🏆 List of Undervalued Dividend Stocks (June '26)

These Stocks are Undervalued! 🔥

At the beginning of each month, I send out a spreadsheet that lists out the dividend stocks that I believe to be undervalued.

This is the end result of 100’s of hours of research every month.

It’s time to dive in.

1. 🌿 NewLake Capital Partners (NLCP)

NewLake Capital Partners is one of the most interesting high-yield REITs on the market right now, yielding over 11%.

NLCP is a cannabis-focused REIT, which means its properties are highly specialized and its tenant base is much more limited than a traditional net lease REIT. If a tenant runs into financial trouble, re-leasing a cannabis cultivation facility is not nearly as simple as replacing a tenant in a retail or industrial property.

However, the key catalyst is cannabis moving toward Schedule III status at the federal level.

Under Schedule I, cannabis operators were unable to deduct normal business expenses due to 280E taxation, resulting in effective tax rates of 60–80% and severely constrained profitability.

Reclassification would allow normal deductions, which should lead to immediate improvements in free cash flow, balance sheets, and overall tenant credit quality.

Tenant risk is the primary reason NLCP trades at such a deep discount, so this would be a major catalyst.

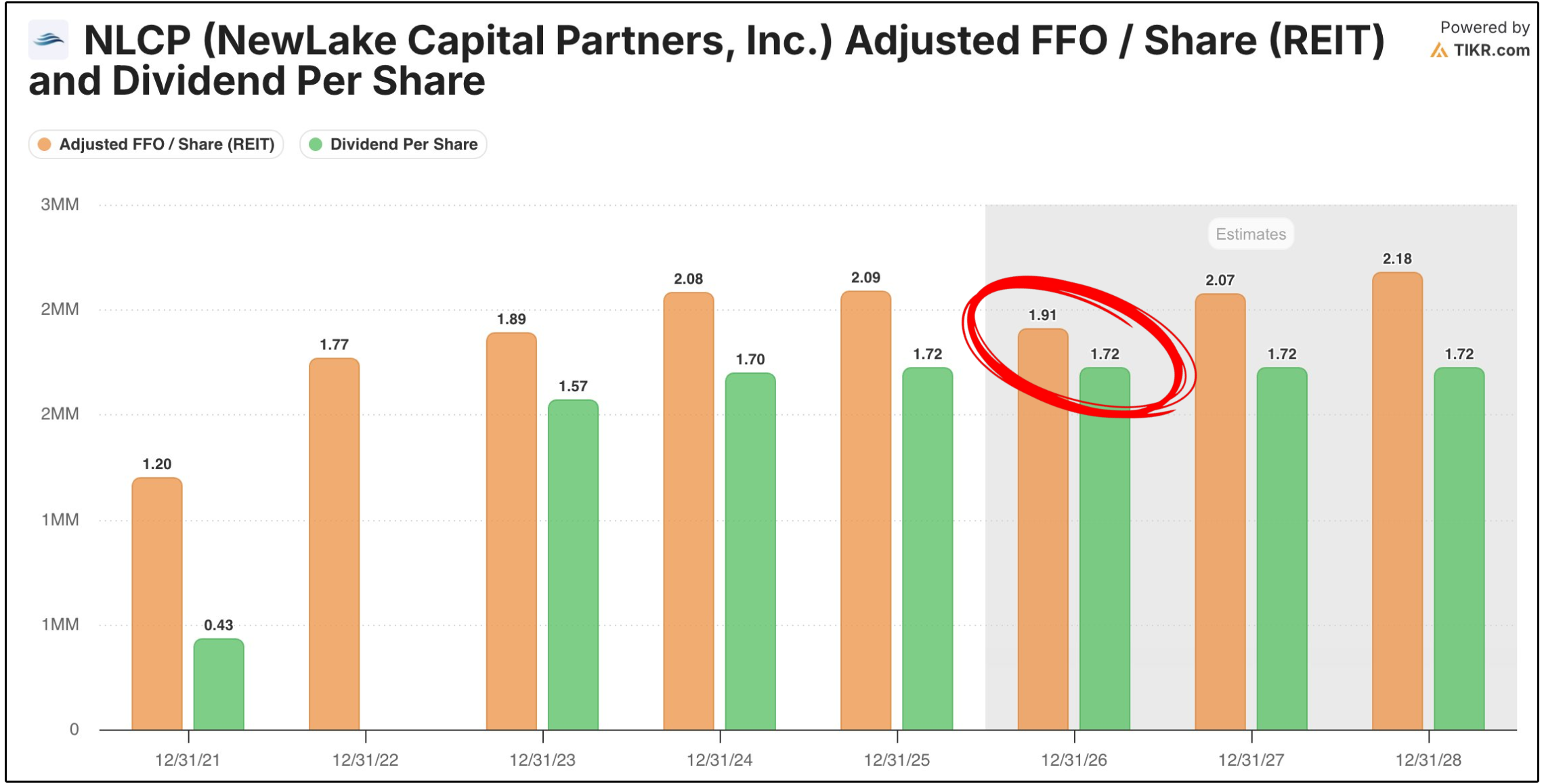

In the most recent quarter, NLCP had three large cultivation facilities sitting vacant, which pressured AFFO per share.

However, rent collection on the rest of the portfolio remained at 100%, showing that the broader portfolio is still performing well despite the challenges.

Management has also said they are seeing an uptick in interest for the vacant properties, though increased conversations do not guarantee those properties will ultimately be leased.

This is the core risk/reward setup.

The stock is cheap because the market is worried about tenant quality, tenant concentration, vacancies, and the specialized nature of cannabis real estate.

But if rescheduling improves operator cash flow and credit profiles, the entire risk profile of the business could improve materially.

This could lead to stronger tenants, easier re-leasing, better rent collection, and potentially improved access to capital for the broader cannabis industry.

Another potential catalyst is a major exchange listing.

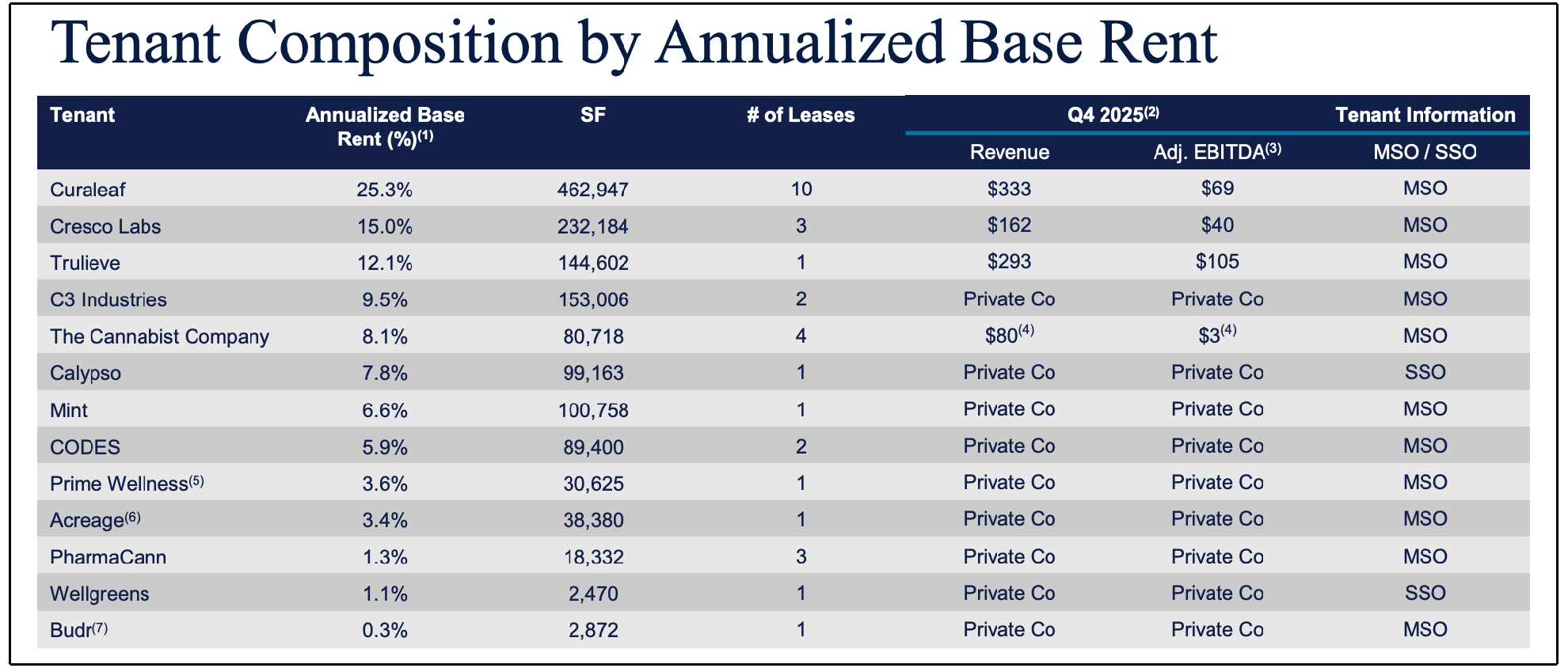

Management has said roughly 50–55% of annualized base rent is currently derived from medical cannabis activities, which could become important for NYSE or Nasdaq listing eligibility as cannabis regulation evolves.

A major exchange listing would likely improve liquidity and could expand the pool of investors willing to own the stock.

Even after the recent rally, NLCP still trades at just 7.98x P/AFFO.

They also trade with:

An 11.32% dividend yield

An AFFO payout ratio of roughly 82%, near the low end of management’s 80–90% target range

A net cash position, with more cash than debt

Even though AFFO per share is projected to drop slightly over the next year, it should still well cover the dividend.

Unlike most REITs, NLCP carries virtually no debt.

That gives the company far more flexibility than the average high-yield REIT, especially in a higher-rate environment.

To be clear, NLCP remains risky.

Rescheduling is not a magic fix.

Even if cannabis moves to Schedule III, the industry will likely remain volatile, and cannabis real estate will probably continue to deserve a higher risk premium than traditional REIT sectors.

NLCP already owns long-term leases with annual rent escalators. If the industry backdrop improves, the market may be forced to re-rate the stock closer to a more normalized valuation.

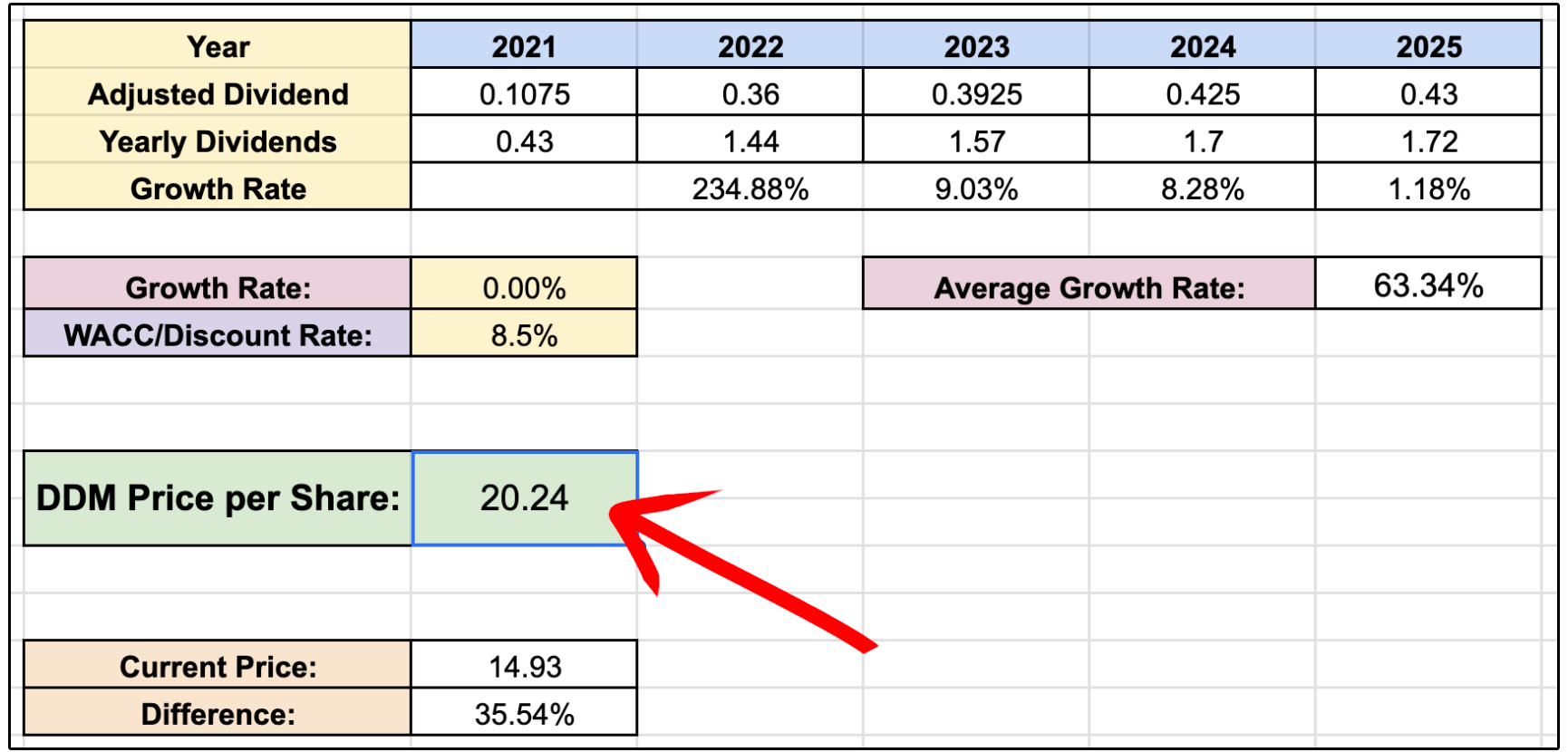

If NLCP can simply maintain their dividend at these levels, it would imply over 35% upside from current prices.

2. 🌲 Rayonier (RYN)

Rayonier is one of the more unique dividend stocks on the list because it gives investors exposure to a very different type of asset:

Timberland.

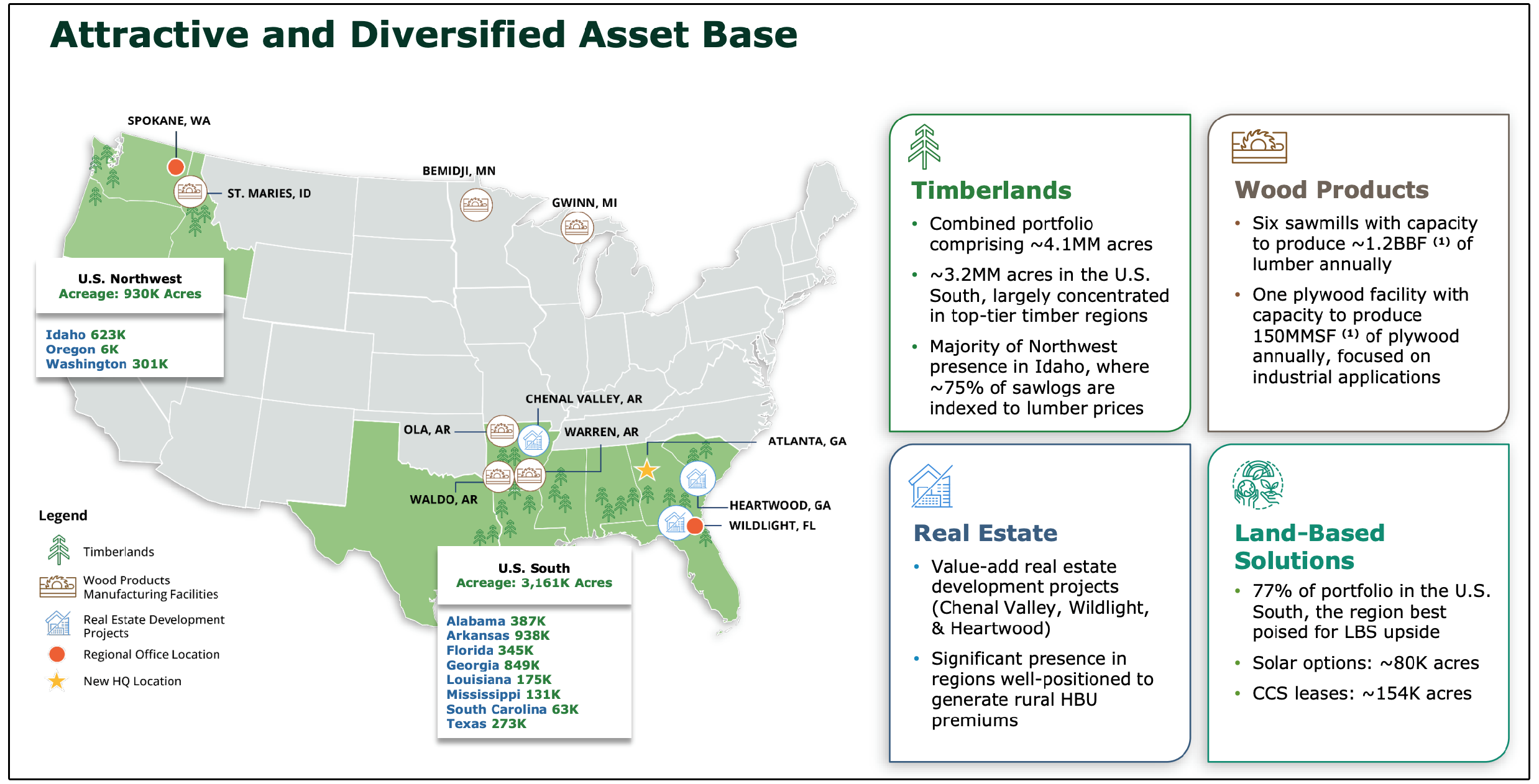

The company owns more than 4 million acres of land across the United States, giving shareholders exposure to hard assets, timber, real estate development, solar optionality, and other higher-and-better-use opportunities.

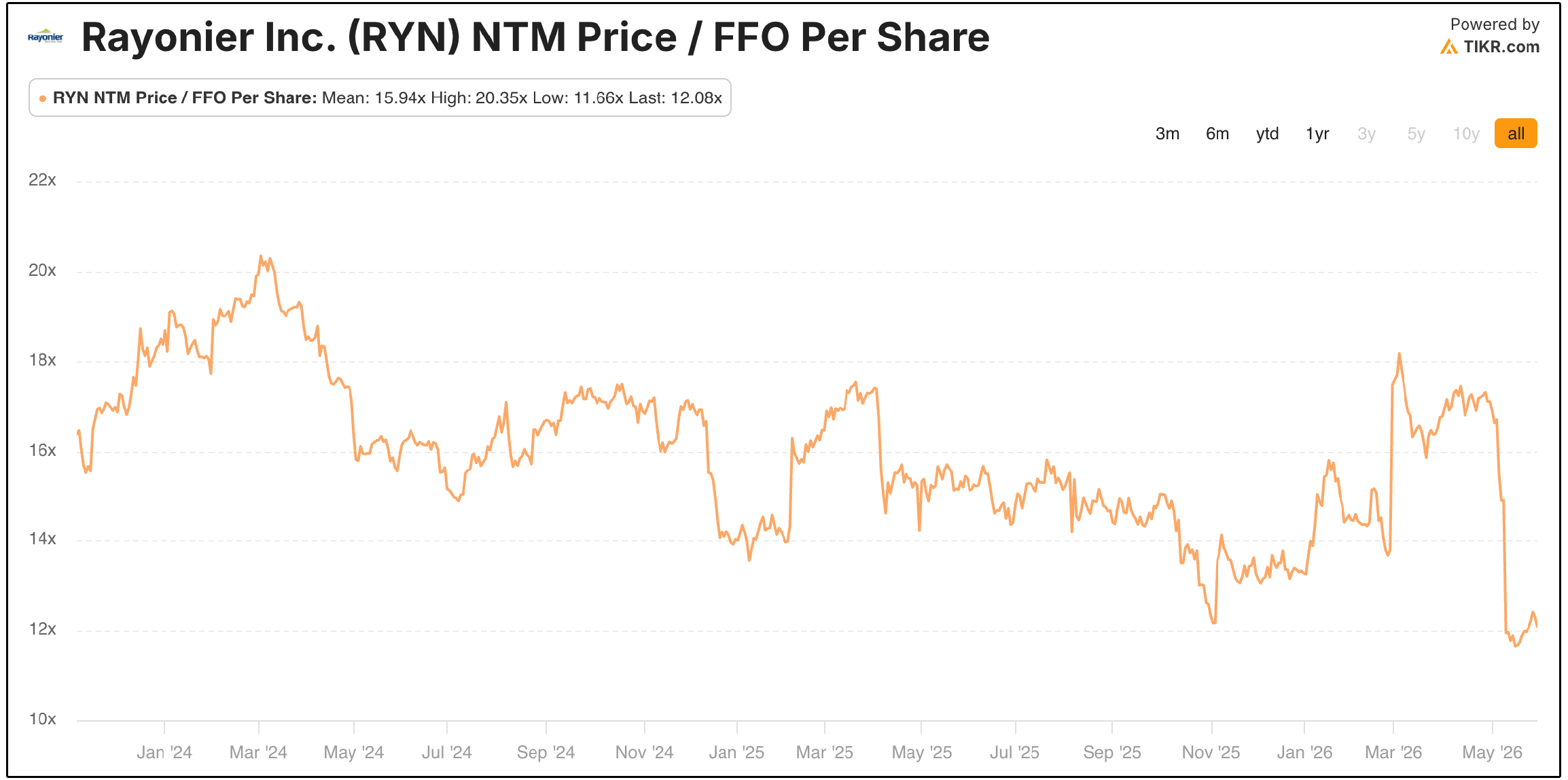

But in the last 5 years, this REIT is down 42%.

The market appears to be valuing the company more like a cyclical lumber business than a scarce land platform.

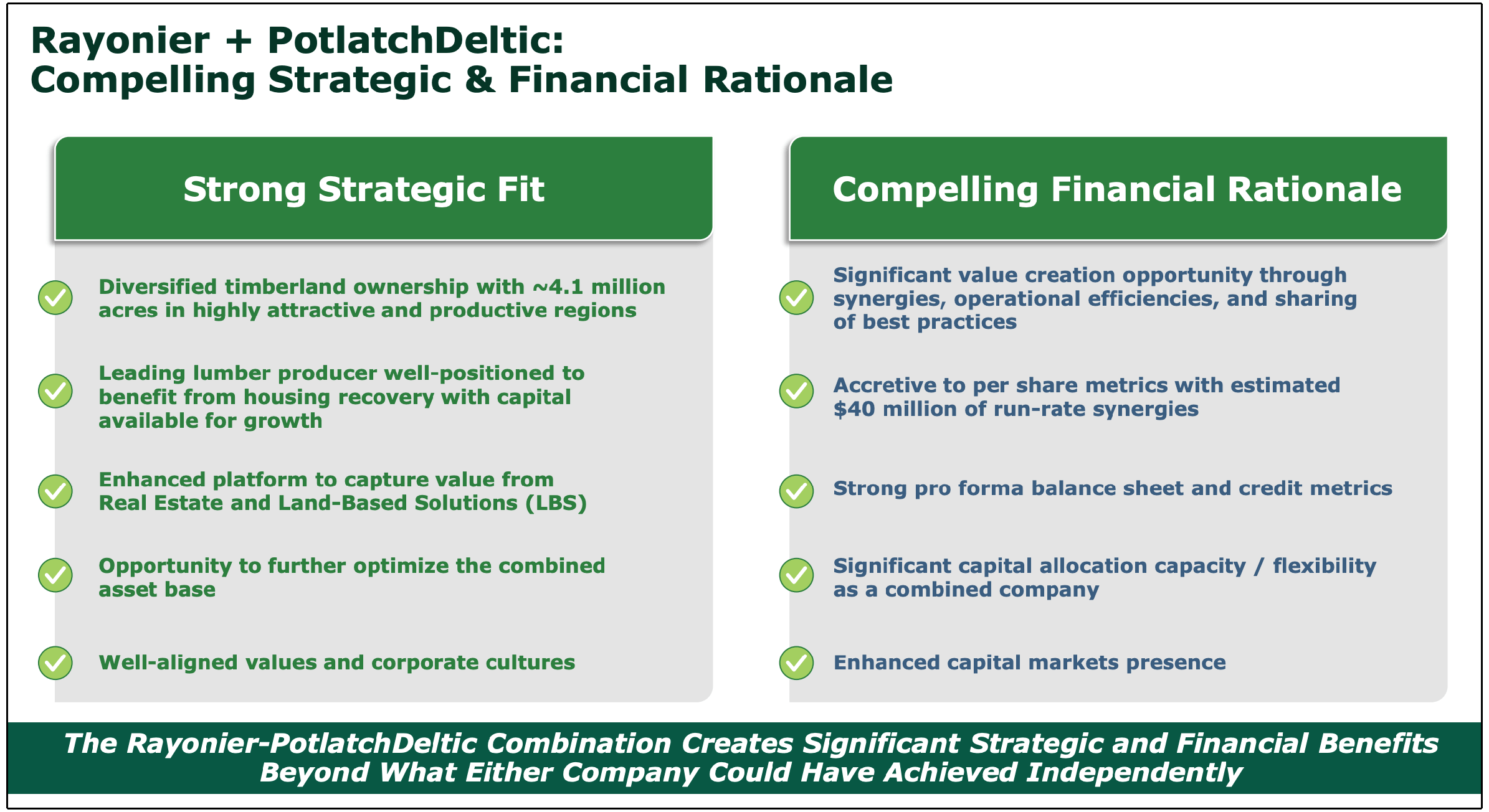

That disconnect likely stems from near-term weakness in housing, pressure on lumber prices, and the company’s increased exposure to wood products following the PotlatchDeltic merger.

Lumber manufacturing is a much more cyclical, lower-margin business than simply owning timberland.

Sawmills have higher fixed costs, less pricing power, and more exposure to swings in lumber prices. This is one of the key risks investors need to monitor going forward.

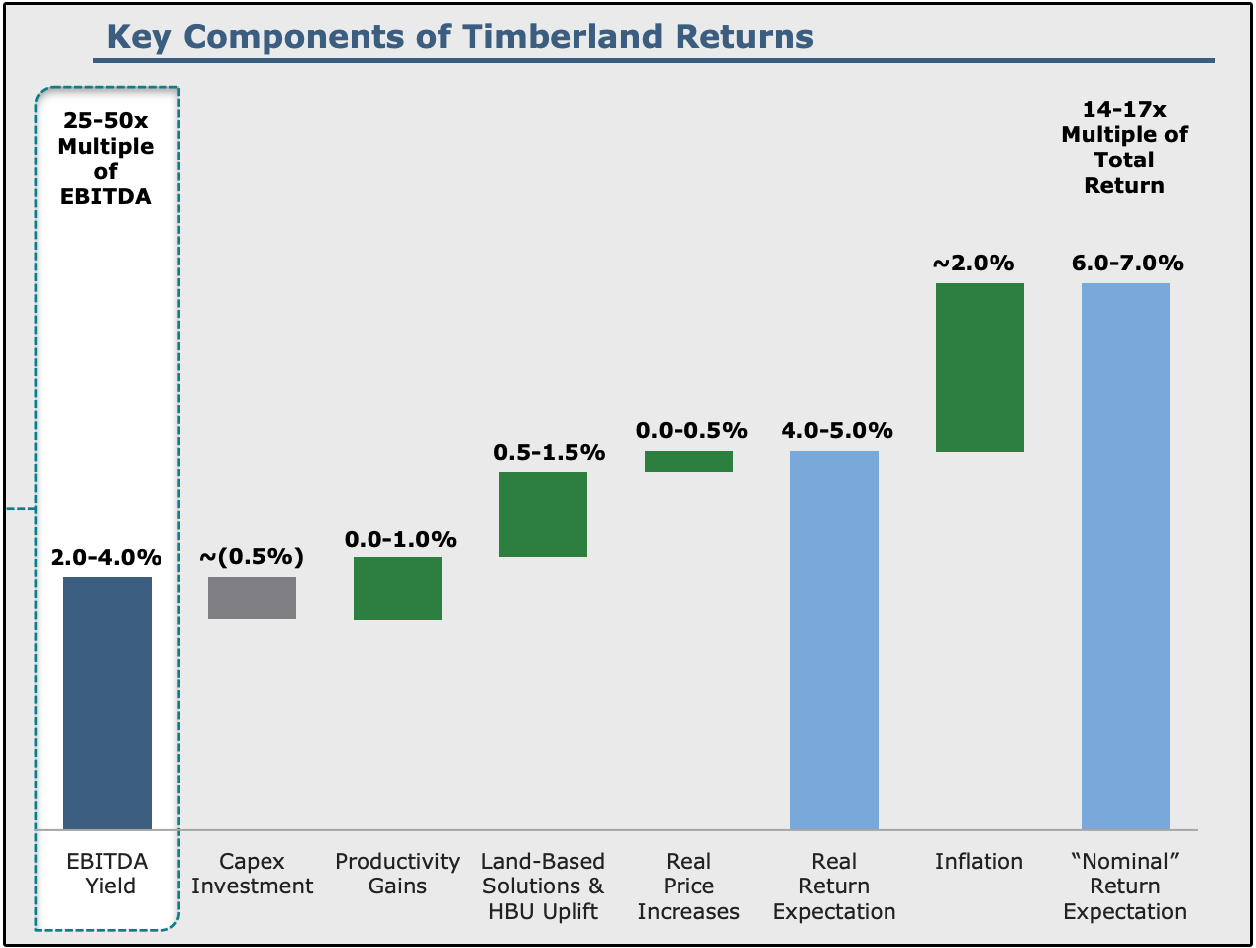

But the core timberland business is structurally different from most commodity businesses.

Unlike crops that must be harvested within a short window, trees can be left in the ground when pricing is weak.

In many cases, waiting can actually increase value, because trees continue to grow in volume and can move into higher-value product categories over time.

That gives timberland owners a level of flexibility that many commodity producers do not have.

The bigger opportunity, however, is Rayonier’s land optionality.

Rayonier owns land that can be monetized through higher-and-better-use projects, including master-planned communities, rural land sales, solar projects, conservation, carbon capture, recreation leases, and other land-based solutions.

The real estate segment is especially important because it can generate far higher margins than timber operations. Projects like Wildlight in Florida, Heartwood near Savannah, and Chenal Valley in Arkansas show how Rayonier can turn ordinary timberland into much more valuable development land over time.

Valuation is where the thesis gets interesting.

Rayonier currently trades at a rare discount to Weyerhaeuser, its closest publicly traded peer.

A sum-of-the-parts approach also suggests the market may be giving very little credit to Rayonier’s underlying land value and HBU opportunities.

When you break the company apart, the value is not just in the current timber cash flow.

There is value in the Southern timberland, Northwest timberland, development land around projects like Wildlight, potential solar acreage, and the wood products business.

Even using conservative assumptions, the estimated net asset value appears meaningfully higher than where the stock trades today.

That means investors may be getting the core timberland business at a discount while paying very little for the upside from solar, real estate development, carbon capture, and other land-based opportunities.

The dividend is another part of the appeal.

Rayonier’s base dividend yield is above 5%, and management has also discussed a special dividend following asset sales.

The company has also repurchased stock and could continue buying back shares if the public market discount to private market value persists.

To be clear, Rayonier is not a perfect dividend growth stock.

Its dividend has been uneven, the lumber market is cyclical, housing remains under pressure, and the PotlatchDeltic merger adds more exposure to manufacturing.

But for investors looking for real asset exposure, timberland, land optionality, and a stock trading at a meaningful discount to estimated private market value, Rayonier looks like an interesting long-term opportunity.

3. 💳 Mastercard (MA)

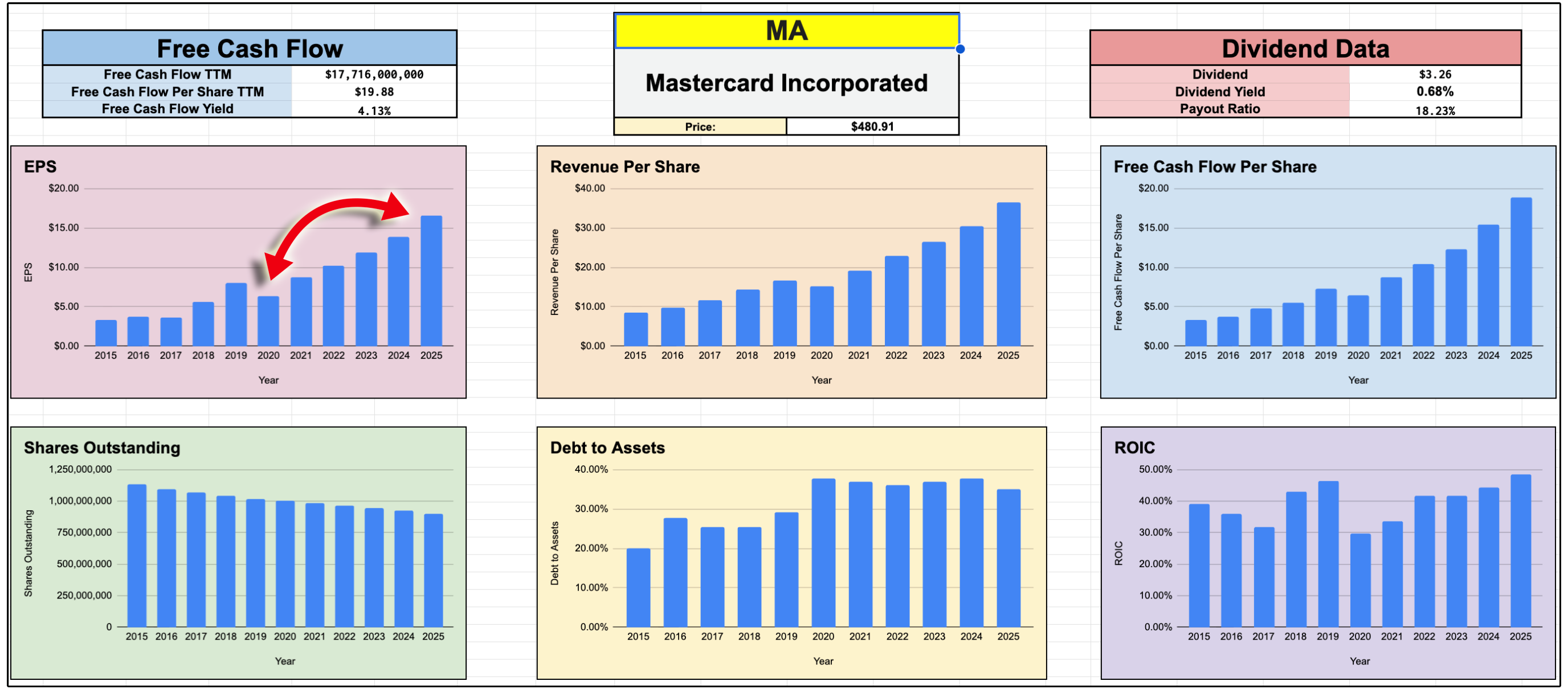

Mastercard is a great example of a capital-light compounding machine.

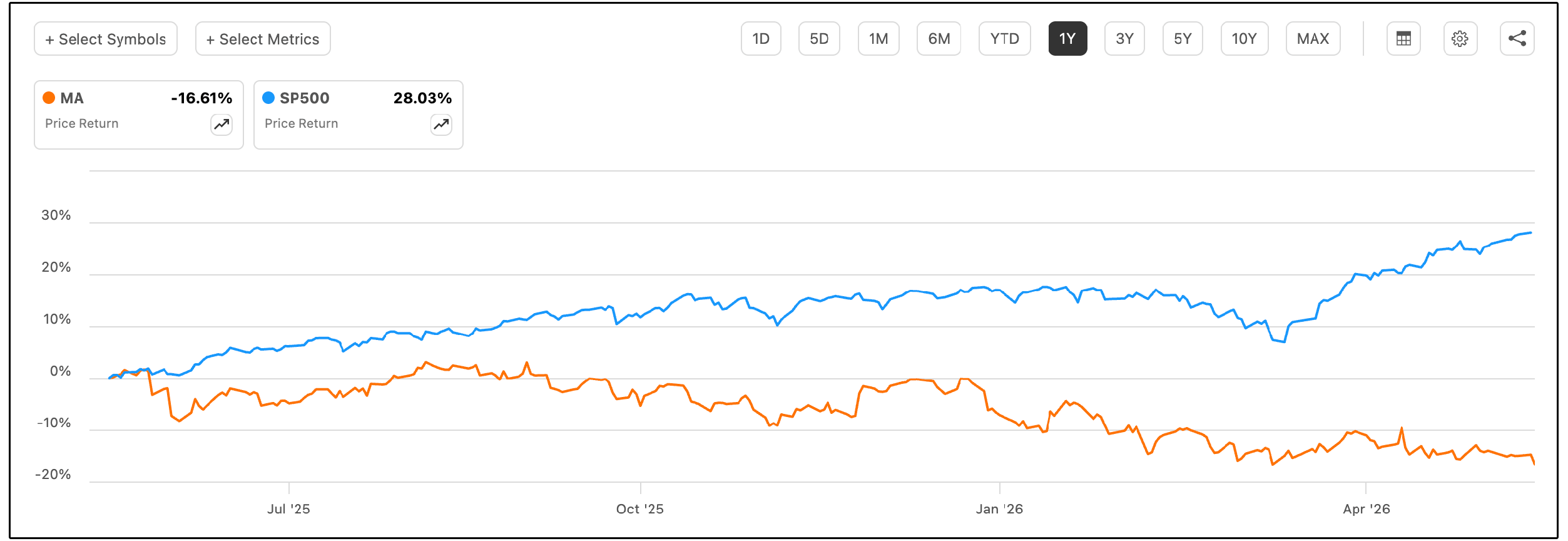

However, over the last year, Mastercard has significantly underperformed the S&P 500.

The stock has fallen double digits while the broader market has moved much higher.

That type of underperformance is unusual for a company that has historically been one of the best compounders in the market.

But the underlying business itself has continued to perform well.

Over the last five years, Mastercard’s earnings per share have grown by roughly 150–160%, while the stock price has only increased by a fraction of that.

When earnings grow much faster than the share price, the valuation naturally compresses.

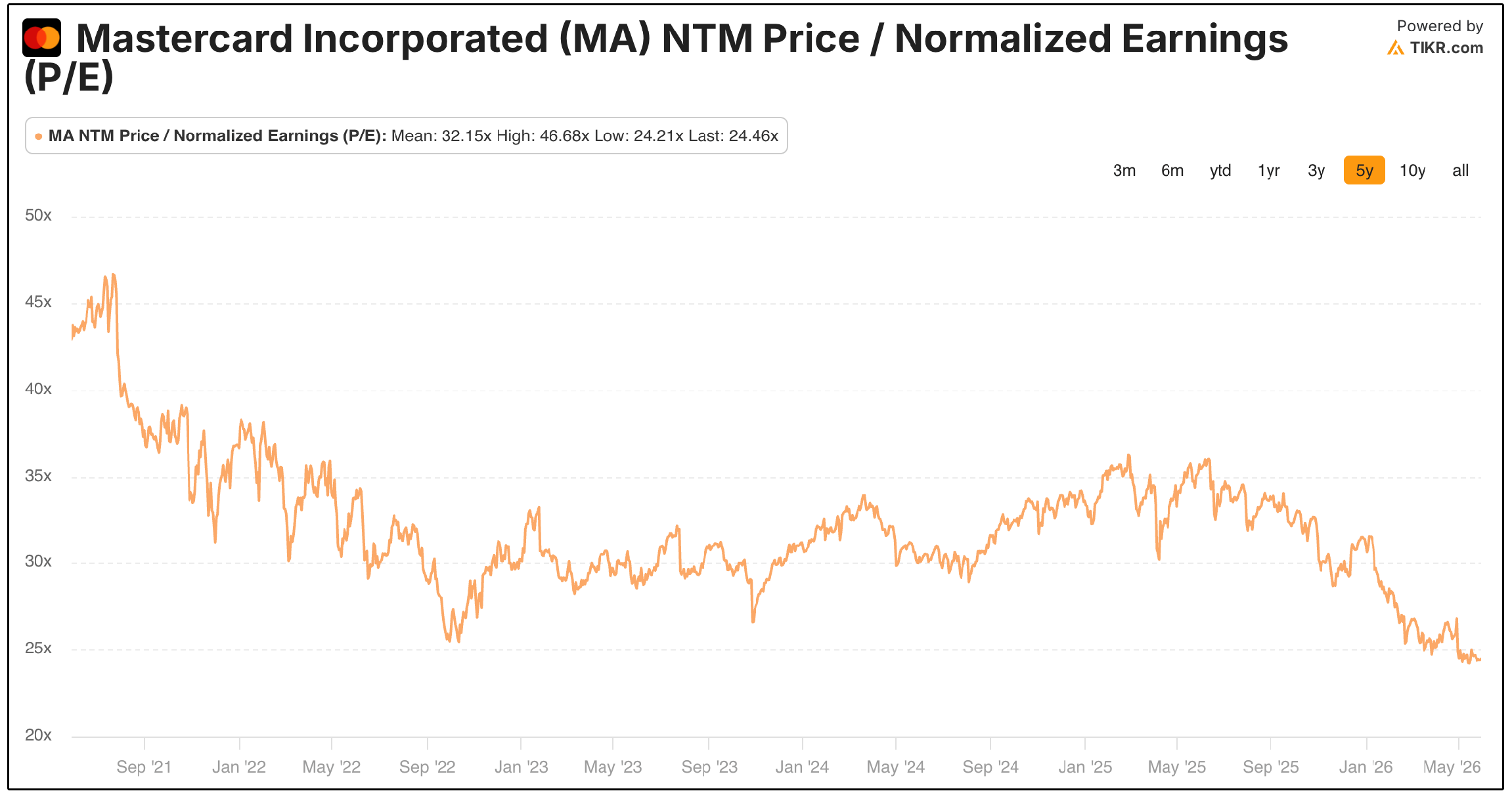

Mastercard is now trading near its lowest valuation multiple in the last five years, despite still being expected to grow earnings at a strong double-digit rate.

The reason Mastercard deserves a premium valuation is because of the quality of its business model.

Mastercard is not a lender.

It does not take credit risk like a bank.

Instead, it operates one of the largest payment networks in the world and earns fees from transaction processing, cross-border volume, assessments, data services, fraud tools, and other payment-related services.

This creates an incredibly capital-light business with very high margins.

From a dividend perspective, the company:

Yields 0.70%

10 YR Dividend CAGR of 15.68%

FCF Payout Ratio of 16.30%

Let’s address a few of the concerns.

The market primarily has three concerns at it relates to Mastercard:

Regulatory risk

Stablecoins

Agentic commerce

The first concern is regulation, especially around credit card interest rates.

But again, Mastercard does not earn its money from interest income.

That risk would primarily fall on the banks issuing the credit cards, not the payment network itself.

Another concern is stablecoins.

The fear is that blockchain-based payments could bypass Visa and Mastercard.

This misses the real value Mastercard provides.

Mastercard is a global trust layer for payments, providing fraud detection, identity verification, compliance, tokenization, dispute resolution, settlement, and merchant acceptance.

Those services may become even more important in a stablecoin world.

The market seems to believe that Agentic commerce is another potential risk, but in reality, it could become a major opportunity.

If AI agents begin making purchases on behalf of consumers and businesses, the number of digital transactions could increase meaningfully.

More transactions should ultimately benefit companies that provide secure payment infrastructure.

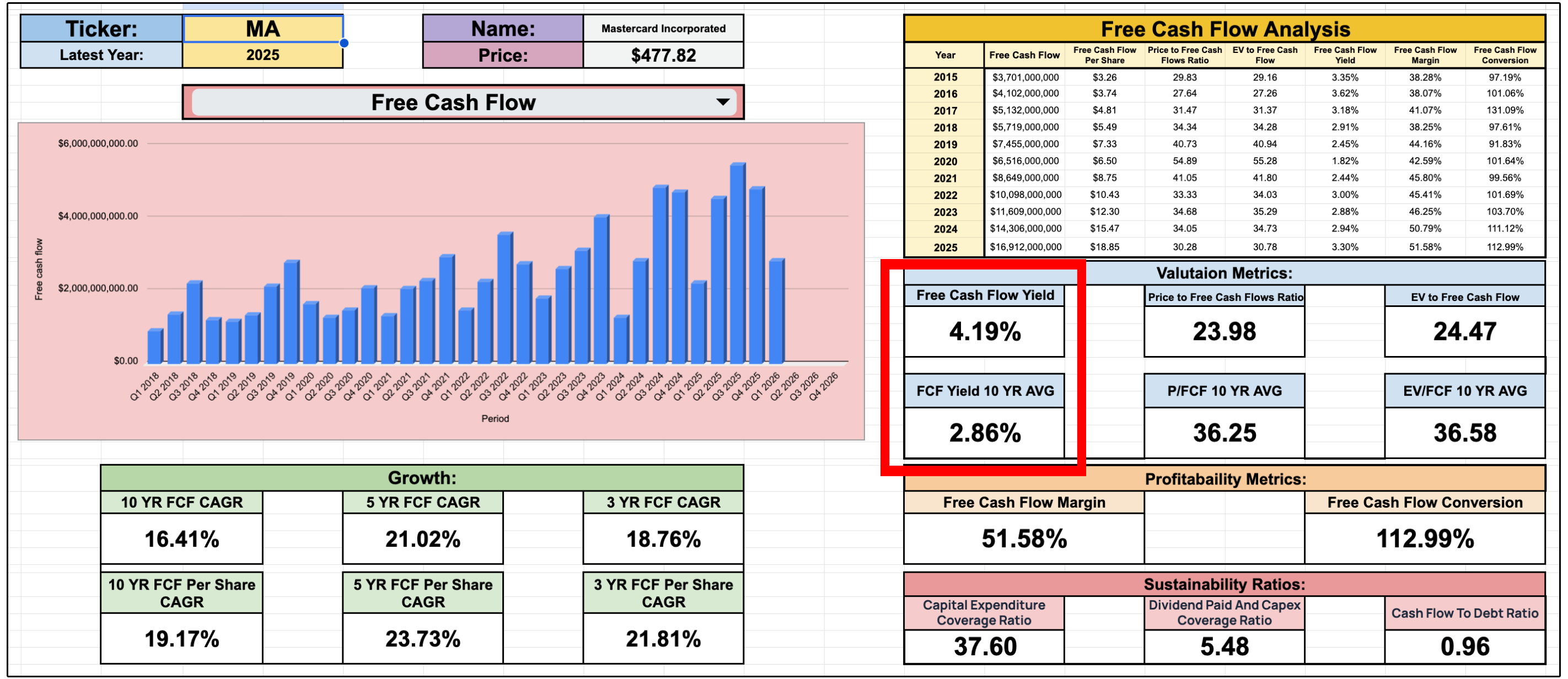

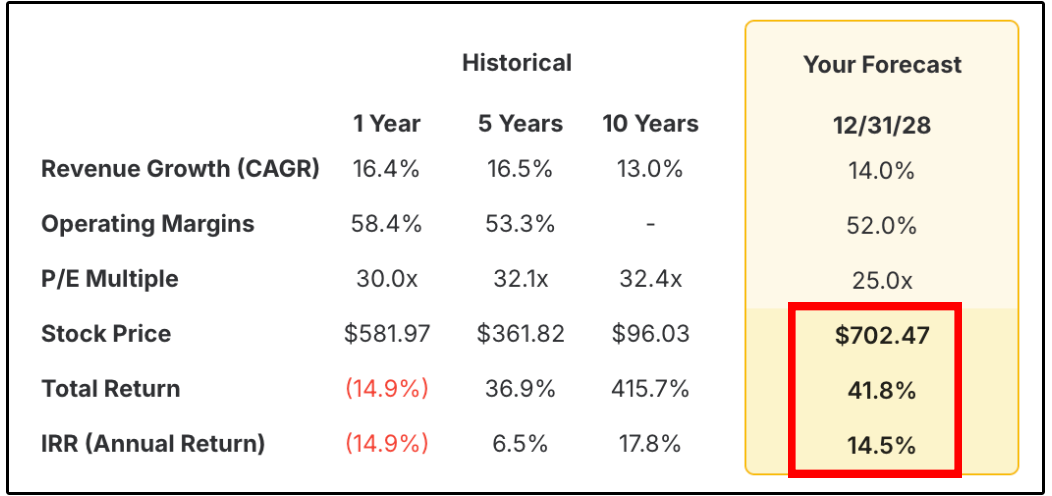

Mastercard now trades at a free cash flow yield of 4.19%, meaningfully above their historical average, despite free cash flow projections remaining strong.

That makes Mastercard look especially interesting right now.

If we make conservative assumptions, and assume that:

Revenue grows at 14% annually

Operating margins slightly decline

The P/E multiple sits around 25x, well below their historic average

You’d still be looking at compounded returns of 14.5% annually through 2028.

Now, let’s review the full list for June.