📊 This High Yield Portfolio Outperformed the Market!

Plus The State of the BDC Market

Last week, we reviewed the positions that are currently in our High Yield Portfolio.

So far, the performance has been phenomenal.

While this performance is certainly exciting, as I pointed out last week and some subscribers have pointed out as well, we are yet to add a single BDC to our portfolio.

BDCs have been a disaster over the last 6 months-

However, there’s been a quiet market shift that is currently creating some high yield opportunities in the BDC market.

Let’s take advantage of this.

📈 Our Outperformance

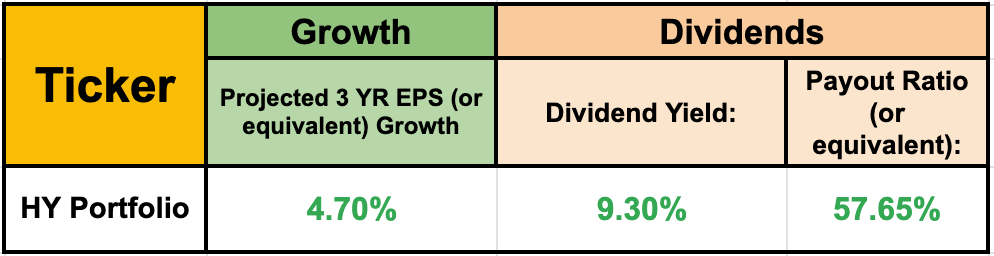

The High Yield Portfolio return has been approximately 9.8% in 2026 on a time-adjusted basis.

Meanwhile, the S&P 500 return has been approximately 9.4% over that same period.

That means our High Yield Portfolio is currently outperforming the S&P 500.

Simply amazing.

But the performance doesn’t tell the whole story.

Not only did this portfolio outperform by a wide margin, but it:

Had lower volatility (standard deviation)

Had a lower maximum drawdown

Had a stronger Sharpe Ratio

The Sharpe Ratio is an important one.

The Sharpe Ratio is a way of measuring how much return you’re getting for every unit of risk you take.

A higher Sharpe Ratio essentially means that you’re being compensated more generously for the volatility your portfolio experiences.

Basically, we took on less risk than the S&P 500, while still experiencing better returns.

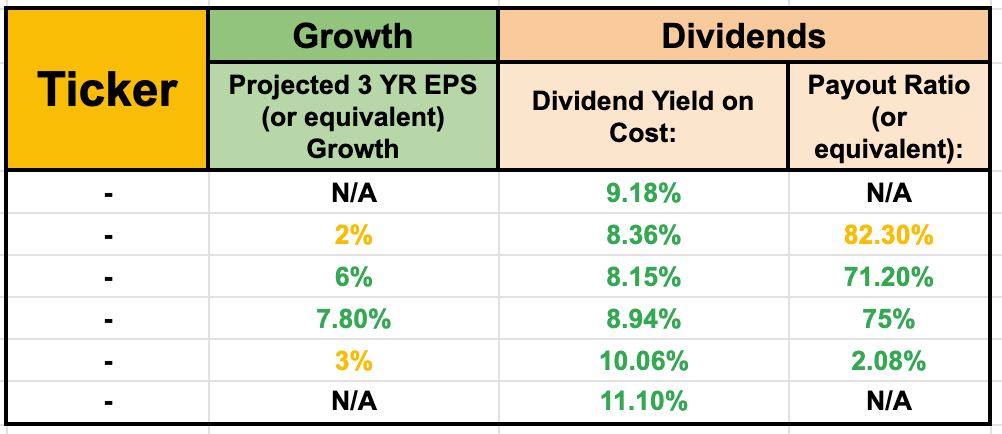

And that’s on top of the portfolio currently yielding a massive 9.30%, with the yield on cost GROWING due to a few of our picks growing their dividend payments.

While it’s still early, this portfolio has simply seen amazing performance.

We’ve undoubtedly selected some under the radar companies that have contributed to this-

But this is also in part due to avoiding the disaster that has been the BDC market, which is where many investors turn to when seeking out high yield.

📉 The BDC Market

I’m not ‘anti-BDC’ whatsoever-

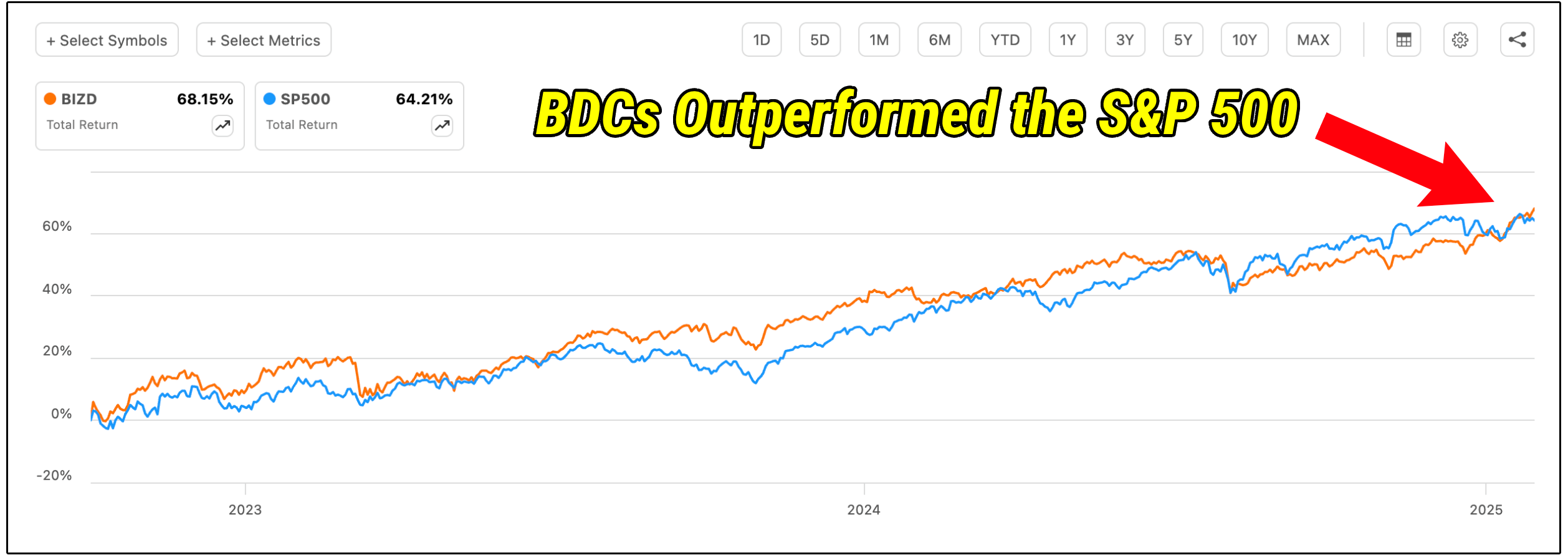

In fact, BDCs even went through a period of time where they outperformed the S&P 500, despite a massive tech rally in the broader market.

It does press the question:

What type of environment were we operating in that allowed such amazing performance from this high yield asset class?

High rates.

After a decade of near-zero interest rates, BDCs suddenly found themselves in one of the most attractive environments they had seen in years.

Most BDCs lend the vast majority of their money to middle-market companies at floating rates.

So when interest rates rose, the income on many of these loans rose as well.

That meant BDCs were able to generate significantly more net investment income, which gave many of them the ability to raise dividends, pay supplemental dividends, and produce very strong total returns for shareholders.

It was an amazing time to be a BDC shareholder.

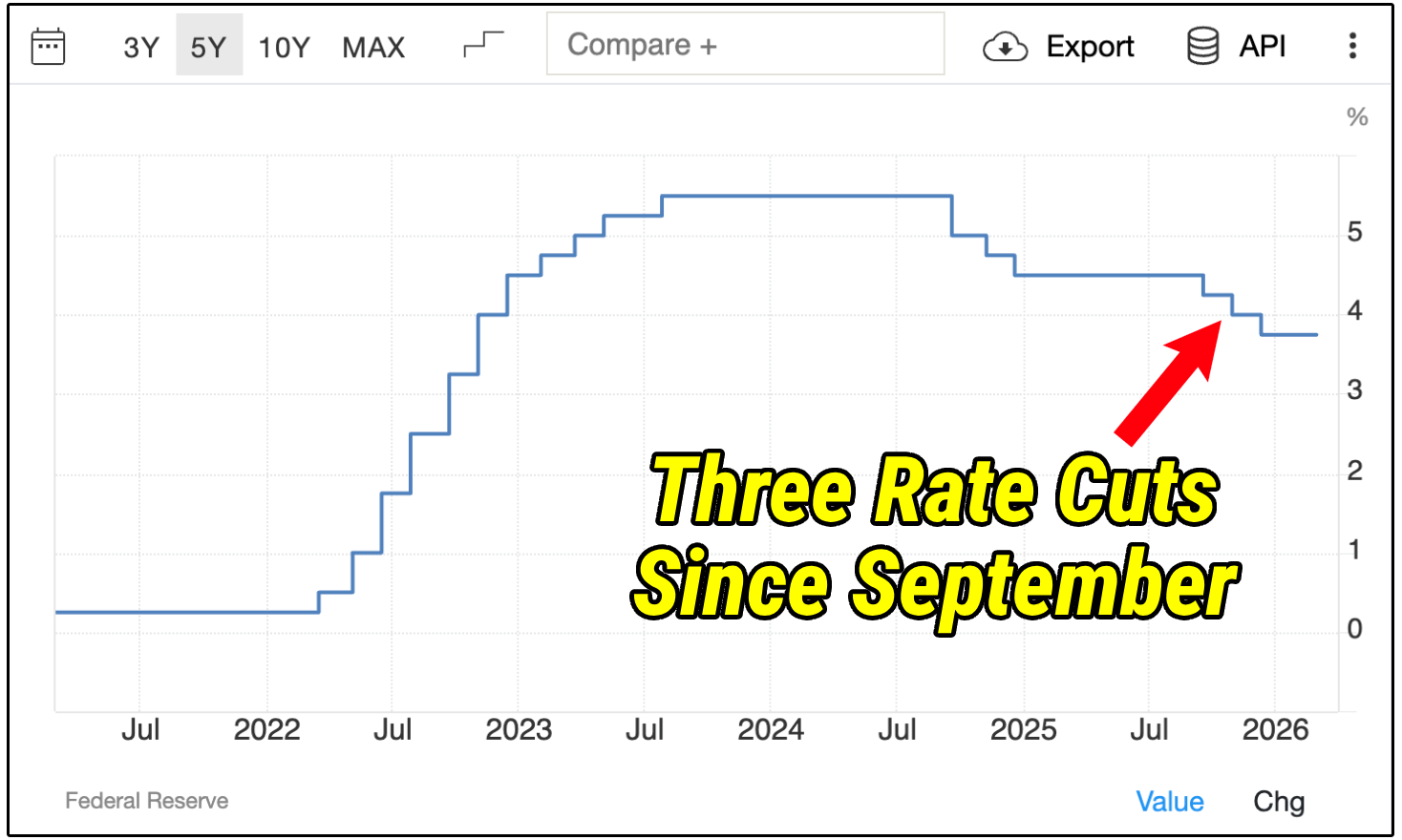

But as inflation rates lowered, the Fed began the process of cutting rates.

And at the beginning of 2026, the market was expecting three more rate cuts throughout the year.

All of a sudden, investors had two major reasons to be concerned about the BDC market:

Declining rates leading to lower net investment income

Overexposure to software companies in their portfolio

Both of these issues have posed serious threats to the BDC market, and as a result we’ve seen distributions fall for many BDCs, and share prices get decimated.

Just take a look at the VanEck BDC Income ETF for reference.

⚠️ Structural Issues?

As stated above, the weakness in the BDC market was primarily due to two issues:

Declining rates leading to lower net investment income

Overexposure to software companies in their portfolio

However, there is a serious difference in the two of these issues.

One is a structural issue, the other is much broader economic issue.

Rates were declining, and were projected to continue to decline, which of course was priced into these BDCs.

However, we’ve seen a dramatic shift in the economy over the last few months.

According to the Federal Reserve, a 10 percent increase in the price of oil raises the energy CPI by about 1.5 percent almost immediately.

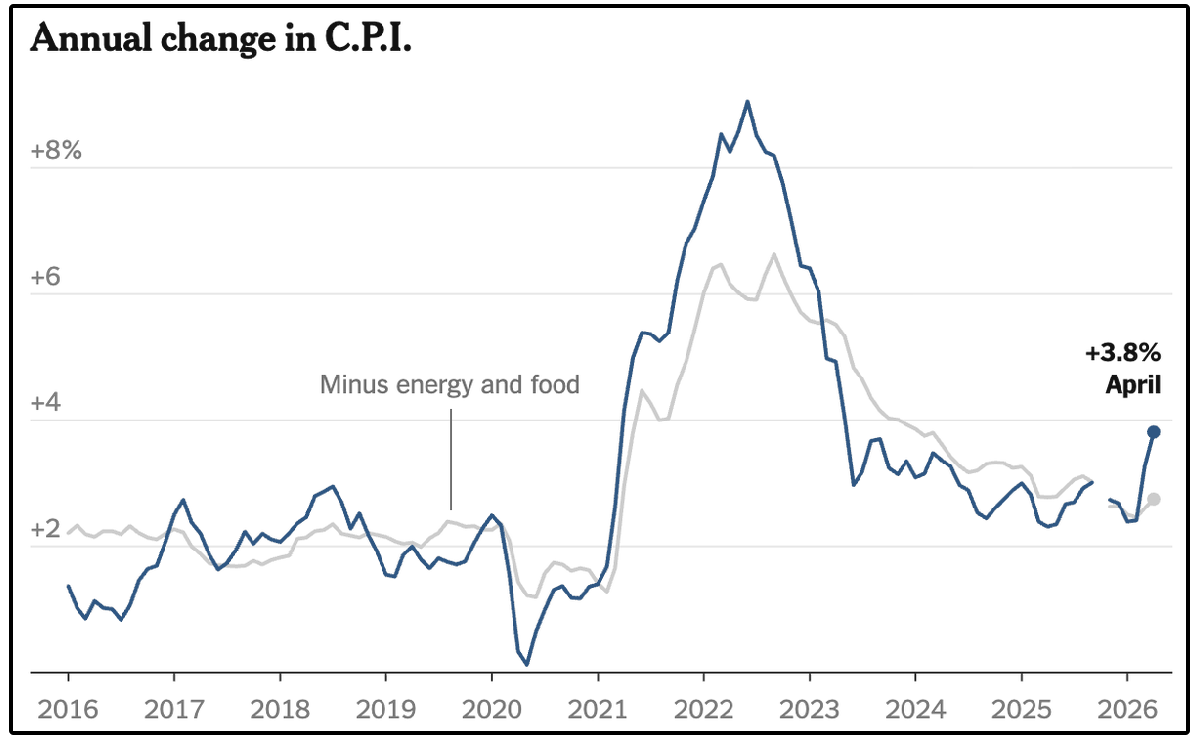

Oil prices have risen dramatically recently due to the Iran conflict, and as a result, inflation just hit its highest level month over month in 3 years.

After years of trying to get inflation tamed in response to the money printing that ensued as a result of 2020, inflation is back.

And of course, the Fed only has one lever to pull when inflation is high.

Raise interest rates-

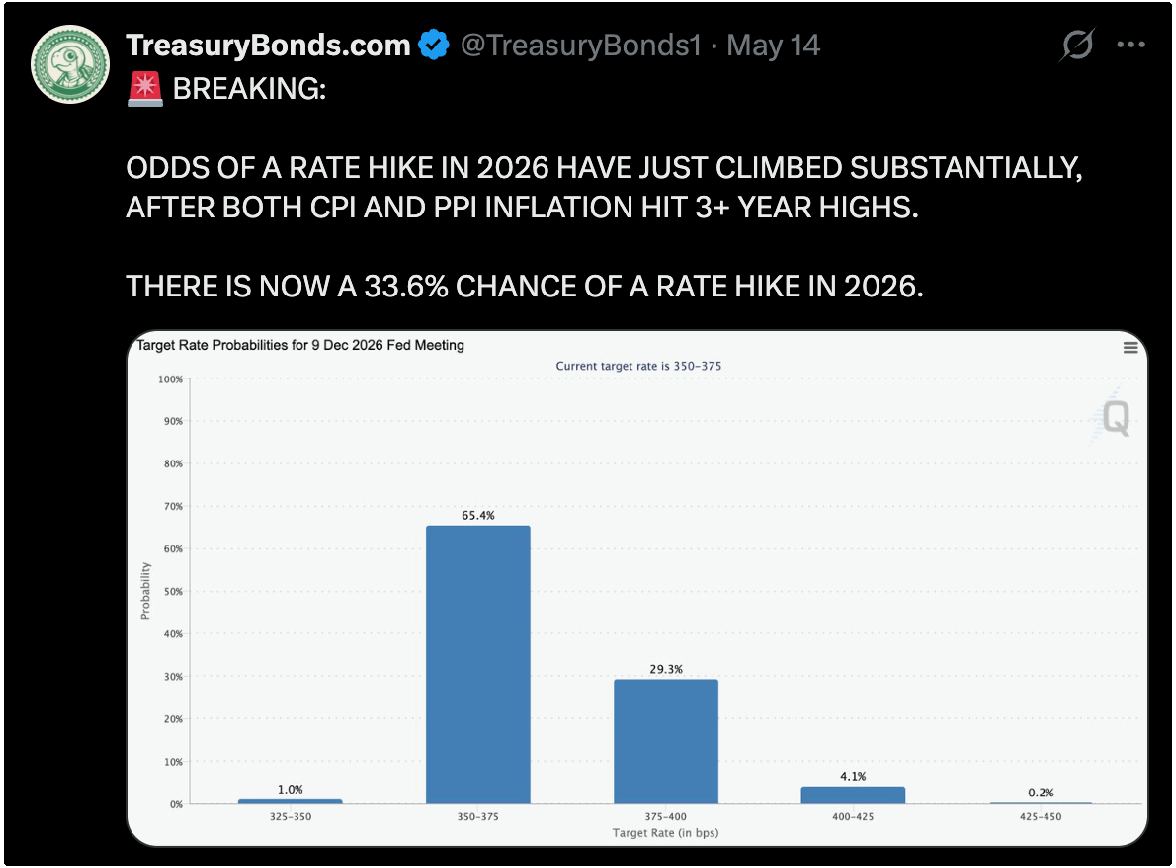

And that is now exactly what the market is expecting them to do.

We’ve gone from expecting three rate cuts in 2026, to an increasing possibility of a rate hike.

So what does this mean for BDCs?

It means the economic issue they’ve been facing is weakening.

While rising rates are certainly an issue for most equities, it’s good news for BDCs.

It’s difficult as investors to handle a headwind that impacts an entire cetor as a whole, which is a large reason we’ve elected to stay away from the BDC market over the last year with the Dividendology High Yield Portfolio.

But this still leaves us with the structural issue of overexposure to software companies-

Which is something we can address much better on an individual company basis.

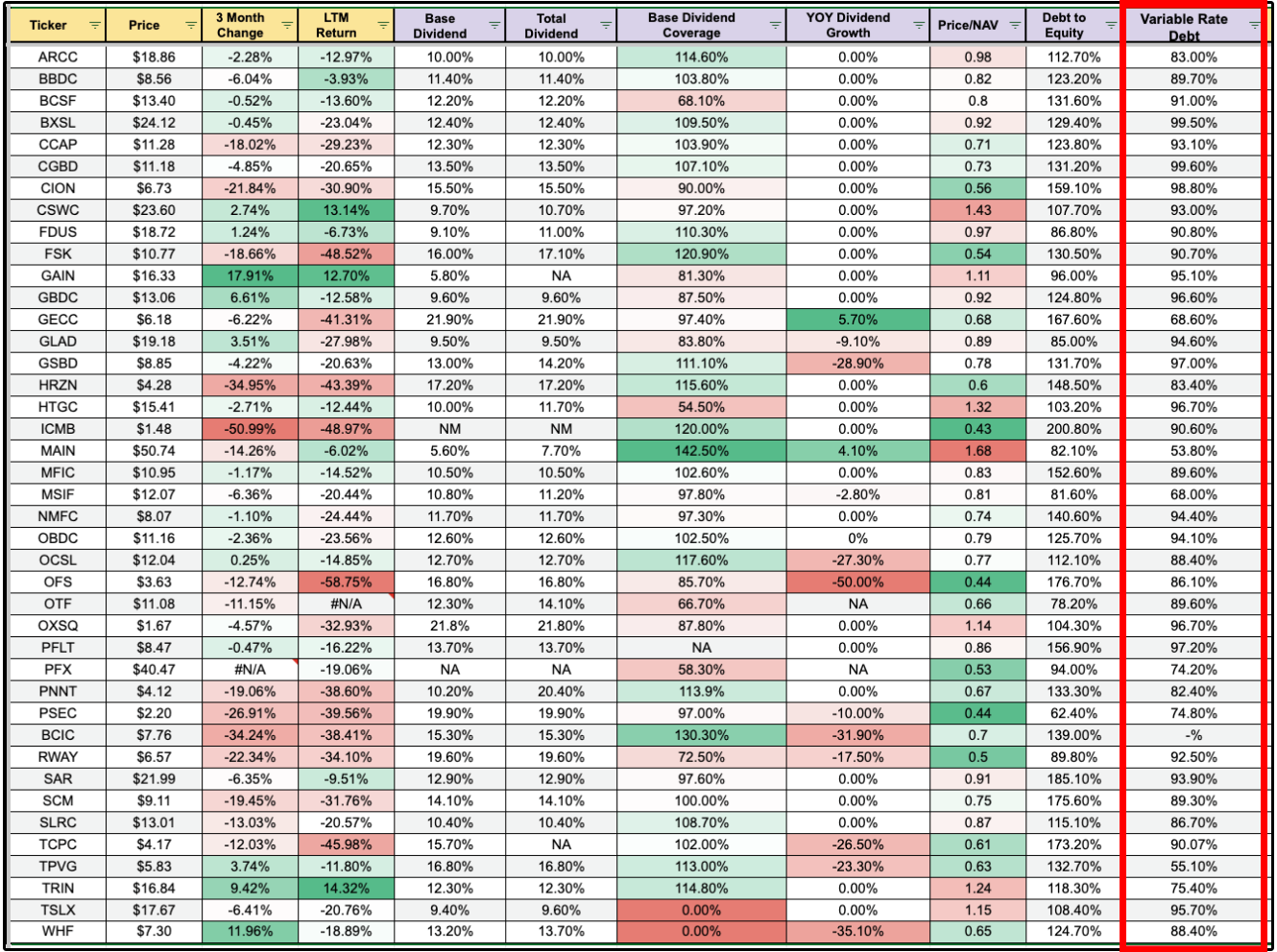

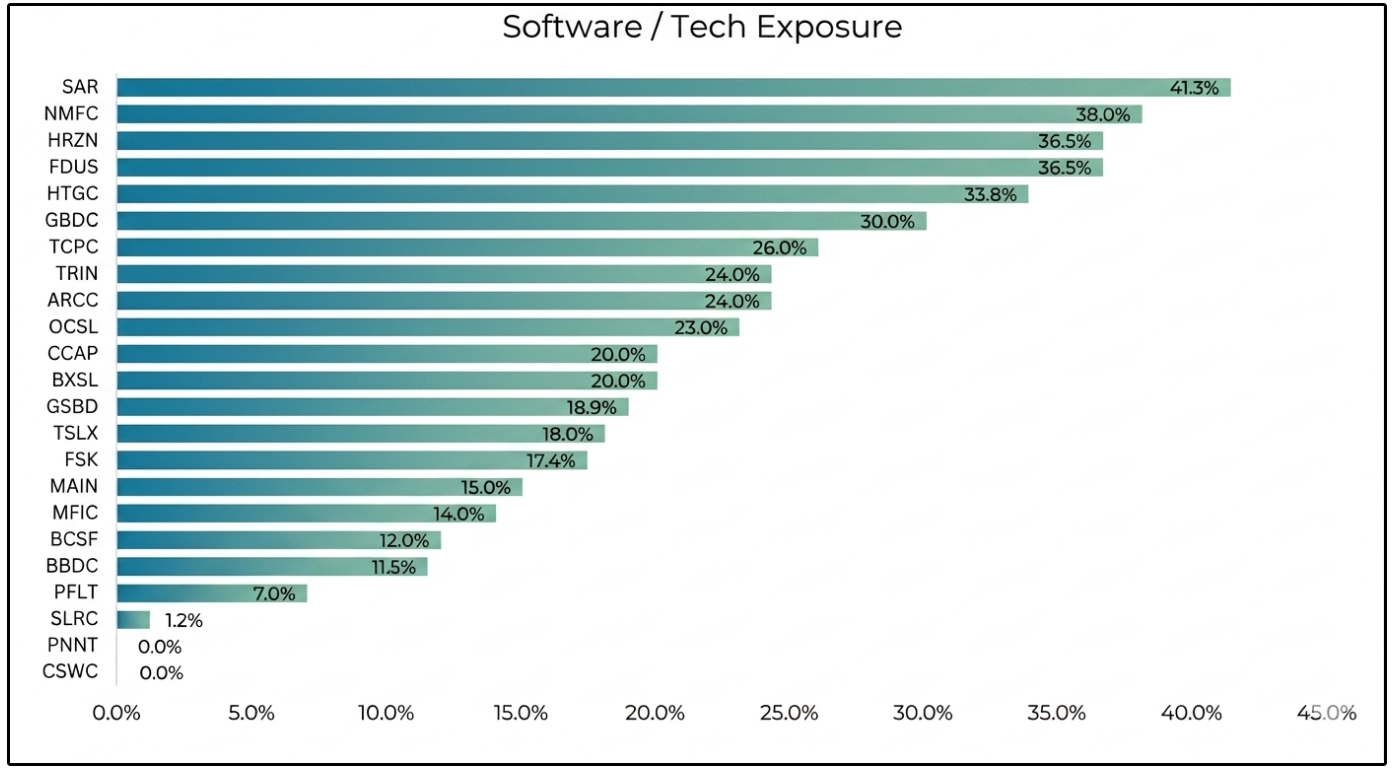

For example, take a look at the software exposure of many of the BDCs in the Dividendology Database.

While this data may have changed slightly as it was pulled last quarter, many BDCs still sit with 20% or more exposure to software companies in their loan portfolio.

However, there are clearly multiple BDCs that are set to benefit from this new rate environment as well as low exposure to software companies.

Let’s look at one of them.

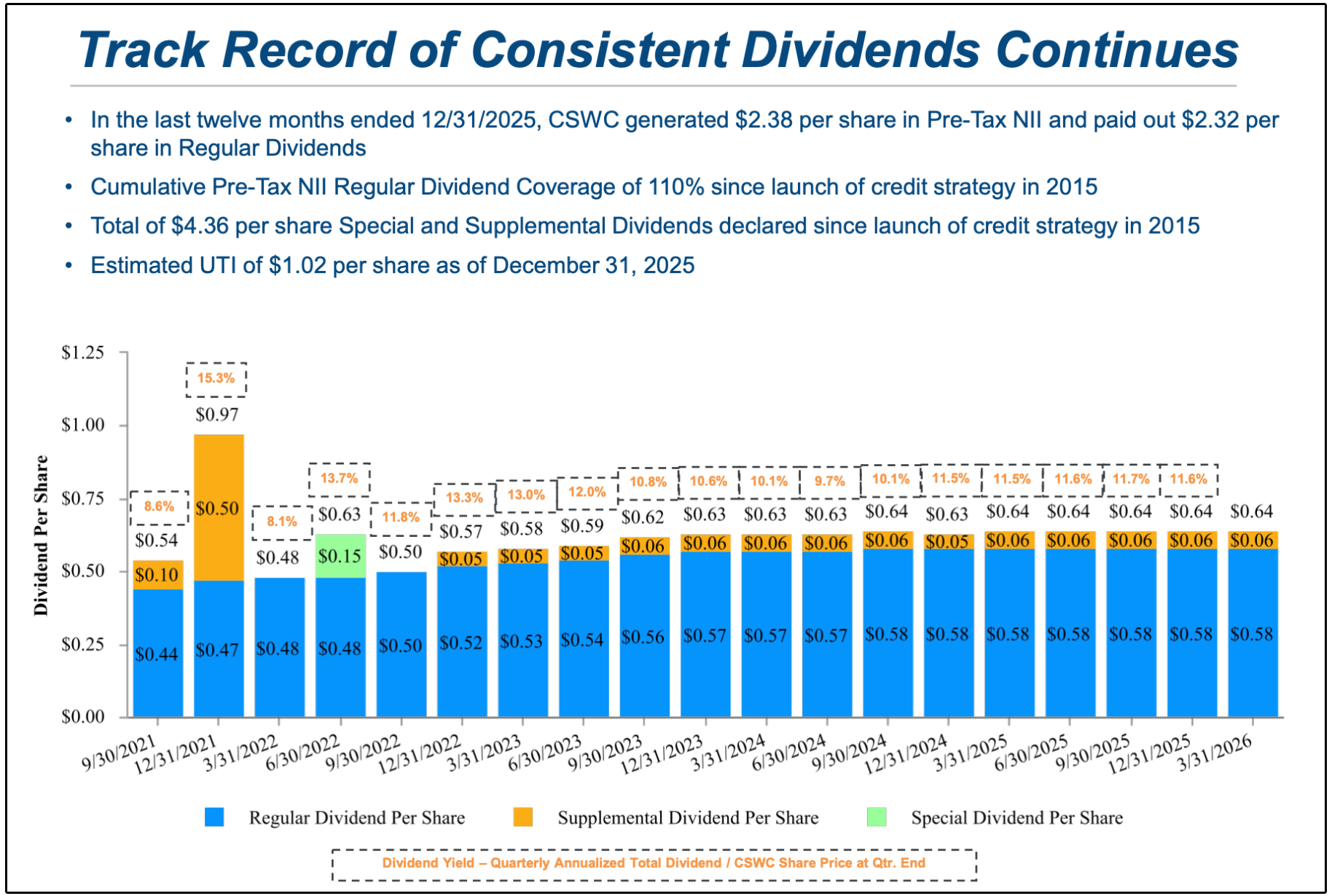

💼 Capital Southwest (CSWC)

Total Yield: 10.67% | Base Dividend Coverage: 101.7%

CSWC is one of the best internally managed BDCs in the market, and it has earned its premium valuation for a reason.

The portfolio is now approximately $2.1B, with the credit book 99% first-lien senior secured debt.

In other words, they are near the front of the line to get paid back (senior), the loan is backed by collateral (secured), such as assets of the company, they have the first claim on that collateral if the borrower gets into trouble (first lien).

A few key numbers stand out:

$0.59/share in quarterly pre-tax NII vs. $0.58 regular dividend

$2.39/share in LTM pre-tax NII vs. $2.32 regular dividends

$1.07/share in undistributed taxable income

Non-accruals at just 1.1% of fair value

Average debt investment hold size of just 0.9%

They clearly have a history of paying and maintaining large dividends.

But the last point made above is potentially just as important.

CSWC’s portfolio is very granular, meaning no single position is likely to make or break the company.

Management also notes that 88% of debt investments are currently rated a “1” or “2,” which means the overwhelming majority of the credit book is still performing well.

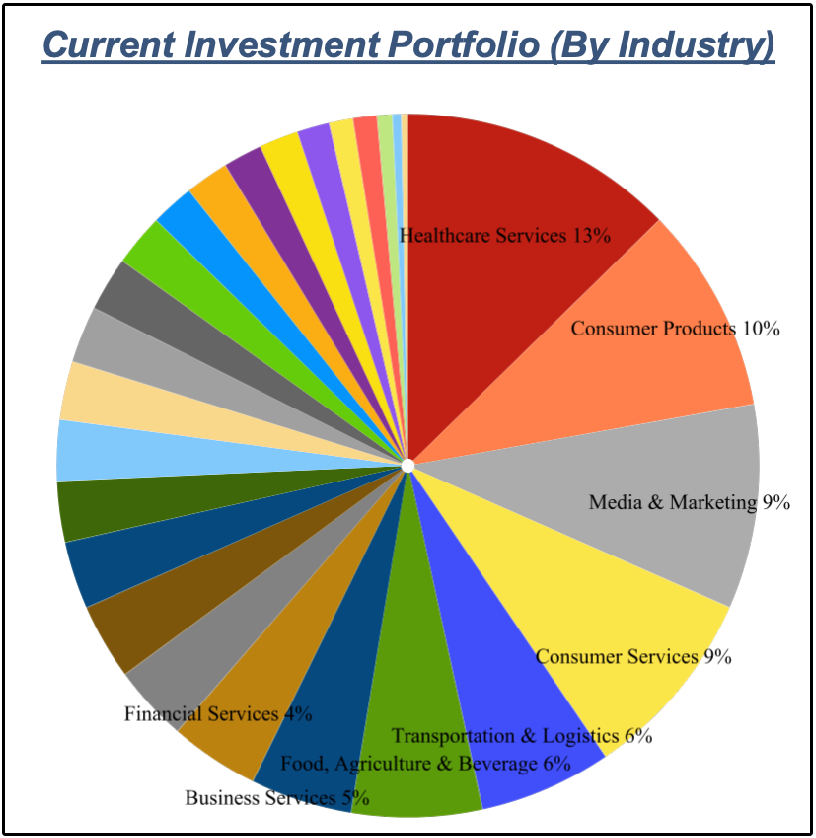

The other thing I like is the low software exposure.

CSWC’s largest industry exposures are healthcare services, consumer services, media & marketing, consumer products, food/agriculture/beverage, transportation & logistics, and business services.

Software is not a top portfolio category.

This makes CSWC very different from some BDCs that have large exposure to private software companies, where investors are increasingly worried about AI disruption, valuation resets, and weaker exits.

Of course, the market has recognized this to some degree, which is why they trade at more a premium valuation relative to the other BDCs in the Dividendology Database.

After climbing almost 7% year to date, CSWC trades at roughly 1.44x price to tangible book value per share.

However, that premium is not crazy for a high-quality internally managed BDC, but it does mean investors are paying up for quality-

Especially as most BDCs are down double digits this year.

So CSWC checks almost every box from a credit quality perspective: strong dividend coverage, first-lien-heavy portfolio, low non-accruals, low software exposure, meaningful spillover income, and a long record of supplemental dividends.

The only real question is whether the premium valuation gives you enough margin of safety.

🧩 Accumulation Phase

With this shift towards a ‘higher rates for longer’ phase-

I think we are finally entering into an accumulation phase for BDCs.

However, I must warn you.

The BDC market is still a landmine right now.

It is just like the old game minesweeper.

If you go around randomly selecting BDCs, you are basically guaranteed to hit a mine.

In the coming weeks/months, we will be taking a closer look in the BDC market, to see if we can potentially find some high yield gems to add to the High Yield Portfolio.

As a reminder, be sure to take advantage of the BDC Database, which is available to members of Dividendology.

This is typically updated a couple of times a month, and I plan on adding new features to it such as software exposure to continue to enhance the experience.

I’m obsessed with providing as much value as possible, and will continue to aim to do exactly that.

If you want to get access to it, as well as all other features mentioned below, then you can join here:

See you soon!

Dividendology

I have owned CWSC for over a year snd it is doing well, I wish I would have bought more.