🚩 These “Safe” Dividend Stocks May Not Be So Safe...

The Dividend Trap Inside Some of America’s Safest Stocks ⚠️

Do you know the most important task of management?

It’s capital allocation.

Proper capital allocation is the difference between stocks that:

Can grow free cash flow and dividends for decades

Are forced to cut dividends

And right now, there are some very dangerous dividends being paid out from companies that investors have historically viewed as safe.

📉 Dividend Cuts

Dividend cuts are the worst nightmare for someone looking to live off dividends.

In February of 2024, I wrote an article on 3M stock, and how a future dividend cut was likely.

Keep in mind, at the time I wrote this article, 3M had grown their dividend payments for over 60+ years (making them a Dividend King)-

And had also just recently announced another dividend increase.

So naturally, I got a lot of pushback for this article. 👇

But just a few months later, a dividend cut is exactly what happened.

In a single moment, the payments investors were receiving from 3M were slashed in half.

Devastating.

But leading up to this event, all of the warning signs were there.

This was completely avoidable-

Investors just didn’t know what to look for.

⚡ Sneaky Dangerous Yields

One of the common mistakes with dividend investing is assuming a company that has historically been a great dividend payer will always be a great dividend payer-

Just like 3M.

This most frequently happens with stocks that have the title of ‘Dividend King’ or ‘Dividend Aristocrat’.

A Dividend Aristocrat is an S&P 500 company that has increased its dividend every year for at least 25 consecutive years.

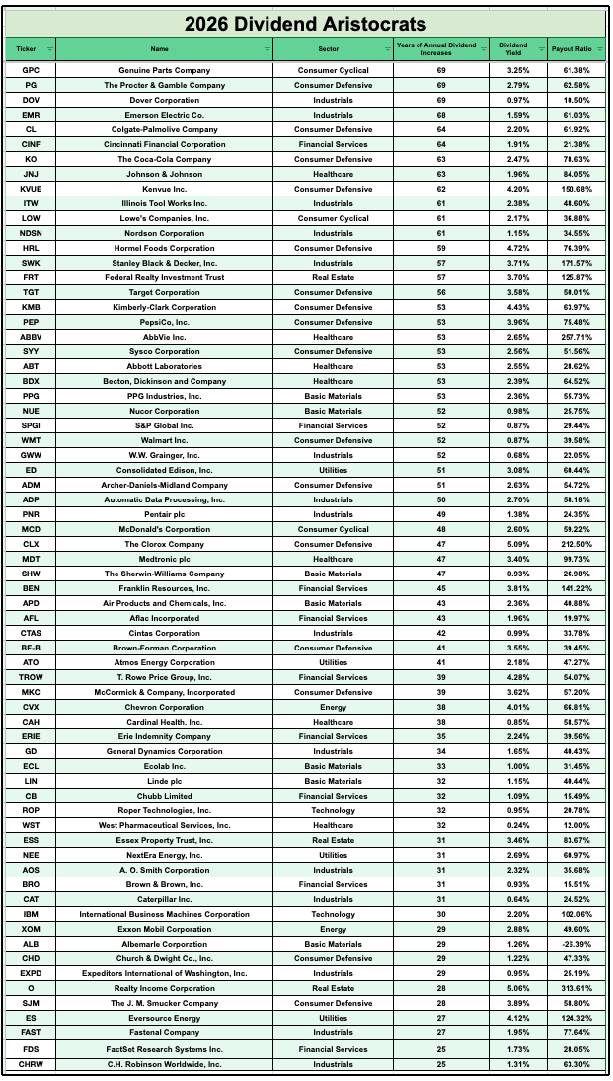

Here is the complete list of Dividend Aristocrat stocks in 2026:

The majority of the companies are healthy, and will likely be able to grow their dividends for decades into the future.

But not all of them.

This is why randomly selecting stocks from this list is so dangerous.

In fact, let’s look at just a few of them that you may be surprised to find out the dividend is in danger.

🚩 Dividend Red Flags

Pepsi has grown dividends now for 53 consecutive years in a row.

In fact, this means it meets the requirements for both Dividend Aristocrat and Dividend King.

Pepsi has historically been considered a durable, defensive business model, that reliably grows dividends every single year.

Take a look at the dividend metrics:

Yield: 4%

Dividend Growth: 6%

50+ Years of Dividend Growth

On the surface level, everything seems fine.

In fact, Pepsi just recently announced a dividend increase of 4% a couple of months ago, continuing their streak of dividend growth.

But remember, the most important task of management is capital allocation.

In other words, how they choose to use the company’s free cash flow.

As a reminder, management generally has five options for allocating free cash flow:

Reinvest in the existing business

Complete mergers and acquisitions

Pay down debt

Repurchase shares

Pay dividends

In other words, if a stock has a free cash flow payout ratio of 100%, then it’s using all of its capital to pay out dividends, leaving no capital to reinvest, buyback shares, or pay down debt.

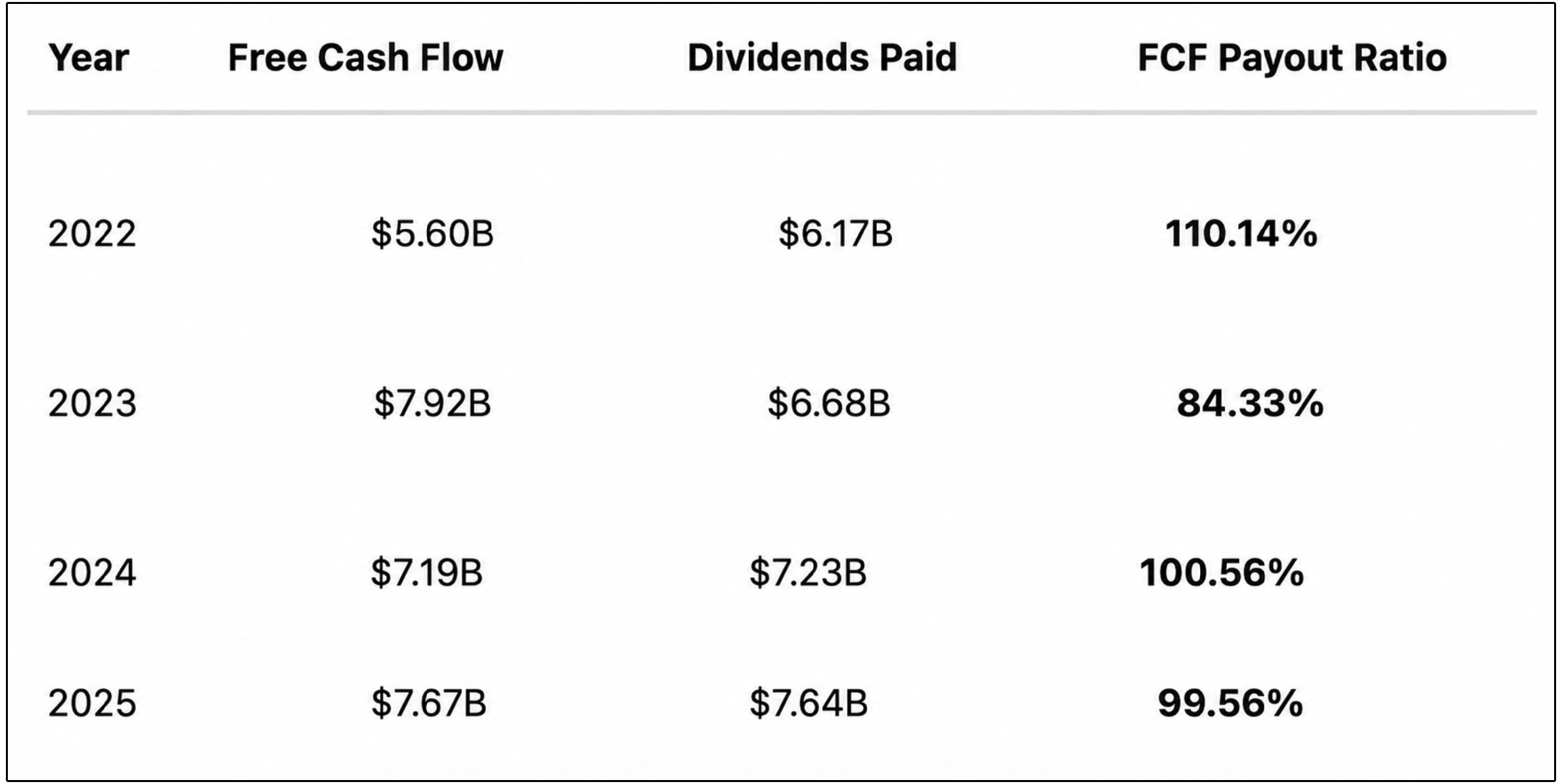

So how has Pepsi’s FCF payout ratio evolved over the last few years?

Pepsi is using all of it’s free cash flow to payout dividends.

There’s a few obvious issues with this.

For one, the company completed last year a nearly $2B acquisition of the Poppi brand.

The only way this type of move could have been made was through a weakening balance sheet, since the company could not use free cash flow to make this move.

Secondly, the company recently issued their 2026 guidance. Here’s what they said to expect:

Organic revenue to increase between 2 and 4 percent

A free cash flow conversion ratio of at least 80 percent

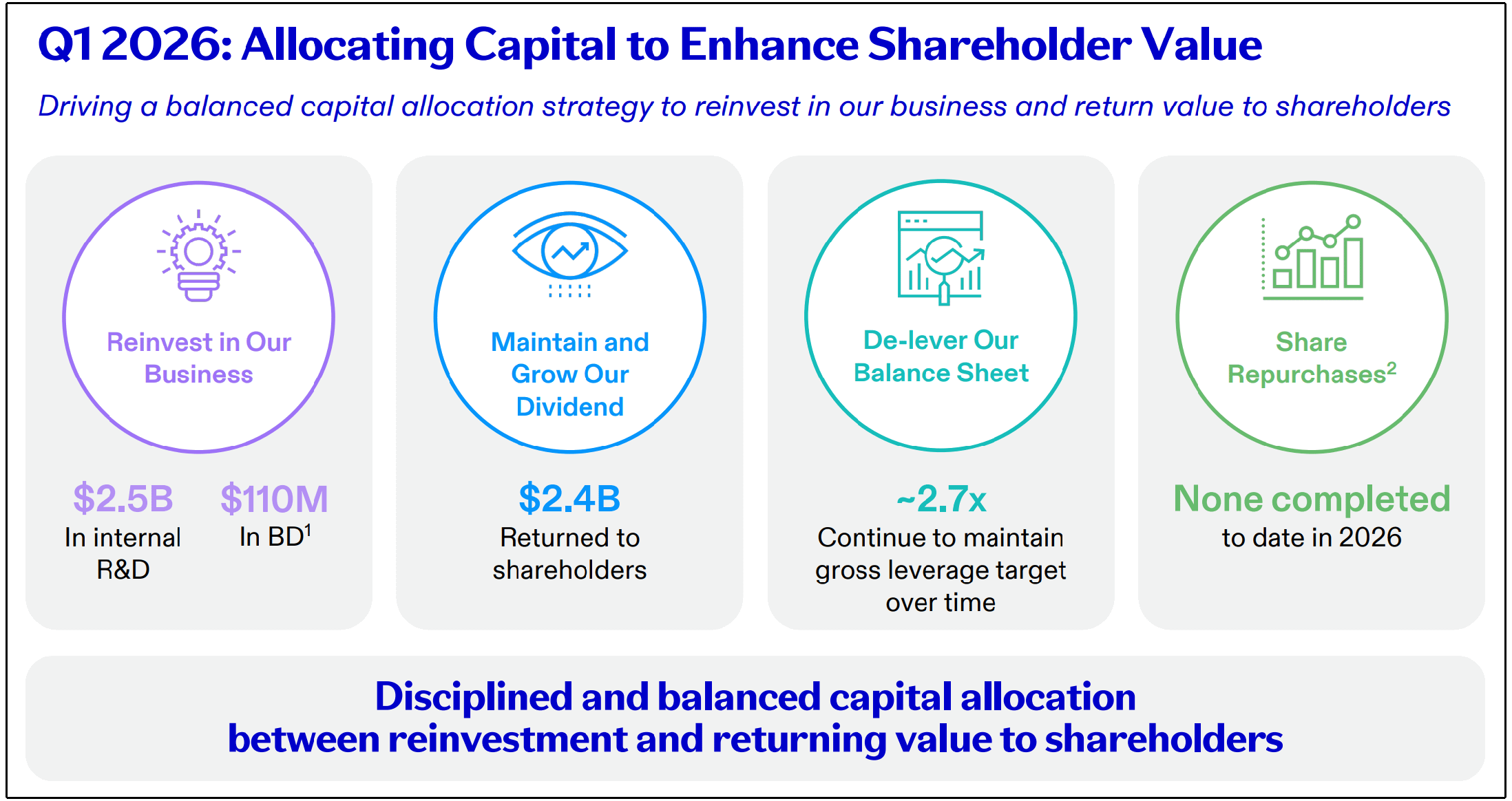

Total cash returns to shareholders of approximately $8.9 billion, comprised of dividends of $7.9 billion and share repurchases of $1.0 billion.

Let’s dissect this a bit further.

Revenue growth is not likely to be above the rate of inflation, and will most likely not come in at 4%, which is the rate they just increased their dividend.

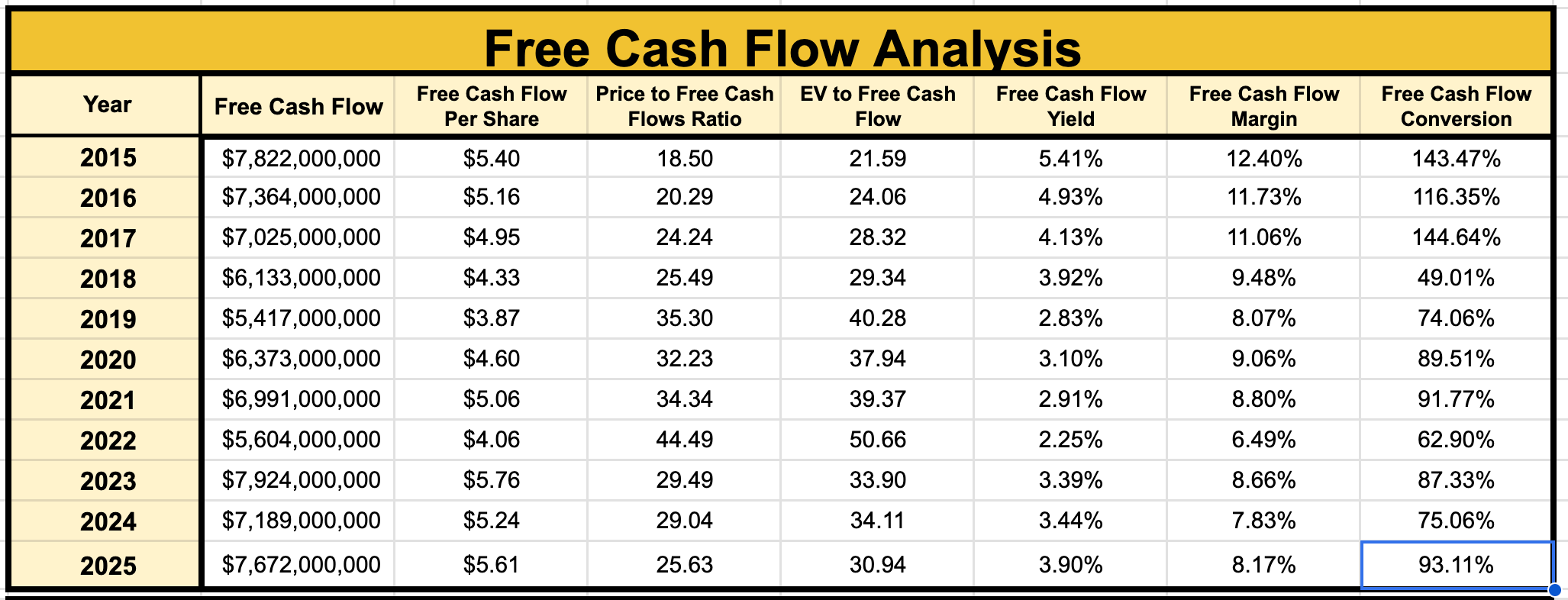

This lack of revenue growth can be made up for if margins are expanding, but Pepsi has guided towards a free cash flow conversion ratio of 80%.

This is down from 93% the previous year.

So revenue is stagnating, while margins are declining.

Despite this, they are paying out $7.9 billion in dividends in 2026, despite the fact free cash flow will very likely not cover this.

This type of capital allocation is simply not sustainable at current levels.

Pepsi’s balance sheet will continue to suffer as they take on more debt to fund their capital allocation priorities.

This is a very similar road that 3M went down.

This doesn’t mean dividend cut in 2026, or even in the next few years.

It does mean if something doesn’t change, the company will continue to get fundamentally weaker, which over time leads to a dividend cut.

⚠️ Another Example

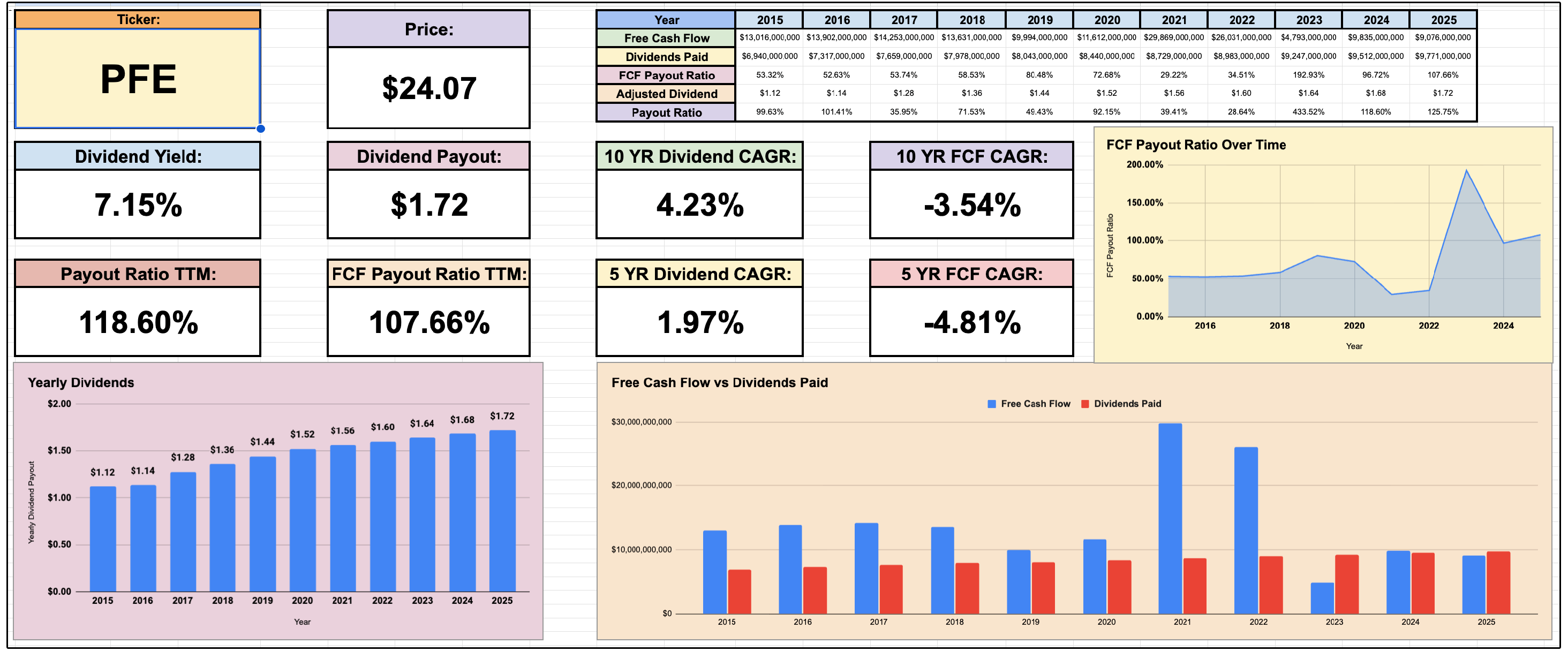

Pfizer is another example.

The company is getting attention right now due to the fact they:

Are yielding over 7%

Are trading at historically low valuation levels

Have a history of dividend growth

But a deeper look into their capital allocation reveals some serious issues.

The free cash flow payout ratio at the end of 2025 was sitting at over 107%, and has been hovering in a dangerous range for over three years now.

That’s not sustainable.

The company also happens to have recently given 2026 guidance, where they indicated they expect no revenue growth, or even the potential for a slight decline.

But here is what perhaps is most ironic:

The company has completed no share repurchases so far in 2026.

Share buybacks are extremely effective when a stock is trading at low valuation multiples, just like Pfizer is right now.

However, because all of their capital is being used to simply maintain the dividend, they can’t pursue this opportunity.

But perhaps most concerning, is the projected continual decline in earnings over the next few years.

If earnings and free cash flow aren’t growing, then dividends can’t grow sustainably.

And if free cash flow is declining while the FCF payout ratio is already above 100% (like Pfizer)…

Huge red flag.

🧼 One More Example

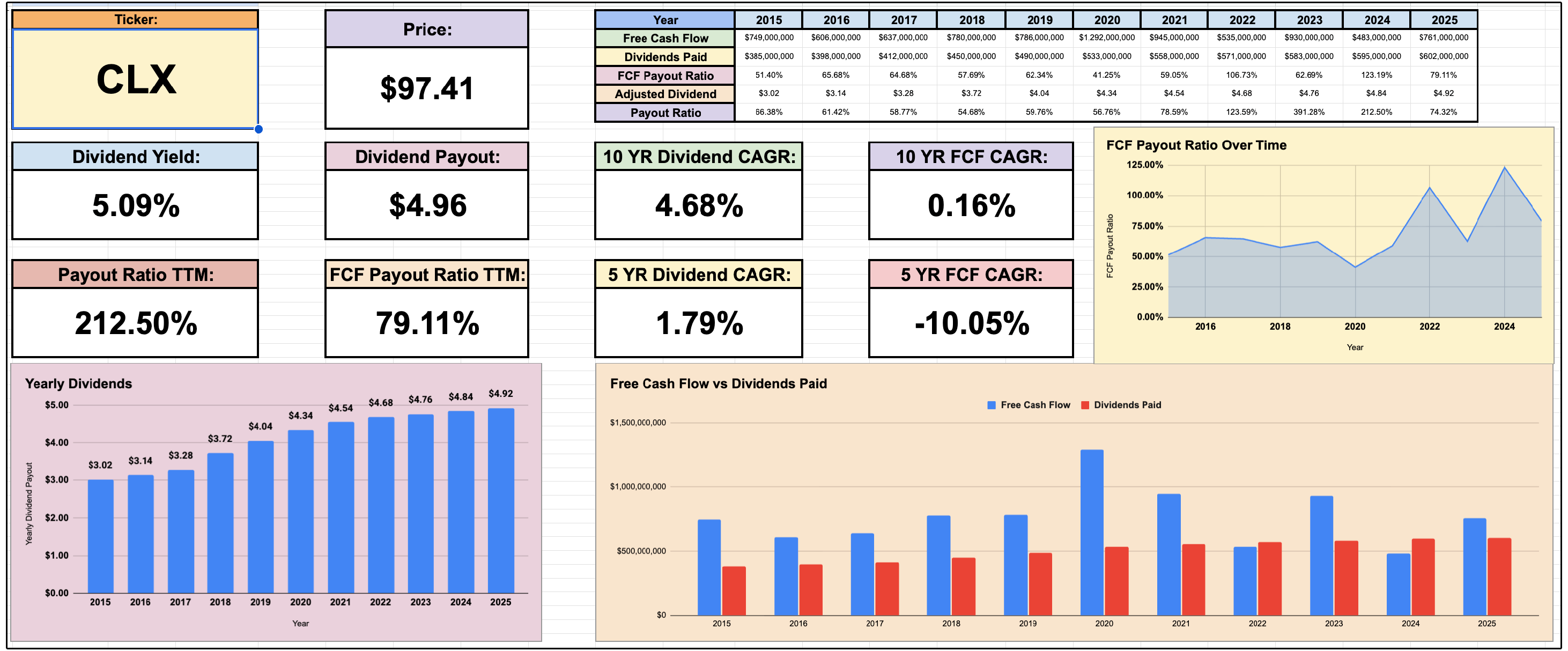

Clorox is currently yielding over 5%, and is a Dividend Aristocrat with over 25 years of consecutive dividend increases.

But look at the FCF payout ratio over the last decade.

It started at just 50%, and hit nearly 125% in 2024, and nearly 80% at the end of 2025.

Again, dividend growth that isn’t backed by free cash flow growth isn’t sustainable.

With their earnings expected to decline in 2026, it’s likely we see the payout ratios climb higher in the coming months.

💰 Sustainable High Yields

There are plenty of high yield opportunities out there if you know where to look.

Many of these opportunities are hidden behind alternative income asset classes.

The Dividendology Database is designed to unlock these opportunities.

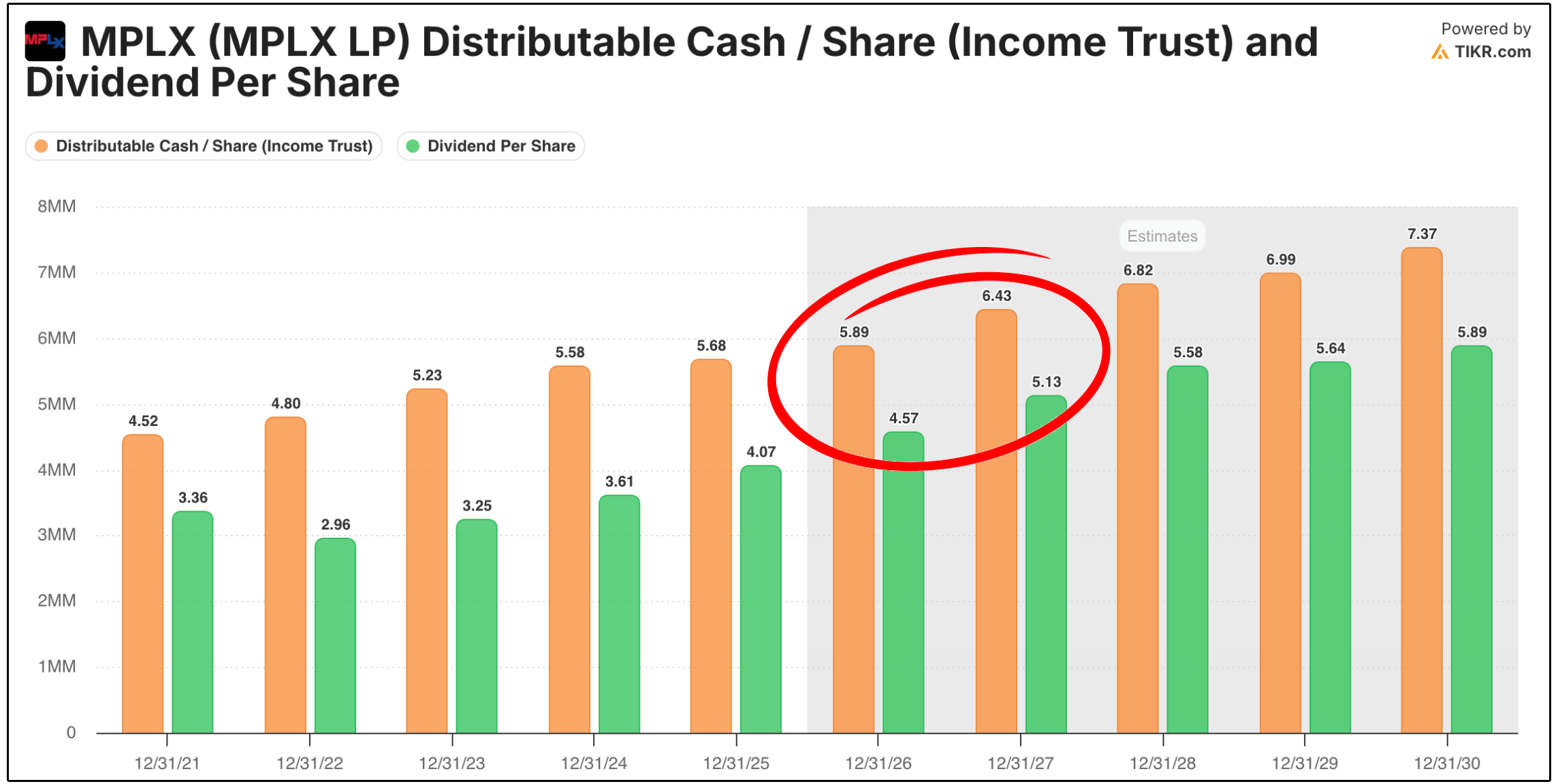

For example, MPLX is yielding 7.5%, up over 12.5%, with sufficient dividend coverage!

Management has even guided towards double-digit distribution growth over the next few years.

Of course, this is a simplified view of MPLX, and the way to analyze dividend durability for high yield assets can vary.

You can learn more about analyzing high yield dividends here.

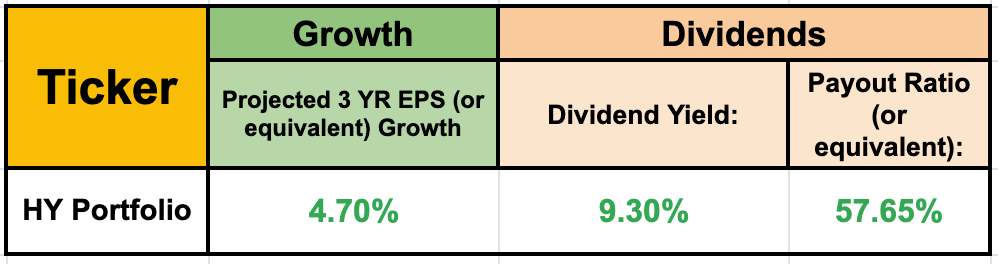

Right now, our model high yield portfolio is yielding 9.3%, has outperformed the market, and has even seen dividend growth from multiple positions in the last year.

🧠 Capital Allocation

Capital allocation will ultimately tell you how a company intends to reward their shareholders, and whether or not a companies dividends are sustainable.

Don’t make the mistake of believing just because a company has historically been a good dividend grower, that it will always be that way.

Management can hide some of the underlying issues on the surface level-

But not if you understand capital allocation and free cash flow.

If you want to take a deep dive into understanding free cash flow, you can click here.

📉 Dividend Cuts

Dividend cuts are the worst enemy for investors looking to live off income.

We must know how to spot the warnings signals before cuts take place.

If you want to get access to the Dividendology Database to help avoid dividend cuts, as well as get access to all the features mentioned below, you can do so here:

See you soon.

Dividendology

Check out these resources:

Tickerdata 🚀 (TICKERDATA SUMMER SALE (CODE: ‘HEAT’ FOR 30% OFF)

Interactive Brokers 💰 (My favorite place to buy and sell stocks all around the world!)

Seeking Alpha 🔥 (Research stocks $30 off! + 7 day free trial)

HYSA 📊 (Get Access to the Best High Yield Savings Accounts!)

Your previous posts on PEP let me out and I settled on MO instead. Payout ratios are too important to ignore.