👑 This Option Income ETF is Different!

High Monthly Income With Historical Outperformance? 📊

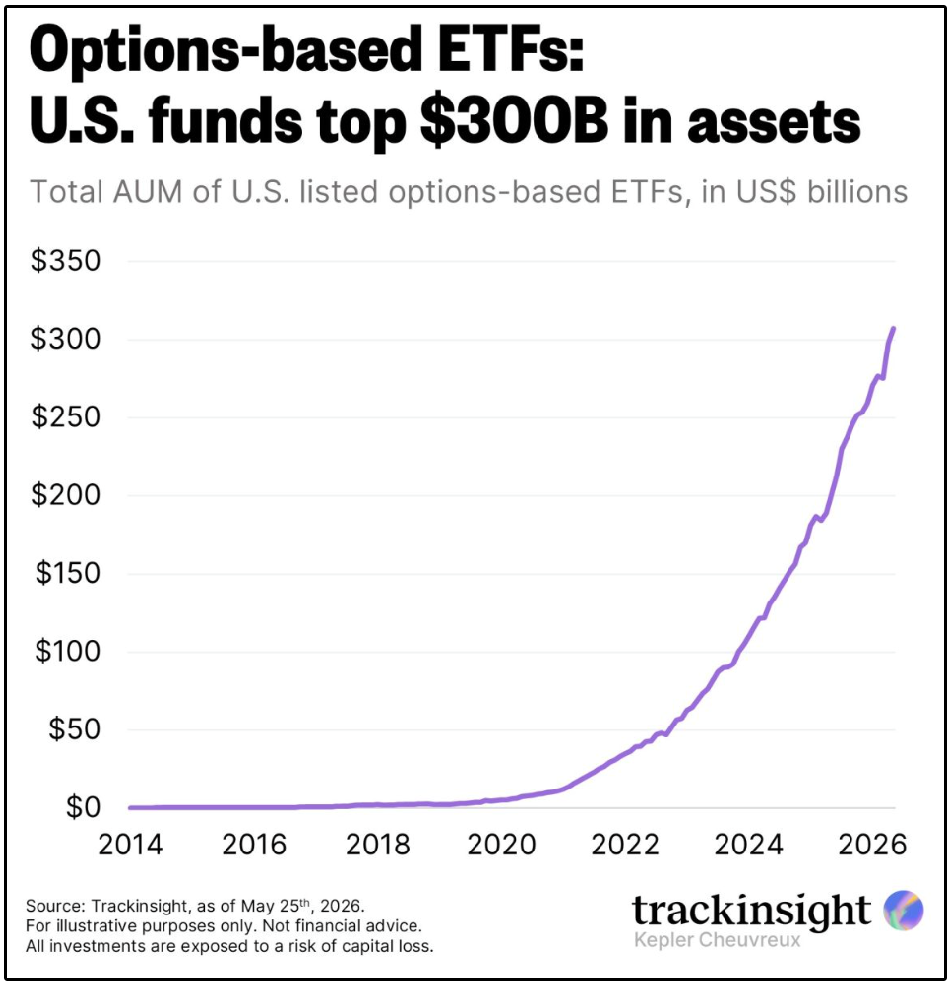

Options based ETFs have now gone from under $10B in assets under management in 2020, to over $300B in 2026.

That is a 30x increase!

Of course, a large portion of this growth is coming from ‘option income ETFs’.

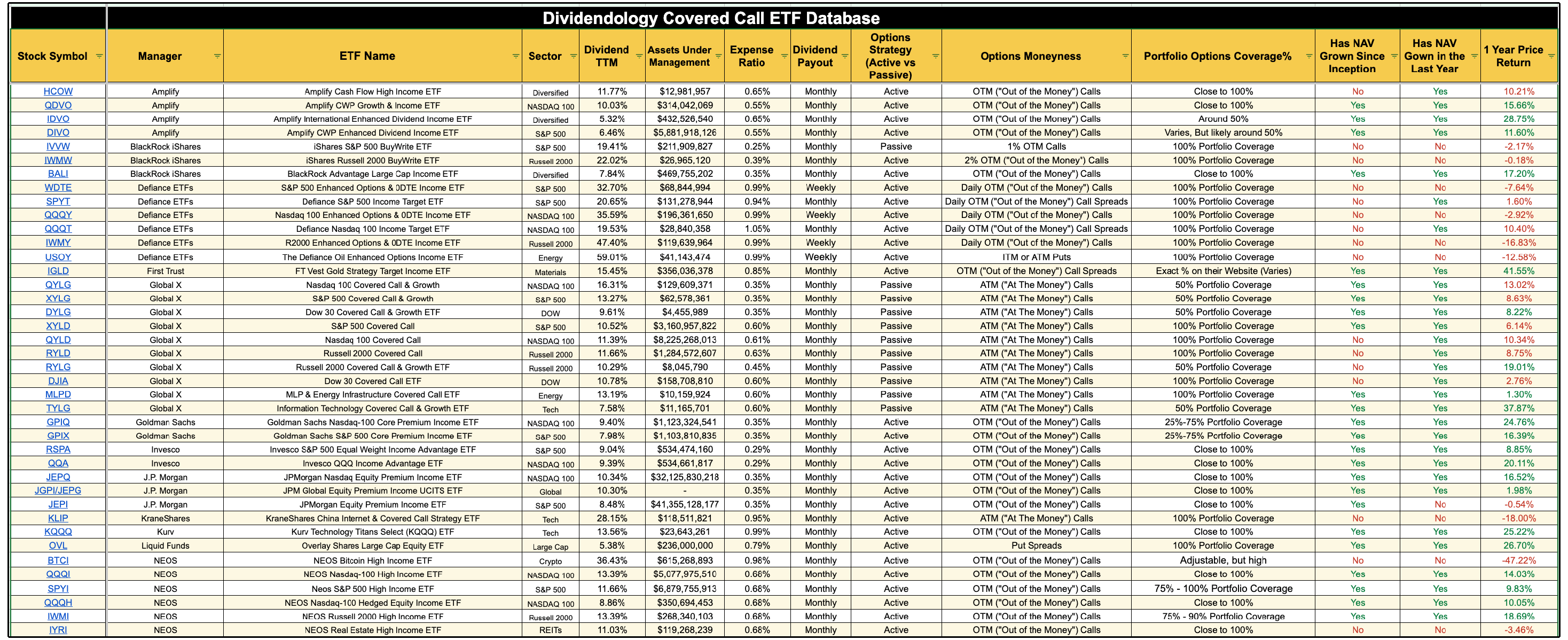

In fact, over the last few years, I’ve been building out an in-depth database on Option Income ETFs.

To better understand how OVL compares within the broader option-income ETF landscape, it is helpful to look at the types of funds currently available in the market.

The excerpt below is a sample from the Dividendology Database, which tracks a wide range of option-income ETFs and their characteristics.

Here’s what we believe is the unfortunate reality about the vast majority of these funds:

They are designed by nature to underperform their underlying holdings.

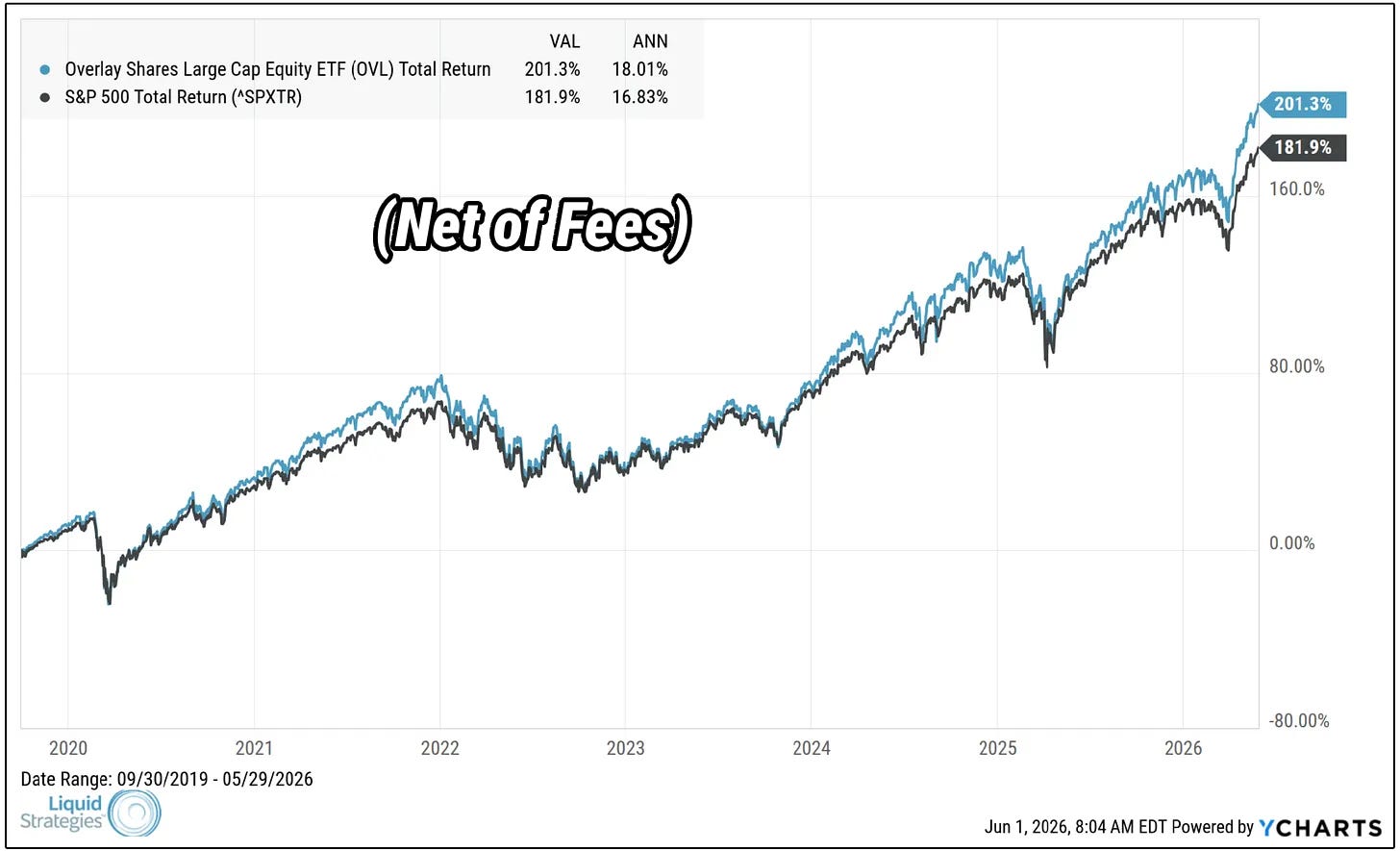

However, I actually recently added a fund to the database that, based on historical total return data since its inception in 2019, has outperformed the S&P 500. Of course, past performance does not guarantee future results.

And today, we’re taking a deep dive into it.

Disclosure: This newsletter is sponsored by Liquid Strategies, LLC, the investment adviser to OVL. Dividendology has been compensated in cash for this content. Dividendology is not a client of Liquid Strategies and has a material conflict of interest in recommending OVL due to the compensation received. The opinions expressed are those of Dividendology and not of Liquid Strategies. Past performance is not indicative of future results.

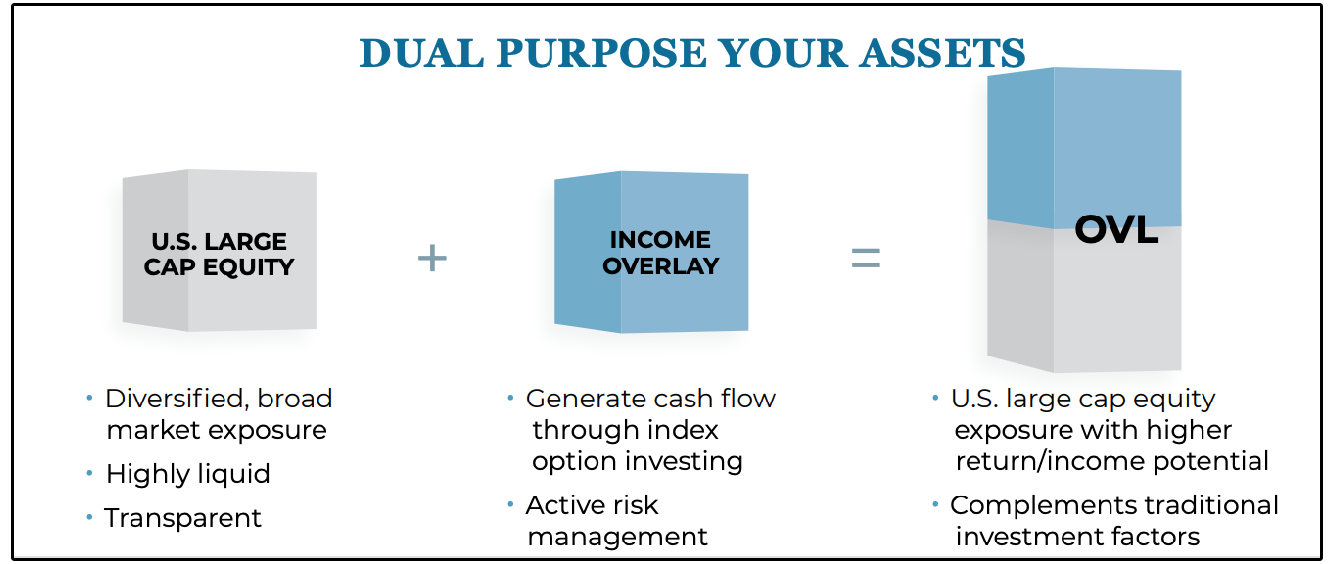

🧩 Overlay Shares Large Cap Equity ETF (OVL)

The Overlay Shares Large Cap Equity ETF (the “Fund”) seeks total return.

OVL combines passive large-cap equity exposure with an actively managed, risk-controlled put-selling options overlay designed to generate additional income-

And the current distribution rate is approximately 10.29% (as of May 31, 2026), paid monthly, with an SEC yield of 0.29% as of 5/31/26.

The distribution rate is not a measure of total return or yield. Distributions may include return of capital, which should not be confused with investment income. The fund's distribution policy may change at any time.

Performance shown is total return since fund inception (September 2019) through 5/29/2026. The S&P 500 Total Return Index is shown for comparison purposes only and is an unmanaged index that cannot be invested in directly. OVL’s strategy, risk profile, and holdings differ materially from the S&P 500. Past performance does not guarantee future results. Standardized performance and current month-end returns are available at https://lsfunds.com/etfs/ovl

The fund currently has a five star Morningstar rating. (Overall rating based on risk-adjusted returns among 85 funds in the Derivative Income category as of 5/31/26. See morningstar.com for more details.

But what makes OVL especially interesting is not just the income.

It is the fact that, based on historical data since the fund’s inception in 2019, OVL has actually outperformed the S&P 500 on a total return basis.

Naturally, we should ask how the fund is structured to understand how this performance was achieved, and what factors may influence future results.

💼 Why the Reported Yield Can Look Misleading

If you currently look at the training twelve month distribution rate for OVL on softwares like Seeking Alpha, you’ll notice it shows approximately 6.31% as of 6/10/2026.

Why is that the case?

This is strictly because OVL recently changed its distribution policy.

I recently interviewed the fund’s Head of Advisor Solutions, Eric McArdle, and he stated this:

The team has historically focused on total return as we can see from their website, but recently updated the distribution policy by moving to monthly payments and distributing a greater portion of the fund’s option premium and realized gains, rather than retaining those amounts within the fund. - Eric McArdle

Distribution amounts and frequency may change at any time at the adviser's discretion.

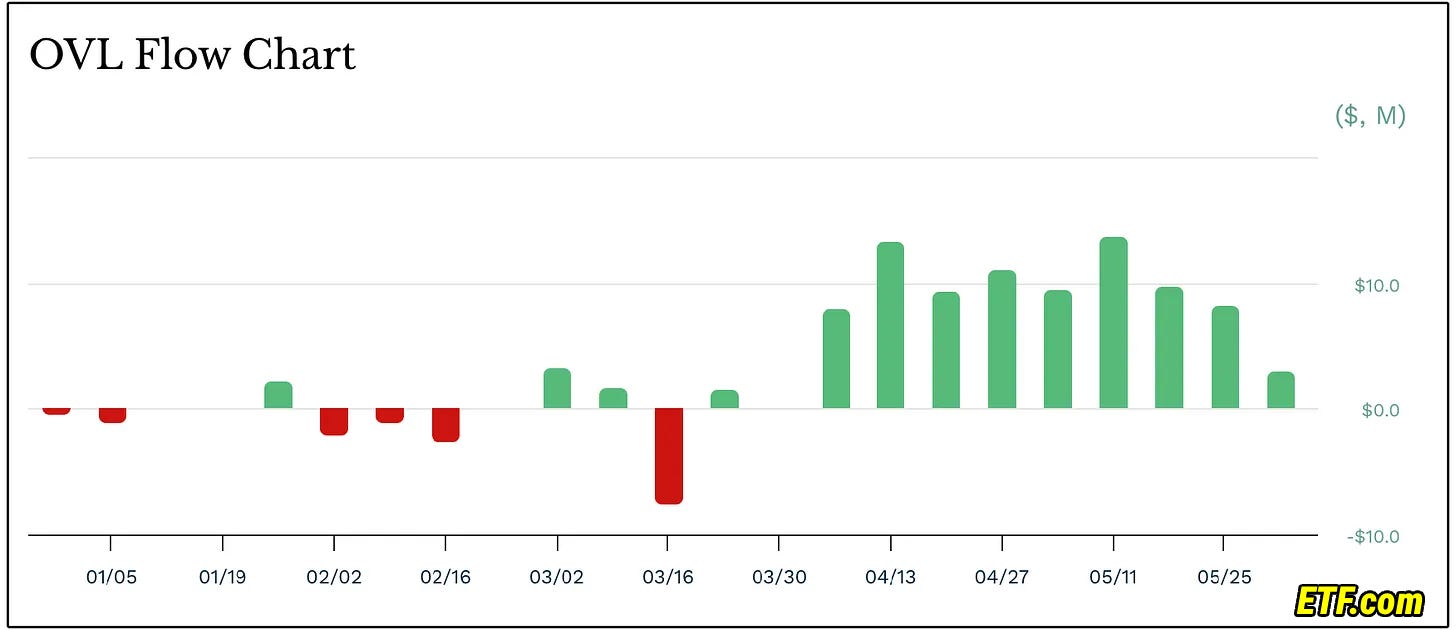

Since the distribution policy update, the fund has seen 10 consecutive weeks of net inflows, meaning investor purchases of fund shares exceeded investor withdrawals during each week.

🔍 How OVL Is Different

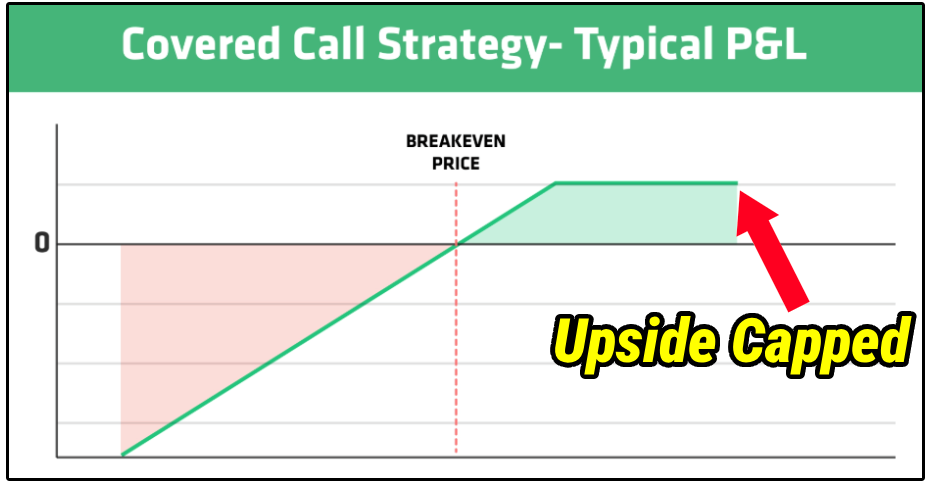

Most option-income ETFs generate cash flow by selling covered calls.

The basic idea is relatively simple:

The fund owns stocks and sells call options against those stocks or an index.

In exchange, the fund collects option premium.

The problem is that selling covered calls (options sold against stocks already owned by the fund) usually caps upside.

If the market rises sharply, the fund may not fully participate because it sold away part of that upside.

This is the main reason many covered call ETFs underperform their underlying index over long periods of time.

OVL uses a different approach.

Instead of relying on covered calls, OVL starts with passive exposure to the U.S. large-cap equity market, typically through holdings that may include broad-market ETFs through holdings that may include broad-market ETFs such as Vanguard's S&P 500 ETF (VOO), which represented 100.19% of OVL's portfolio as of June 18, 2026.

So investors still get broad market equity exposure.

Then, on top of that equity exposure, the fund runs a short-term laddered put spread strategy on the S&P 500, using multiple put spread positions that expire at different times and are regularly replaced as they mature.

In a simplified example, if the market is trading at 100, the fund may sell a put option slightly below that level and buy another put option further below as a hedge.

The premium collected from selling the higher-strike put is greater than the cost of buying the lower-strike put.

That creates a net premium.

The fund then continuously recycles these positions every couple of weeks.

This type of strategy can generate income when the market is up, flat, or even modestly down.

The key difference is that OVL is selling puts instead of calls.

That means the fund is not directly capping its upside in the same way many covered call ETFs do.

However, the put spread strategy does carry downside risk. In sharp market declines, losses on the put spreads can partially offset equity gains. No options strategy eliminates market risk.

It helps explain how OVL has been able to generate meaningful income while still participating in equity market upside.

🛡️ Is the Distribution Sustainable?

For income investors, the most important question should not just be how high the yield is.

The real question is whether the income is sustainable-

Which is where many high-yield option-income ETFs struggle.

A fund can always create a high distribution rate in the short term.

But maintaining that distribution while also preserving NAV and delivering strong total returns is much harder.

According to Liquid Strategies, OVL’s goal is not to maximize income at the expense of everything else.

Instead, the fund seeks to provide a combination of high current income and strong total return.

In a prolonged down market, the team has said their goal would be to prioritize consistency and avoid cutting distributions every time the market pulls back.

However, there is no guarantee that distributions will remain at current levels.

Distribution amounts are determined by the adviser and may be adjusted based on market conditions and fund performance.

The idea is that as markets recover, the NAV can recover as well, and the option strategy has the potential to continue compounding over time.

This makes sense, of course, because the S&P 500 has historically climbed higher over the long term, though past performance is no indicative of future results.

Past performance is no guarantee of future results. Index performance is not illustrative of fund performance. One cannot invest directly in an index.

🎙️ Interview with Eric McArdle

Members of Dividendology have access to the ETF Database, where I post interviews with fund managers, and you can see my interview with Eric McArdle from Liquid Strategies there.

If you’d like to get a more in-depth look at the fund, you can do so by watching this video:

I’ll be doing another interview with Eric in the future, so if you have any questions you’d like for me to ask, reply to this email and let me know!

If you want to get access to the Dividendology Database, you can do so here:

That’s all for now.

See you soon!

Dividendology