🏆 List of Undervalued Dividend Stocks (July '26)

These Stocks are Undervalued! 🔥

Meta once dropped 70%. Netflix: 50%. Amazon: 40%. Every investor had ruled them out, citing “the companies were done”.

But they all rebounded - Meta: 690%. Netflix: 540%. Amazon: 153%.

Every world-class company suffers deep drawdowns. Rebound Capital identifies high-quality companies undergoing drawdowns to capitalize on their eventual rebound.

In year one, they initiated coverage on 27 companies, calling ASML (up 135%), AMD (up 152%), and Eli Lilly (up 72%) before the market re-rated them. 10 names in their coverage are still trading below fair value today.

Dividendology Readers can unlock the full deep dive on all 10 rebound opportunities, free.

Thanks to Rebound Capital for sponsoring.

💰 Undervalued Dividend Stocks

At the beginning of each month, I send out a spreadsheet that lists out the dividend stocks that I believe to be undervalued.

This is the end result of 100’s of hours of research every month.

It’s time to dive in.

1. 📊 S&P Global (SPGI)

S&P Global has had some characteristics of exceptional quality historically:

Approximately 96% of S&P Global’s revenue is recurring in nature

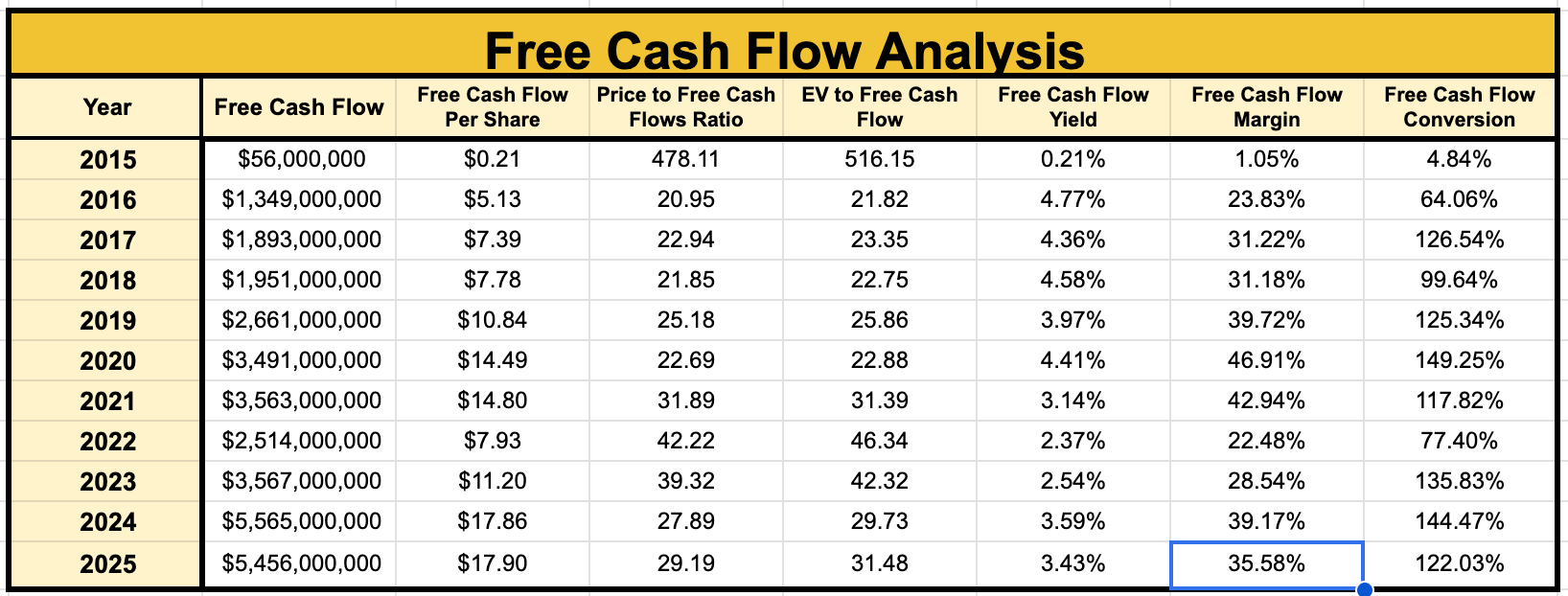

free cash flow margin recently reached roughly 35.6%

Free cash flow per share has also compounded at approximately 16% annually over the past five years

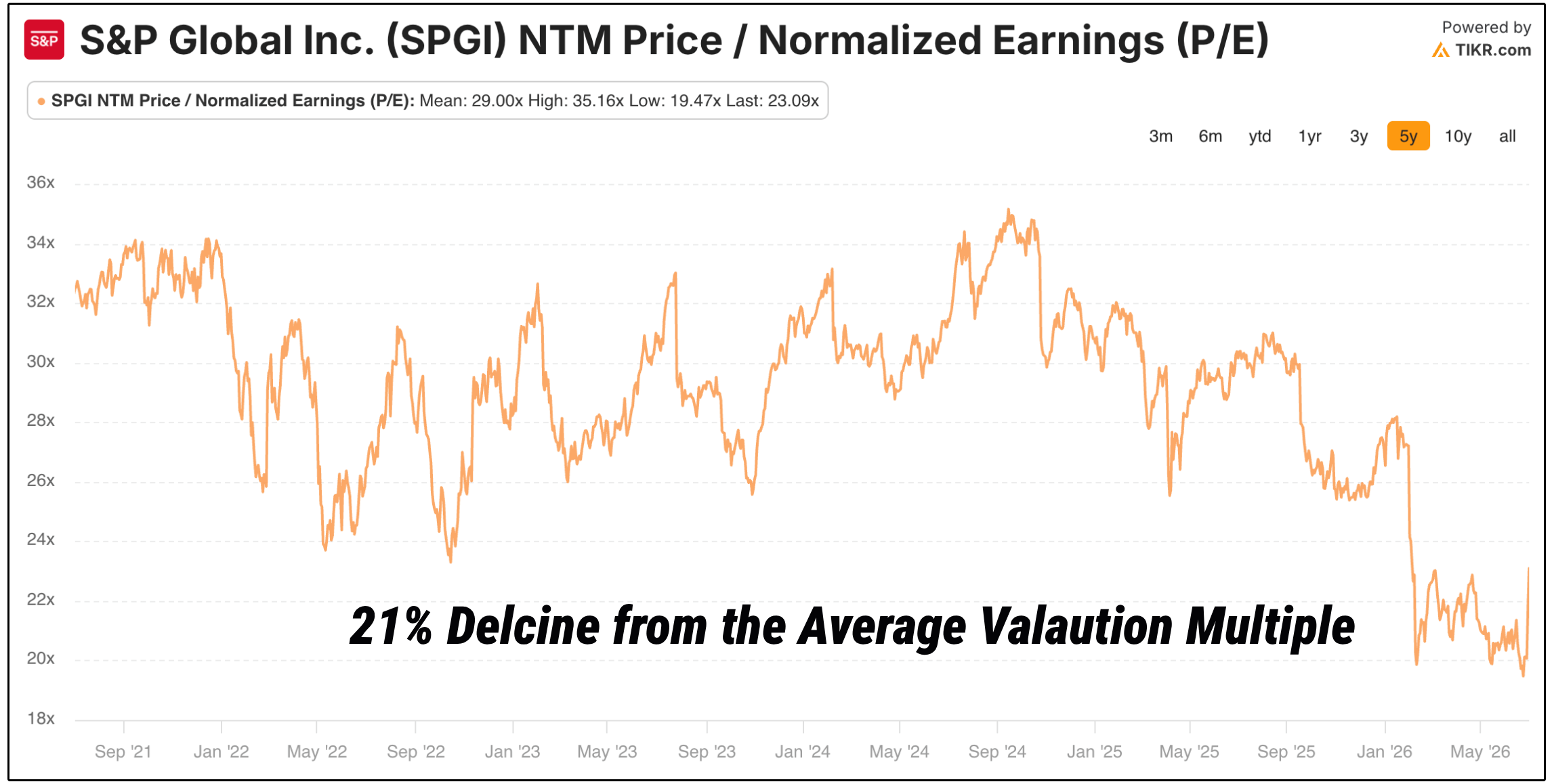

However, the company is down nearly 16% year to date.

This is solely due to a decline in the valuation multiple.

S&P Global is currently trading at a P/E multiple of 23x, which is 21% below their historic average multiple.

But a few things have changed, even in just the last few weeks.

SPGI just completed the separation of their mobility business segment a few days ago.

This is incredibly important in terms of valuation for SPGI.

Why?

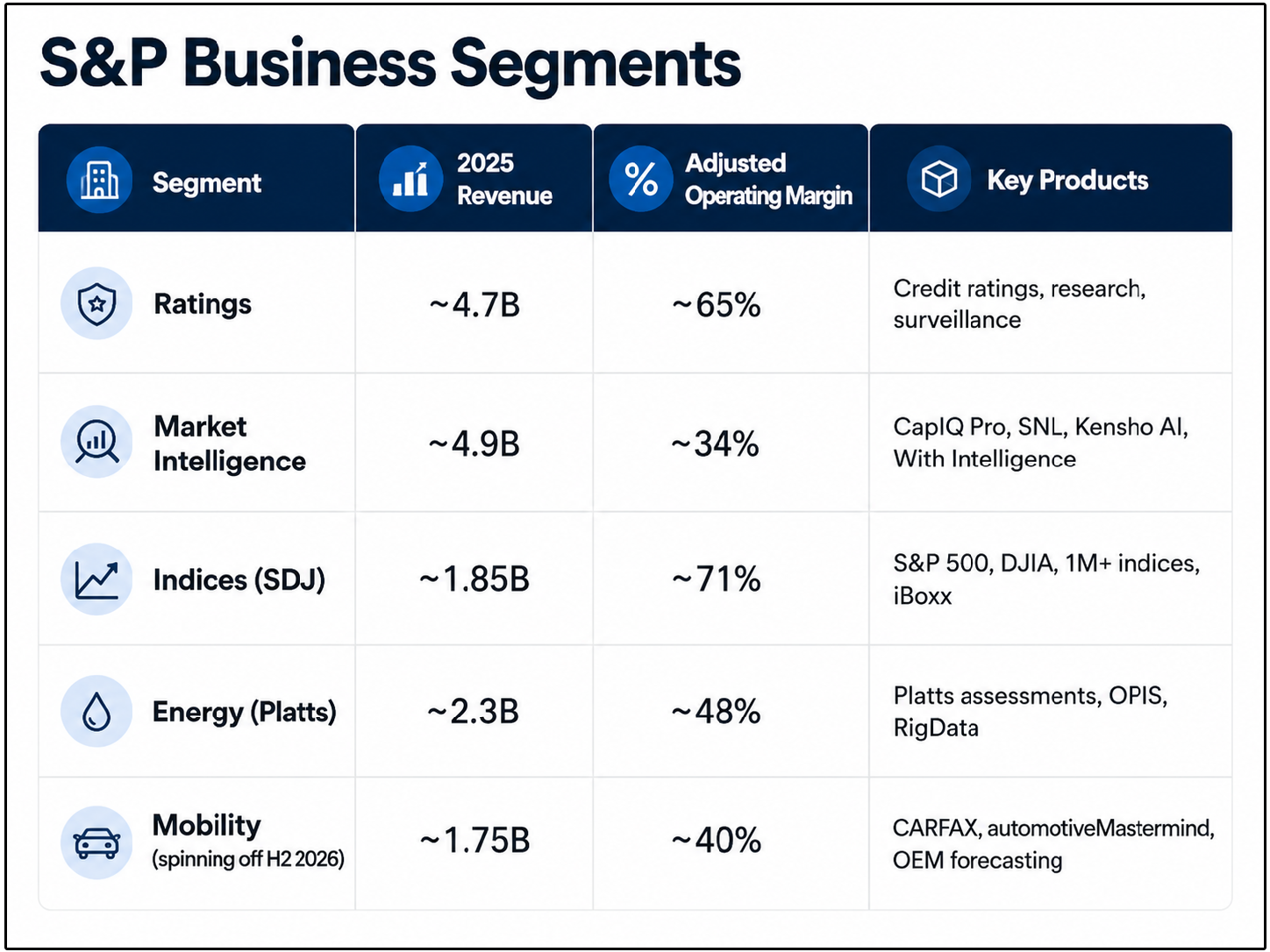

Because SPGI contains business segments of vastly different quality.

Its ratings, indices, commodity benchmarks, and proprietary data operations regularly produce operating margins above 50%, while growing at strong rates.

However, the company has been valued more like its slower-growing Mobility division, which owns businesses such as CARFAX and automotiveMastermind and generates margins closer to 40%.

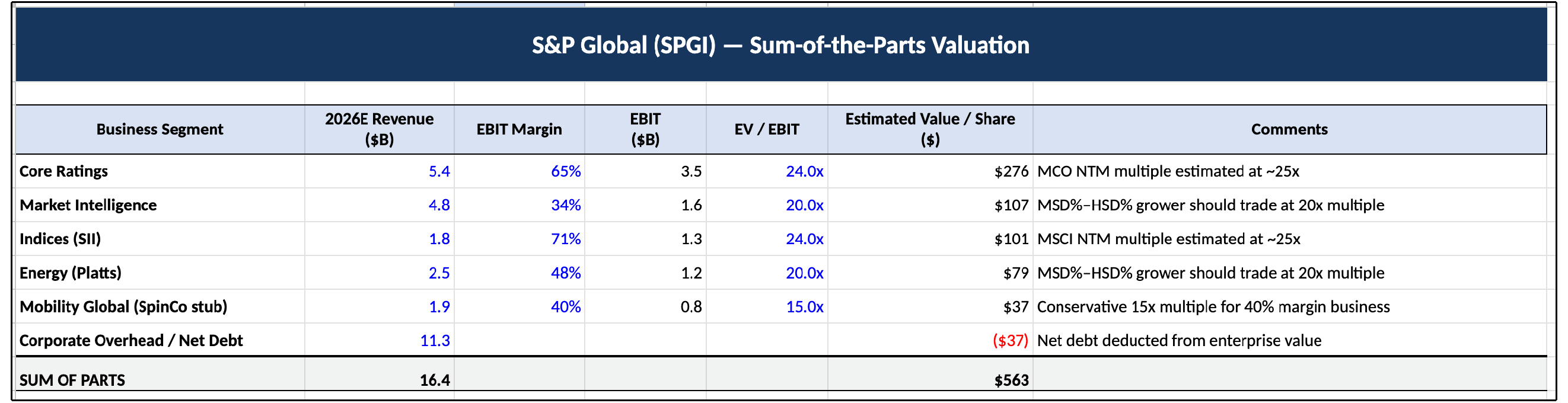

This is where a sum-of-the-parts valuation becomes useful.

Instead of applying one multiple to the entire company, each segment can be valued based on its own margins, competitive position, and comparable businesses.

The ratings division can be compared with Moody’s, while the index business can be compared with MSCI.

Both peers typically receive premium valuation multiples because of their recurring revenue, regulatory advantages, and high margins.

Applying appropriate segment-level multiples and subtracting net debt results in an estimated value of approximately $563 per SPGI share.

This would imply 28% upside from current prices.

The market is currently assigning too little value to the company’s highest-quality assets.

With Mobility trading independently as MBGL, the remaining SPGI business will consist primarily of higher-margin, less cyclical operations.

If the core company receives a valuation closer to Moody’s, the remaining entity alone could be worth approximately $500–$550 per share, before including the value of Mobility.

This dividend king is trading at an attractive value.

2. 🎰 VICI Properties (VICI)

Here’s your fun fact for the day:

REITs and Gold have both outperformed U.S. Stocks since the year 2000.

Of course this is primarily driven by the disaster ‘lost decade’ of the 2000s for equities.

However, the point remains the same:

Investors who view REITs as sub optimal investments are often plagued by recency bias.

VICI Properties has become one of the most compelling opportunities in the REIT market.

The REIT is currently yielding 6.62% and is well covered by it’s growing AFFO.

VICI owns some of the most recognizable gaming and entertainment properties in the world, including Caesars Palace and the Venetian.

It operates primarily through triple-net leases, meaning its tenants are responsible for property taxes, insurance, maintenance, and operating expenses.

These leases also include contractual rent escalators, providing VICI with predictable and gradually growing cash flow.

The company has collected 100% of its rent for years, including throughout the pandemic.

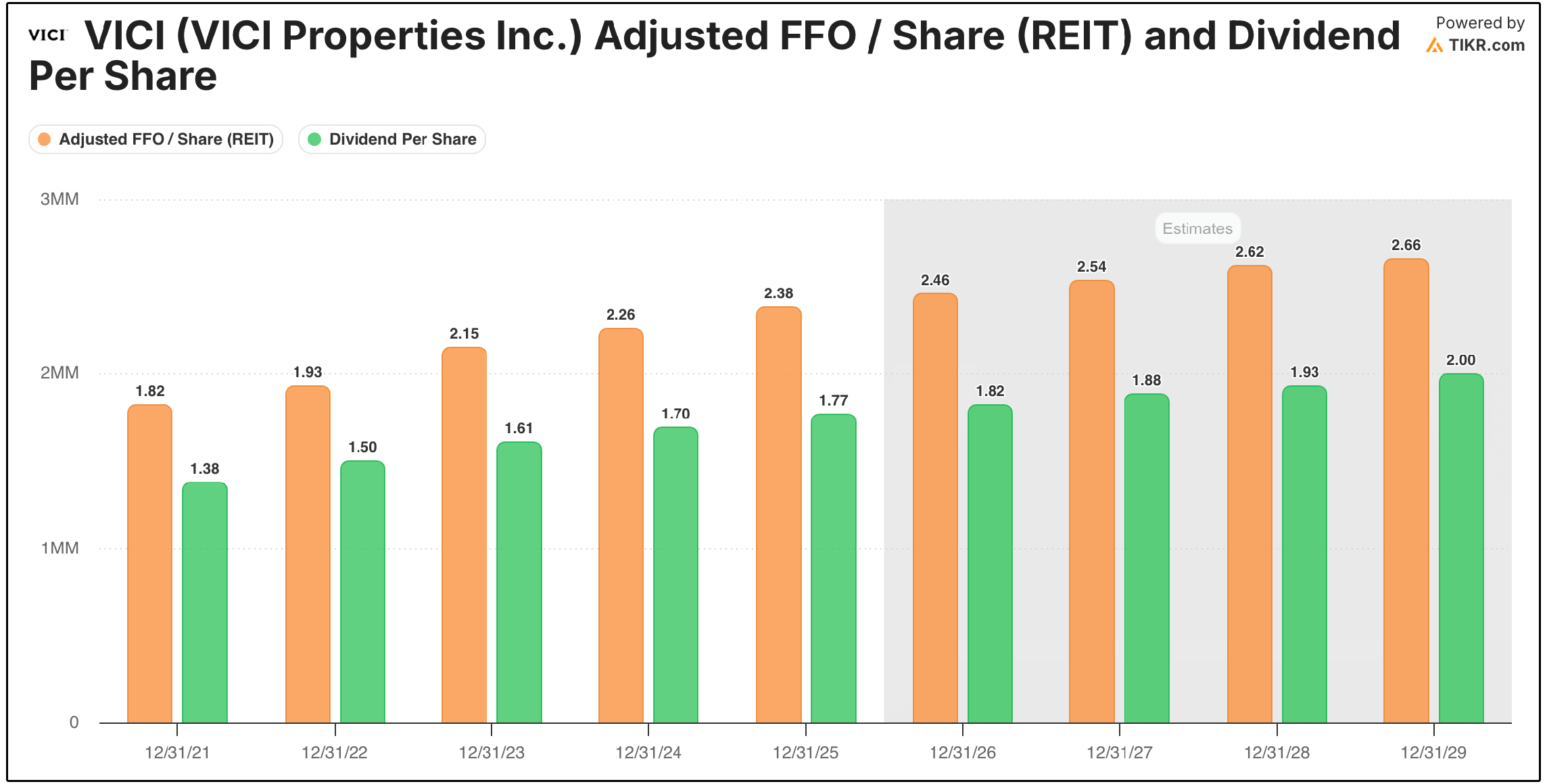

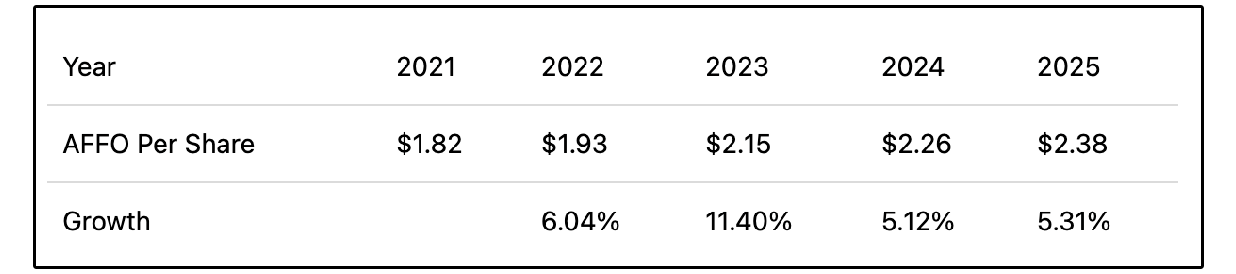

AFFO per share increased from $1.82 in 2021 to $2.38 in 2025, while the company also paid investors an average dividend yield near 5.5% during 2025.

This combination produced double-digit operational returns, even though the declining valuation multiple prevented those results from translating into strong share-price performance.

Today, VICI trades at approximately 10.98 times AFFO, its lowest valuation since the 2020 market crash and roughly 22% below its five-year average.

At the same time, its dividend yield has climbed to approximately 6.6%.

The market’s primary concern is weakening performance among certain casino tenants.

Las Vegas visitation declined sharply in 2025, while some regional Caesars properties experienced lower rent coverage due to increased competition.

However, neither issue has prevented VICI from collecting the rent it is owed.

VICI is also protected by long-term master leases, many of which have approximately 40 years remaining.

These agreements prevent tenants from abandoning weaker properties while retaining stronger assets under the same lease.

Despite the negative sentiment, VICI recently reported 4.5% AFFO-per-share growth and raised its 2026 guidance.

The company maintains an investment-grade credit rating, operates within its targeted leverage range, and has an AFFO payout ratio of approximately 74%, providing comfortable dividend coverage.

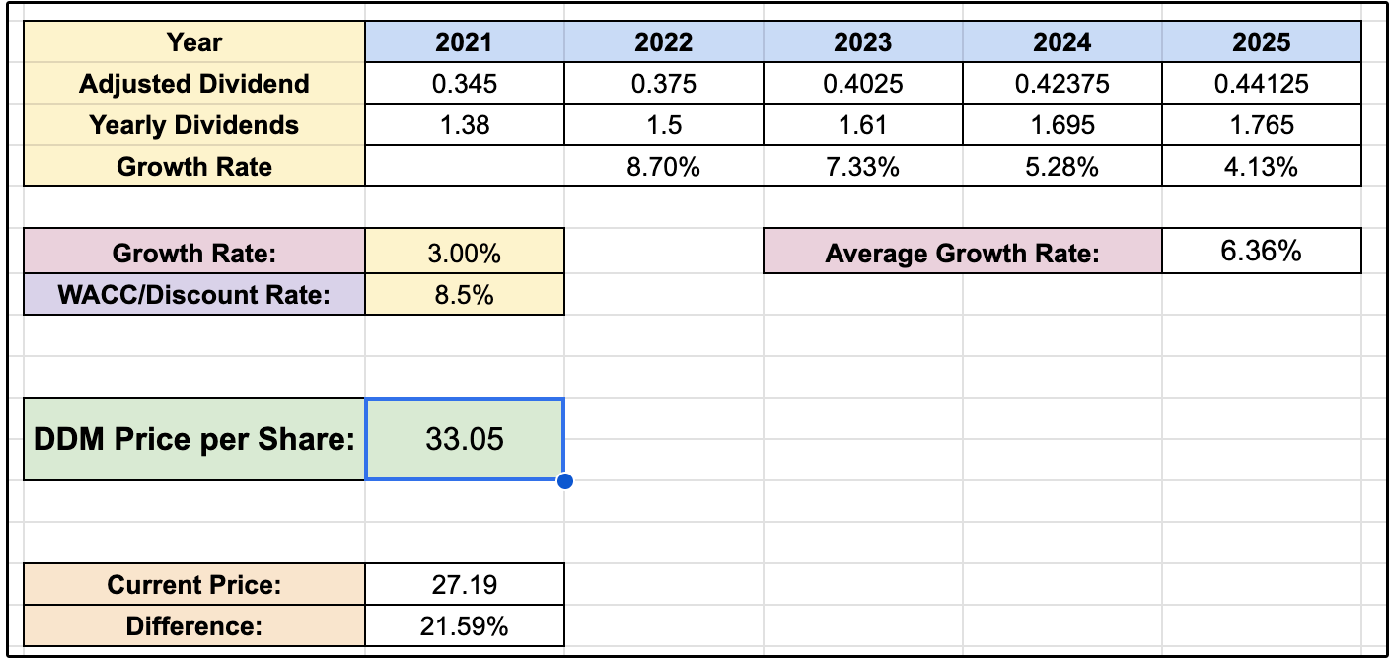

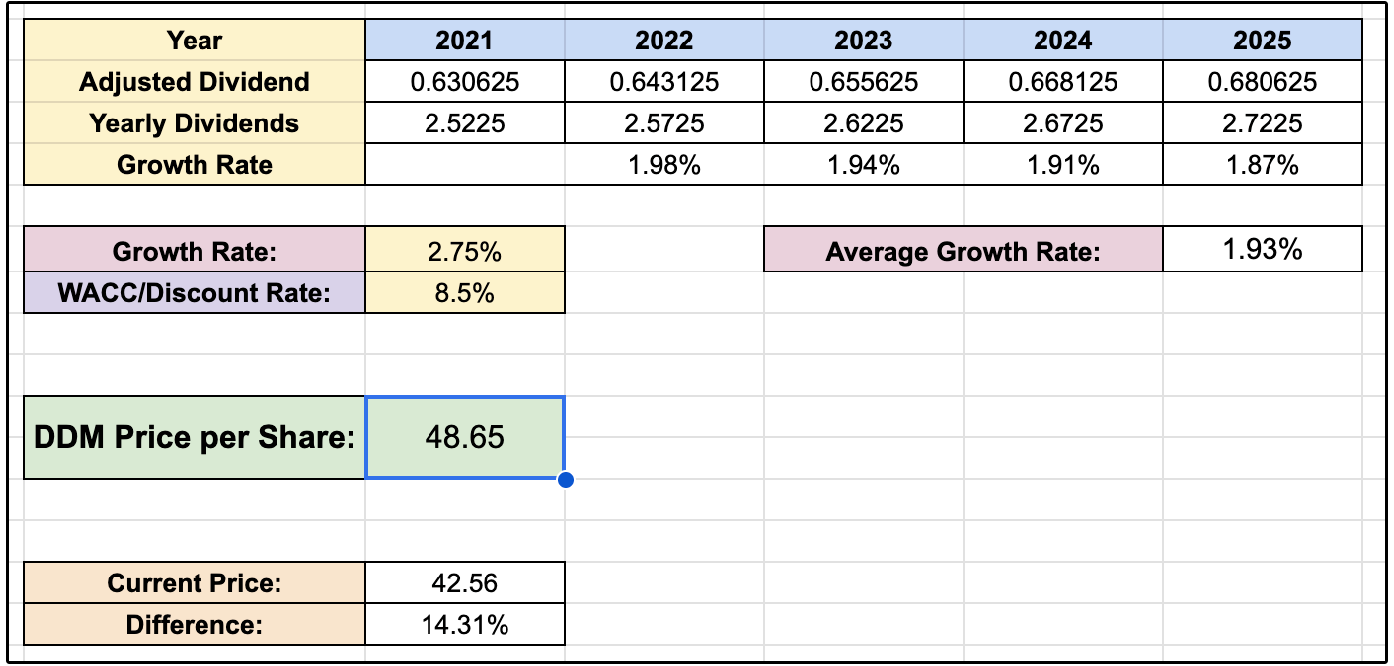

Assuming dividend growth of only 3%, a dividend discount model produces an estimated intrinsic value of approximately $33 per share.

That suggests meaningful upside of around 22%, combined with a starting yield of around 6.6%.

Higher interest rates could continue weighing on VICI’s valuation in the short term.

However, the underlying business continues to perform considerably better than the share price suggests.

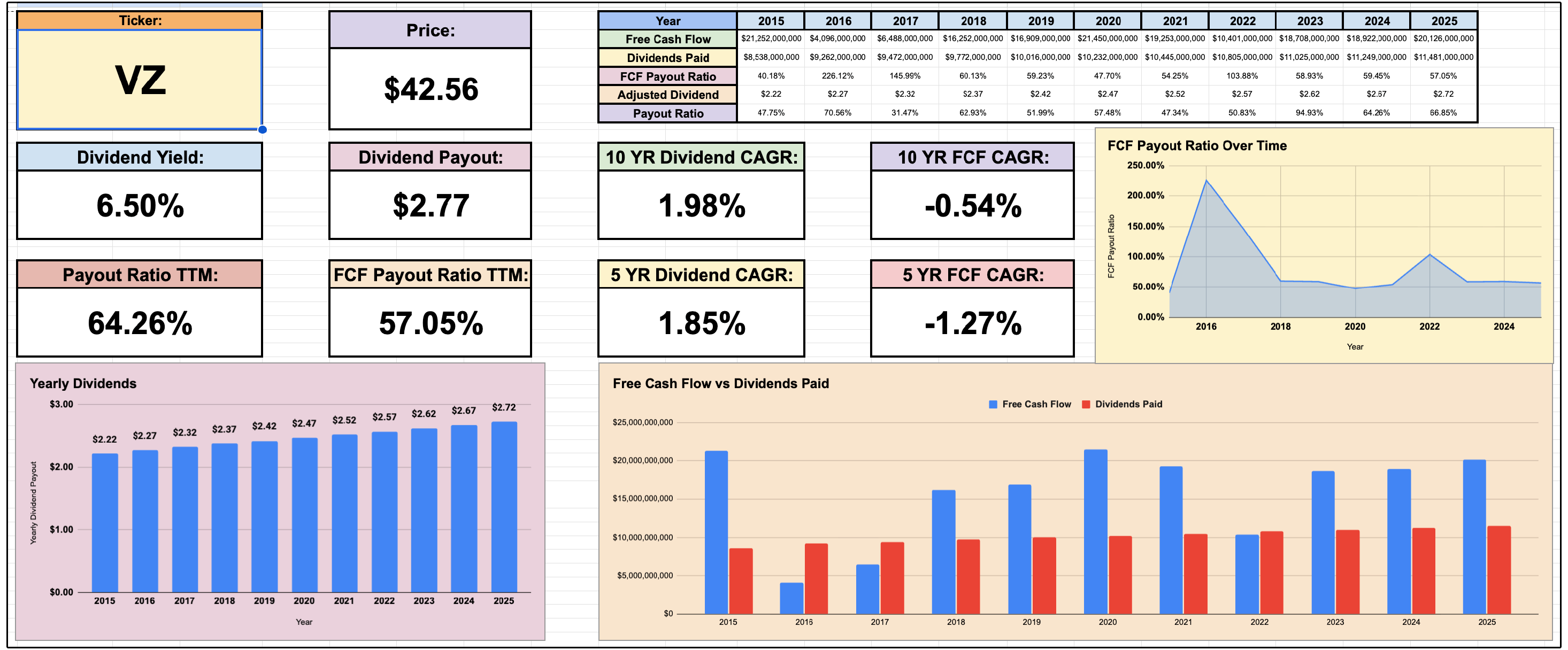

3. 📡 Verizon Communications (VZ)

Verizon often gets overlooked considering it’s history of slow earnings growth.

It’s certainly not a dividend growth play, but at certain points has offered a high yield with upside as well.

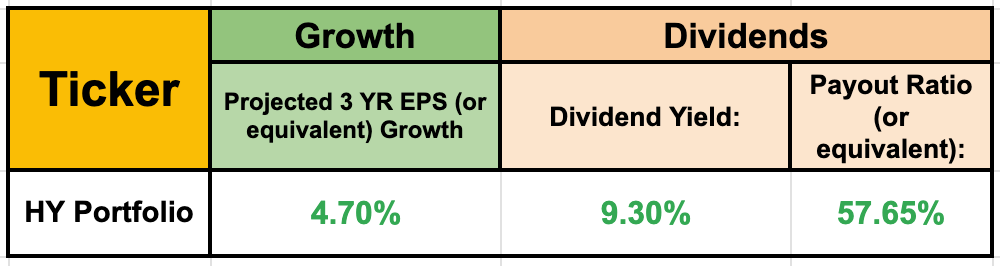

Those are the type of high yield plays we look for when adding to our High Yield Portfolio at Dividendology.com-

Which is currently outperforming the market while yielding 9.3%!

Verizon currently offers a combination of a high starting yield, improving free cash flow, and the potential for earnings growth to accelerate over the next several years.

The company is unlikely to deliver explosive revenue growth, but investors may not need much growth to generate attractive returns from today’s valuation.

Verizon currently offers a dividend yield of approximately 6.5%, with an annualized dividend of $2.77 per share.

Its free cash flow payout ratio sits at just 57%, meaning the dividend remains very well covered, especially for a high yield stock.

But here’s what most investors are currently missing:

Analysts expect Verizon’s earnings growth to accelerate gradually.

EPS is projected to reach $4.94 in 2026, $5.27 in 2027, $5.77 in 2028, and $6.41 in 2029.

That translates into expected annual growth of approximately 5% in 2026, rising to more than 11% by 2029.

Several factors are driving this acceleration:

Verizon has moved beyond the most capital-intensive stage of its 5G network buildout, allowing more operating cash flow to become free cash flow. The company can now focus on monetizing its network through wireless pricing, premium plans, fixed wireless, and fiber broadband rather than continually increasing capital expenditures.

The Frontier acquisition should also expand Verizon’s fiber footprint and create opportunities for customer growth, lower churn, and cost synergies. Integration expenses and additional debt may limit the immediate benefit, but analysts appear to expect the acquisition to become more accretive over time.

Even modest revenue growth can translate into stronger EPS growth if Verizon improves margins, reduces interest expense, and repurchases shares.

Even if VZ only grows their dividend at 2.75% moving forward, which should be easily attainable if EPS growth is truly anywhere close to projected-

Then VZ easily has over 14% upside at current prices, combined with their starting yield of 6.5%.

Now, let’s jump into this month’s full list.