🏆 List of Undervalued Dividend Stocks (June '25)

These Stocks are Undervalued 🔥

At the end of every month, I send out a spreadsheet that lists out the dividend stocks that I believe to be undervalued.

This is the end result of 100’s of hours of research every month.

If you’d like to receive it, consider becoming a paid member.

Now, let’s dive in.

LIKE ALWAYS… Before we even begin to look at the stocks listed on the spreadsheet, it’s important we understand a few important points.

I almost always discuss these points in my paid newsletters, but it’s important we revisit them for newcomers and as a reminder to ourselves.

Just because a stock is undervalued, does not mean you should buy it. (Make sure it fits into your portfolio.)

What’s considered a good buy for one person, may be a bad buy for another person.

It can take time for a stock to revert to intrinsic value.

The Market Moves in Cycles

Before we look at the sheet, let’s review a few interesting opportunities:

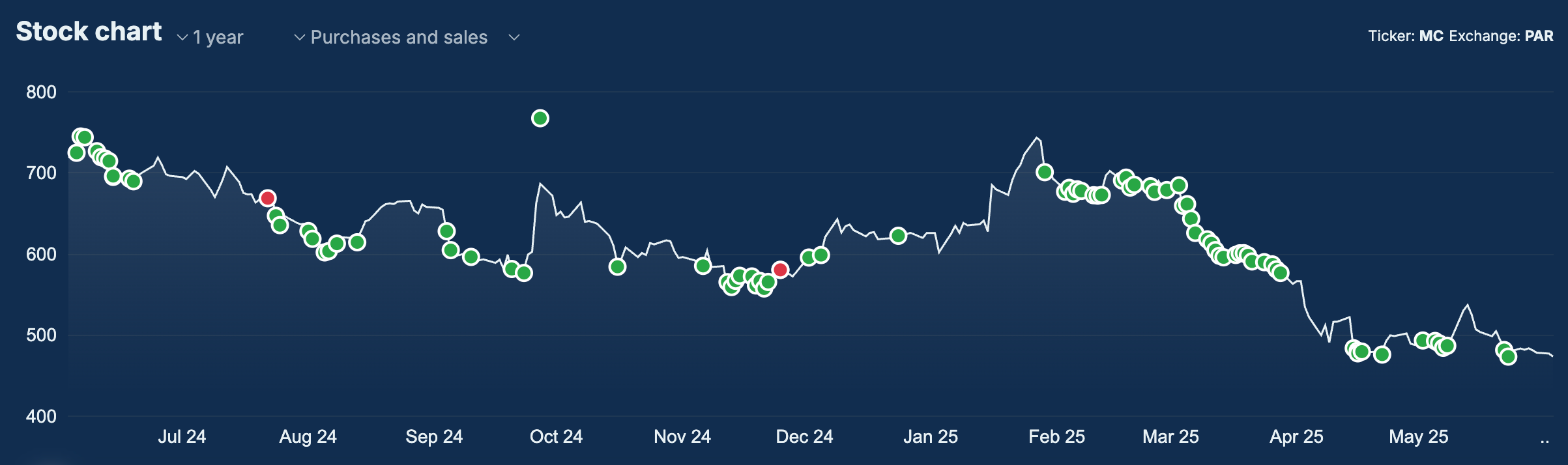

1. 👜 Louis Vuitton (LVMHF)

Louis Vuitton is now down -32% in the last year and trading right at their 52 week low, giving them a starting yield of 3.15%.

This is in the midst of founder Bernard Arnault continuing to make a substantial amount of insider purchases since the beginning of 2025.

The Arnault Family had around 48% ownership of LVMHF at the end of 2023, so it’s likely they are aiming to have over 50% control over the business. Keep in mind, research has shown that stocks that are ‘founder led’ typically outperform the market over the long term.

Not only is Arnault buying these shares at the companies lowest share price since 2020, but he is buying them at the lowest Price to Cash Flow valuation in over 5 years as well.

While the company is still seeing growth in US and European markets and significant growth in Japan, Asian markets are currently a significant pain point for the company.

Despite strong growth and easing inflation in 2024, Asia-Pacific’s near-term outlook has been downgraded due to new U.S. tariffs, global trade tensions, and weak external demand. Growth is expected to slow through 2026, but the long term outlook is still positive.

LVMHF is currently trading at a price-to-earnings ratio that is 22.38% below its historical average.

While a somewhat lower PE ratio may be warranted due to lower growth projections over the next year and a half, the selloff appears over exaggerated.

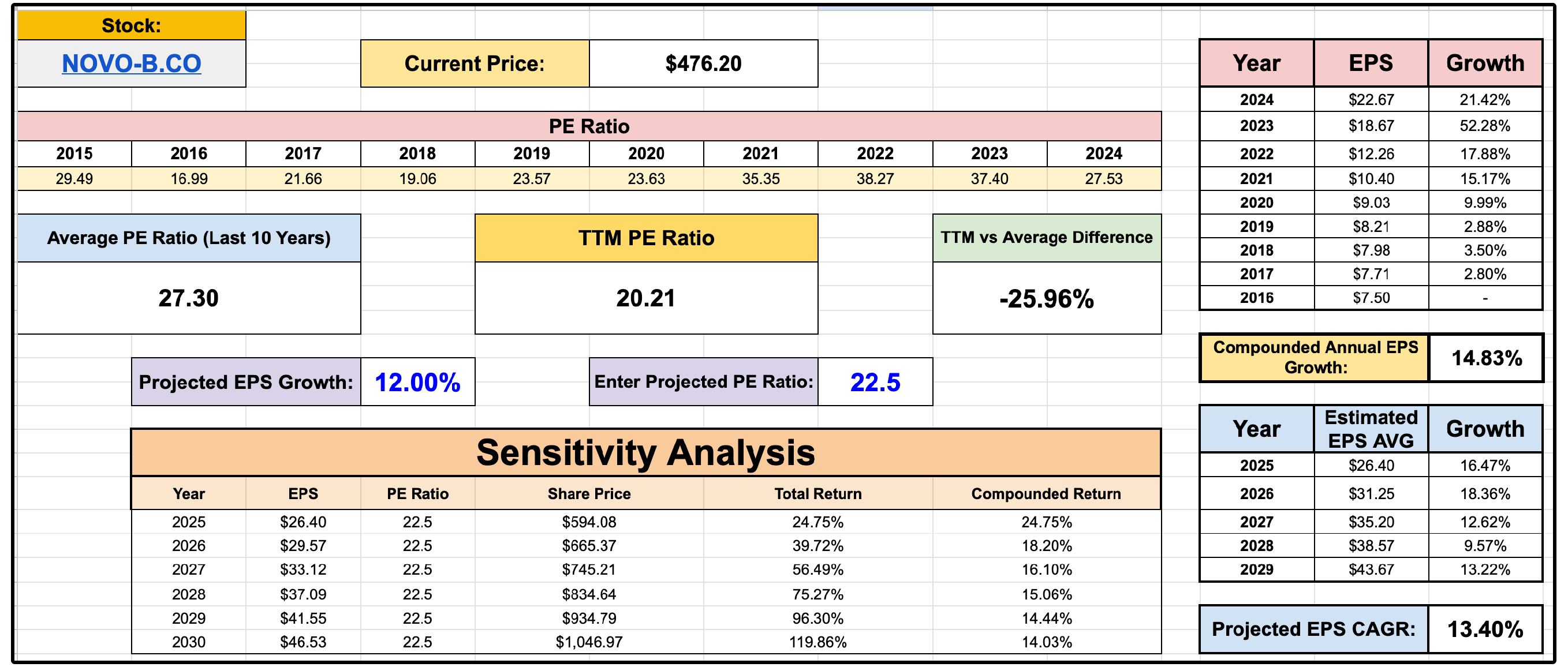

2. 💉 Novo Nordisk (NVO)

Novo Nordisk is down nearly 48% over the last year and has fallen over 15% year-to-date, despite continued strength in its core diabetes and obesity franchises.

Because of the sell off and due to the fact they have grown their dividend at above a 20% CAGR over the past 5 years, they now have their highest starting yield in over 5 years.

The company recently cut its 2025 guidance for revenue and operating profit growth, changed CEO leadership, and now trades at a forward P/E ratio of just 19.25, which is nearly 30% below its 5-year historical average of 27.3.

Despite near-term concerns around market share pressure from Eli Lilly, Novo still dominates the GLP-1 space with over 50% market share, and the obesity drug market is expected to grow to $170B by 2030 at a staggering 32% CAGR — faster than AI.

Even with competition, Novo is well-positioned to ride that wave of their market growth.

Financially, Novo remains a juggernaut: a 5-year EPS CAGR of ~14.4%, FCF CAGR of 14.4%, and dividend CAGR of 21.5%, with a current forward yield above 3%.

The company also boasts a gross margin near 85% and ROIC near 40%, two indicators of sustained competitive advantage.

Based on current EPS growth projections and a modest reversion in valuation, analysts see the potential for ~120% total returns by 2030, around a 14% compound annual return, without pricing in a best-case scenario.

Despite the selloff, the underlying fundamentals remain strong. Novo Nordisk looks like a rare case of a market leader trading at a discount.

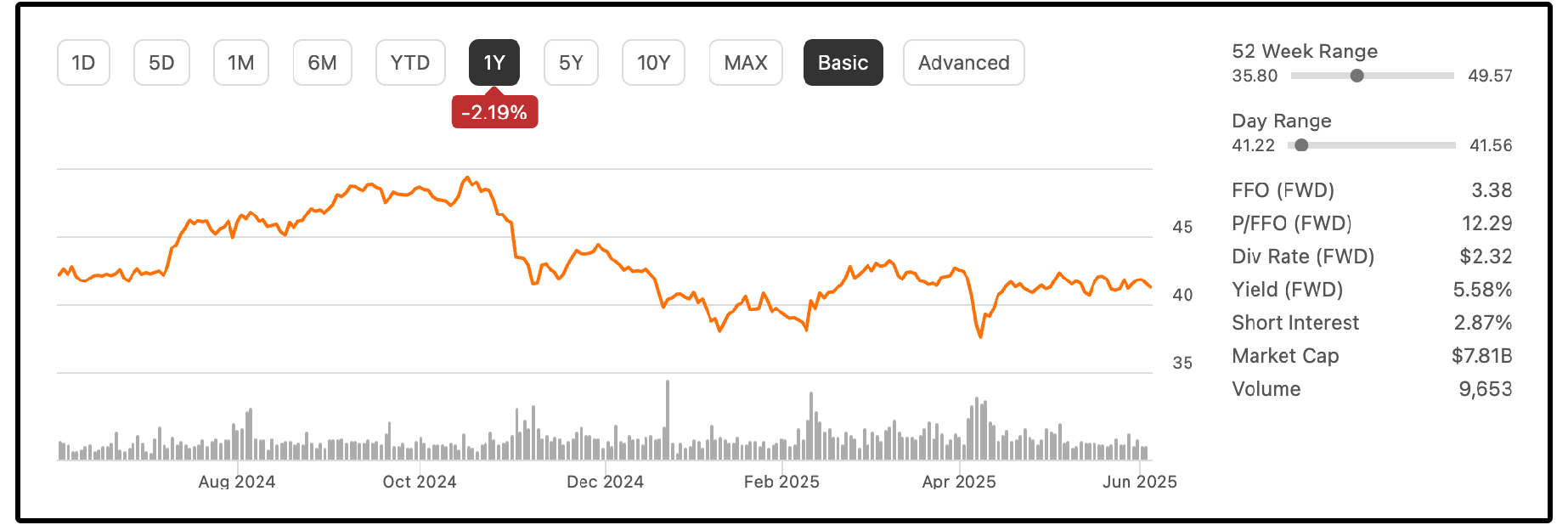

3. 🏬 NNN Reit (NNN)

NNN REIT is currently trading just under $42/share with a 5.58% yield, and remains flat over the past year, despite rising FFO per share, AFFO per share, and revenue growth in Q1 2024.

Keep in mind, growing AFFO per share is the ultimate ‘value driver’ long term for REITs.

NNN REIT posted solid Q1 results with higher revenue and FFO, but tenant issues caused occupancy to dip to 97.7% from 99.4% last year.

Management is actively addressing the problem, having sold or re-leased many of the affected properties, and expects full resolution by year-end.

Meanwhile, the portfolio grew to 3,641 properties with $232.4M in new investments.

These investments were made at an average cap rate of 7.4%, which is a measure of expected return based on the property’s income.

A 7.4% cap rate generally indicates the company expects to earn a 7.4% return annually on those new investments, before factoring in financing costs.

Despite macro headwinds, NNN maintains one of the strongest dividend profiles in the REIT sector.

Their AFFO payout ratio was just 66% in Q1, with an expected full-year payout ratio below 70%, more conservative than peers like Realty Income (O) and Agree Realty (ADC).

NNN has increased its dividend for 34 consecutive years, most recently by 2.7%.

A modest bump to $0.595/quarter would mark another year of consistent growth, pushing the annual dividend to $2.35/share.

Longer term, as tenant turnover is completed and the macro environment stabilizes, NNN could trade at a 14x–16x AFFO multiple, compared to its current 12.15x, implying a price target between $48–$51/share.

This would put their valuation multiple in line with their peers.

Now, let’s jump into this month’s full list below. 👇