🏆 List of Undervalued Dividend Stocks (April '26)

These Stocks are Undervalued! 🔥

At the beginning of each month, I send out a spreadsheet that lists out the dividend stocks that I believe to be undervalued.

This is the end result of 100’s of hours of research every month.

It’s time to dive in.

1. 💳 Mastercard (MA)

Mastercard operates with four primary business segments:

Transactions Processing (the largest segment)

Domestic Assessments

Cross Border Volume Fees

Value-Added Services & Solutions

At its core, Mastercard operates a global payments network connecting consumers, merchants, banks, and governments across more than 210 countries.

Every time a transaction is processed, Mastercard earns a small fee.

Importantly, it does not issue credit cards, lend money, or take on credit risk. Instead, it acts as the “toll road” of global commerce, collecting fees as money moves across its network.

This results in an incredibly capital-light and high-margin business model.

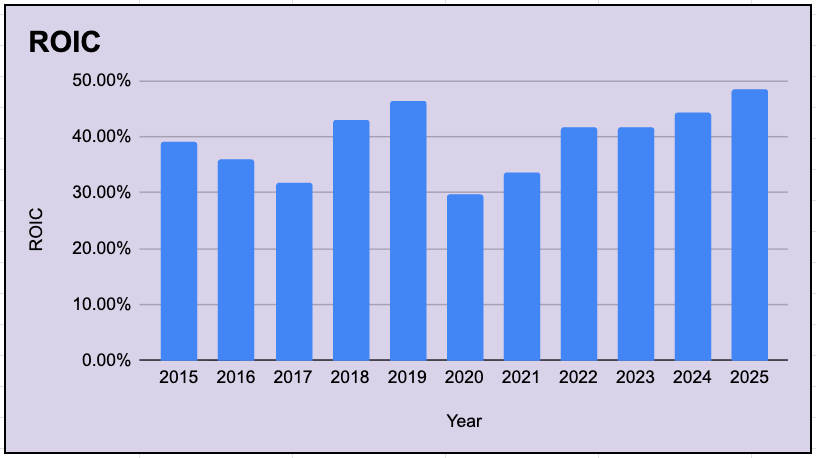

In 2025, Mastercard generated a gross profit margin of over 83% and a return on invested capital above 48%, highlighting just how efficient and scalable the business is

Mastercard’s capital light model has historically made it a very attractive compounder.

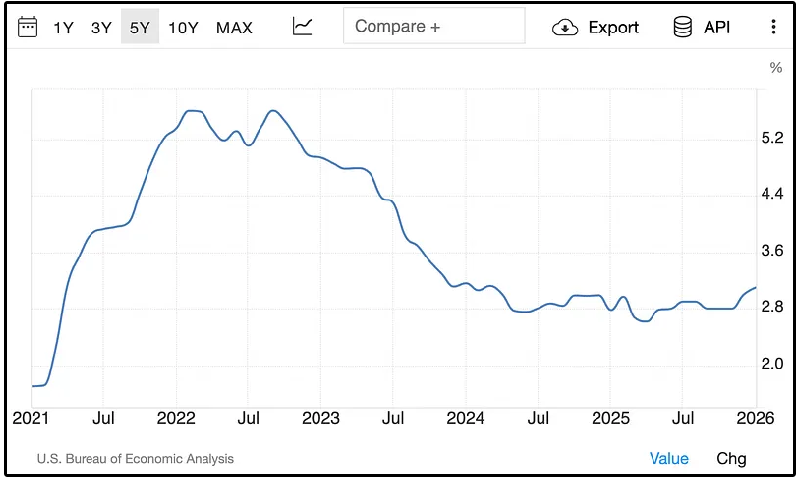

Keep in mind, we just saw the largest monthly inflation increase since 2022.

When oil spikes, it raises transportation, manufacturing, and food costs, which eventually flow through the entire economy.

Crude oil has surged ~46% in the past month alone.

According to Federal Reserve research-

A 10% increase in oil prices can lift headline CPI by roughly 0.4% over time when accounting for broader economic effects

Scale that to a move of this magnitude, and you’re looking at meaningful upward pressure on inflation.

How does this impact Mastercard?

Because its fees are based on a percentage of transaction value, higher prices across the economy directly translate into higher revenue, without requiring additional capital or customers.

Mastercard is the ultimate inflation hedge.

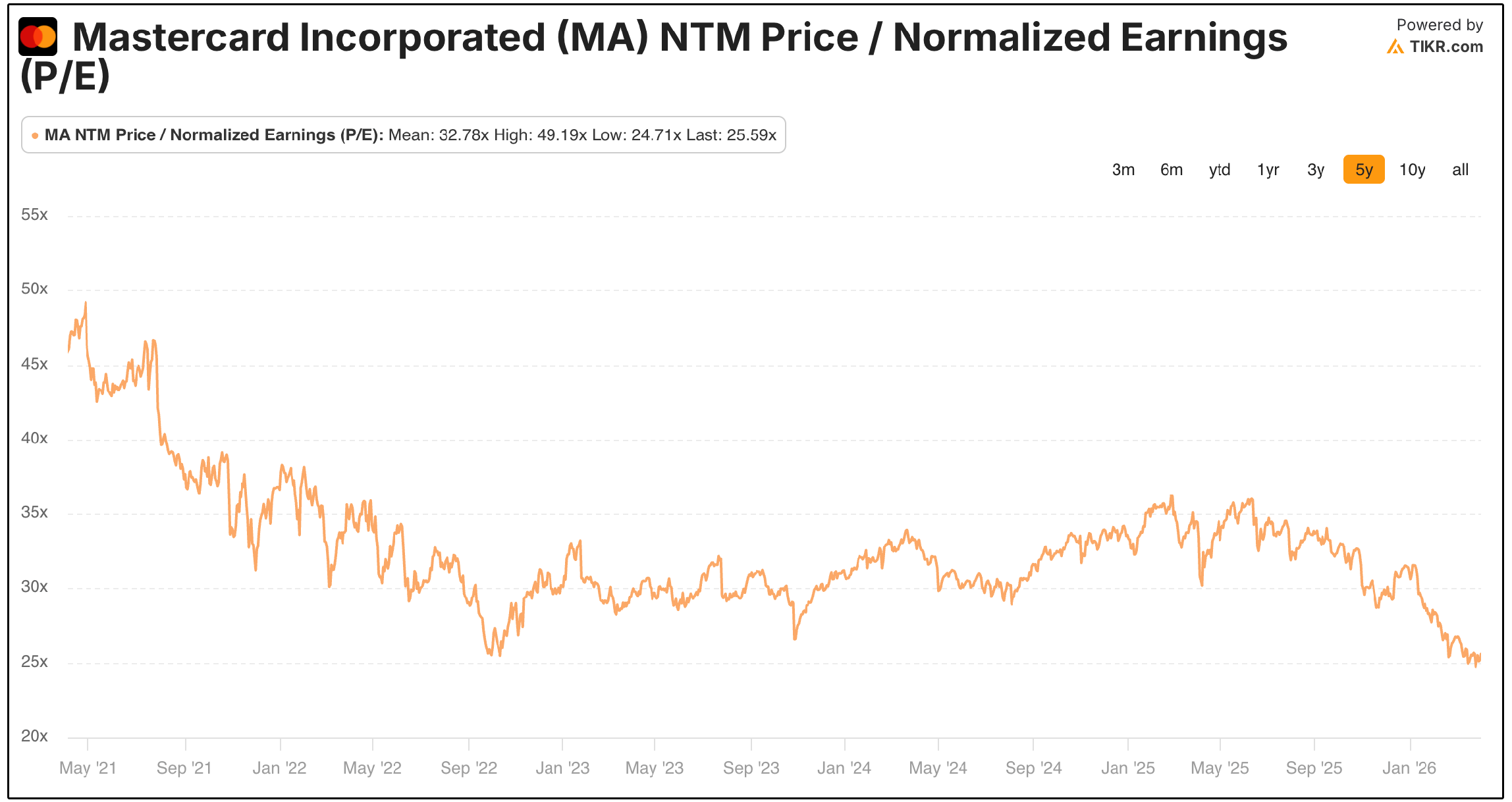

But what makes Mastercard most interesting right now is the valuation.

Mastercard is currently trading at their lowest forward P/E multiple in over 5 years.

Despite this, their projected 3-5 year EPS CAGR sits at 16.33%.

The growth story remains firmly intact.

Mastercard continues to benefit from the global shift toward digital payments, cross-border transactions, and e-commerce.

Cross-border volume, in particular, is a key earnings driver due to its higher margins. On top of this, the company’s Value-Added Services segment, focused on fraud prevention, data analytics, and cybersecurity, is growing rapidly and carries higher-margin, recurring revenue streams, further strengthening the business model.

Nothing about the business has deteriorated, yet the valuation has compressed, creating the most attractive entry point in years.

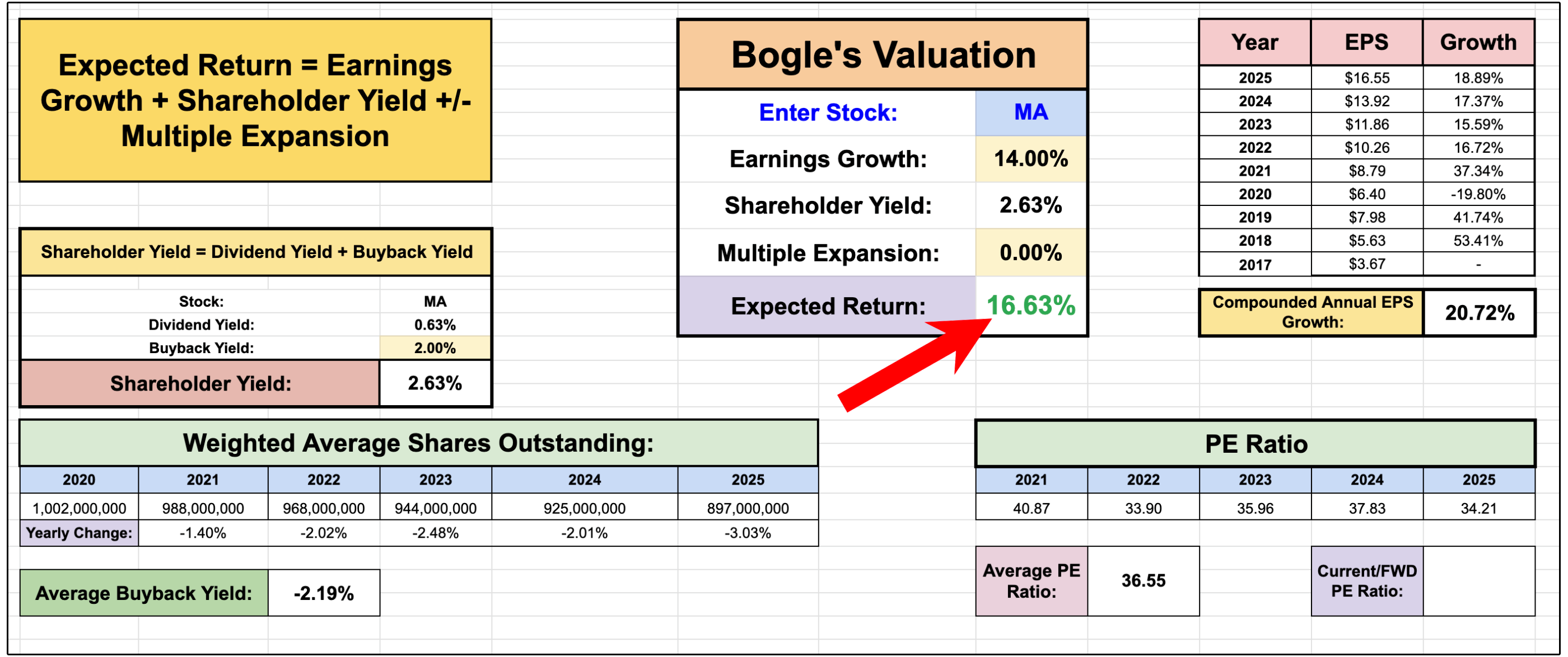

Using Bogle’s valuation, even if we assume Mastercard delivers EPS growth below expectations and continues to trade at their lowest valuation in the last 5 years, forward looking returns still look incredibly attractive.

2. 🛢️ The Williams Companies, Inc. (WMB)

WMB is one of the most critical energy infrastructure platforms in the United States, and it is currently set to benefit from three independently investable theses that are about to converge:

Transco pipeline is structurally irreplaceable, 95% fee-based, and benefits from inflation

$5.1B Power Innovation division is pre-contracted to Meta and hyperscalers on 10-year take-or-pay terms directly tied to the AI power buildout

U.S. LNG export capacity doubling by 2028 creates incremental unmodeled throughput revenue

Roughly 95% of Williams’ cash flows are fee-based and backed by long-term contracts, which makes the business highly predictable and insulated from commodity price swings.

So this is not a bet on gas prices, it’s a bet on volumes moving through an essential network…

And those volumes are set to rise.

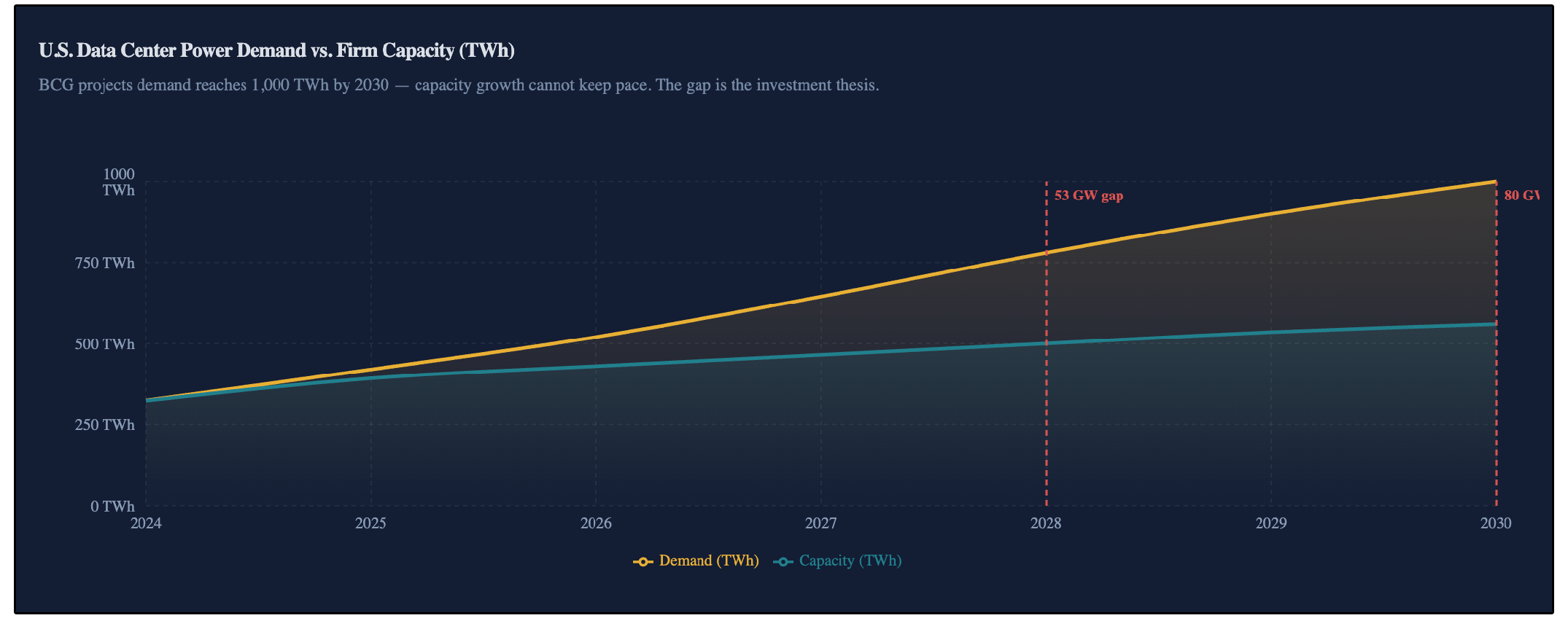

U.S. electricity demand is beginning to inflect higher for the first time in decades, driven largely by AI data centers and electrification.

Estimates now show power demand approaching 1,000 terawatt-hours by 2030, while current infrastructure is nowhere near sufficient to meet that demand.

That supply-demand imbalance needs to be solved, and natural gas is the most immediate bridge.

Williams is already leaning into this trend through its Power Innovation segment, a $5.1B platform tied directly to the buildout of power infrastructure.

Importantly, this isn’t speculative growth.

The company has already secured 10-year take-or-pay agreements with players like Meta Platforms, Inc., locking in long-duration, contracted cash flows tied to AI demand.

On top of that, (like mentioned above for Mastercard), Williams has built-in inflation protection.

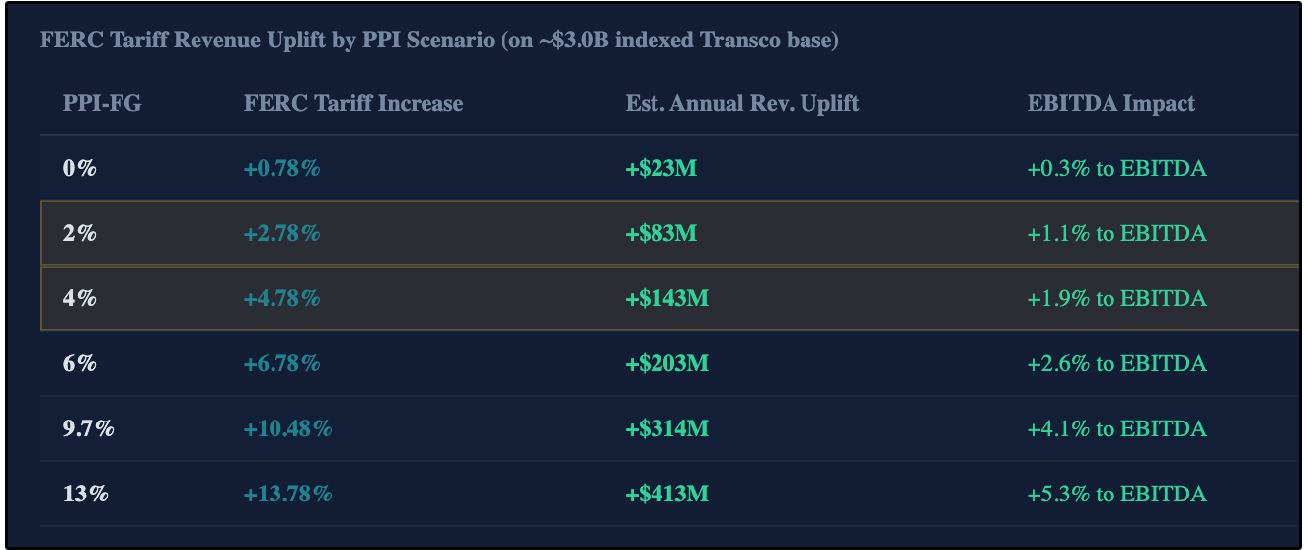

A large portion of its pipeline revenues are regulated by the Federal Energy Regulatory Commission and indexed to producer price inflation (PPI), meaning higher inflation directly increases the rates Williams is allowed to charge.

As shown below, even modest inflation has a measurable impact:

At just 2% inflation, EBITDA increases by ~1.1%

At 4% inflation, EBITDA rises nearly 2%

There’s also a third driver that the market is underappreciating: LNG (liquefied natural gas).

U.S. LNG export capacity is expected to double by 2028, which requires significantly more natural gas to flow through pipeline systems like Transco.

This creates incremental throughput demand for WMB.

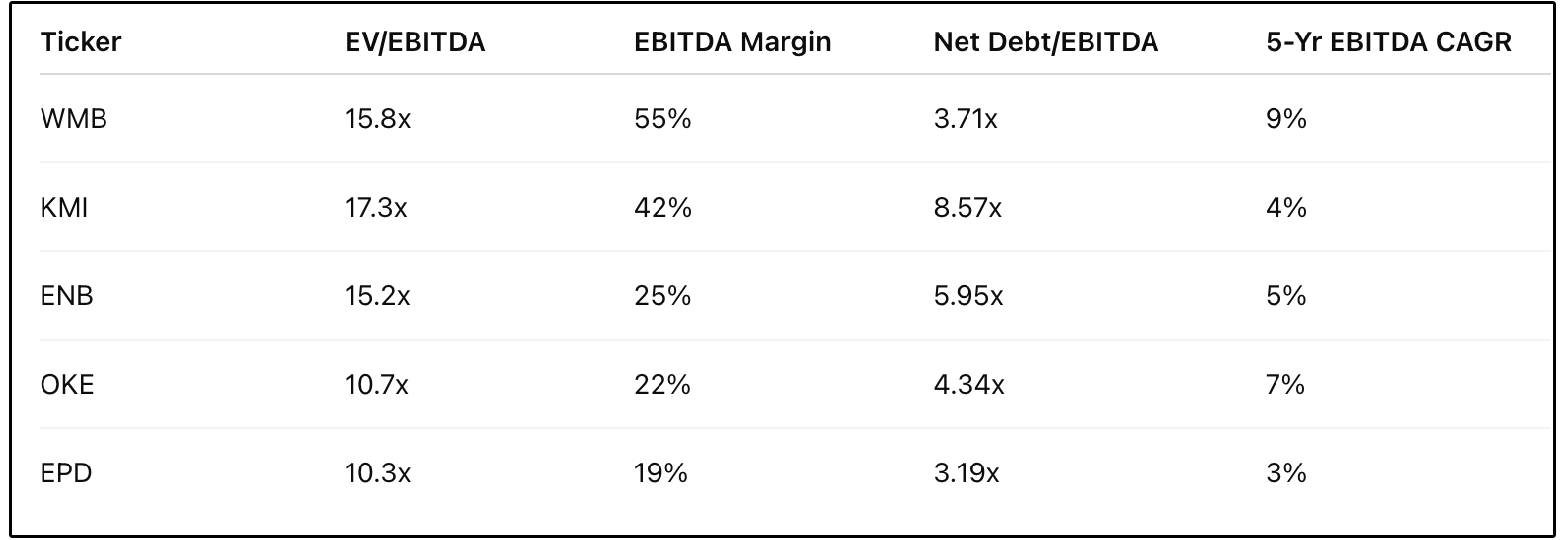

Despite these structural advantages, WMB trades at a valuation that I find compelling relative to their peers.

Despite trading at a lower valuation multiple to their closest peer (KMI), at current prices, WMB:

Is growing EBITDA faster

Has higher EBITDA margins

Has lower leverage

Than basically all of their peers.

If we look at them through the lens of a sensitivity analysis, assuming a 10% EBITDA CAGR with no multiple expansion over just a 2 year time period, we would be looking at a price target of $99 a share.

3. 💊 AbbVie (ABBV)

AbbVie operates across four primary business segments:

Immunology — Skyrizi, Rinvoq, and Humira

Neuroscience — Botox Therapeutic, Vraylar, Qulipta, and Ubrelvy

Oncology — Venclexta and Epkinly

Aesthetics — Botox Cosmetic, Juvederm, and related products

I’ve always been wary about investing in pharmaceutical companies due to the unpredictable nature of their future cash flows and reliance on constantly needing to add new drugs to their pipeline.

Because of this, I don’t often consider them ‘long term holds’ in a portfolio.

However, this doesn’t lead me to avoiding them entirely.

For years, the story surrounding AbbVie was simple:

The company was built around Humira, the best-selling drug in pharmaceutical history, and when its patent expired in 2023, investors braced for a cliff.

That cliff came.

However, AbbVie was able to successfully replace Humira revenues.

Skyrizi and Rinvoq just delivered $25.9 billion in combined 2025 revenue, surpassing AbbVie’s own 2027 long-term guidance target by $500 million, two full years early.

Management is now guiding these two drugs to generate over $31 billion combined in 2026, growing more than 20% year-over-year.

To put that in context: Humira, at its absolute peak, never generated that kind of revenue.

The replacement drugs for Humira are far exceeding expectations.

So why is AbbVie down roughly 15% from its October highs?

This is primarily due to two fears:

Competitive pressure — J&J received FDA approval for an oral psoriasis treatment, raising concerns about Skyrizi’s market share

Legal headwinds — A court upheld a law forcing AbbVie to extend 340B discounts to contract pharmacies, creating near-term margin pressure

These are real issues that we need to take into consideration.

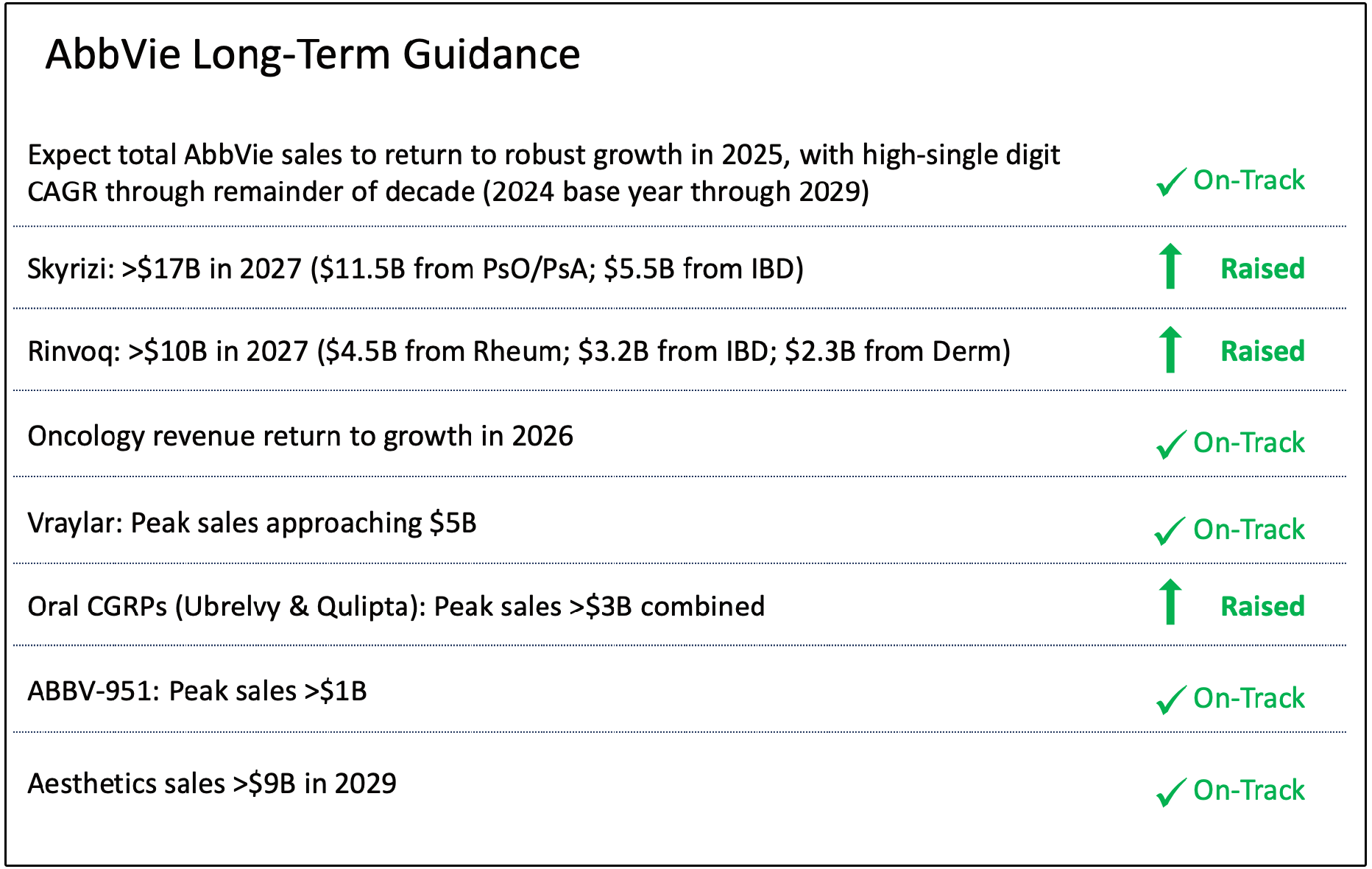

However, every single major growth target AbbVie has set is either on track or has been raised.

Skyrizi’s 2027 guidance has been raised to >$17B, Rinvoq’s 2027 guidance has been raised to >$10B. Oral CGRPs raised, and the high-single digit revenue CAGR through 2029 is still on track.

A single oral competitor in one indication does not dismantle a platform where management is raising guidance across the board.

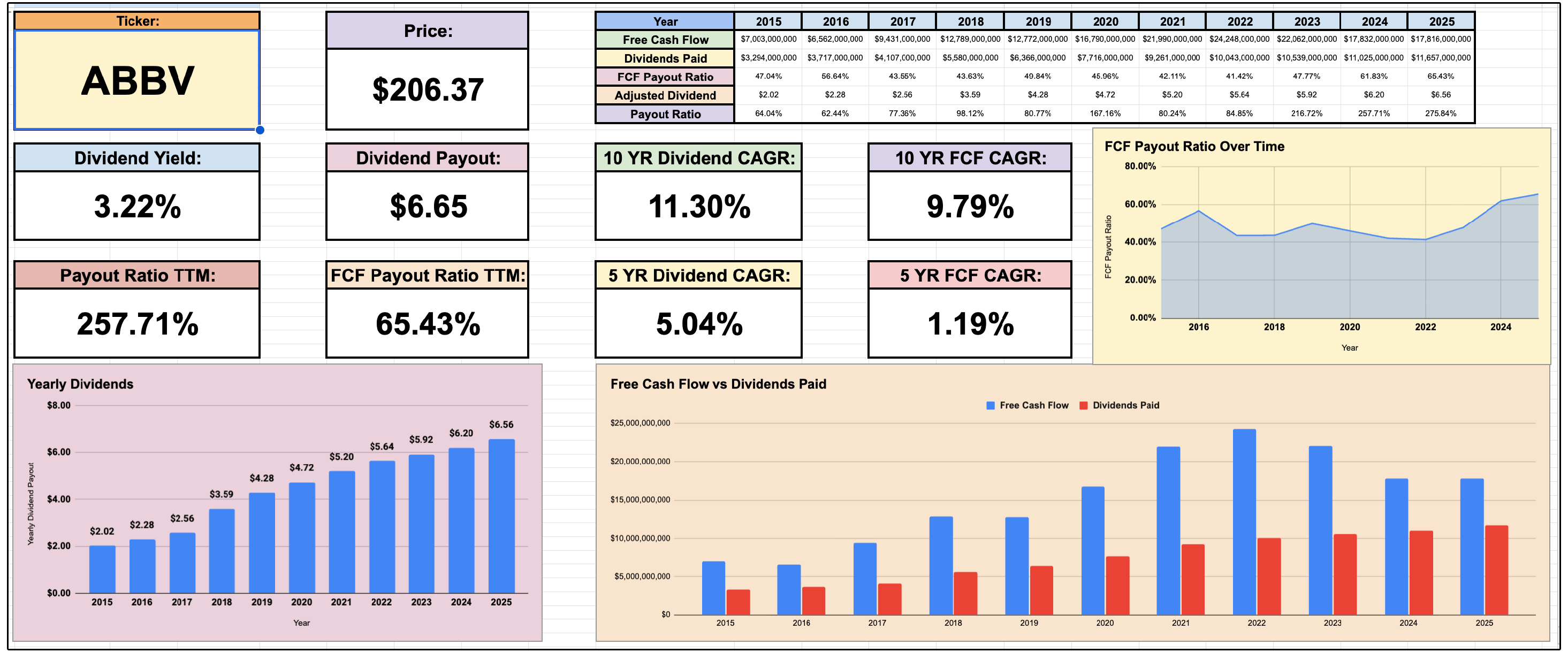

On top of this, AbbVie has raised its dividend for 54 consecutive years, making it a Dividend King.

The yield sits at 3.22% on an annualized payout of $6.92 per share, with a 5-year dividend CAGR of 5.9%.

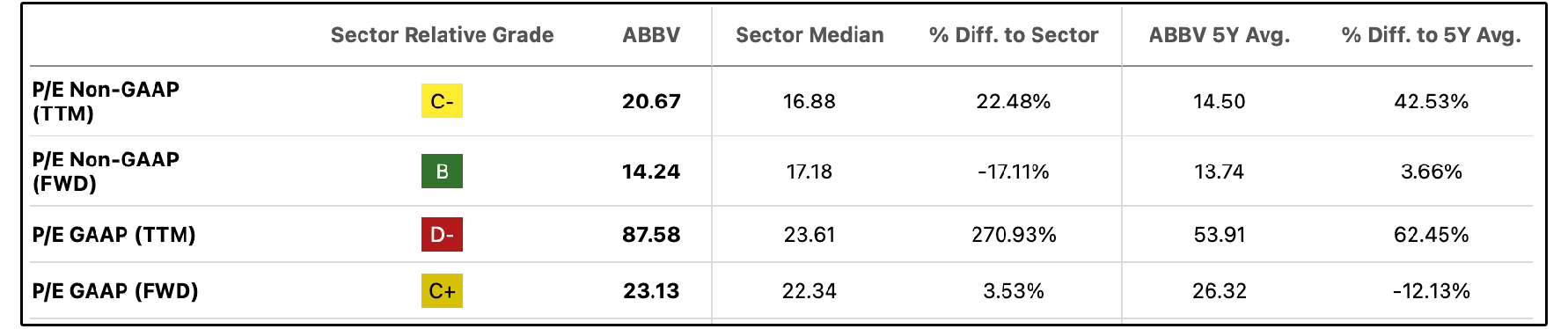

And the dividend is far more secure than the trailing P/E (~88x) makes it appear.

That number is almost entirely a function of temporarily compressed earnings during the Humira patent cliff.

On a forward basis, the picture is completely different.

AbbVie guided 2026 adjusted EPS to $14.37–$14.57, a 45%+ earnings reset in a single year as the Humira drag fades.

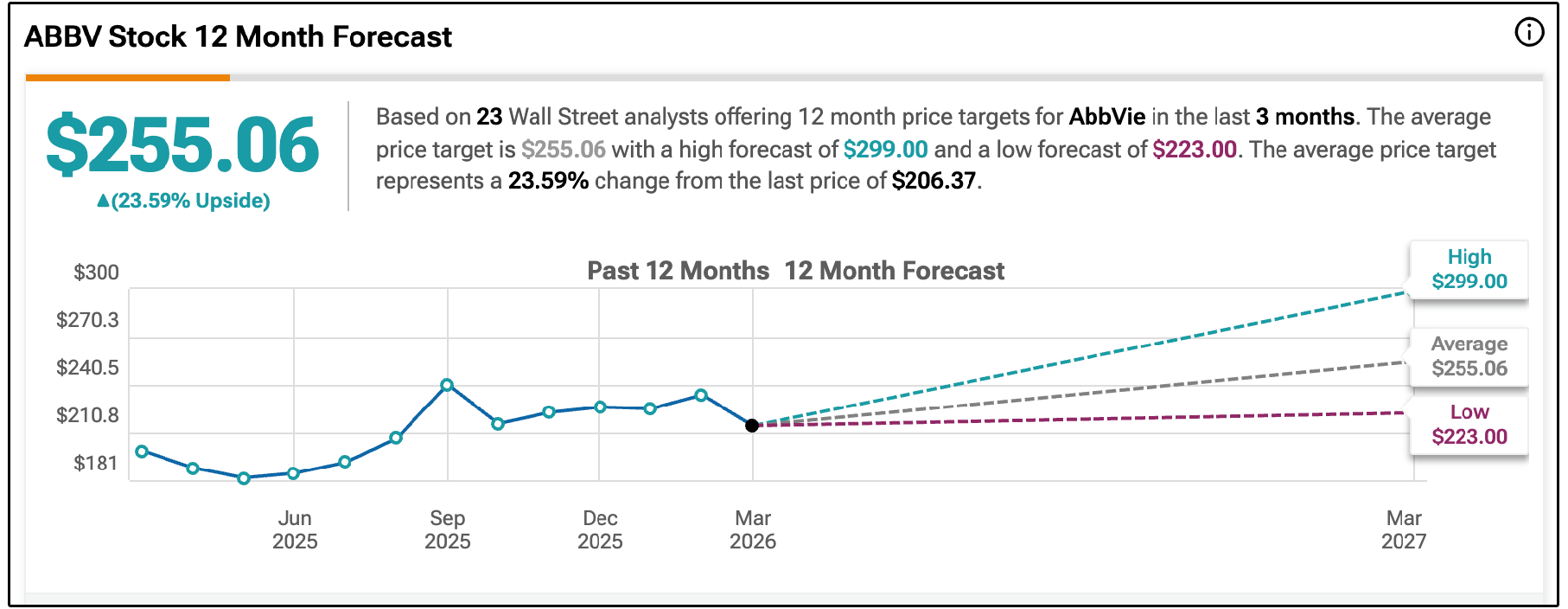

At a forward P/E of roughly 14.2x, analysts are giving them a price target of $255.

For a Dividend King yielding 3.3% with a high-single-digit revenue CAGR guided through 2029, that is one of the more compelling setups for AbbVie in the last few years.

Now, let’s review the full list for April.