📊 The Top High Yield Dividend Stocks!

Generate 10%+ Yields Sustainably 💰

High Yield Investing does NOT always equal high risk.

In reality, a stock or fund’s dividend yield tells us nothing about the sustainability of the dividend.

It’s always about the fundamentals.

The issue with this?

The vast majority of investors have no idea how to assess the dividend sustainability of high yielding assets.

Today, we will be reviewing the 5 major high yield asset classes, and how to analyze them for dividend sustainability

And on Friday-

We will be adding a stock yielding 9% to the High Yield Portfolio.

⚠️ 2 Major Issues…

When I look at the high yield investing space, I see two major issues:

Lack of knowledge on how to analyze High Yield assets

Lack of data on these assets

Not only do investors not know how to analyze these assets, traditional softwares don’t provide the necessary data to analyze them.

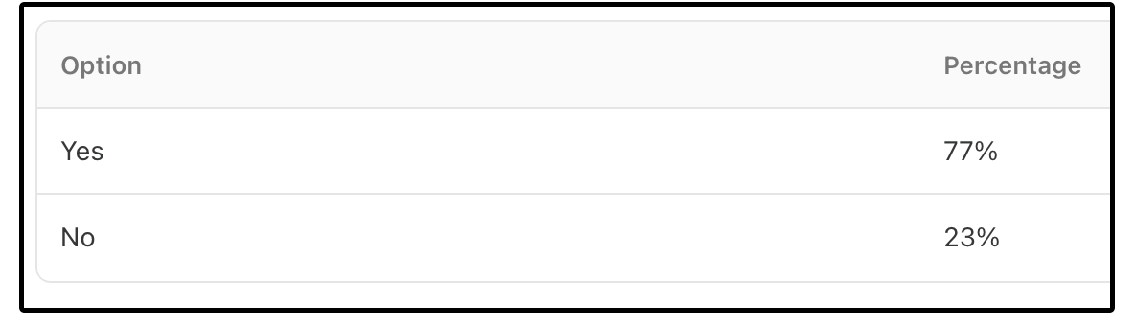

Despite this I ran a poll last month asking if my subscribers owned any of these asset classes, and 77% of you said you did!

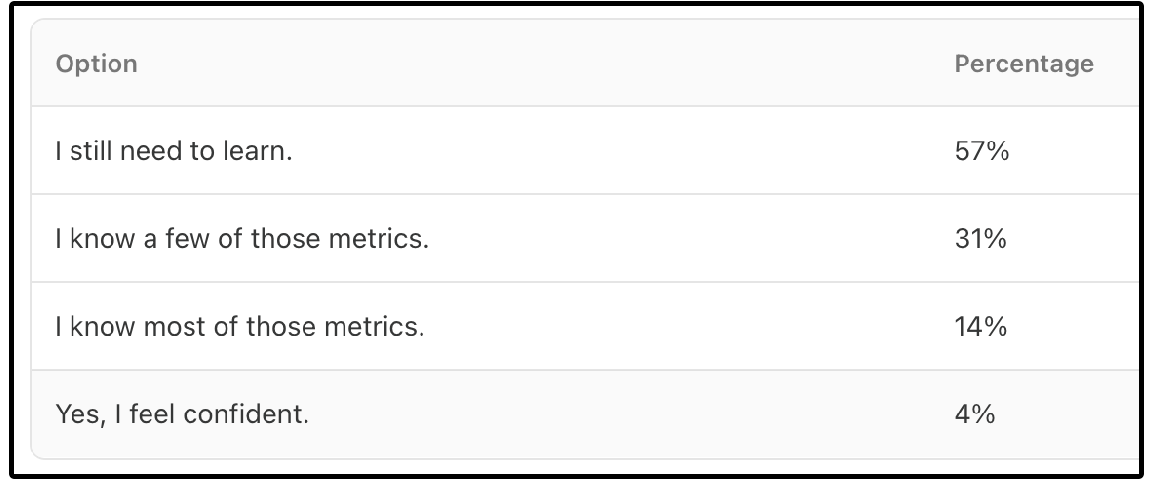

What was even more shocking were the results from when I asked if you had a general understanding of how to analyze the alternative income assets classes…

77% of the people who took the survey stated they owned these asset classes-

But only 4% felt confident in how to analyze the key metrics for these asset classes!

Today, we will be solving both of these problems.

There are 5 main asset classes that typically have high yields:

💰 Covered Call ETFs

🛢️ MLPs (Master Limited Partnerships)

🏢 REITs (Real Estate Investment Trusts)

💼 BDCs (Business Development Companies)

🧾 Preferred Shares

The way we analyze the dividend sustainability for each of them is different.

Let’s look at an example of each.

1. 💰 Covered Call ETFs

Example: ICAP - Infrastructure Capital Equity Income Fund ETF

ICAP currently yields 8.54%.

But many high-yield ETFs are just slowly liquidating themselves.

Here’s why that’s dangerous:

Shrinking Net Asset Value → fewer assets to write call options → lower premiums → dividend cuts

ICAP only writes options on around 30% - 40% of their portfolio.

Because of this, ICAP’s net asset value has held up well (and even grown), which tells us:

Its yield is more sustainable

It’s not eroding capital just to fund distributions

Softwares don’t provide data on things like portfolio options coverage and options moneyness, making covered call ETFs incredibly difficult tom analyze.

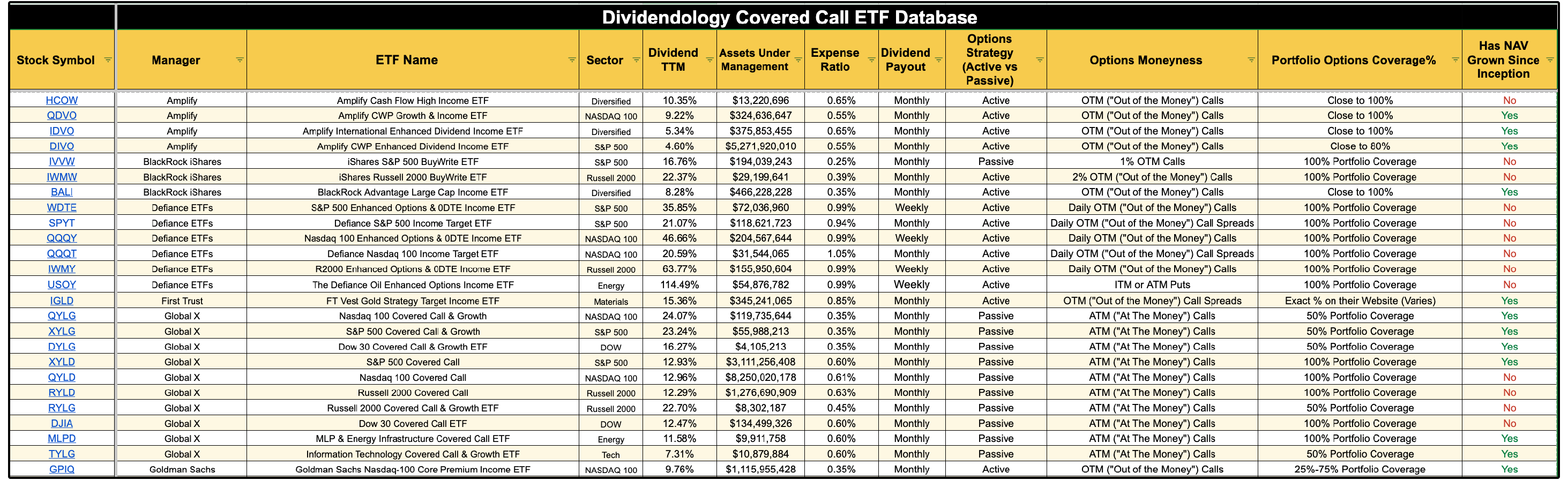

This is why we built the Dividendology Covered Call ETF Database.

It provides data on things like:

Portfolio options coverage

Options moneyness

NAV since inception

This provides us much of the information we need to assess dividend sustainability for covered call ETFs.

If you want to learn more about ICAP, you can do so here.

2. 🛢️ MLPs (Master Limited Partnerships)

Example: MPLX - MPLX LP Common Units

Have you heard of MPLX?

MPLX is a midstream energy partnership formed by Marathon Petroleum in 2012.

It operates pipelines, terminals, and storage across major U.S. basins, focusing on crude oil, refined products, natural gas, and NGLs.

MPLX generates stable cash flow through long-term, fee-based contracts.

A few things you need to know about MPLX:

MPLX’s business model is highly defensive, generating stable, long-term contracted cash flows through its midstream operations.

These contracts provide strong insulation from commodity price volatility.

The balance sheet is solid, with a 3.4x leverage ratio and a BBB credit rating.

But what about the dividend?

MPLX is currently yielding 7.86%

They have a 10 year dividend compounded annual growth rate of 8.77% (Wow!)

But how do we assess the dividend sustainability of MPLX and Master Limited Partnerships?

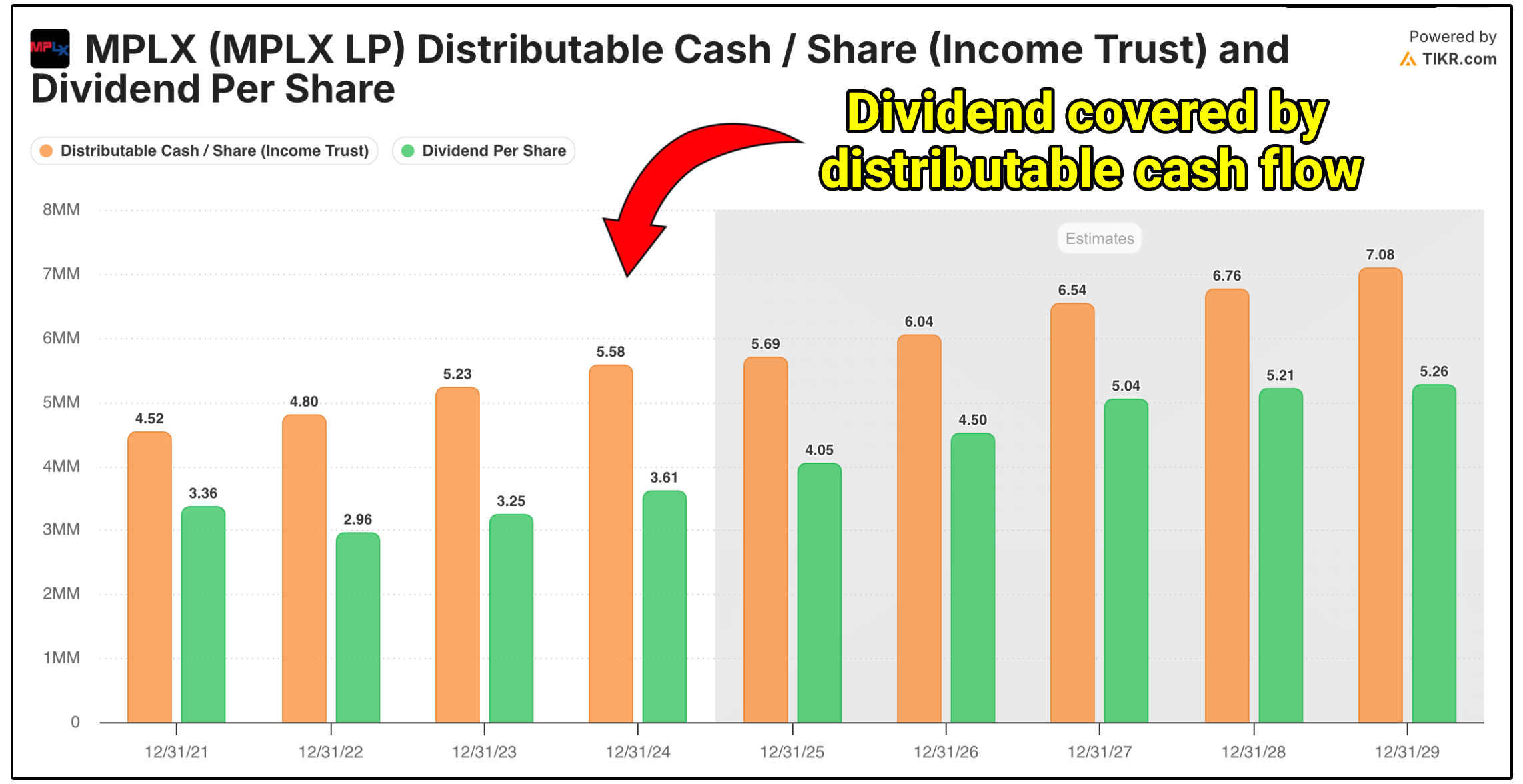

We look at the distributable cash flow (DCF) coverage ratio.

Formula: DCF Coverage Ratio = Distributable Cash Flow / Distributions PaidWhat to look for:

>1.2x = Comfortable cushion

<1.0x = Red flag; they’re paying more than they generate

The MPLX dividend is well-covered by distributable cash flow, with a current coverage ratio of 1.5x

On top of this, management made this statement in a recent earnings report:

We see a period of time where 12.5% is very doable. It’s tough to give you an extremely long horizon, but we certainly are trying to convey to you that distribution growth at 12.5% has the potential...to be durable for a period of time.

Not only do they expect their large payouts to be sustainable, they expect to grow them at a 12.5% annual growth rate!

An amazing combination of yield with dividend growth.

3. 🏢 REITs (Real Estate Investment Trusts)

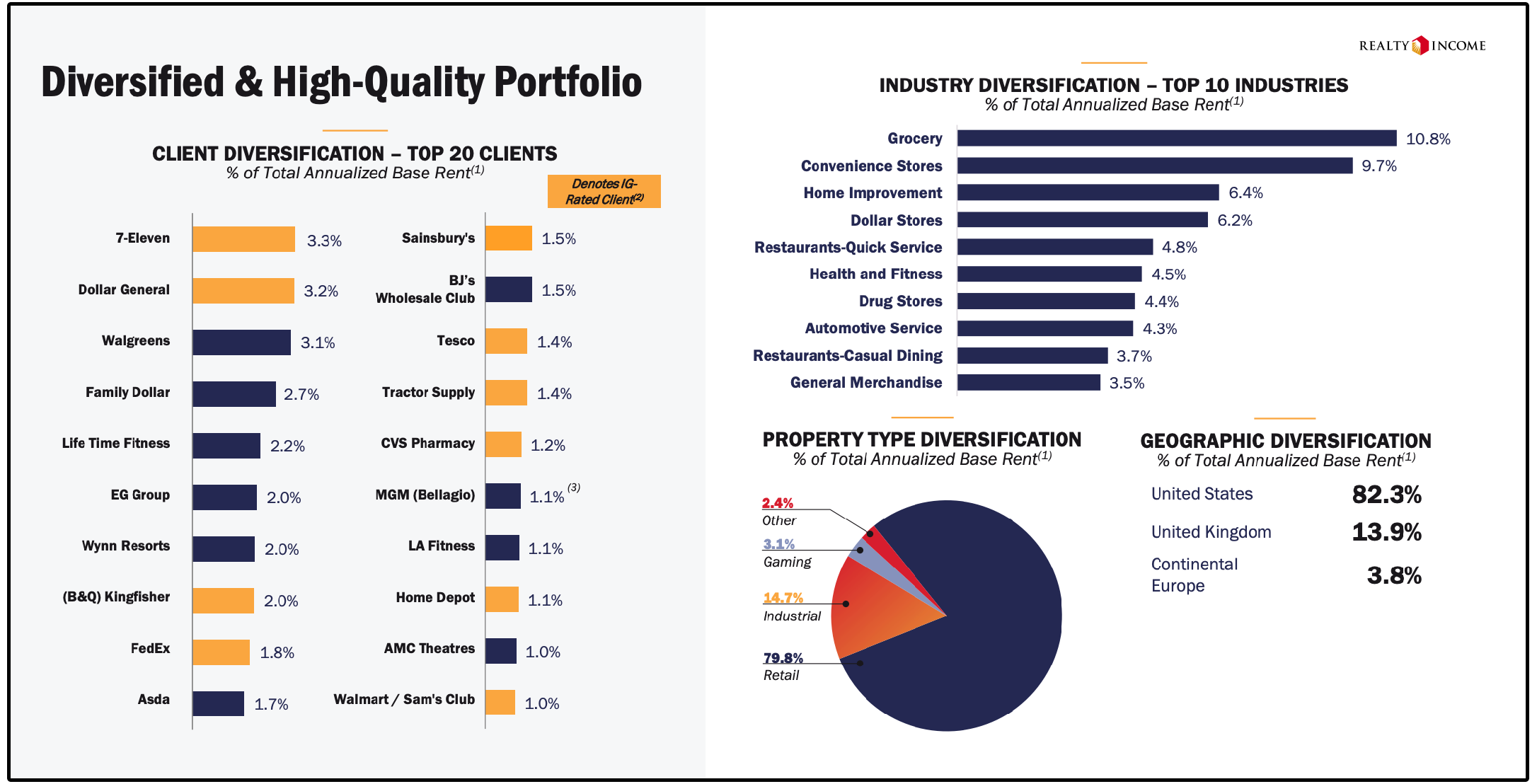

Example: O - Realty Income Corporation

Realty Income makes money by owning and leasing single-tenant, net-lease commercial properties to some of the strongest retailers and service businesses in the world.

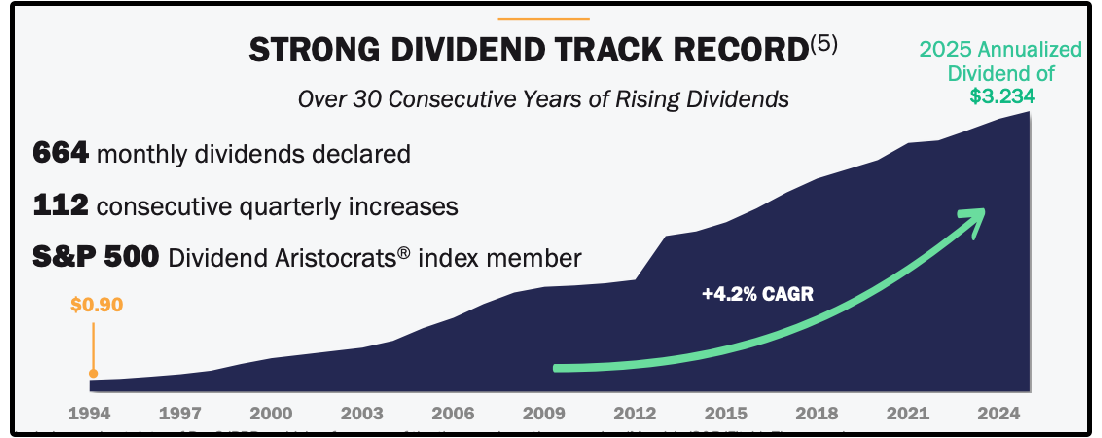

The company is known as “The Monthly Dividend Company” because it generates highly predictable rental income from long-term leases-

Most of which are triple-net leases, meaning tenants pay property taxes, insurance, and maintenance.

Here are a few key things to know about Realty Income:

Realty Income has grown AFFO per share consistently over time, supported by disciplined acquisitions and contractual rent escalators

The majority of Realty Income’s debt is fixed-rate and long-dated, which significantly reduces interest-rate risk compared to many REIT peers

•The company currently yields 5.4%, with steady dividend growth of roughly 3–4% annually, supported by recurring cash flow

But how do we assess the dividend sustainability of Realty Income (and REITs in general)?

We don’t use the traditional payout ratio.

We don’t rely on free cash flow either.

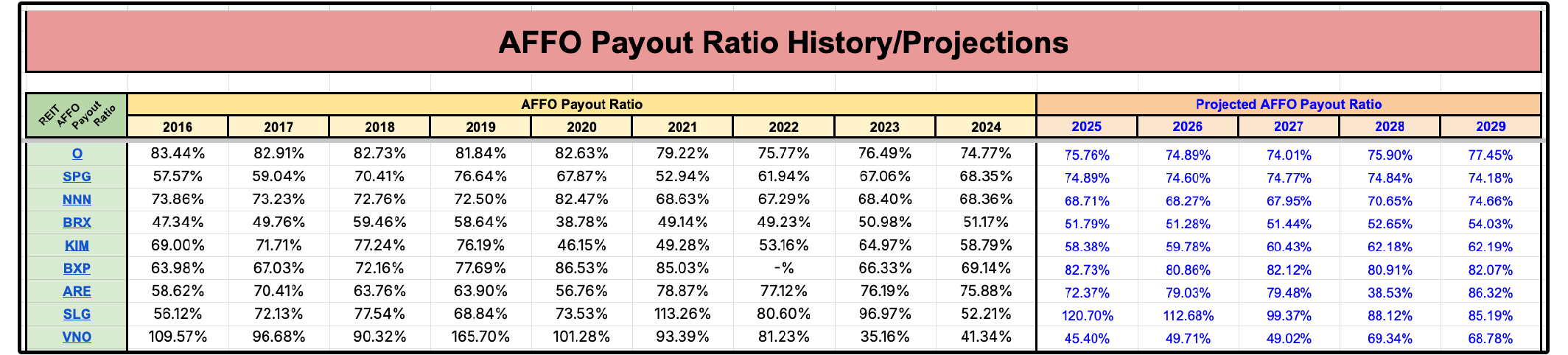

Instead, we look at AFFO (Adjusted Funds From Operations).

AFFO is the REIT equivalent of free cash flow and is the best measure of how much cash is truly available to pay dividends.

Formula: AFFO Payout Ratio = Dividend per share ÷ AFFO per shareHow to interpret AFFO payout ratios:

• Below 80% → Safe

• 80–90% → Occasionally Acceptable

• Above 90% → Riskier, less margin in downturns

We closely track historical AFFO payout ratios, as well as projected AFFO payout ratios in the Dividendology REIT Database.

Here is a small snippet from the database:

Realty Income currently has an AFFO payout ratio of roughly 75%, which places the dividend firmly in the safe and sustainable range.

4. 💼 BDCs (Business Development Companies)

Example: MAIN - Main Street Capital Corporation

Have you heard of MAIN?

Main Street Capital is a Business Development Company (BDC), which means they generate income by lending to small and mid-sized private businesses at high interest rates and collecting interest income, fees, and sometimes equity stakes in return.

Here’s a few things you need to know about MAIN:

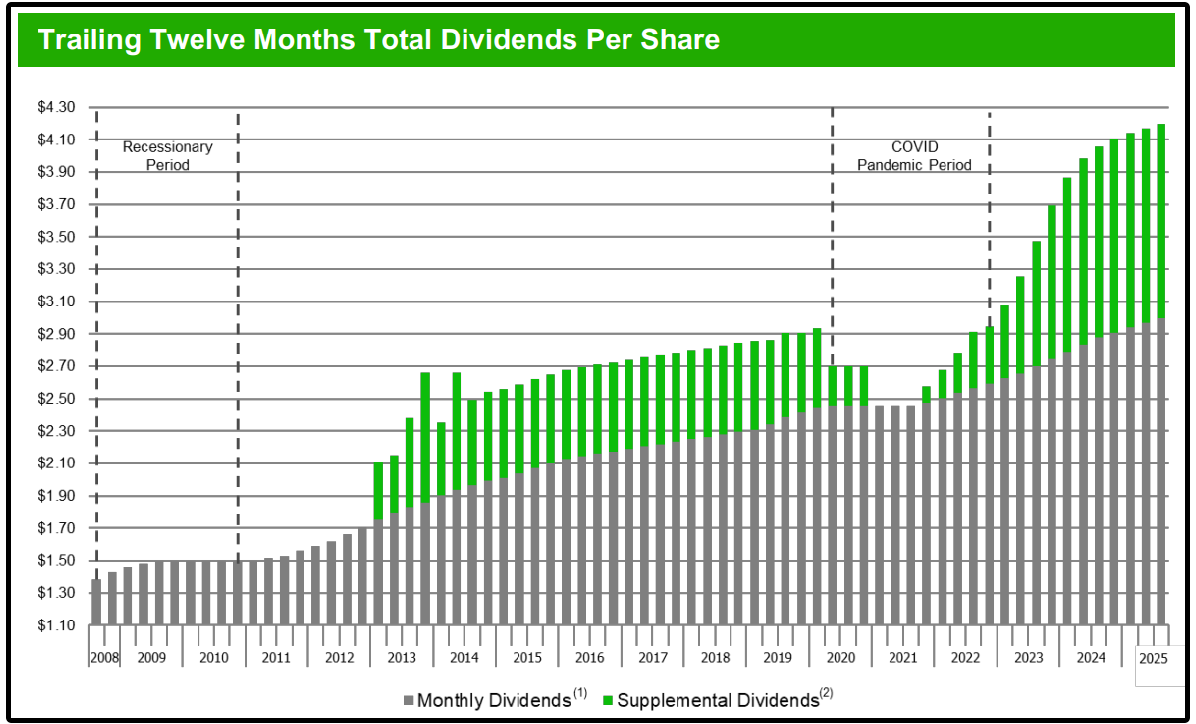

Pays monthly dividends + frequent special dividends

Never decreased its regular monthly dividend

Many loans are floating-rate, so higher rates = higher income = more special dividends

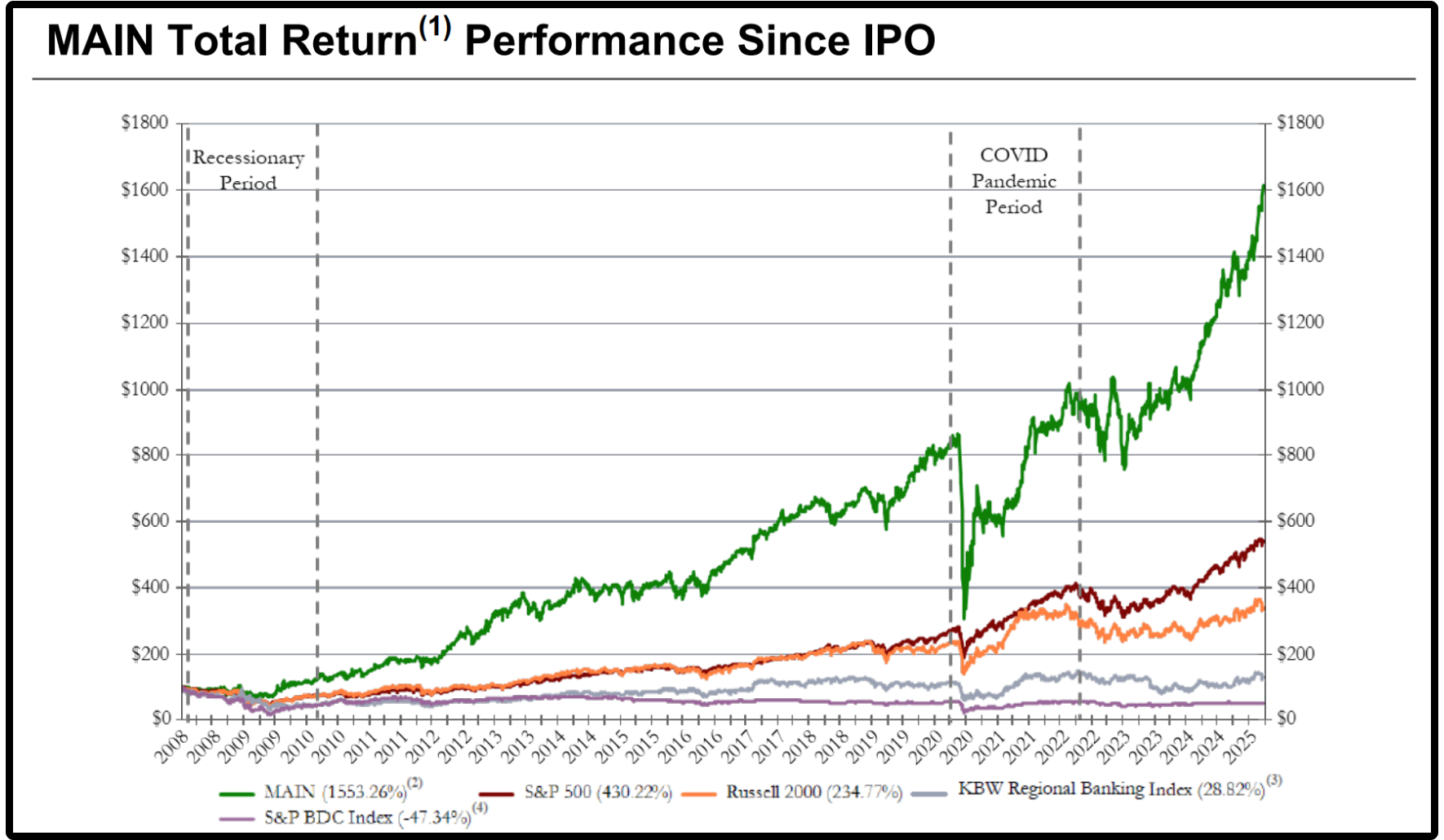

Since their IPO in 2008, they have a total return of 1,553%, vs the S&P BDC index sitting at -47.34%.

MAIN currently has a dividend yield of around 7%, with a 3 year dividend growth rate of over 5%.

But how do we assess the dividend sustainability of MAIN and Business Development Companies?

Really, there are 3 things we have to consider:

Dividend Coverage Ratio

Formula: Dividend Coverage Ratio = Net Investment Income (NII) / Dividends PaidTarget:

>1.0x = Covered

<1.0x = Risky

MAIN has a dividend coverage ratio of 1.34

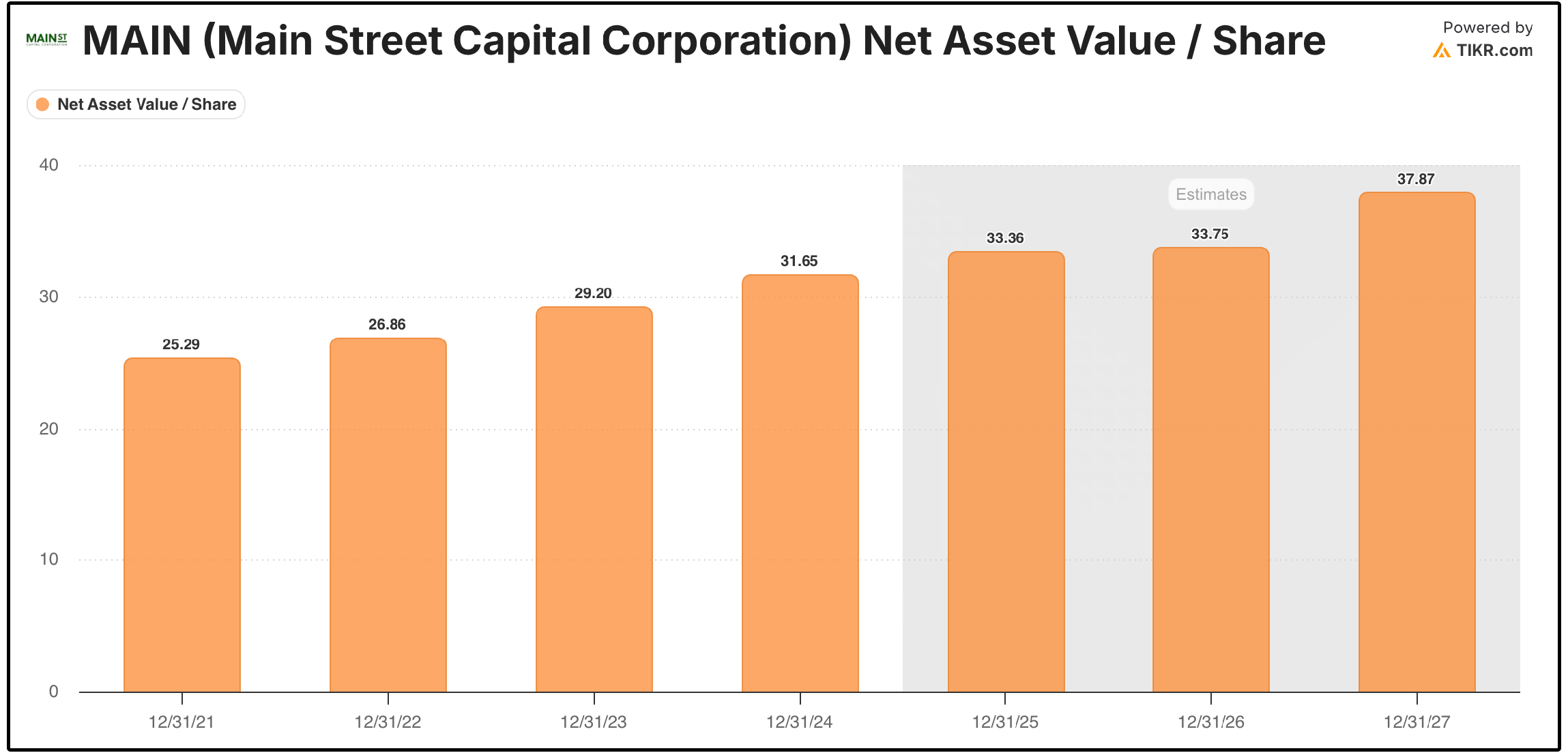

NAV Per Share

NAV (Net Asset Value) represents the per-share value of a BDC’s assets minus liabilities.

A BDC paying more in dividends than it earns can erode its NAV, which is a clear warning sign.

A rising NAV per share indicates that payouts are backed by real income, not unsustainable practices.

The strongest BDCs steadily grow NAV per share, which signals a sustainable dividend with the potential to grow.

Main Street Capital recently reported they expect record net asset value per share for the eleventh consecutive quarter.

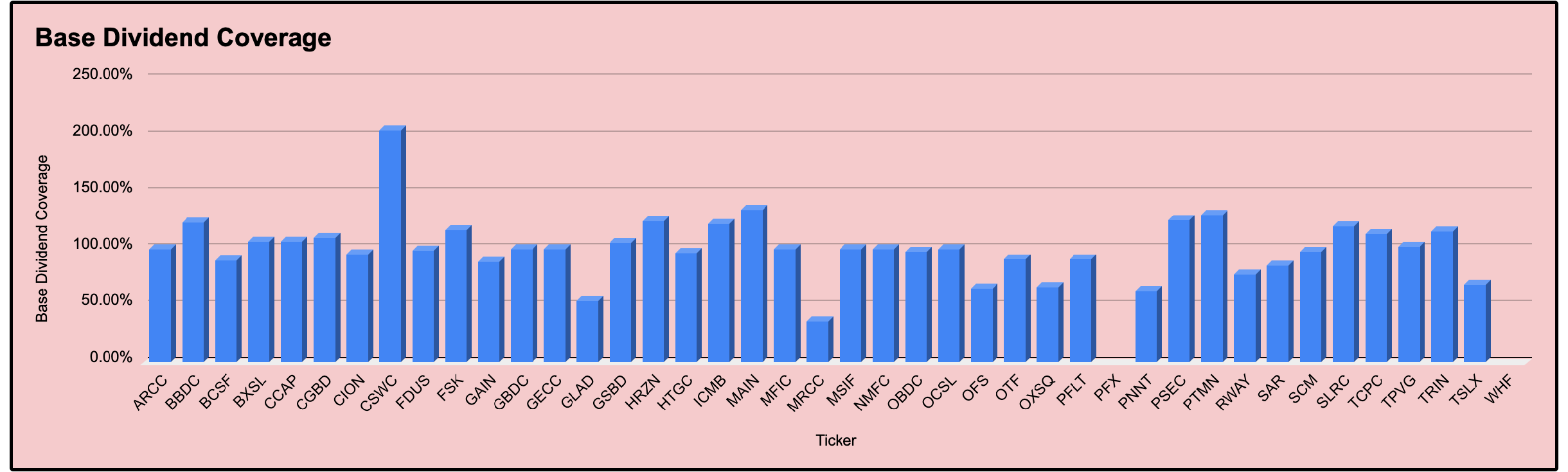

Base Dividend vs Total Dividend

As I’ve been building out the BDC Database, I’ve come to notice that nearly every single software lists the incorrect yield for BDCs.

Why is this?

Because BDCs technically have 2 yields:

Base Dividend Yield

Total Dividend Yield

The base yield is the yield we should (hypothetically) be guaranteed to get.

Anything above that is considered “special dividends” that depends on how much extra income a BDC is generating in the moment.

Here is Main Street Capital’s dividends paid, as well as special dividends in green.

The base dividend coverage tells us how sustainable those base dividend payments are, NOT how sustainable the total dividends are

We track these metrics very closely with the Dividendology BDC Database.

5. 🧾 Preferred Shares

Example: PFFA - Virtus InfraCap U.S. Preferred Stock ETF

Have you heard of PFFA?

To be fair, I cheated on this one just a bit.

PFFA isn’t a preferred stock, but is an actively managed ETF that invests in U.S. preferred stocks.

Here’s what you need to know about preferred shares:

They oftentimes offer way higher dividend yields compared to common stock

Preferred shares are higher in the capital stack than common stock but lower than debt (in a bankruptcy, debt holders are paid first, then preferred shareholders, then common shareholders)

They generally have less price volatility than common stock but offer limited upside.

And here’s what you need to know about PFFA:

The fund currently yields around 9.35%, with monthly income payouts

It invests primarily in preferred stocks from high-quality issuers, many of which are investment-grade.

As an ETF, it provides built-in diversification, which helps reduce the risk of any one issuer defaulting.

But how do we assess the dividend sustainability of PFFA and Preferred Shares?

Dividend sustainability for preferred shares isn’t too different from a typical stock.

Look for the dividend coverage (payout ratio) of the underlying holdings, the credit quality of the underlying stock, and look for the underlying holding to grow earnings and free cash flow.

Preferred stocks may not offer as much upside as common stocks, but funds like PFFA offer high, consistent yield with lower volatility.

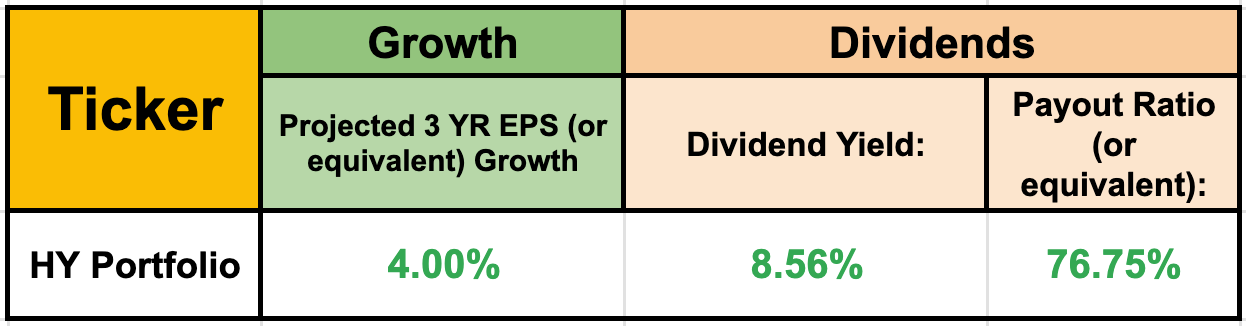

🏆 Our High Yield Portfolio

On Friday, we will be adding a new position to our High Yield Portfolio that yields near 9%.

As of right now, our portfolio is yielding a sustainable 8.56%, with improving underlying fundamentals.

As a reminder, members of Dividendology can view the High yield Portfolio at anytime here, and can also get access to the Dividendology Database.

If you want even more out of the community and access to all the features mentioned below, you can join here:

See you on Friday!

Dividendology 🚀

Hi, you put up a post on IG today about dollar cost averaging. For the high yield portfolio is there any plan to DCA positions that are in a deep value state like the REIT holding in the portfolio?

https://open.substack.com/pub/companycharts/p/the-best-high-yield-dividend-stocks?r=6kpr46&utm_medium=ios