🔎 The Top 5 High Yield Small Cap REITs

The Market is Overlooking These Opportunities 💎

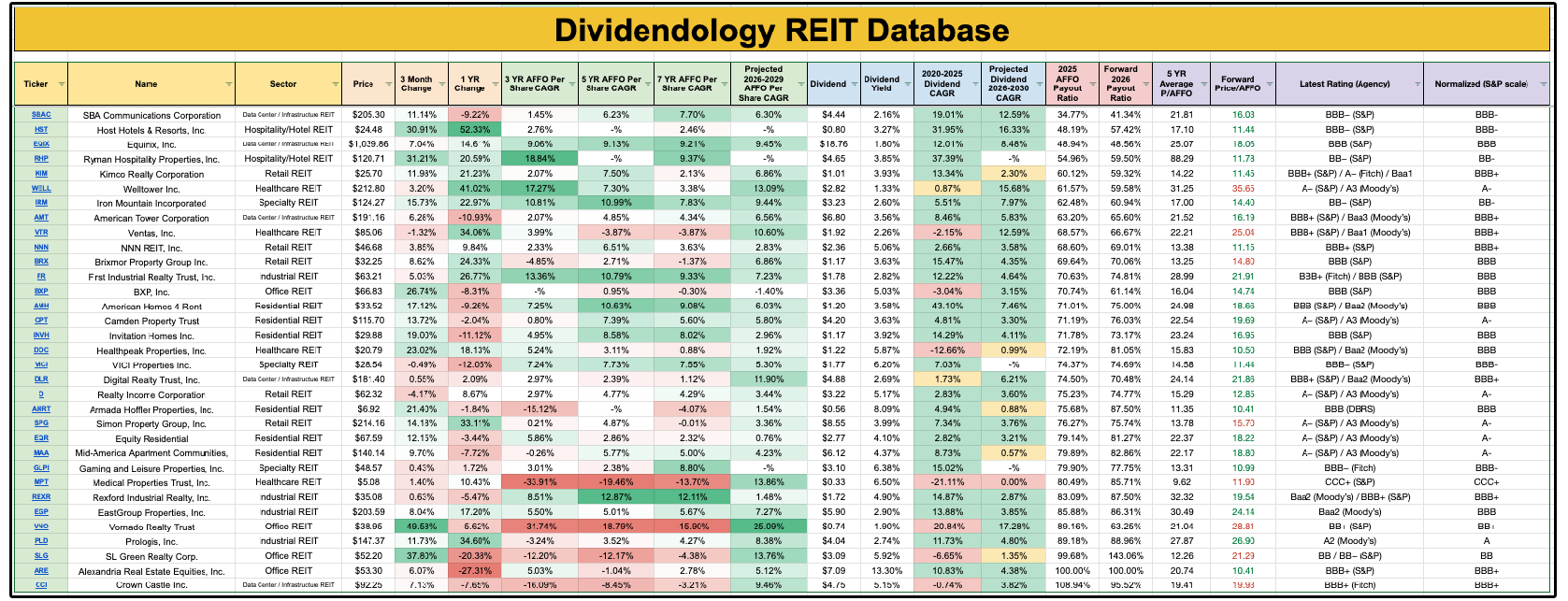

On Wednesday, we reviewed how disconnected current REIT valuations were from their intrinsic value-

And created an investable universe using the Dividendology REIT Database.

Today, we’ll be exploring a potentially much more interesting, subcategory of REITs:

Specialized small cap REITs.

These REITs often have:

Very little analyst coverage

Misunderstood business models

Less institutional ownership

This lack of coverage and institutional ownership often results in valuations getting disconnected from the REITs fundamentals, which also leads to high starting yields.

This is a major advantage for investors willing to do the deep research.

Today, we will be analyzing the Top 5 High Yield Small Cap REIT Opportunities-

As well as one we own in our High Yield Portfolio that yields over 10% with strong dividend coverage.

🧮 REIT Sentiment

Most investors currently write off REITs.

But the reality is this is primarily due to recency bias.

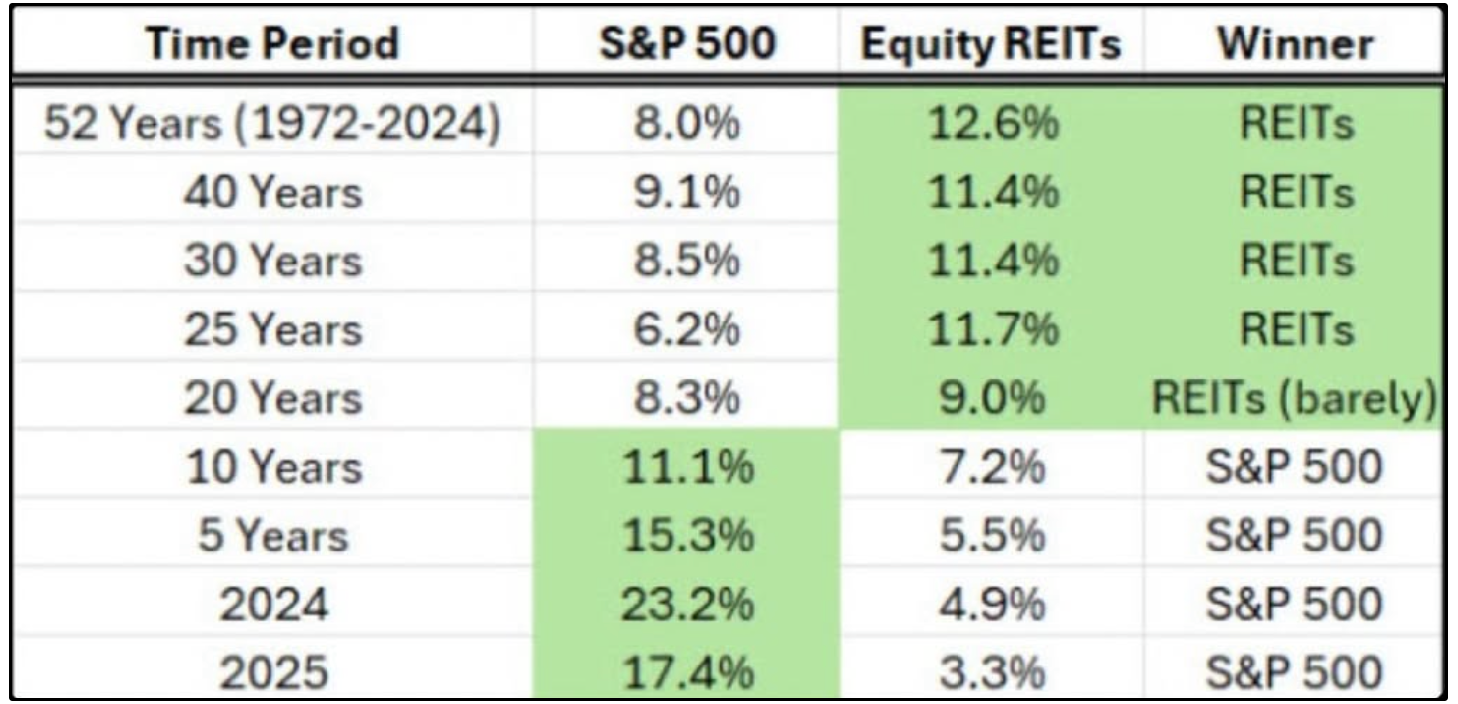

REITs have drastically underperformed the market over the last 5 years-

But historically have provided superior returns to the S&P 500, a fact very few investors are aware of.

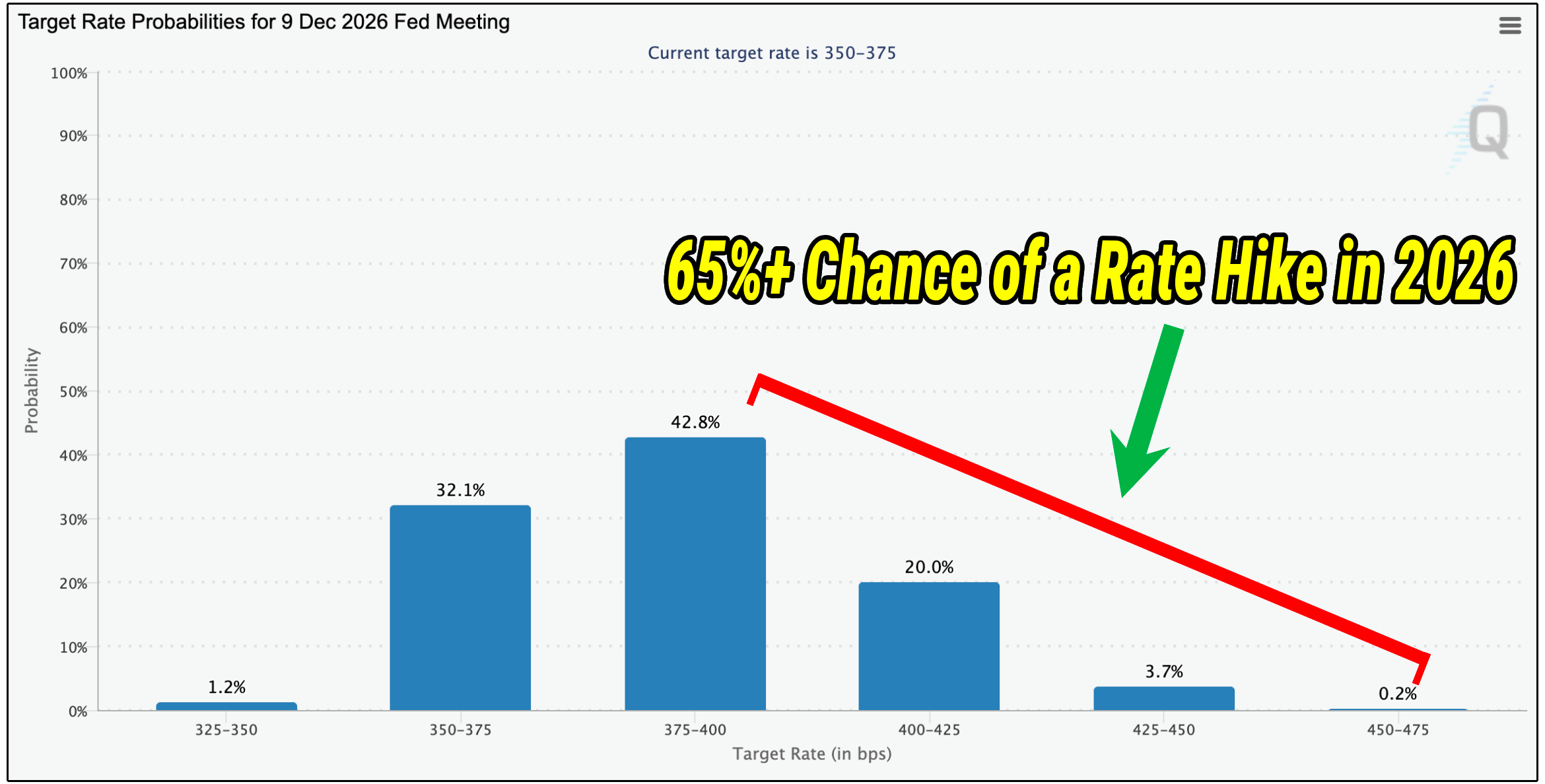

As mentioned on Wednesday, the rate environment REITs operate in plays a major role on future returns.

And the high rate environment over the last few years has not been optimal, and it appears it may stay that way for at least the next year.

But quality REITs continue to grow AFFO per share (the driver of intrinsic value for REITs) during high rate environments.

This naturally creates attractive valuations.

This fact, combined with the reality that specialized, small cap REITs already see their valuation disconnected from fundamentals can create incredible opportunities.

Let’s review these top 5 opportunities:

5. 🏬 CTO Realty Growth (CTO)

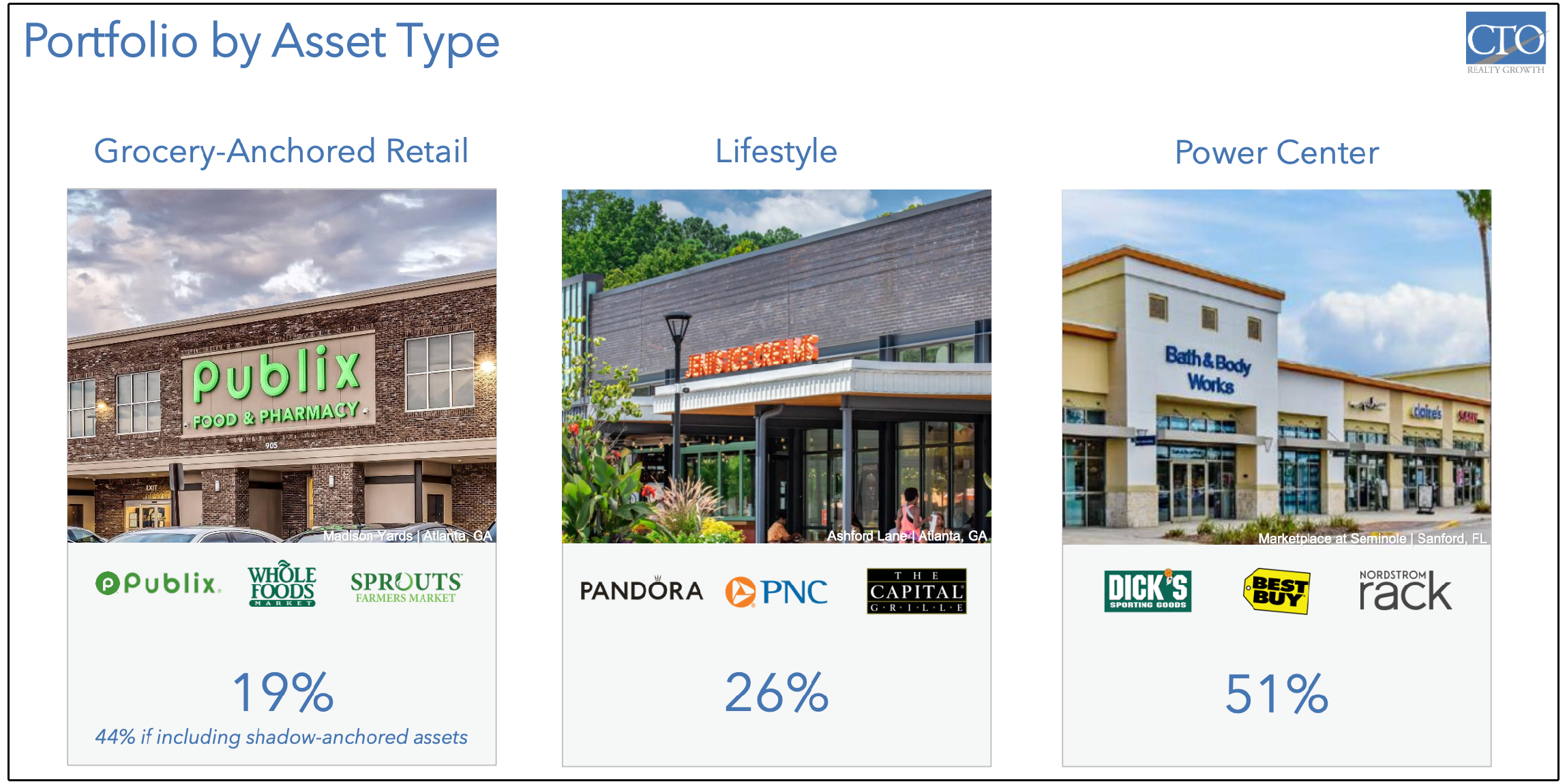

CTO is a small-cap retail REIT focused primarily on open-air shopping centers in high-growth Sunbelt markets.

The company owns retail properties that benefit from strong demographics, steady tenant demand, and embedded leasing upside.

This is not a struggling mall REIT.

CTO’s portfolio is centered around open-air retail, where demand has remained much healthier than many investors expected

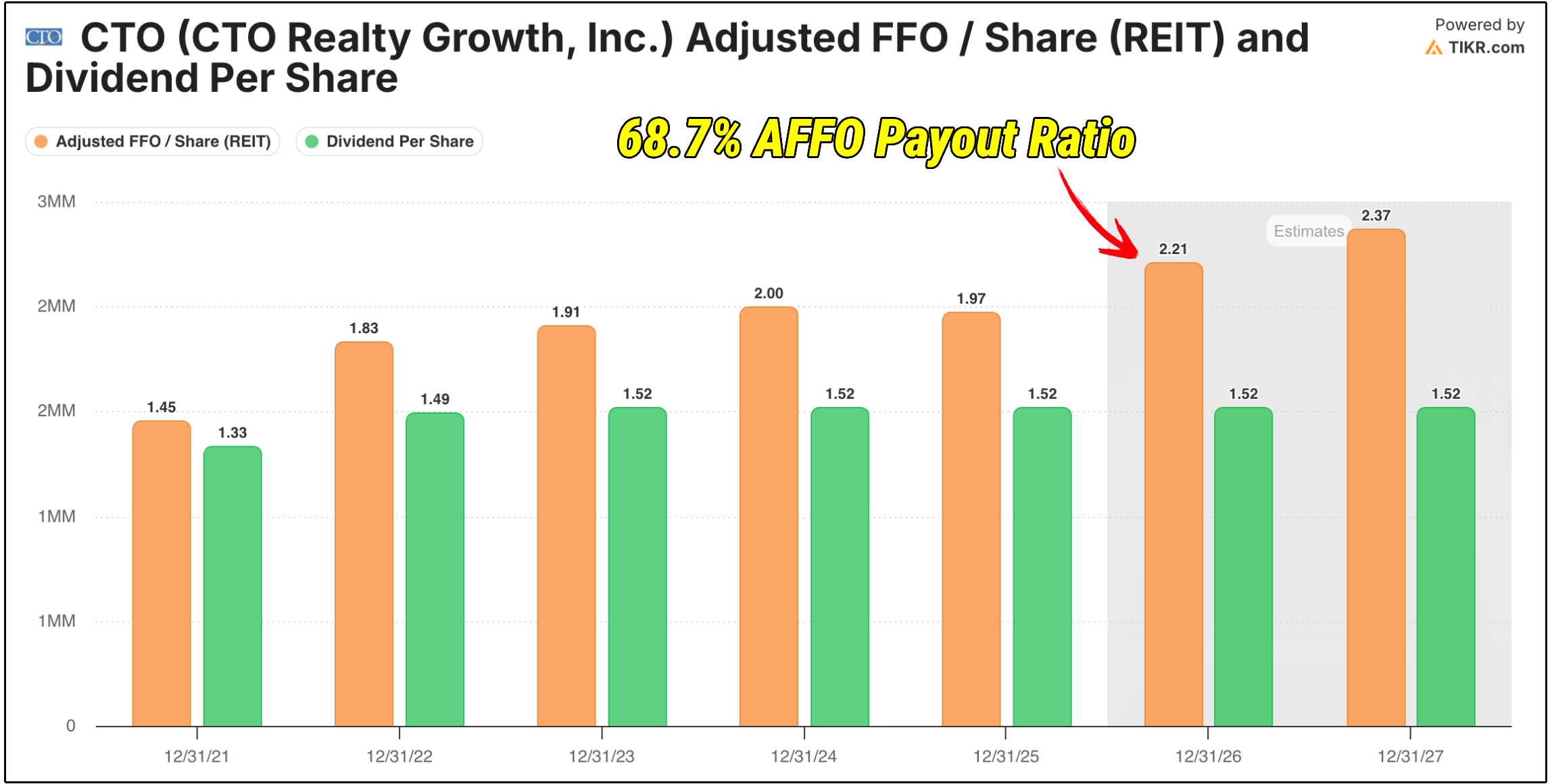

In Q1, CTO reported strong results, including AFFO per share growing by 14% year over year and portfolio occupancy at 95.4%.

Here’s what makes CTO stand out:

7.3% dividend yield

Roughly 9.2x forward P/AFFO

Sunbelt-focused retail portfolio

Growing signed-not-open rent pipeline

Never reduced its dividend

The signed-not-open pipeline is especially important.

CTO finished Q1 with $6.2 million of signed-not-open rent, representing 5.5% of in-place cash ABR, meaning CTO has already signed leases with tenants, but those tenants have not opened yet, so the rent is not fully showing up in current revenue yet.

This gives CTO a built-in organic growth runway, without needing to rely entirely on acquisitions.

Despite yielding 7.3%, the company is currently only using 68.7% of their AFFO to payout dividends, creating strong dividend coverage.

To be clear, CTO still has risks.

Retail is tied to consumer spending, and their Net Debt to Adjusted Ebitda ratio is around 6.4x, a bit higher than we typically like to see.

But CTO appears to be executing well.

The company is growing AFFO per share at a strong rate, improving leasing spreads, recycling capital, and redeploying into higher-yielding opportunities.

At today’s valuation, investors are getting a 7.3%+ dividend yield while paying roughly 9.3x forward AFFO.

At the same time, they are trading at a much lower valuation than their peers, while growing substantially faster.

For a REIT producing double-digit AFFO growth with a Sunbelt retail portfolio, this is a compelling risk/reward setup.

4. 🌿 NewLake Capital Partners (NLCP)

NewLake Capital Partners is a high-yield REIT where fundamentals may be improving faster than the market is willing to price in.

The key catalyst is medical cannabis is moving to Schedule III status at the federal level.

Under Schedule I, cannabis operators were unable to deduct basic business expenses, resulting in effective tax rates of 60–80% and severely constrained profitability.

Schedule III treatment should allow normal deductions, which could lead to immediate improvements in free cash flow, balance sheets, and overall tenant credit quality.

Obviously that is important, as tenant risk is the primary reason NLCP trades at such a deep discount.

Even after the recent rally, NLCP still trades at:

7.87x P/AFFO

Price to book value of just 0.82, meaning the market is valuing the company at 18% less than the value of its net assets

11.27% dividend yield

Net cash position, with more cash than debt

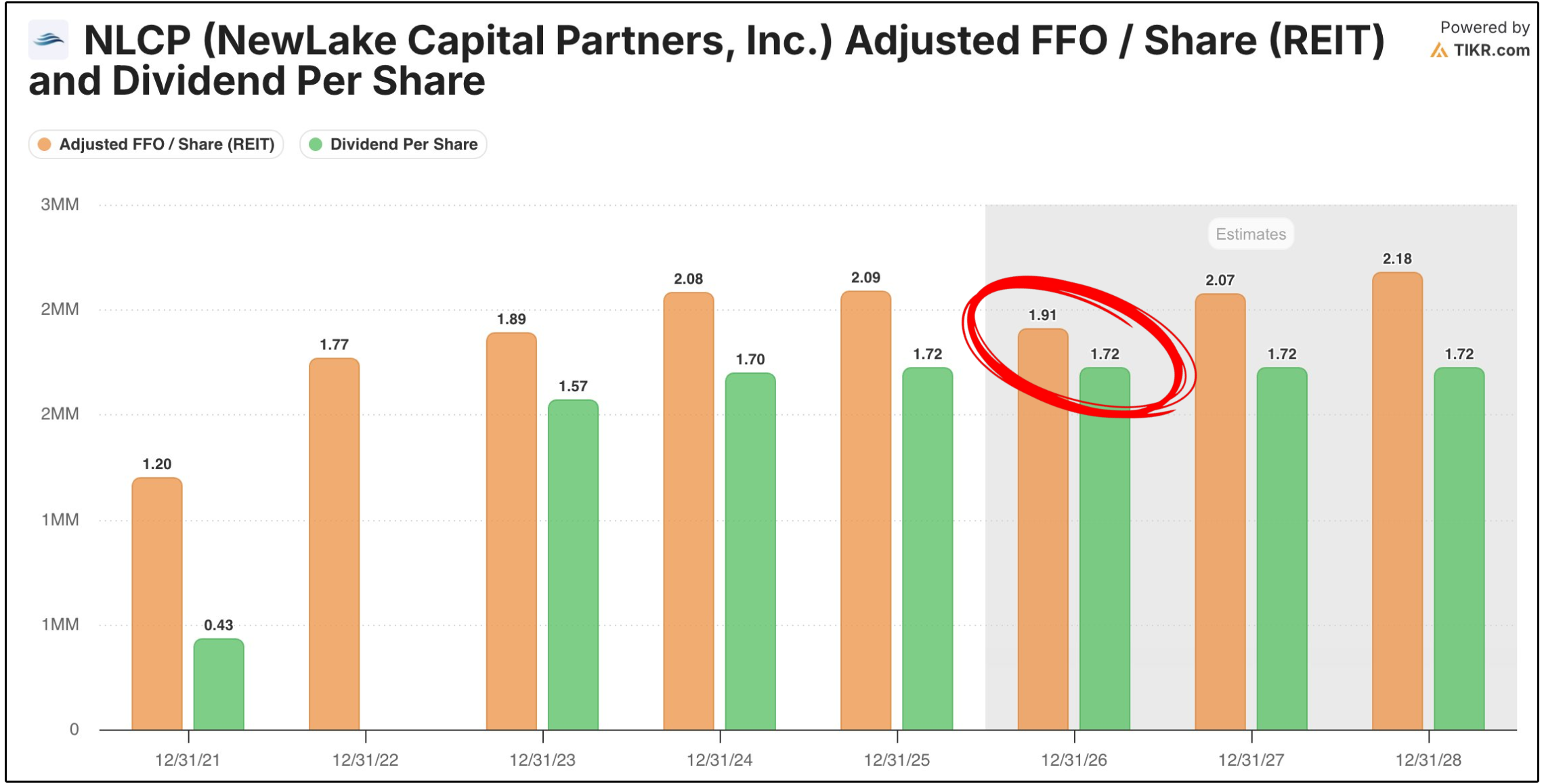

However, the projected drop in AFFO this year puts their AFFO payout ratio right at 90%, which is at the top of management’s target range.

To be clear, NLCP has faced real challenges, including tenant restructurings and vacancies, which explains the depressed valuation.

In the most recent quarter, NLCP had three large cultivation facilities sitting vacant, which pressured AFFO per share.

However, rent collection on the rest of the portfolio remained at 100%, showing that the broader portfolio is still performing well despite the challenges.

Management has also said they are seeing an uptick in interest for the vacant properties, though increased conversations do not guarantee those properties will ultimately be leased.

The stock is cheap because the market is worried about tenant quality, tenant concentration, vacancies, and the specialized nature of cannabis real estate.

But at the same time, Schedule III will improve operator cash flow and credit profiles, the outlook for rent collection, re-leasing, and long-term cash flow stability improves materially.

Another potential catalyst is a major exchange listing.

Management has said roughly 50–55% of annualized base rent is currently derived from medical cannabis activities, which could become important for NYSE or Nasdaq listing eligibility as cannabis regulation evolves.

A major exchange listing would likely improve liquidity and expand the pool of investors willing to own the stock.

NLCP remains a riskier speculative REIT and should be sized appropriately.

Cannabis real estate will likely continue to deserve a higher risk premium than traditional net lease real estate.

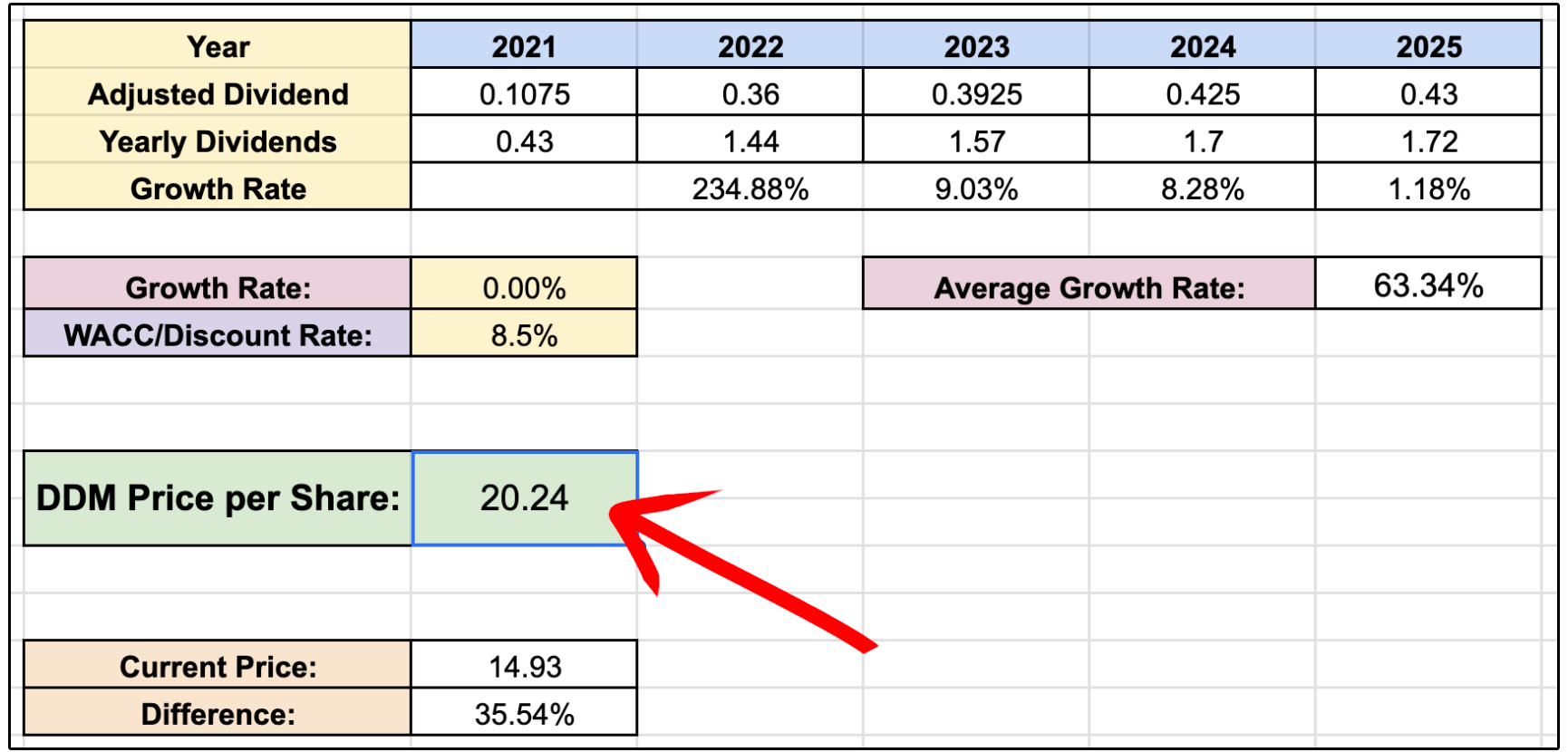

If NLCP can simply maintain their dividend at these levels, it would imply over 35% upside from current prices.

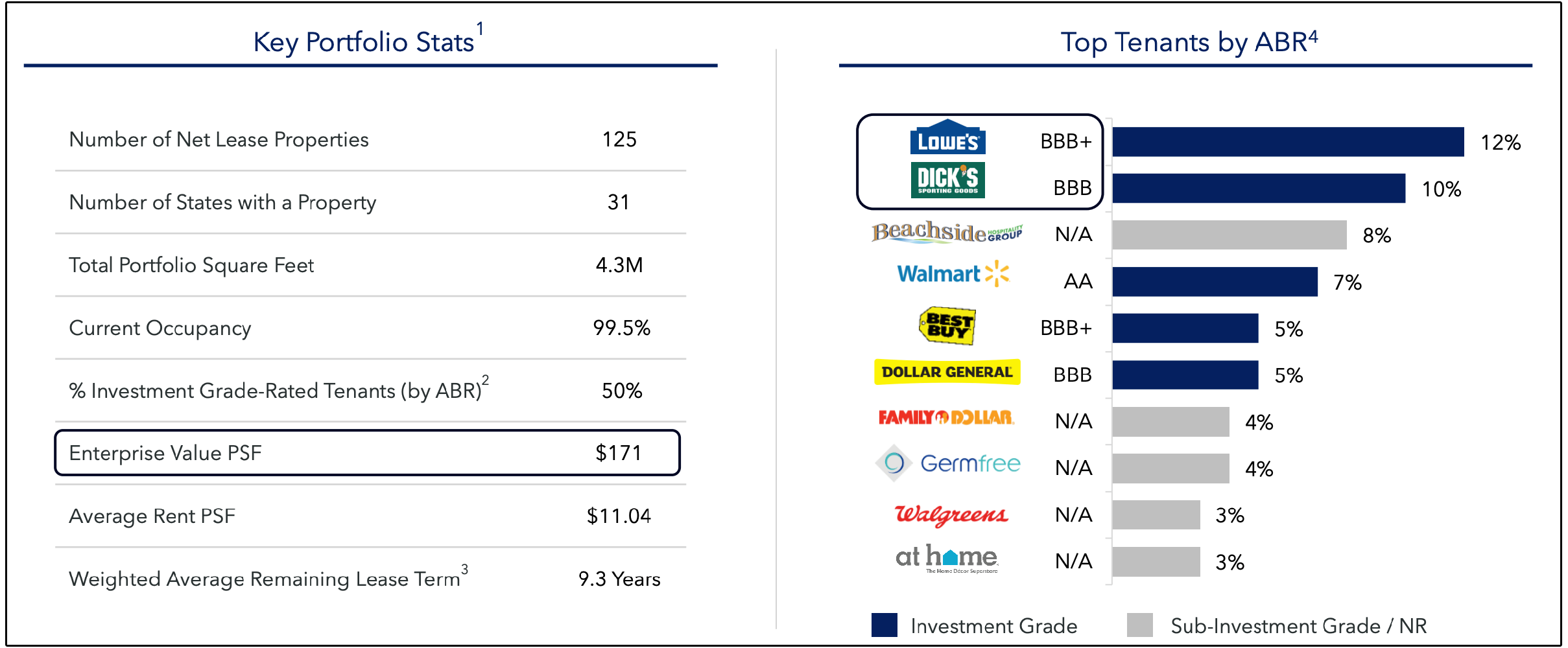

3. 🏔️ Alpine Income Property Trust (PINE)

PINE is a small-cap net lease REIT that often gets overlooked because of its size.

It’s only a $350M market cap REIT, so it’s quite small-

But the underlying story is becoming one of the more interesting setups in the small-cap REIT space.

The company owns 125 properties across 31 states, with 99.5% occupancy and a 9.3-year weighted average lease term.

Roughly 50% of annualized base rent comes from investment-grade rated tenants, which is one of the stronger concentrations in the net lease space.

Here’s what makes PINE stand out:

6.1% dividend yield

57% estimated AFFO payout ratio

99.5% occupancy

50% of rent from investment-grade tenants

The dividend coverage is by far what is most impressive.

A 6%+ yield with a 57% AFFO payout ratio is rare in the REIT market, especially when you consider the rate this REIT is growing AFFO per share.

Q1 transactions came in at a 14.1% blended initial yield, including a downtown Aspen retail property with a 50-year lease and 1.25% annual escalators, plus a $32M Georgia retail development loan at a 13% rate.

This is where PINE’s small size becomes an advantage.

Smaller transactions that would barely matter for Realty Income or Agree Realty can actually move the needle for PINE.

Net debt to pro forma EBITDA is around 6.6x, which is higher than ideal, so this is another small cap REIT with more leverage.

Typically, we like to see net debt to EBITDA at no greater than 5.5x.

The commercial loan portfolio also adds complexity, with roughly a third of invested capital sitting in loans rather than owned properties.

Those loans yield 13–15%, including some paid-in-kind interest, which means a portion of income is non-cash until the borrower performs.

But the market may be over-discounting those risks.

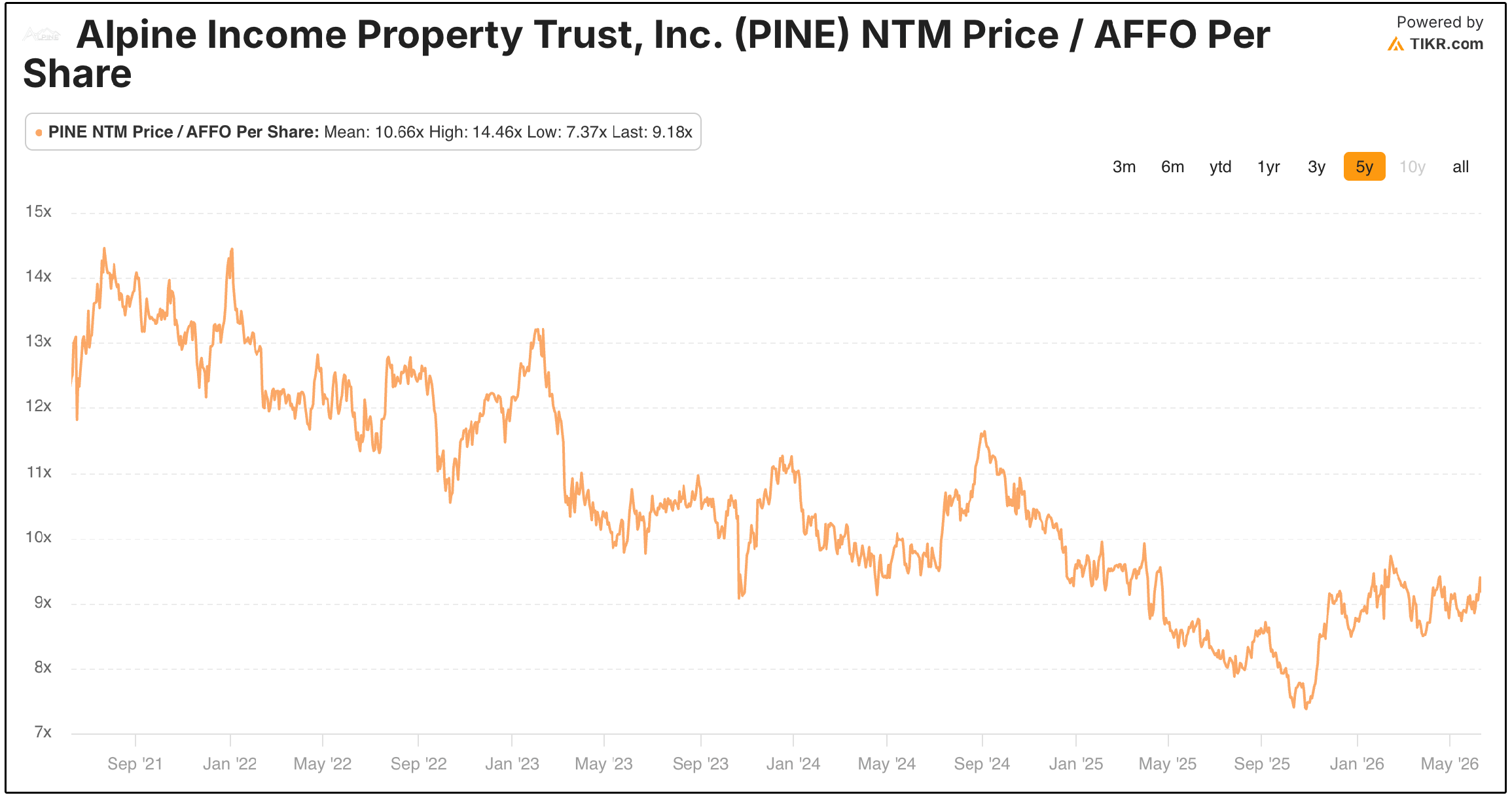

They’re currently trading at a P/AFFO multiple of just 9.18x, while the projected CAGR for AFFO per share through 2030 is close to 6.2%.

Growing the dividend at just 3.5%, which should be quite easy with the low payout ratio and 6.2% AFFO per share growth, would imply around 20% upside from current prices.

2. 🏗️ AH Realty Trust (AHRT)

AH Realty Trust, formerly Armada Hoffler Properties, is one of the more controversial small-cap REITs in the market today.

The REIT owns a portfolio of mixed-use office and service-oriented retail properties, with a focus on walkable communities, grocery-anchored retail centers, and high-growth markets.

But the bigger story is the strategic transformation currently underway.

Historically, AHRT operated with a development-first model, generating income from construction contracts, development fees, lending, and one-off transactions.

That worked well in strong markets, but it also created lumpy earnings, more complexity, and more risk when rates spiked and credit tightened.

This eventually led to AFFO not covering the dividend, which forced the company to cut the payout.

Now, under CEO Shawn Tibbetts, AHRT is reshaping the business.

The company is selling its multifamily portfolio, exiting construction and lending operations, reducing leverage, and refocusing around its core retail and mixed-use office properties.

Here’s what makes AHRT stand out:

8.2% dividend yield

Roughly 50% discount to estimated NAV

Insiders own over 10% of the business

~96% occupancy

Simpler retail and mixed-use office strategy

The key idea is that AHRT is becoming a cleaner REIT.

The two biggest historical problems were leverage and complexity.

By selling non-core assets and using proceeds to reduce debt, management is trying to strengthen the balance sheet.

And by exiting construction, lending, and multifamily, AHRT should become easier for investors to understand and value.

The management team recently stated:

“While 2026 represents a transition year for the company, I want to underscore that throughout this period, we continue to maintain full dividend coverage from the cash flows generated by our operating properties, while also meaningfully reducing debt.”

Importantly, the underlying property portfolio is still performing reasonably well.

If management successfully simplifies the business, reduces leverage, and proves the dividend is sustainable, AHRT could eventually be re-rated to a much higher valuation multiple.

Finally, let’s review the number 1 specialized small-cap REIT.

This is a REIT we added to our High Yield Portfolio when it was yielding over 10%, with extremely strong dividend coverage, and we’re already up 11% on this position.

Let’s take an updated look at it: