volatility and left the company more exposed when credit tightened and rates spiked.

This ultimately led to some major issues.

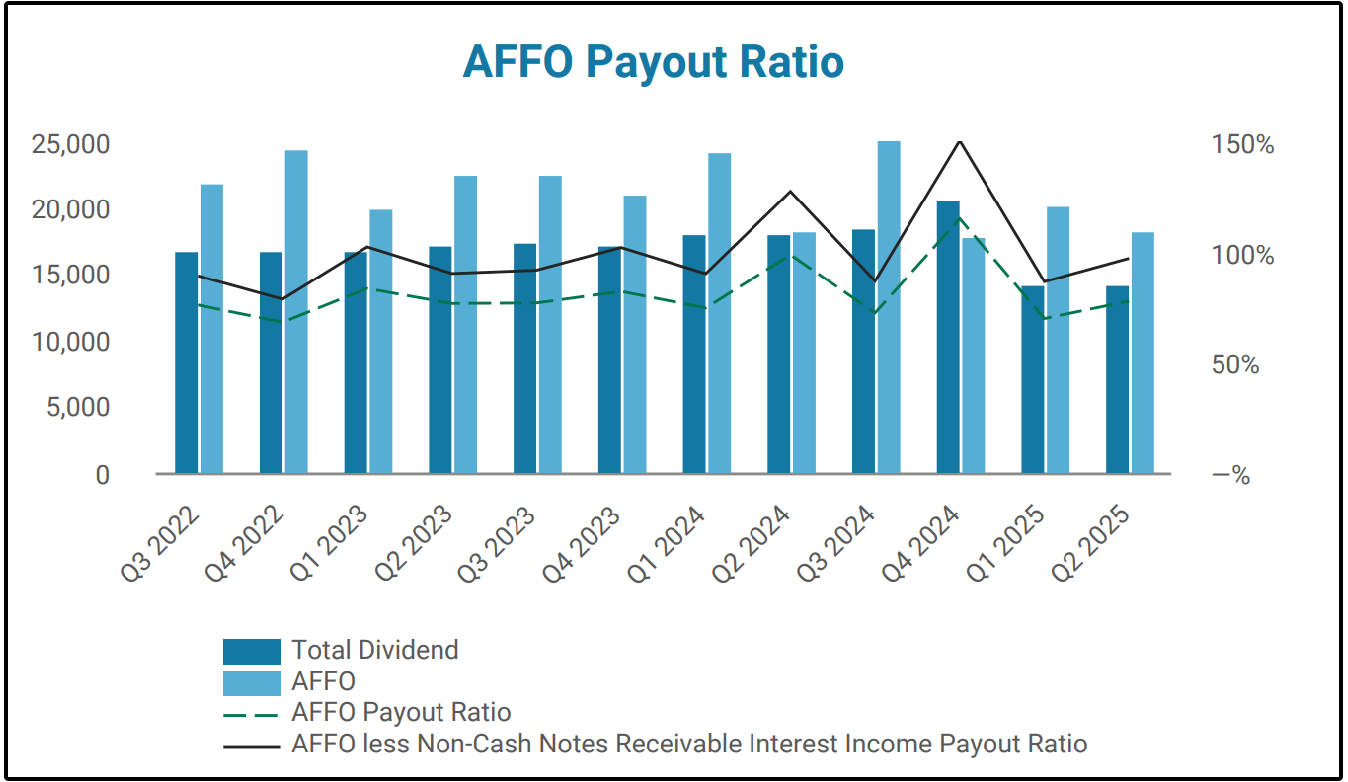

Most notably, it led to AFFO not covering their dividend payments, which led to a dividend cut.

Under CEO Shawn Tibbetts, the company is fundamentally reshaping the business.

Armada Hoffler recently rebranded to AH Realty Trust (AHRT) and announced plans to simplify its structure by selling its multifamily portfolio, exiting its construction and lending operations, and using the proceeds to reduce leverage while focusing the company around its core retail and mixed-use office properties.

This shift has created near-term uncertainty, pushing the REIT to a 52-week low.

However, the strategy directly addresses two of the biggest issues that historically caused Armada Hoffler to trade at such a large valuation discount.

The first issue was leverage.

The company carried more debt than many REIT peers, which increased investor concerns during the recent interest rate cycle.

By selling assets and using the proceeds to pay down debt, management is actively working to strengthen the balance sheet.

The second issue was complexity/unpredictability.

Unlike most REITs, Armada Hoffler generated a portion of its earnings through development, construction, and lending operations.

While these businesses could generate attractive returns in strong markets, they also created lumpy earnings and made the company harder for investors to value.

Most REIT investors prefer simple property platforms that generate stable rental income, leading to reliable dividend income.

By exiting these non-core businesses, AHRT is becoming a much cleaner and more focused real estate company.

Importantly, the underlying real estate portfolio remains strong. The company’s properties currently maintain occupancy levels of roughly 96%, demonstrating that its mixed-use office and service-oriented retail assets continue to perform well even in a challenging environment for commercial real estate.

There are still real risks.

The management team recently stated:

“While 2026 represents a transition year for the company, I want to underscore that throughout this period, we continue to maintain full dividend coverage from the cash flows generated by our operating properties, while also meaningfully reducing debt.”

The AFFO payout ratio is projected to be close to 86% in 2026.

If management successfully simplifies the business and reduces leverage, the current valuation could eventually prove far too pessimistic.

For investors willing to accept some short-term volatility, AHRT represents one of the more interesting deep value opportunities in the REIT market today.

2. 🌿 Innovative Industrial Properties (IIPR.PR.A)

Innovative Industrial Properties (IIPR) is a specialized REIT that owns cultivation and processing facilities leased to licensed cannabis operators across the United States.

The REIT is currently yielding close to 14%!

However, I’m not interested in the REIT itself.

I’m interested in their preferred shares.

The preferred shares currently trade at roughly $22.50, giving them a yield of 10%.

The reason this is so interesting, is because IIPR has one of the most conservative balance sheets in the REIT sector.

That combination of a near double-digit yield and discounted price is unusual for a preferred security backed by a REIT with such a conservative balance sheet.

Interestingly, this opportunity exists despite improving fundamentals in the cannabis REIT sector.

Earlier this year, President Trump signed an executive order initiating the process to reschedule cannabis as a Schedule III drug, which would eliminate the punitive 280E tax rule that currently prevents cannabis operators from deducting normal business expenses.

If implemented, this change could dramatically improve the profitability and cash flow of cannabis companies, strengthening their ability to pay rent and improving the financial outlook for landlords like IIPR.

Keep in mind, the preferred shares are relatively thinly traded, and the company has issued additional preferred equity recently, which has likely pressured prices in the short term.

But when looking at the underlying credit profile supporting the preferred dividend, the numbers are striking, especially when you compare them to peers.

Innovative Industrial Properties operates with an extremely conservative balance sheet, carrying with a roughly 1.4x debt-to-EBITDA ratio, which is among the lowest leverage levels in the entire REIT sector.

More importantly, the preferred dividend is covered nearly 50x by AFFO, providing an enormous margin of safety for income investors.

In other words, if IIPR’s rental income were cut in half, the preferred dividend would still remain well covered by cash flows.

While the cannabis sector will likely remain volatile, the risk-to-reward profile for the preferred shares looks unusually compelling.

Investors today are collecting nearly 10% annual income from a cumulative preferred security backed by one of the lowest-levered REIT balance sheets in the market.

These are the type of opportunities that get incredibly little coverage, and one of the reasons the high yield space is so interesting for those who do deep research.

3. ⚡ Broadcom (AVGO)

This wouldn’t be a complete list without covering at least one dividend growth opportunity.

I’ve been bullish on AVGO for years, and it has continued to perform exceptionally.

The temptation of every investor is to look at a stock that has performed this well and simply assume the opportunity has passed.

But the reality is that share price alone tells us very little about how the valuation of the company has actually changed.

We must account for changes in the earnings power of the business.

Despite the fact the stock is up over 86% in the last year, the P/E valuation multiple has actually declined.

In other words, earnings grew even faster than the share price in 2025-

And earnings are projected to grow at simply amazing rates.

Not only that, but the visibility/predictability of those earnings have improved as well.

Broadcom CEO Hock Tan made this comment during the recent earnings call:

“Our visibility in 2027 has dramatically improved. Today, in fact, we have line of sight to achieve AI revenue from chips, just chips, in excess of $100 billion in 2027. We have also secured the supply chain required to achieve this.”

Valuation multiples are determined primarily by future earnings growth rate (which is already quite high for AVGO), but the predictability of those future earnings plays a major role as well, and this is where AVGO is seeing improvement.

If AVGO achieves the average analyst EPS estimate over the next few years AND even sees the trailing 12 month P/E multiple fall back significantly-

Forward looking returns still look incredibly attractive, with compounded returns through 2030 sitting at 17.35%.

Now, let’s review the full list for March.