⚠️ The 4% Rule Will Destroy You

Why the 4% Rule is more Dangerous than Ever 🚨

Have you heard of the 4% rule?

The idea is simple:

In year one of retirement, withdraw 4% of your portfolio. Each year after, withdraw the same dollar amount, adjusted up for inflation. Do that, and history says your money should last at least 30 years.

The 4% rule has become the most popular retirement strategy over the last three decades.

But there is a MAJOR problem with the 4% rule…

🚨 The 4% Rule is More Dangerous Than Ever

On a $1,000,000 portfolio, the 4% rule generates $40,000 in year one, then $41,200 in year two if inflation runs 3%, and so on.

The trinity study found this strategy worked more than 95% of the time on a 30-year retirement horizon.

That’s where the “95% success rate” you hear parroted everywhere comes from.

But here’s where things get interesting.

The 95% success rate is a historical average.

It blends together retirees who started in cheap markets with retirees who started in expensive ones.

And when you pull those two groups apart, the story changes dramatically.

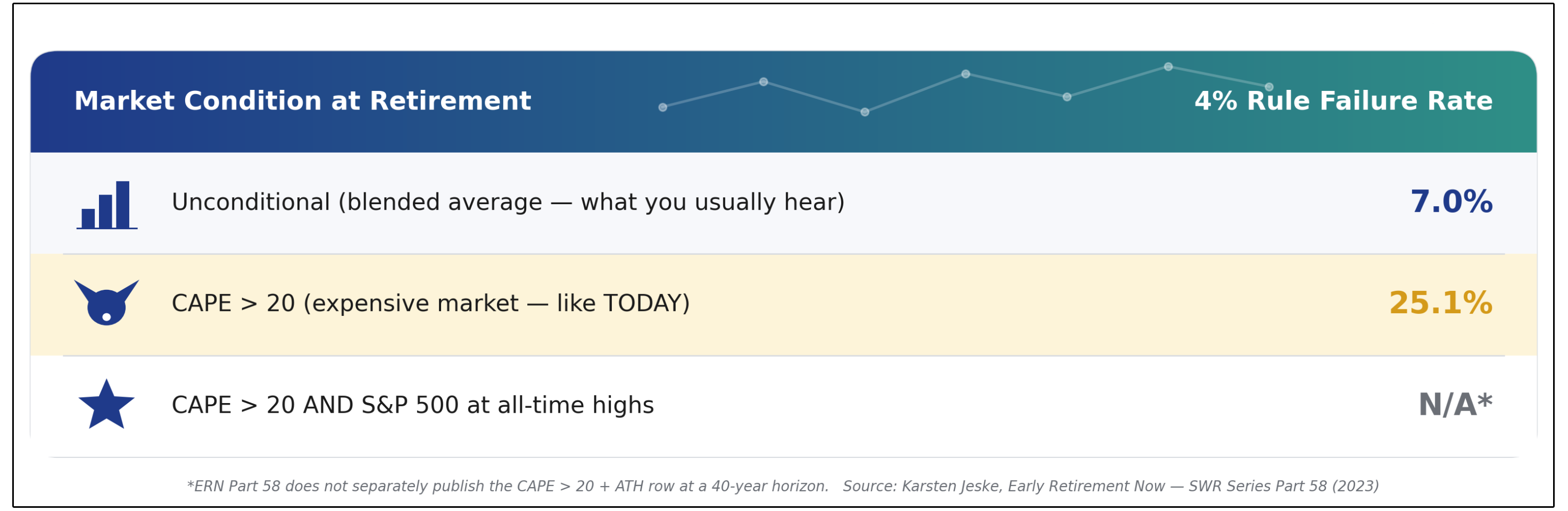

Here’s the uncomfortable truth: every single historical failure of the 4% rule happened when stocks were expensive at the start of retirement.

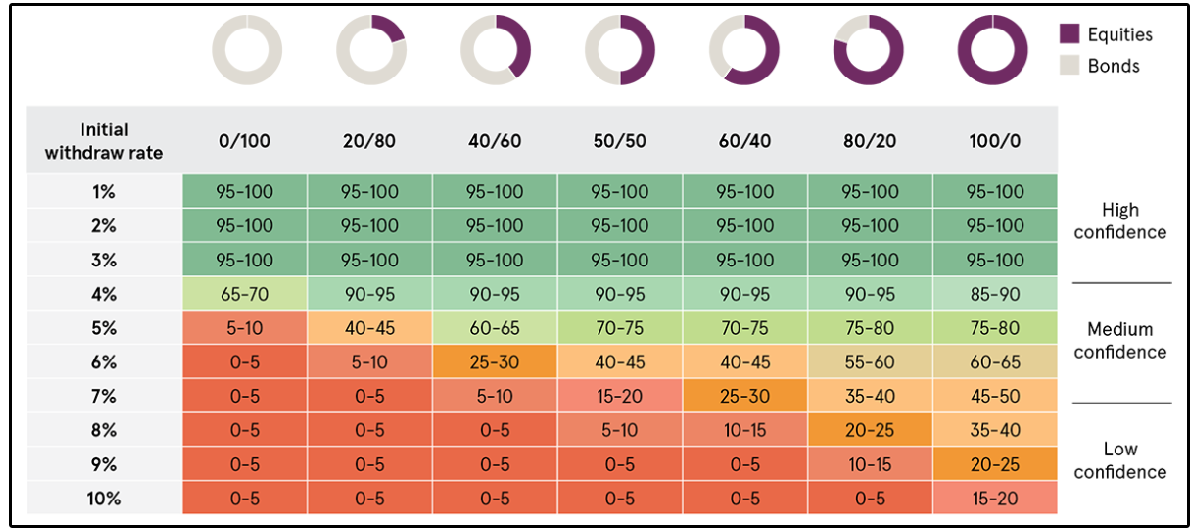

📊 What The Research Actually Shows

What does the success rate for the 4% rule look like when also accounting for valuation?

When the CAPE ratio is above 20, the historical failure rate jumps all the way to above 25%!

As a reminder, the CAPE ratio (Cyclically Adjusted Price-to-Earnings) is one of the most widely used ways to measure how expensive the stock market is.

Instead of looking at just one year of earnings like a normal P/E ratio, CAPE looks at the average of the past 10 years of earnings, adjusted for inflation.

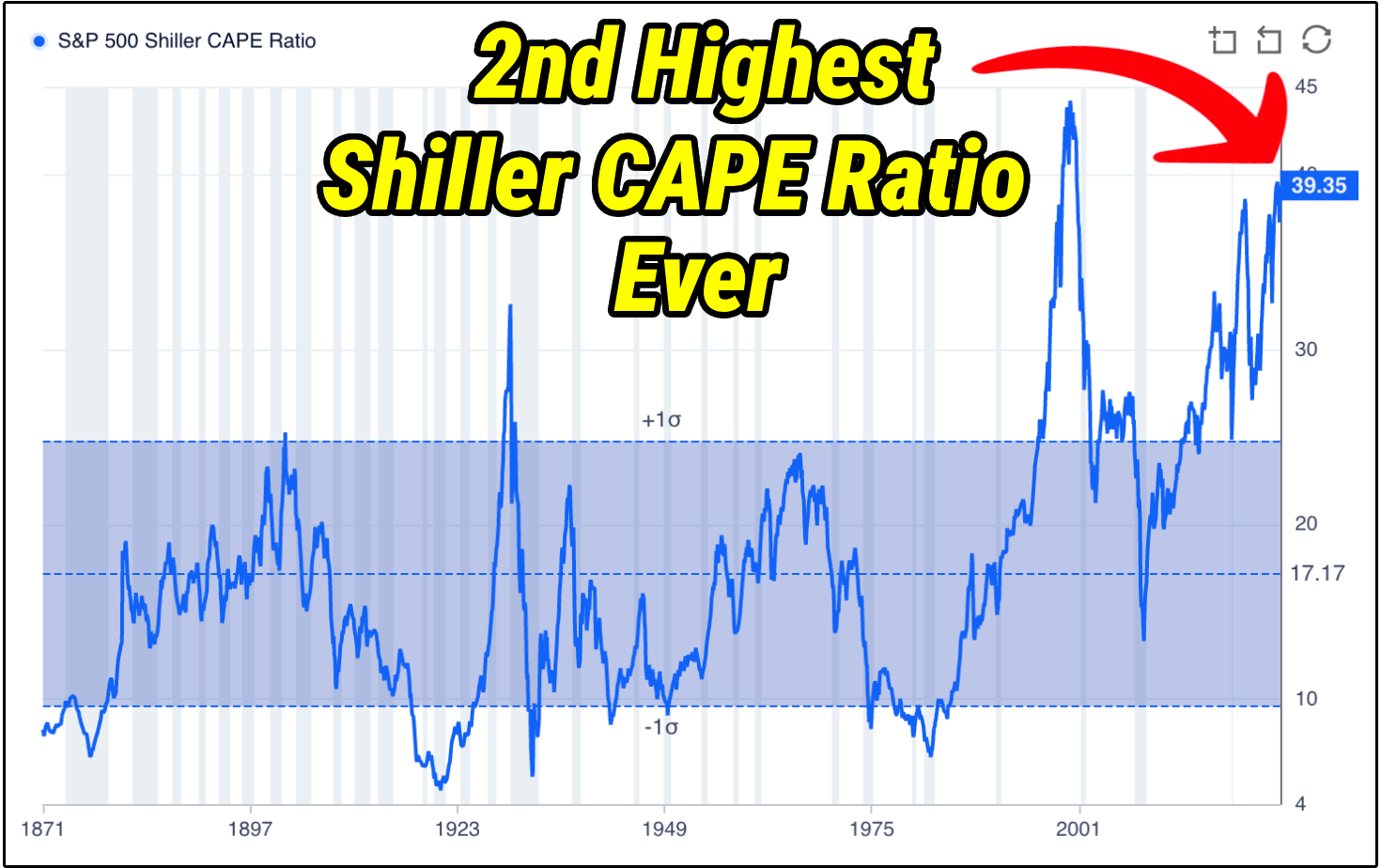

So where is the CAPE ratio today?

Sitting at 39.95.

The CAPE ratio is the second highest it has ever been, second only to the dot com bubble.

In other words, we are sitting in exactly the valuation range where the 4% rule has historically broken down.

We don’t even have enough historical data to know what the success rate of the 4% rule would be in this valuation range.

However, as I’ve pointed out before, this isn’t the only issue with the 4% rule.

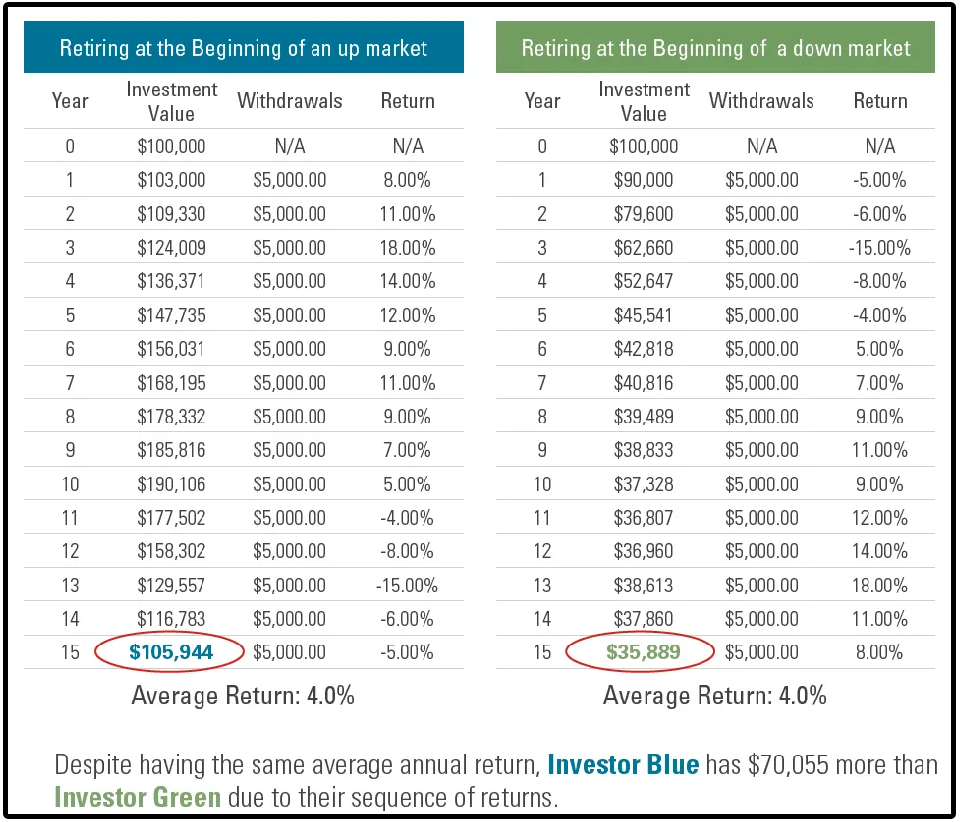

🎲 Sequence Risk

Sequence risk refers to the danger of experiencing poor investment returns early in retirement, when an investor is making withdrawals.

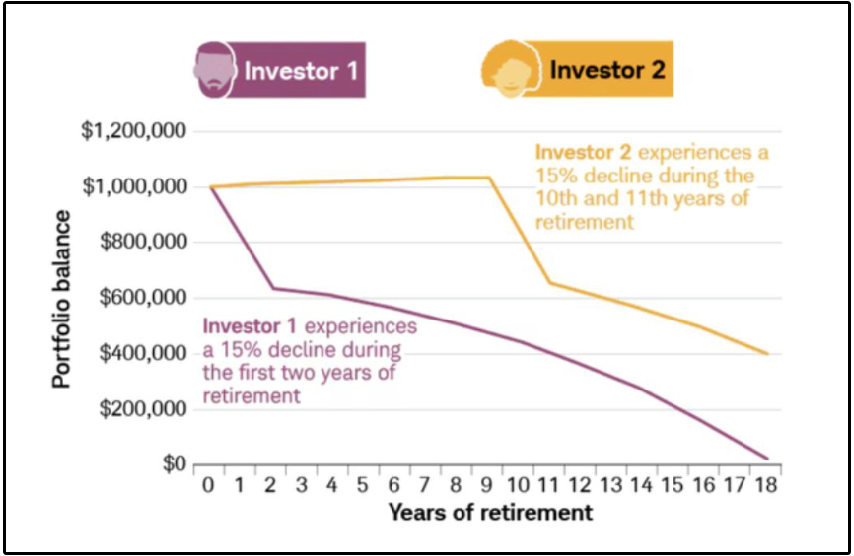

Look at the example pictured below.

In the above example, both investors started with $100,000, and had an average annual return of 4% over a 15 year time period.

But here is what each finished with:

Investor 1: $105,944

Investor 2: $35,889

Why such a difference?

Because the sequence of returns you get plays a major role in the potential longevity of your portfolio.

The 4% rule killed many investors ability to retire in 2020, 2022, and essentially for the entire decade of the 2000s.

Consider someone who retired in 1966 with a $1M portfolio (60% bonds, 40% stocks) and pulled 4% per year, inflation-adjusted.

From 1966 to 2000, the portfolio actually averaged a 9.5% annual return.

Sounds great, right?

They ran out of money in retirement.

Why?

The late 1960s and 1970s delivered terrible real returns and brutal inflation right at the start of their retirement.

By the time the roaring ‘80s and ‘90s arrived, there wasn’t enough portfolio left to benefit from the rebound.

💰The Solution: Live off the Dividends

The 4% rule is much more dangerous than the average investor realizes, primarily due to the two reasons just mentioned:

Current Valuation

Sequence Risk

While obviously the valuation in the future can come down to more reasonable levels, sequence risk still remains a tremendous risk for investors.

Here’s the core insight that the 4% rule ignores entirely-

You don’t have to sell anything if your portfolio is paying you.

Sequence risk only exists because the 4% rule forces you to sell shares in down markets to fund your withdrawal.

Every share you liquidate at a low price is a share that can’t recover when the market rebounds.

If you retired at the peak of the dot-com bubble in early 2000 holding TXN, you watched the stock crash more than 80%-

And it took 17 years for the share price to reclaim its high!

Under the 4% rule, you’d have been forced to sell shares at deeply depressed prices every year just to fund your withdrawals, locking in permanent losses during the worst possible stretch.

But here’s what the price chart doesn’t show.

Over that same “lost” 17 years, Texas Instruments:

Raised its dividend every single year, through the dot-com crash, 2008 financial crisis, and 2020 COVID crash

Grew the annual dividend roughly 2,388% (Yes, I typed that right)

A retiree living off TXN’s dividends in 2000 was able to continue living off their dividends.

In fact, their paycheck kept growing the entire time.

They never had to sell a single share at the bottom.

And by the time the stock finally recovered, their income stream was many times larger than when they started.

That is the difference between a 4% rule strategy and a dividend strategy.

The dividend strategy forces you to focus on the underlying fundamentals of the company, to assess their ability to continue paying dividends.

If you can learn to do that, you will be set for life.

Dividendology

This is definitely a better strategy than selling off equities in your portfolio. However, if there was a large draw-down like the dot-com bubble and then a long period where indexes also lag long term average rates of returns, the leverage strategy could become problematic and, I'm sure would be emotionally difficult.

Bookmarking this to reread later.