🔥The Tech & Software Apocalypse is Here

And How to Use It to Grow Your Dividend Income! 💸

If you have a heavy allocation to software stocks in your portfolio-

Then you’ve likely seen a large drop in your portfolio over the last few months.

But it isn’t just software stocks selling off.

Many names across tech have also pulled back meaningfully over the past ~2 months, even after strong long-term runs.

The message the market is sending is actually quite clear:

AI will be the downfall of software stocks

Tech companies are overspending on capex

Whether or not you agree with that narrative, that is how the market is currently pricing the sector.

On top of this, the shift toward AI is introducing meaningful risks that the market has not fully priced in yet, and investors need to be aware of them.

However, this is creating some incredible opportunities, particularly from a dividend growth investor perspective.

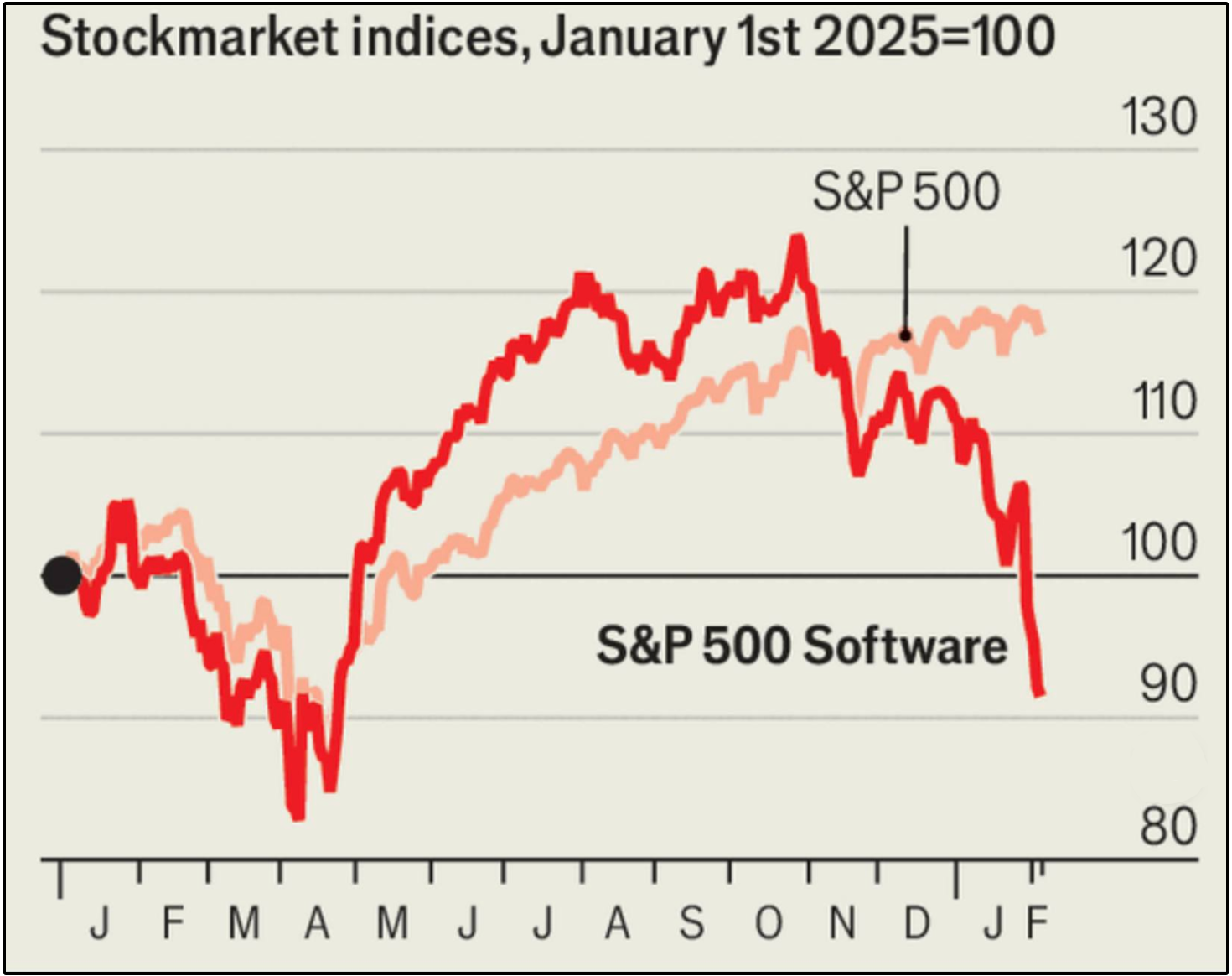

🪫 Are Software Stocks Dead?

The S&P 500 is in the green year to date, but that does not paint the picture for what is actually going on.

We are currently being carried by 4 sectors that are up double digits:

Energy

Materials

Consumer Staples

Industrials

Despite this, the S&P 500 is only up 1.7%.

Why?

Because tech makes up the largest portion of the S&P 500, and software in particular has been hammered.

Whenever we have an entire sector selling off as a whole, it typically means one thing:

The market is not intelligently selling off equities.

What do I mean by this?

Not all stocks (even stocks in the same sector) are created equally.

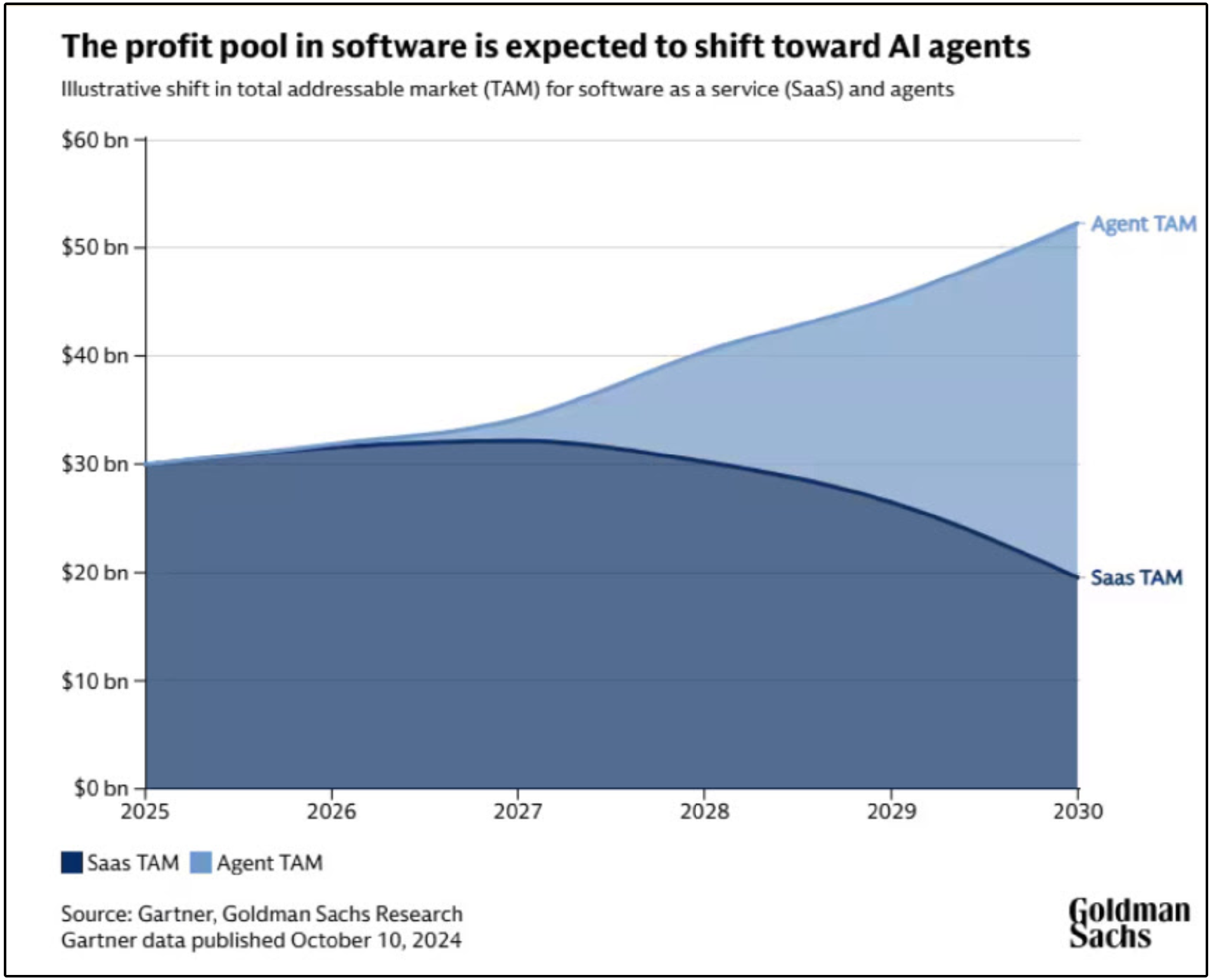

In other words, this sell-off may be justified for some software stocks as the total addressable market is being reduced by AI-

But for others, it certainly is not.

Let’s look at an obvious example.

Chegg.

Chegg is a software-based education platform that built its business around helping students complete homework, study for exams, and access step-by-step solutions.

For years, this was a great business model.

Recurring subscriptions

High margins

A clear value proposition

But the problem?

That value proposition has now been directly challenged by AI.

When a student can open an AI tool and get an instant explanation, often for free, the core reason to pay for Chegg starts to disappear.

This is what true disruption looks like.

In cases like this, the market is absolutely right to be ruthless.

It’s being sold off because the long-term cash flow outlook has fundamentally changed.

Now let’s look at the other side of the spectrum.

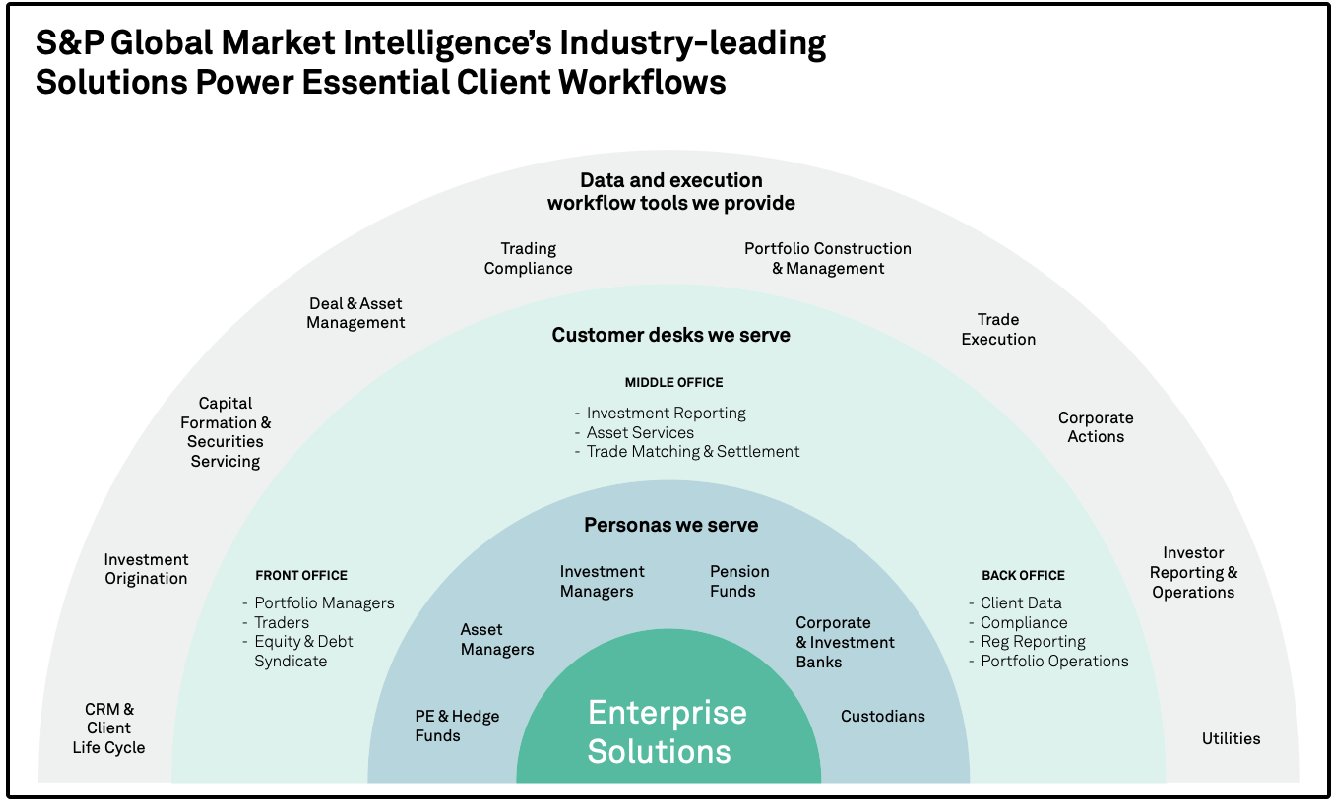

S&P Global (SPGI).

At a glance, SPGI gets lumped into the same bucket as “software and data” companies.

But economically, it couldn’t be more different than a company like Chegg.

Chegg’s product delivers answers.

SPGI’s products deliver infrastructure.

SPGI sits at the center of the global financial system:

Credit ratings that determine borrowing costs for governments and corporations

Indices that underpin trillions of dollars of passive investment flows

Market and commodity data embedded directly into institutional decision-making

An AI model can explain a concept to a student and eliminate the need for Chegg.

But an AI model cannot invent decades of proprietary financial data.

🧩 What About Capex Spending?

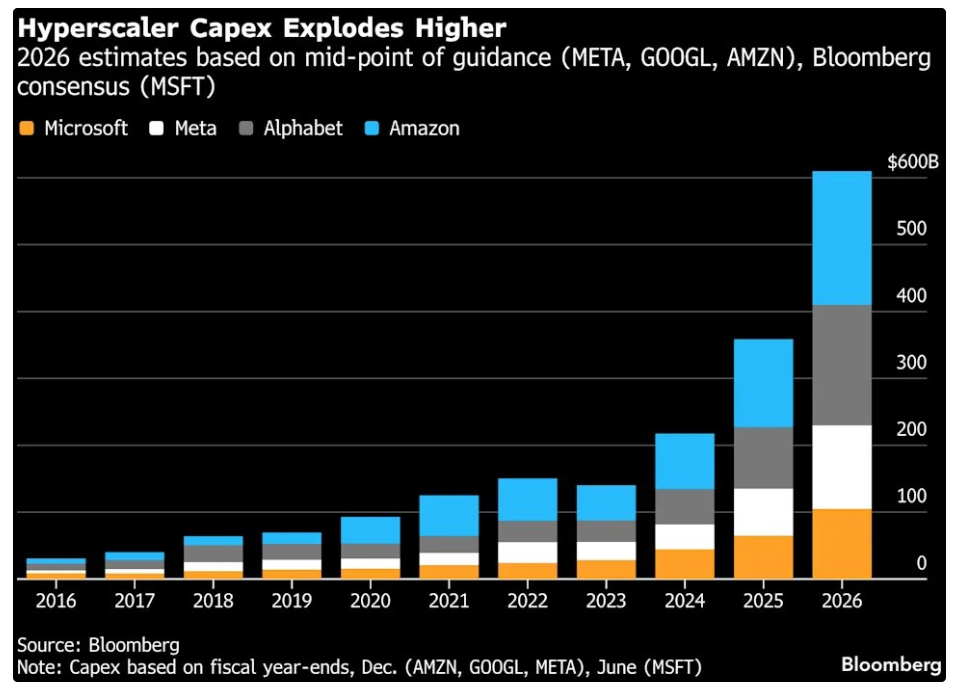

Capex spending from Big Tech has certainly risen to absurd levels.

Capex spending from META, AMZN, GOOG, & MSFT has nearly 3x’d in just the last 2 years.

And this is where the conversation around “tech risk” starts to shift from valuation risk to something potentially more important for the long term:

Capital allocation risk.

For most of the past decade, large-cap software and tech companies were incredible businesses for one simple reason:

They were cash machines with high margins, low capital intensity, and exceptional ROIC, which translated to rapidly growing free cash flow.

That free cash flow could be used to:

Buy back shares

Strengthen balance sheets

Make disciplined acquisitions

Or increase dividend payments

But the AI arms race is changing that dynamic.

Rapidly.

Many of these companies are now pouring hundreds of billions of dollars into data centers, chips, energy infrastructure, and networking equipment.

In other words…

They are transforming from asset-light software businesses into capital-intensive infrastructure businesses.

This is why investors can no longer just look at how much a company is spending on capex.

They must analyze the quality of that capex, and its ability to justify itself with a clear, predictable return on invested capital over time.

With this massive capex spending, there will be winners, and there will be losers.

🎯 Stock Pickers Market

For years, passive investing worked beautifully.

Why?

Because capital-light tech businesses compounded earnings at high rates, margins expanded, and multiples followed.

You didn’t need to pick winners, you just needed exposure.

That environment is changing.

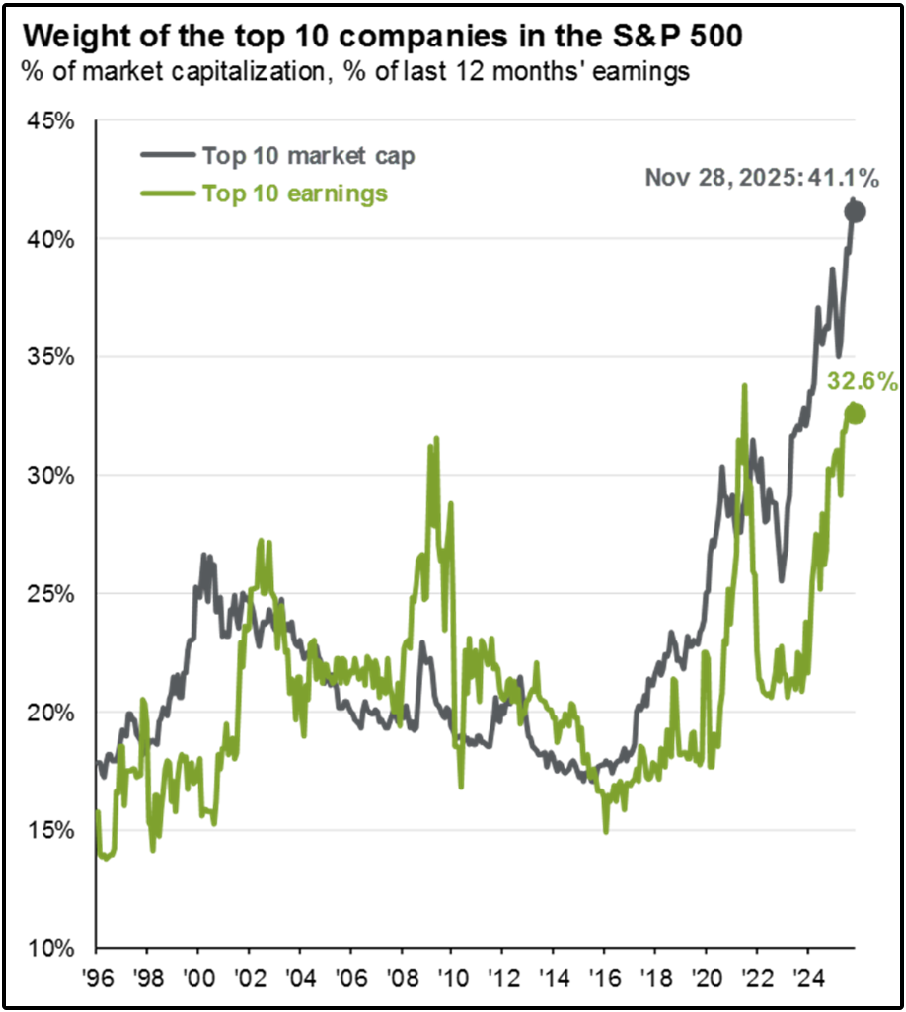

Today, when you buy an index like the S&P 500, you are making a very specific bet:

Nearly 40% of your capital is allocated to a handful of hyperscalers

Those hyperscalers are spending aggressively on AI infrastructure

Free cash flow is being compressed by capex

Returns now depend heavily on flawless execution

Passive investing is no longer a neutral bet.

It’s an active bet, disguised as a passive one.

💵 Buy Predictable Businesses

For the dividend growth investor, I certainly still believe tech and many software stocks should have a place in your portfolio-

But you must have the ability to assess things right now like:

How they are threatened by AI

The quality of their capex spending

Their valuation risk

We will continue to take advantage of irrationality in the tech sector as we build our dividend growth portfolio on Dividendology.com.

However, there’s another group of assets quietly benefiting from the market shift that is happening.

Real assets.

REITs, MLPs, infrastructure businesses, and utilities are already designed to operate in capital-intensive environments.

They are built around:

Long-lived assets

Contractual cash flows

Regulated or toll-road-style revenue

Inflation-linked pricing in many cases

And most importantly…

They don’t rely on hope for future monetization.

For example, REITs own tangible assets with contractual lease revenue.

Data centers, industrial facilities, energy infrastructure, housing, these assets are becoming more valuable as AI expands, not less.

And unlike tech stocks, many REITs already price in capital intensity.

Which means their returns depend less on perfect execution and more on steady cash flow.

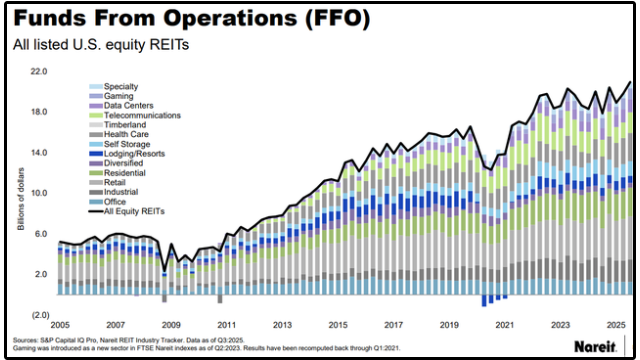

And despite the fact REITs are still trading at historically low valuations, their funds from operations have continued to grow.

MLPs are another interesting option in this market.

MLPs and midstream businesses operate like toll roads.

Volumes flow through pipelines and infrastructure whether commodity prices are volatile or steady.

They have:

Long-term contracts

Fee-based revenue

Predictable cash generation

These businesses are boring and predictable by design.

It’s why we’ve already added two MLPs to our High Yield Portfolio, both of which are yielding over 8% and growing distributions with healthy dividend coverage.

💰 The Perfect Dividend Growth Scenario

This environment is a gift for dividend growth investors.

Why?

Because volatility does four powerful things:

It pushes prices lower, raising starting yields

We reinvest dividends at better valuations, increasing our future dividend income

Share buybacks are performed at lower valuations, enhancing a company’s ability to pay dividends

It creates mispricings between quality and speculation

All four of these lead to an increase in the speed of the dividend snowball effect, which ultimately determines how soon you can live off dividends.

🚀 Keep Growing Your Income

The tech and software selloff we’re seeing today isn’t random, and it isn’t purely emotional, it’s the market grappling with a real shift in capital allocation, business models, and risk.

Some software companies will come out of this stronger.

Others won’t.

This is no longer a market where passive exposure alone guarantees success.

It’s a market that will reward investors ability to actually buy high quality businesses.

For dividend growth investors, this is an opportunity to take advantage of.

By buying high-quality businesses at lower valuations, and buying ‘AI proof’ assets like REITs and MLPs, and reinvesting income during periods of volatility, you accelerate the dividend snowball in your favor.

We are still in the beginning stages of building out our real money Dividend Growth and High Yield Portfolios.

If you want to get access to the Portfolios and all the features mentioned below, you can do so here:

Check out these resources:

Tickerdata 🚀 (My automated spreadsheets and instant stock data for Google Sheets!)

Interactive Brokers 💰 (My favorite place to buy and sell stocks all around the world!)

Seeking Alpha 🔥 (Research stocks $30 off! + 7 day free trial)

HYSA 📊 (Get Access to the Best High Yield Savings Accounts!)

My portfolio loves it... keep giving me 52 week lows and 30% discounts on 5yr P/E averages!

Or, be in energy and commodities. GSCI/SPX ratio is pretty clear on that.